AI의 미래: 소셜 데이터와 체인 내 인사이트가 더 현명한 투자에 기여하는 방식

AI가 거래 게임을 혁신하고 있다

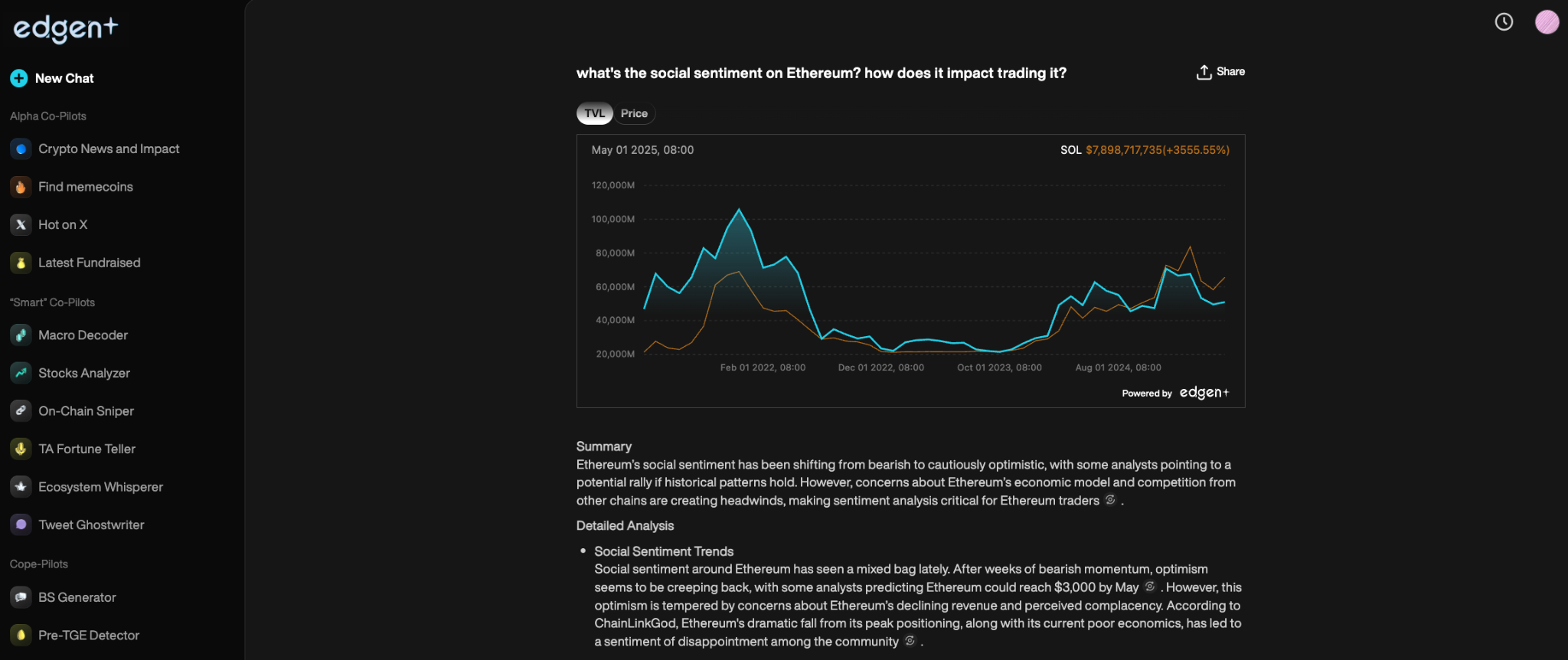

재정 시장은 더 이상 차트와 기초 분석에만 의존하지 않습니다. 소셜 미디어의 화제, 인플루언서의 의견 및 실시간 블록체인 활동이 자산 가격을 점점 더 형성하고 있습니다.

AI 기반 도구들인Edgen AI놀랄 정도로 빠른 속도로 대량의 데이터를 분석하여 트레이더에게 즉각적인 통찰력과 강력한 예측을 제공합니다. 이러한 도구를 사용하는 트레이더는 수동 분석에 의존하는 트레이더들보다 지속적으로 우수한 성과를 보입니다.

AI가 더 현명한 투자 전략을 만드는 방식

인공지능이 인간보다 시장 분석을 더 빠르게 수행한다

전통적인 방법은 현대 시장의 속도를 따라가지 못한다. 인간은 수십억 개의 데이터 포인트를 실시간으로 추적하고, 라이브 뉴스를 처리하며 시장 동향을 즉시 예측할 수 없다.

AI 기반 플랫폼은 다음과 같이 인간의 능력을 넘어섭니다:

- 실시간 대량 데이터를 빠르게 처리합니다.

- 소셜 미디어 신호와 블록체인 거래에서 시장 움직임 예측하기

- 자주 잘못된 거래 결정으로 이어지는 감정적 편견을 제거합니다.

이로 인해 실시간 데이터 기반 분석을 바탕으로 한 더 지능적인 투자 결정이 가능해집니다.

사회적 데이터 분석: 대화를 시장 통찰로 전환하기

사회 데이터 분석 이해

사회적 데이터 분석은 자산 가격에 영향을 미치는 온라인 대화, 감정 변화 및 등장하는 트렌드를 추적합니다. AI는 다음 소스를 빠르게 스캔합니다:

- 트위터/X: 인플루언서 대화, 소매 거래자 감정

- 금융 뉴스 및 블로그: 시장에 영향을 미치는 발표

- 체인 내 활동: 실시간 지갑 이동 및 블록체인 거래.

AI는 주류 시장이 인식하기 전에 트레이더가 추세를 감지할 수 있도록 합니다.

인공지능이 소셜 데이터를 실행 가능한 거래 신호로 전환하는 방법

엣지나 AI는 고급 머신러닝을 활용합니다, natural language processing (NLP)사회 데이터에서 핵심 패턴을 식별하기 위한 대규모 데이터 분석 및, 예를 들어:

- 긍정적인 감정 급등은 구매 기회에 대한 경고를 트리거합니다.

- 부정적 감정 성장은 가격 하락을 시사합니다.

- 영향력 있는 의견 변화는 추세 전환을 조기에 신호로 보낸다.

실시간 소셜 감정 분석은 거래자에게 핵심적인 타이밍 이점을 제공합니다.

감정 분석: 시장의 감정을 해독하다

감정 분석이란 무엇인가요?

감정 분석은 온라인 텍스트에서 인간의 감정과 태도를 해석하며, 시장 논의를 다음과 같이 분류합니다:

- 상승세(긍정적):확률적인 가격 상승을 나타냅니다.

- 비바람 (부정적):가격 하락을 시사합니다.

- 중립 (불확실):앞으로의 변동성을 시사합니다.

Edge AI는 동시에 수천 개의 온라인 대화를 분석하여 거래자에게 명확한 감정 인사이트를 제공하여 정보 기반 결정을 지원합니다.

How Edgen AI Enhances Trading with Sentiment Analysis

엣지엔 AI가 감성 분석을 통해 거래를 어떻게 향상시키는가

빠르게 소셜 논의를 스캔함으로써 Edgen AI는 트레이더에게 다음과 같은 것을 제공합니다:

- 가격이 급등하기 전에 시장의 열기를 인식하라.

- 하락 전에 부정적인 감정 변화를 식별하라.

- 온라인 활동의 사기 또는 인위적으로 과장된 활동을 탐지합니다.

거래자들이 사용하는 Edgen Feed실시간 감정, 등장하는 토큰 대화, 대중 예측 알파에 접근하여 실시간 우위를 확보하라.

대체 데이터: 다른 사람들이 놓친 시장 신호를 밝혀내다

전통적인 금융 지표와 기초 데이터는 부족하다. 트레이더들은 이제 독특한 거래 신호를 위해 대체 데이터 소스에 의존한다. EDGEN AI는 다음과 같은 대체 데이터를 모니터링한다:

- 체인 내 거래:공개되기 전에 내부자 거래 활동을 드러냅니다.

- 검색 트렌드:바이럴이 되기 전에 등장하는 토큰을 추적하세요. Edgen Radar Trending체인 내 동력과 소셜 피크를 기반으로 한 것.

- 소셜 미디어 행동:소매 투자자의 관심이 증가하고 있음을 나타냅니다.

Edgen Radar이 데이터 스트림을 지속적으로 분석하여 거래자에게 결정적인 우위를 제공합니다.

인공지능 기반 거래의 미래: 다음은 무엇인가?

AI 거래 도구의 진화는 가속화되고 있다. 다음 혁신에는 다음과 같은 것이 포함된다:

- 강화된 사회적 지능:인플루언서 내러티브 및 온라인 감정의 정밀 추적

- 고급 블록체인 분석:복잡한 블록체인 데이터의 AI 기반 디코딩을 통해 스마트 머니 이동을 식별합니다.

- 완전 자동 거래 봇:자기 학습 AI가 복잡한 전략을 자율적으로 실행합니다.

왜 에드진 AI가 인공지능 거래 혁명을 이끄는가

에드진의 AI 인프라가 얼마나 효과적인지 알아보세요. About Edgen여기서 거래자가 실시간 인사이트, 예측 분석 및 커뮤니티 기반 신호를 제공하는 방법을 알아보세요.

- 체인 내 기본 정보 및 소셜 실시간 분석펌프멘탈즈."

- Edgen Search인간이 타이핑, 스크롤링 또는 필터링할 수 있는 것보다 훨씬 빠르게 몇 초 만에 깊은 시장 통찰을 발견할 수 있는 차세대 검색 기능을 제공합니다.

- AI 기반 커뮤니티 생성 거래 신호

트레이더들은 에드진 AI를 활용하여 점점 더 인공지능이 강화된 시장에서 지속적으로 앞서나가고 있습니다.

인공지능 거래를 수용하여 시장 경쟁력을 확보하세요

AI는 거래를 근본적으로 재구성한다: 사회적 감정, 블록체인 데이터 및 알고리즘 정확도가 점점 더 투자 결정을 이끌어간다.

에지나 AI와 같은 AI 솔루션을 채택함으로써 트레이더는 다음과 같이 할 수 있습니다:

- 실시간 감정 인사이트를 통해 시장 변화를 빠르게 식별하세요.

- AI 기반 알고리즘을 사용하여 빠르고 정확하게 거래하세요.

- 예측 분석을 통해 투자 리스크를 사전에 관리하십시오.

미래는 인공지능 기반의 지능을 활용하는 거래자들에게 속합니다. 더 현명하게 거래하고 시장 경쟁력을 확보할 준비가 되었나요?

더 많은 사람보다 먼저 알파를 찾고 싶으신가요?

시장은 빠르게 움직이니 뒤처지지 마세요. With Edgen Search당신은 주로 대중화되기 전에 실질적인 알파를 발견하기 위해 블록체인 트렌드, 소셜 감정 및 등장하는 서사들을 즉시 스캔할 수 있습니다.

에드진 검색으로 지금 바로 탐색을 시작하고, 더 현명하고 빠른 거래 결정을 내리세요.

투자, 드디어 혼자 안 해도 돼요.

Edgen 무료 체험. 신용카드 필요 없고, 약정도 없어요.