The war in Iran has ignited the most significant global energy price shock in nearly two decades, forcing governments into costly new subsidies and complicating the path for central banks worldwide.

Back

The war in Iran has ignited the most significant global energy price shock in nearly two decades, forcing governments into costly new subsidies and complicating the path for central banks worldwide.

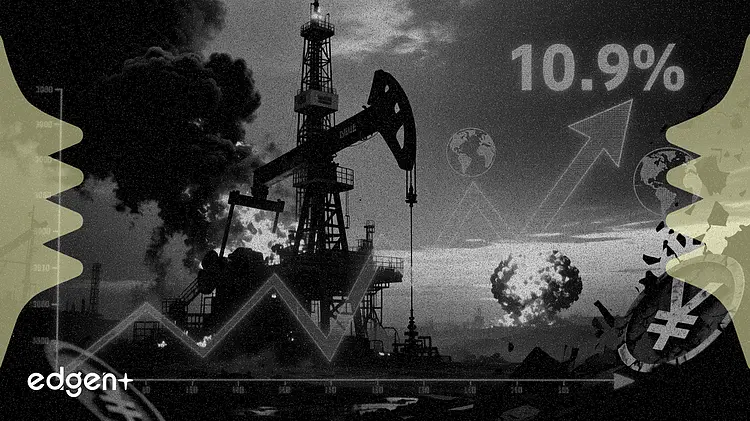

The escalating conflict in Iran triggered a massive 10.9% surge in the global energy index in March, pushing the U.S. consumer price index up 0.9% and fueling fears of a new wave of stagflation that threatens to derail a fragile economic recovery.

"The shock comes at a critical transition point, intensifying inflationary pressures and raising living costs for households," Nigeria's Finance Minister Wale Edun said in a statement, highlighting the severe impact on emerging markets.

The surge was driven by a record 21.2% jump in gasoline prices, the largest since 1967, after the conflict shut down the critical Strait of Hormuz shipping lane. The disruption sent Brent crude soaring above $110 a barrel, while U.S. natural gas futures topped $8.50/MMBtu. In response, the U.S. dollar index climbed 1.2% as investors sought safe-haven assets.

With the IMF and World Bank set to downgrade global growth forecasts, the energy crisis now forces a difficult choice on central banks: fight rampant inflation with aggressive rate hikes that could trigger a recession, or support growth and risk embedding higher prices for longer. The European Central Bank has already signaled that future rate decisions depend on the secondary effects of the oil shock.

Governments are scrambling to shield their economies from the fallout. Germany's coalition government unveiled a €1.6 billion package to cut fuel levies, with Chancellor Friedrich Merz stating, "This war is the real cause of the problems we are experiencing in our own country." Sweden followed suit, announcing $825 million in fuel tax cuts and electricity subsidies. The United Kingdom is also preparing support for businesses grappling with energy prices that have been uncompetitive for years. These fiscal responses, however, add to national debt piles already swollen by pandemic-era spending.

The strain is most acute in developing nations. Nigeria, an oil-producing country, has seen local petrol prices jump over 50% and diesel more than 70% since the conflict began on February 28. The nation is now seeking greater international support to manage the crisis, which threatens to undo recent economic stabilization efforts. The disruption to energy supplies represents the third major shock to the global economy in recent years, following the Covid-19 pandemic and Russia's invasion of Ukraine.

Beneath the headline numbers, a more complex picture emerges. While energy and transport costs are soaring, core inflation—which excludes volatile food and energy—rose a more contained 0.2% in the U.S., according to the Bureau of Labor Statistics. This divergence highlights a "two-speed" economy where resilient labor markets and spending by high-income households still support growth, even as consumer sentiment plummets. The LSEG/Ipsos Primary Consumer Sentiment Index fell a sharp 3.4 points to 50.0 in April, its lowest level in a year.

The Iran conflict is upending monetary policy globally. The Bank of Japan, once seen as likely to hike rates, is now backing away as the energy shock clouds the growth outlook. The last time oil prices saw a similar spike was in the lead-up to the 2008 global financial crisis, a historical parallel that weighs heavily on policymakers. The European Central Bank has made it clear that any further rate hikes will be contingent on how the energy price surge feeds into the broader economy, a process that remains highly uncertain.

This article is for informational purposes only and does not constitute investment advice.