I Can’t Keep Up With This Clown Market Anymore. So I Built Edgen.

I’m not a professional writer. To be honest, I’m not even sure if I’m supposed to be writing this. But I wanted to tell you myself why we built Edgen, because it’s something that means a lot to me personally.

I got into crypto for probably the same reasons you did: I wanted freedom, I wanted a shot at making it, and, I’ll be honest with you, I wanted to make some money. Nothing wrong with that.

I've been trading crypto for a years now. I'm not new to this space and had a lot of fun in it. I’ve been working at Everest Ventures Group (EVG), backed and built promising DeFi and SocialFi projects in Asia, navigated through bull runs and bear markets, and built a professional network that I think is pretty okay. By most standards, I would say I am fairly well-connected in the space, I can’t lie.

But recently, even I started feeling overwhelmed. Over the years, I've learned that trading crypto is a lot tougher than it looks, even in a bull market (which are actually “clown” markets in crypto). If you've ever had that annoying experience of checking your portfolio at 3am and realizing you were right but you're entering too late (again), you know exactly what I'm talking about.

Crypto moves faster today than ever before. Way too fast. Wayyyyyy too fast. Hundreds of tokens pop up every day. Memecoins that go 100x in hours, narratives shifting overnight, hidden signals in whale wallets I’ve never heard of… the noise never stops. No matter how experienced you are, or how good your research and network is, keeping up is just impossible.

I've missed good entries, missed opportunities, and found myself always struggling to catch up. Even with my resources and connections, trying to stay ahead is so fucking exhausting. And I don’t consider myself as a particularly bad trader.

I’m married with kids now. I feel old and tired. And if someone like me, with extensive connections and years of experience, feels this overwhelmed, I know ordinary, more humble, first-time traders have to feel it even more, sometimes with dramatic consequences.

Crypto was supposed to be the golden ticket and level the playing field. It was supposed to be about giving everyone a fair shot, no matter who you were or how much money you started with. But the reality we live in right now? It doesn’t feel fair at all. It feels rigged. That’s why I decided we had to build something to change that.

I built Edgen for the little guy (because I kinda am one)

Edgen is something I desperately needed myself to not become crazy. I wanted a tool that instantly gathers collective intelligence from every corner of crypto, Crypto Twitter, smart wallets, on-chain signals, developer activity, recent VC fundraises, and delivers it clearly and quickly to me.

Something that could filter through the shitposts and rugs and show me what's genuinely important before it's too late.

So we built an AI-powered market intelligence platform that's simple enough for anyone to use, but smart enough to actually help. I can’t guarantee you'll make money every trade, no one can promise that, and whoever does is scamming you. But what I can promise is that you'll never ever trade blind again.

So we’re starting with two simple, powerful tools to start. Thanks to the proprietary social and market data we've spent countless hours accumulating and refining, Edgen’s purpose-built AI is unmatched at delivering sharp insights—whether you're researching blue-chip tokens, fresh memecoins, influential market players, or the latest fundraising deals.

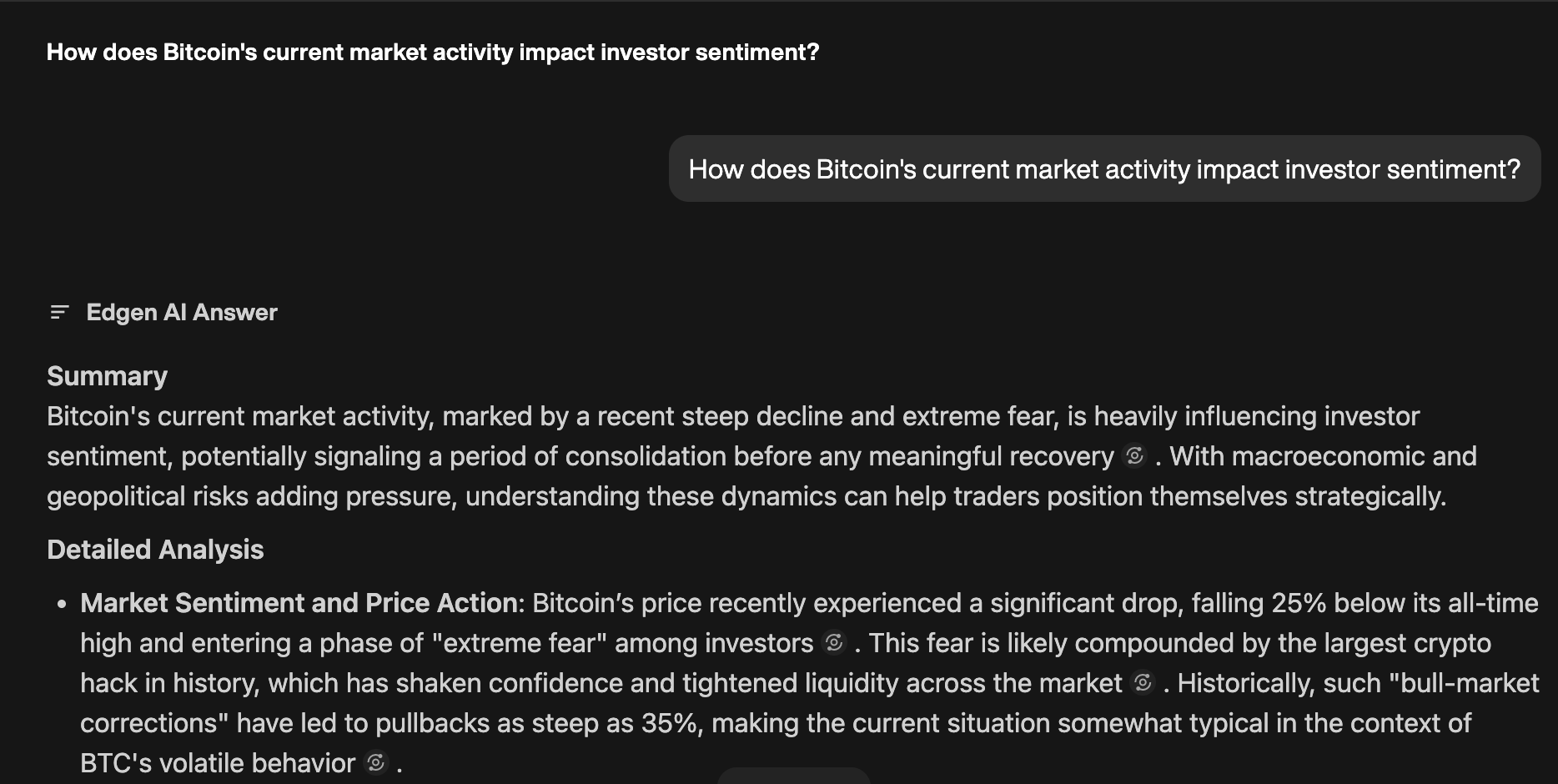

Edgen Search:

Ask any crypto question you have, complex or simple, and get immediate, actionable insights from real-time data. No more late-night doomscrolling. Our custom-trained LLM cuts through noise with precision, instantly surfacing signals and opportunities across the entire crypto landscape. And even beyond, into stocks.

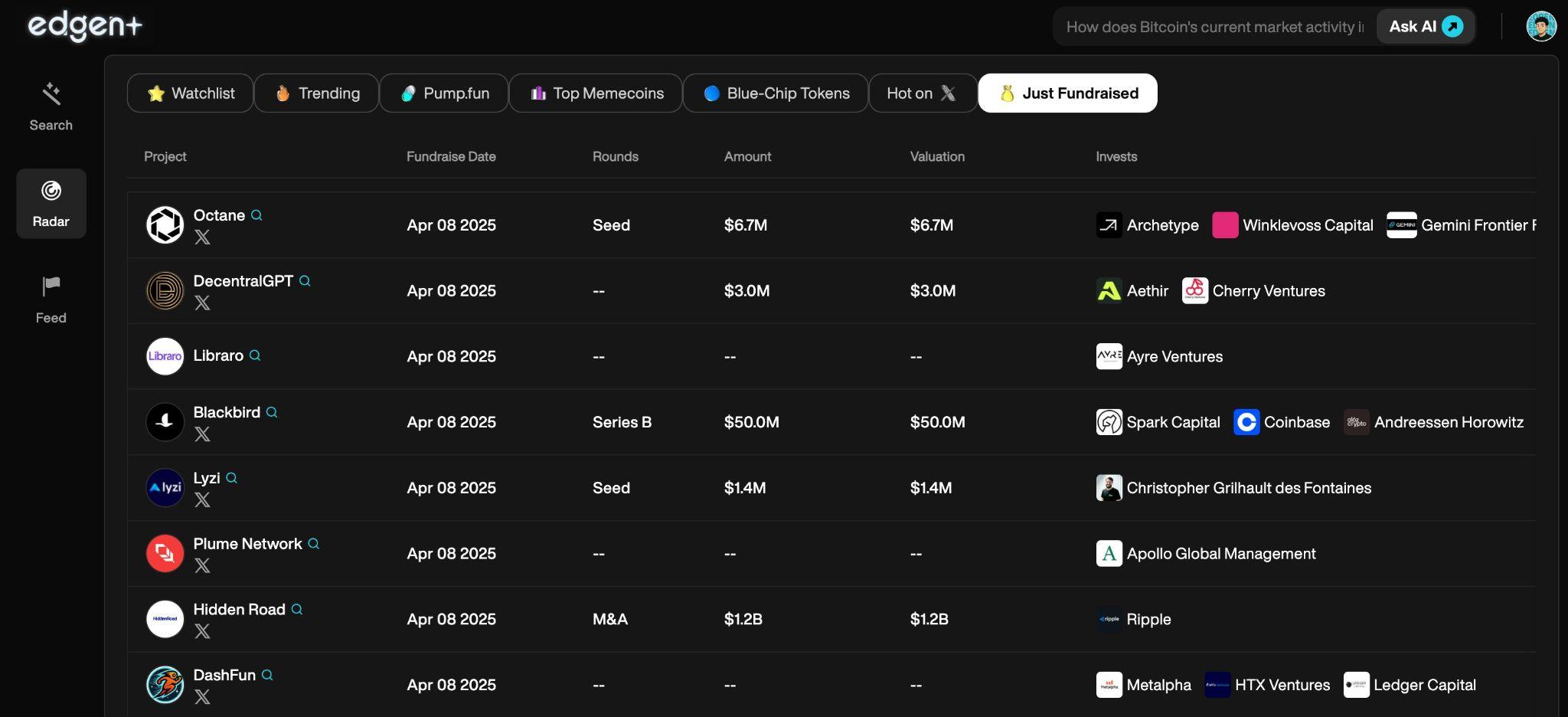

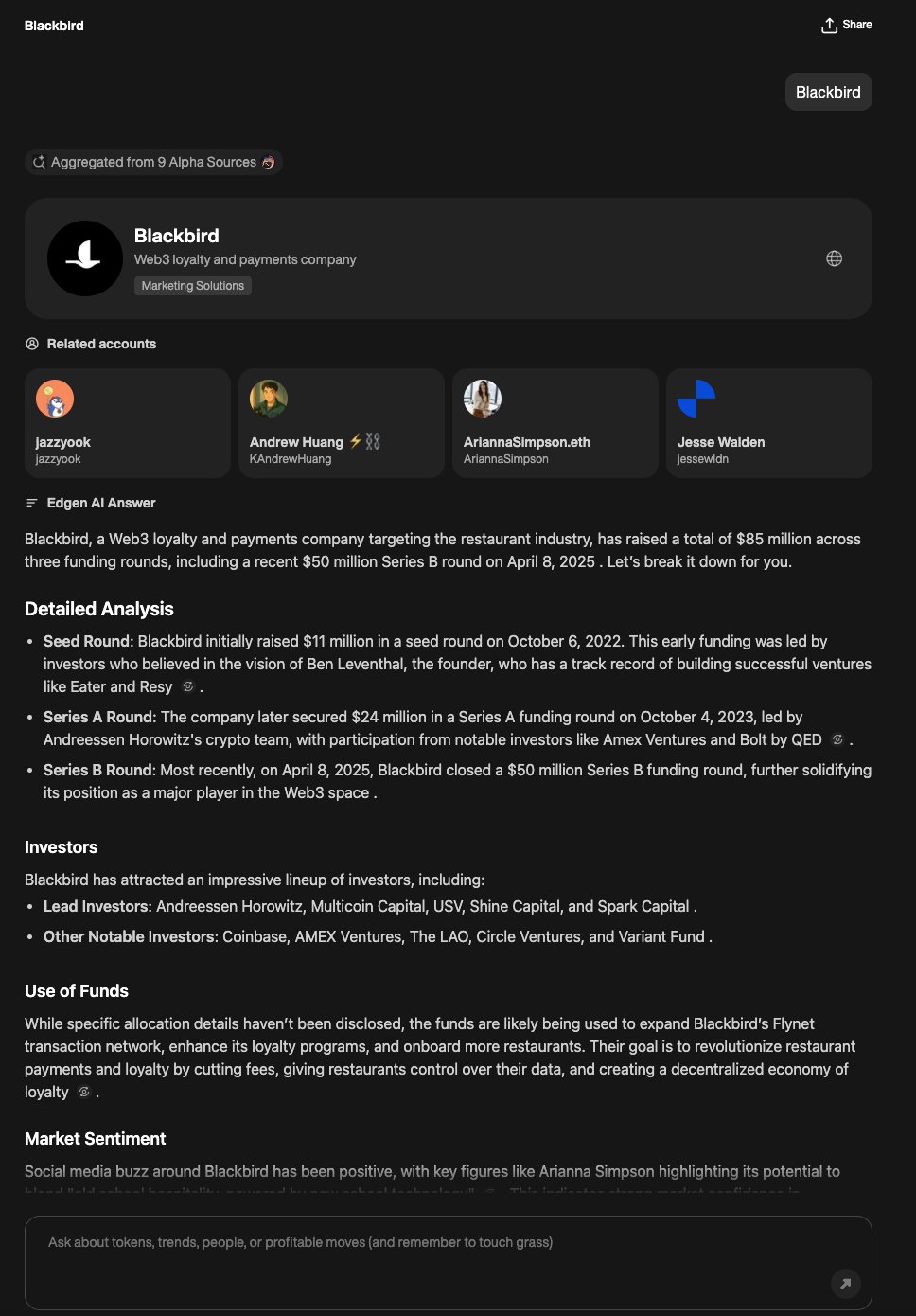

Edgen Radar:

Radar as your personal scouting dashboard. It continuously scans all kinds of tokens, blue-chip, pump.fun graduates, moonshot tokens, trending tokens, etc, and alerts you when something interesting starts happening, like smart wallet buys and sells, community hype, or key influencers quietly shifting their focus by following the token.

Go ahead and start with Search! Ask it your stupidest crypto questions, the answers you'll get back are either brutally honest or straight-up hilarious 😂

We have more tools coming soon, like Feed and, especially, Aura, but that’s a story for another day. I can tease it here though.

Aura: Identifying who you can really trust

I stop you here already: Aura is not a token. It’s a reputation system. But it’s almost the same, because in this economy, reputation is currency. Aura is your proof-of-alpha score.

Every time someone in the Edgen community shares valuable insights on Twitter, like accurate market calls, spotting emerging trends, or making predictions that turn out to be right, they farm Aura, and train Edgen’s AI to become smarter day by day. Over time, Aura shows exactly who’s trustworthy, who consistently provides genuine alpha, and who you should pay attention to.

In other words, Edgen helps you understand what’s happening, but also understand who to trust in this noisy market.

On top of the exclusive and proprietary data we’ve accumulated beforehand to make Edgen different from other LLMs, Aura is what will make our specialized, purpose-built LLM smarter by the day, in a way that isn’t replicable anywhere else.

Some of you know me from the journey I started with OpenSocial. Edgen is actually a major upgrade from OpenSocial, built on the same core vision: giving real, quantifiable value and genuine ownership to social capital and influence. With Edgen, we're taking this mission even further, transforming social insights and collective intelligence into clear, actionable market Alpha. It's everything OpenSocial aimed to be, and much more. It is its natural evolution considering today’s market.

Edgen is the great market equalizer

I built Edgen because crypto shouldn’t just benefit insiders or those who are terminally online. Of course, not everyone can make money all the time. That’s unrealistic. But with the right information, delivered clearly and quickly, anyone can have a fair chance to make money.

My dream is for Edgen to become the great equalizer in crypto trading. If we do our job right, ordinary traders of all backgrounds, from all around the world, will no longer have to feel constantly behind.

So that's my story. I'm not a fancy trader with a Wall Street background, and I definitely didn’t write this perfectly. I'm just a guy who loves crypto, and wanted something better.

So, that's the real reason why I built Edgen. I needed it myself. And I believe it can help you too.

Thanks for giving it a chance.

Sean Tao, Edgen Co-Founder

Your money person, finally.

Try Edgen free. No credit card. No commitment.