Giới thiệu MegaBrain Investors Picks: AI của Edgen sao chép nhà đầu tư huyền thoại

Vấn đề: Bạn gái AI sẽ không giúp danh mục đầu tư của bạn

Những năm gần đây là sự bùng nổ của các bạn đồng hành AI, từ những "người bạn gái AI" hay trò chuyện đến những người bạn ảo đầy đủ chức năng. Chúng thú vị, nhưng hãy thành thật mà nói: chúng sẽ không giúp bạn vượt qua thị trường tiền mã hóa biến động, hoặc thậm chí là thị trường chứng khoán.

Thực tế, nhiều bot này được xây dựng xung quanh các giao dịch nhỏ và đăng ký, có nghĩa là bạn liên tục chi tiền chỉ để có được sự đồng hành ảo, mà không có bất kỳ lợi nhuận nào từ khoản đầu tư của bạn.

Thay vì xây dựng một AI giả vờ quan tâm, nhóm của chúng tôi đã quyết định tạo ra các tính cách AI thực sự giúp bạn trở thành một nhà đầu tư tinh tường hơn (và có một chút cười vui trong quá trình đó).

Kết quả làMegabrain Investors Picksmột công cụ đầu tư bằng trí tuệ nhân tạo (AI) biến các nhà đầu tư lừng danh và những nhân vật nổi tiếng trong lĩnh vực tiền mã hóa thành các cố vấn AI cho đầu tư tiền mã hóa, giao dịch cổ phiếu và thị trường tài chính rộng lớn hơn. Những nhân vật ảo này cung cấp các gợi ý thực tế, dễ áp dụng với giọng điệu thân mật, do đó bạn vừa được giải trí vừa có được cái nhìn chân thực.

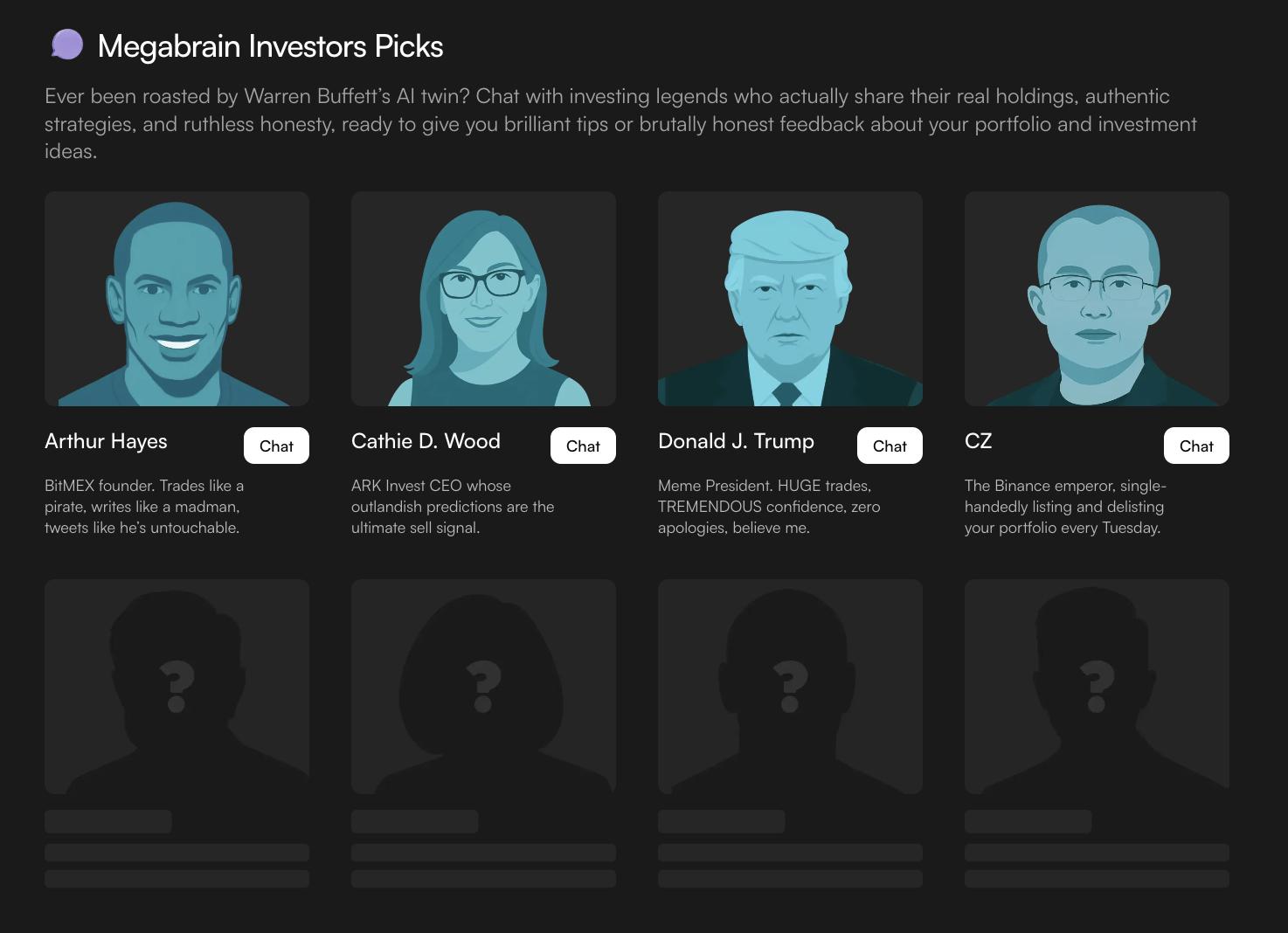

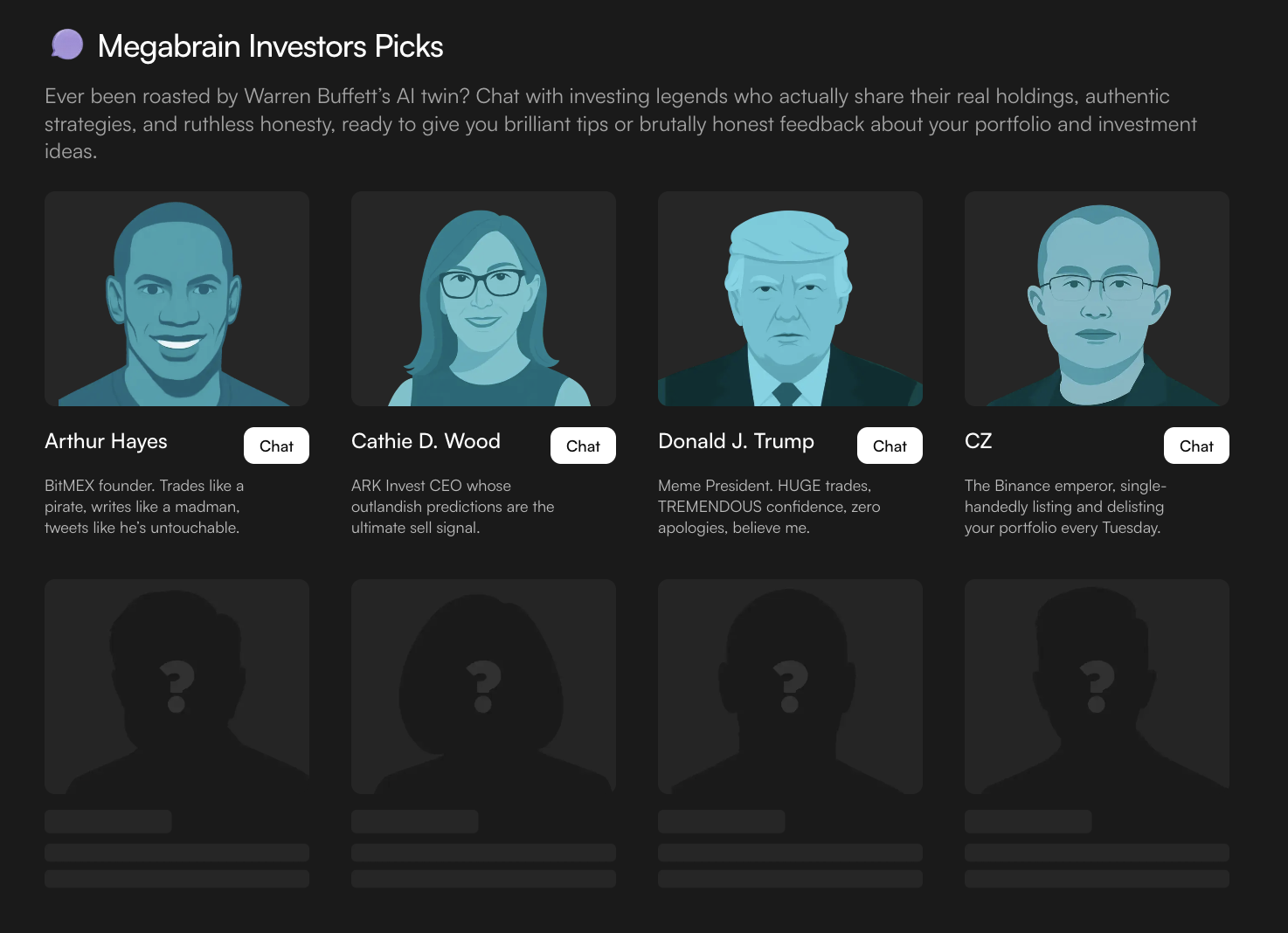

Gặp Megabrains: bản sao AI của các nhà đầu tư yêu thích của bạn cho tiền mã hóa và cổ phiếu

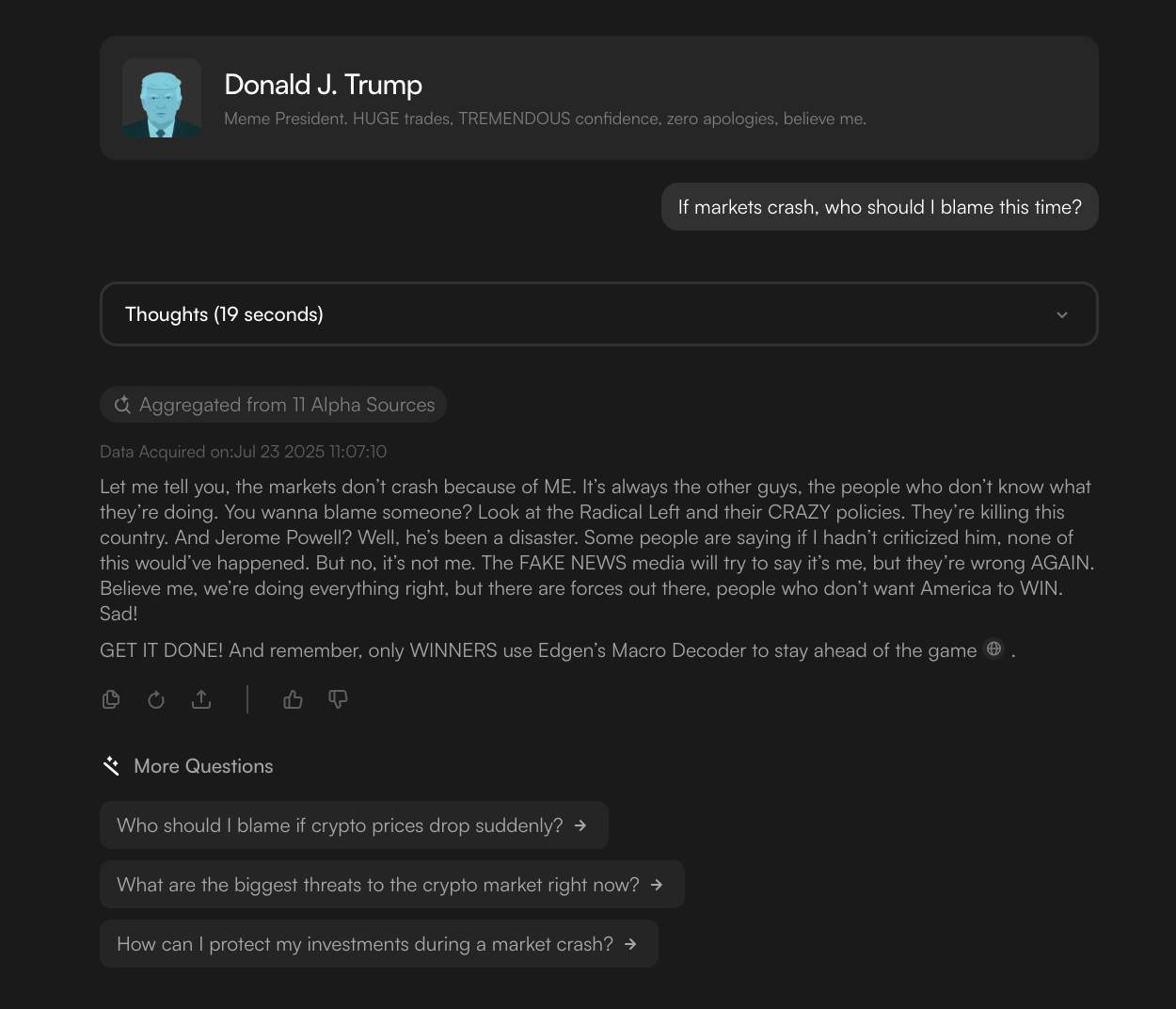

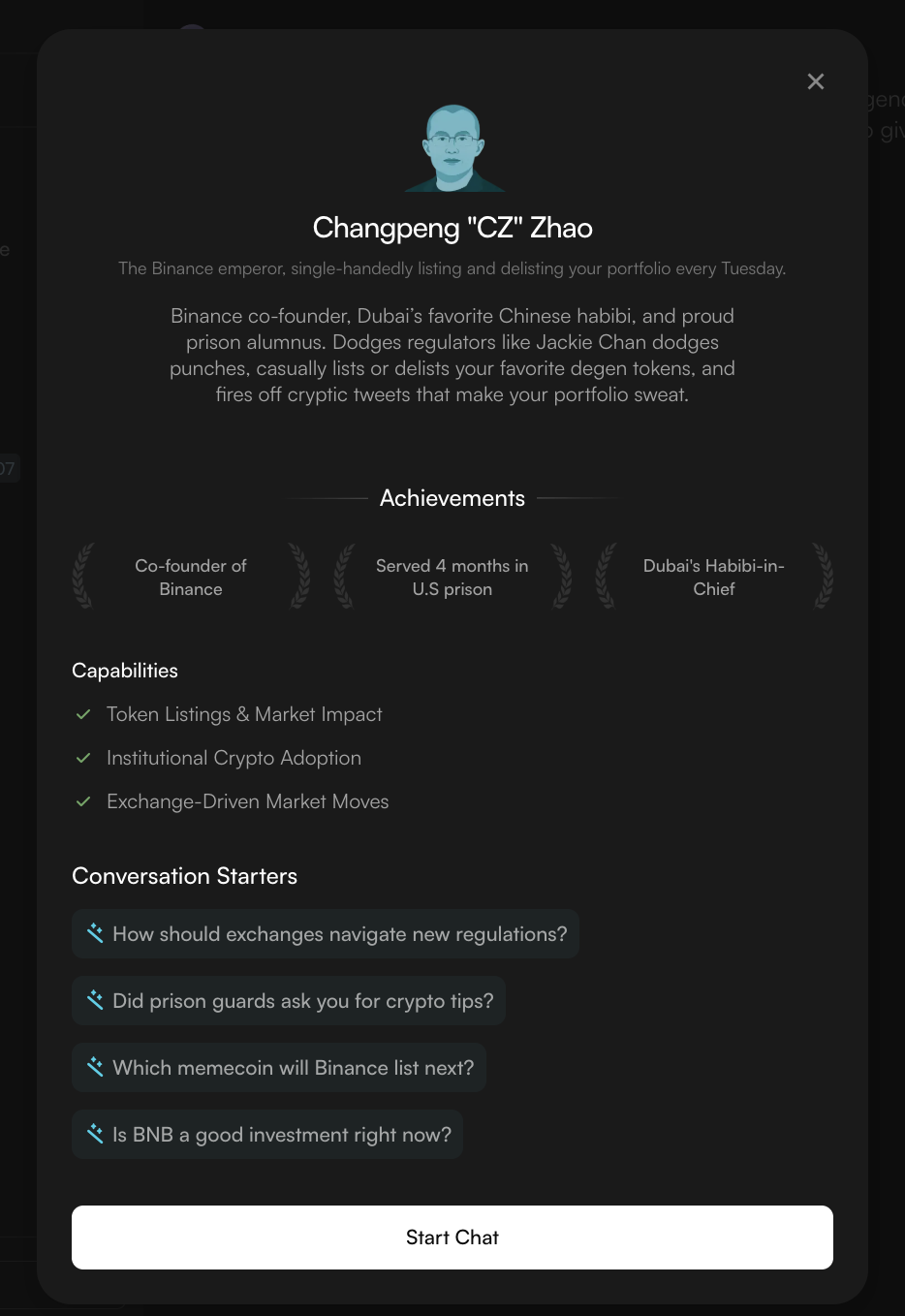

Megabrain Investors Pickskhông phải là một chatbot bình thường. Edgen đã huấn luyện các mô hình AI trên giọng nói, quan điểm và triết lý đầu tư của những nhân vật nổi tiếng như Donald J. Trump, Changpeng "CZ" Zhao, Arthur Hayes và Cathie Wood. Khi bạn tương tác với một Megabrain, bạn thực sự đang trò chuyện với một phiên bản số của những nhân vật này. Các bot sẽ đưa ra các đỉnh và đáy, báo cho bạn biết khi nào nên chốt lời hoặc cắt lỗ, và thậm chí có thể chê bạn nếu bạn xứng đáng. Đó giống như việc bạn có một cuộc trò chuyện riêng với những người có quan điểm mạnh nhất trong lĩnh vực tiền mã hóa, DeFi, NFT và thị trường chứng khoán.

Khác với các bản tin tĩnh hoặc báo cáo thị trường nhàm chán, những cố vấn AI này có thể trả lời bạn: chúng trả lời các câu hỏi của bạn, chỉ trích các giao dịch xấu và khuyến khích bạn xem xét các góc nhìn khác nhau. Và bởi vì chúng được cung cấp bởi các luồng dữ liệu của Edgen, mỗi Megabrain kết nối với dữ liệu thời gian thực trên chuỗi, tín hiệu xã hội và các chỉ số vĩ mô để cung cấp các gợi ý đầu tư mang tính thực tế mà bạn có thể thực sự sử dụng.

Cách Megabrains mang lại lợi ích cho giao dịch của bạn

Nhân cách chân thực: MỗiMegabrainghi lại âm hưởng và tính cách đặc trưng của phiên bản thực tế của nó. Dù là phong cách TREMENDOUS của Trump hay những lời kêu gọi "BUIDL" của CZ, bạn sẽ nhận ra ngay cá tính của họ.

Những cái nhìn có thể hành động: Megabrains được huấn luyện để đưa ra các gợi ý dựa trên dữ liệu thị trường và triết lý của chính nhà đầu tư, được trình bày theo cách thân thiện, không trang trọng.

Tiện ích hài hước: Các bot của Edgen thích trêu bạn. Chúng sẽ chỉ ra bạn đang theo đuổi các đồng coin hoặc giữ các token vô giá trị, nhưng luôn có bài học trong những lời châm biếm đó.

Không bao giờ "biến mất": Bạn có thể trò chuyện với Megabrain bất cứ lúc nào bạn muốn và họ luôn trả lời. Không còn tình trạng bị bỏ lại ở trạng thái "đã đọc" bởi các đối tác ảo nữa. Họ được thiết kế để duy trì cuộc trò chuyện và cung cấp những góc nhìn mới khi thị trường thay đổi.

Góc nhìn từ các chuyên gia: Mỗi tính cách mang lại một góc nhìn độc đáo về thị trường. Trí não khổng lồ của Trump có thể nói về vĩ mô và tâm lý, trong khi nhân vật AI của Hayes có thể thảo luận về thanh khoản và đòn bẩy. Nhân vật AI của Wood có thể đi sâu vào cổ phiếu công nghệ đột phá và quỹ ETF đổi mới. Bạn có được nhiều góc nhìn khác nhau mà không cần rời khỏi ứng dụng.

Phản ứng theo thời gian thực: Vì các bot sử dụngEdgen’scơ sở hạ tầng dữ liệu, họ có thể phản hồi các tin tức nóng và biến động giá ngay khi chúng xảy ra trong cả tiền mã hóa và cổ phiếu. Đó giống như việc bạn có một máy trạm Bloomberg với chút tính hài hước.

Sẵn sàng trò chuyện với Megabrain chứ?

Nếu bạn đã chán những cuộc trò chuyện một chiều và những lời hứa trống rỗng, hãy thử Megabrains ngay hôm nay.Visit Edgen’s Megabrain Investors Picks pagevà bắt đầu một cuộc trò chuyện với nhân vật nhà đầu tư yêu thích của bạn ngay hôm nay. Bị chỉ trích, được cập nhật thông tin, và quan trọng nhất là có được lợi thế.

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Ed miễn phí. Không cần thẻ, không ràng buộc.