Litecoin est une monnaie numérique pair-à-pair très sécurisée et fiable, optimisée pour des paiements mondiaux rapides et à faible coût. Pour un guide sur le Litecoin, cliquez ici

En bref

- Litecoin (LTC) est l'une des blockchains Proof-of-Work les plus établies et fiables, offrant une histoire éprouvée de dix ans de disponibilité à 100 % et une sécurité robuste.

- Des opportunités de croissance significatives se profilent à l'horizon, stimulées par la forte probabilité d'une approbation d'ETF spot américain, ce qui débloquerait des investissements institutionnels substantiels et validerait son statut de matière première numérique.

- Litecoin évolue d'un réseau de paiement pur à un écosystème polyvalent grâce à la couche 2 LitVM, jetant les bases des contrats intelligents, de la DeFi et des actifs du monde réel.

- Avec une marque profondément établie, une forte adoption par les commerçants pour les paiements et une émission de l'offre presque complète, Litecoin démontre une force fondamentale remarquable pour sa prochaine phase de croissance.

Qu'est-ce que le Litecoin (LTC) ?

Litecoin est une cryptomonnaie pair-à-pair et un projet de logiciel open source publié sous la licence MIT/X11. En tant que fork précoce du code de Bitcoin, il a été conçu pour être « l'argent du Bitcoin », offrant une alternative plus rapide et moins chère pour les transactions quotidiennes. Sa technologie de base est construite sur un modèle de preuve de travail (PoW) hautement sécurisé, qui a maintenu un record parfait de 100 % de disponibilité pendant plus d'une décennie.

Les principales caractéristiques du réseau comprennent un temps de bloc de 2,5 minutes pour des confirmations plus rapides et une offre maximale de 84 millions de pièces. Les avancées technologiques récentes, telles que les blocs d'extension MimbleWimble (MWEB) pour une confidentialité accrue et le développement de la couche 2 LitVM, signalent une expansion stratégique des capacités de Litecoin, passant d'un rail de paiement fiable à une plateforme de contrats intelligents à part entière, prête pour l'innovation future.

Partie I : Analyse fondamentale et stratégique

Direction stratégique et trajectoire narrative

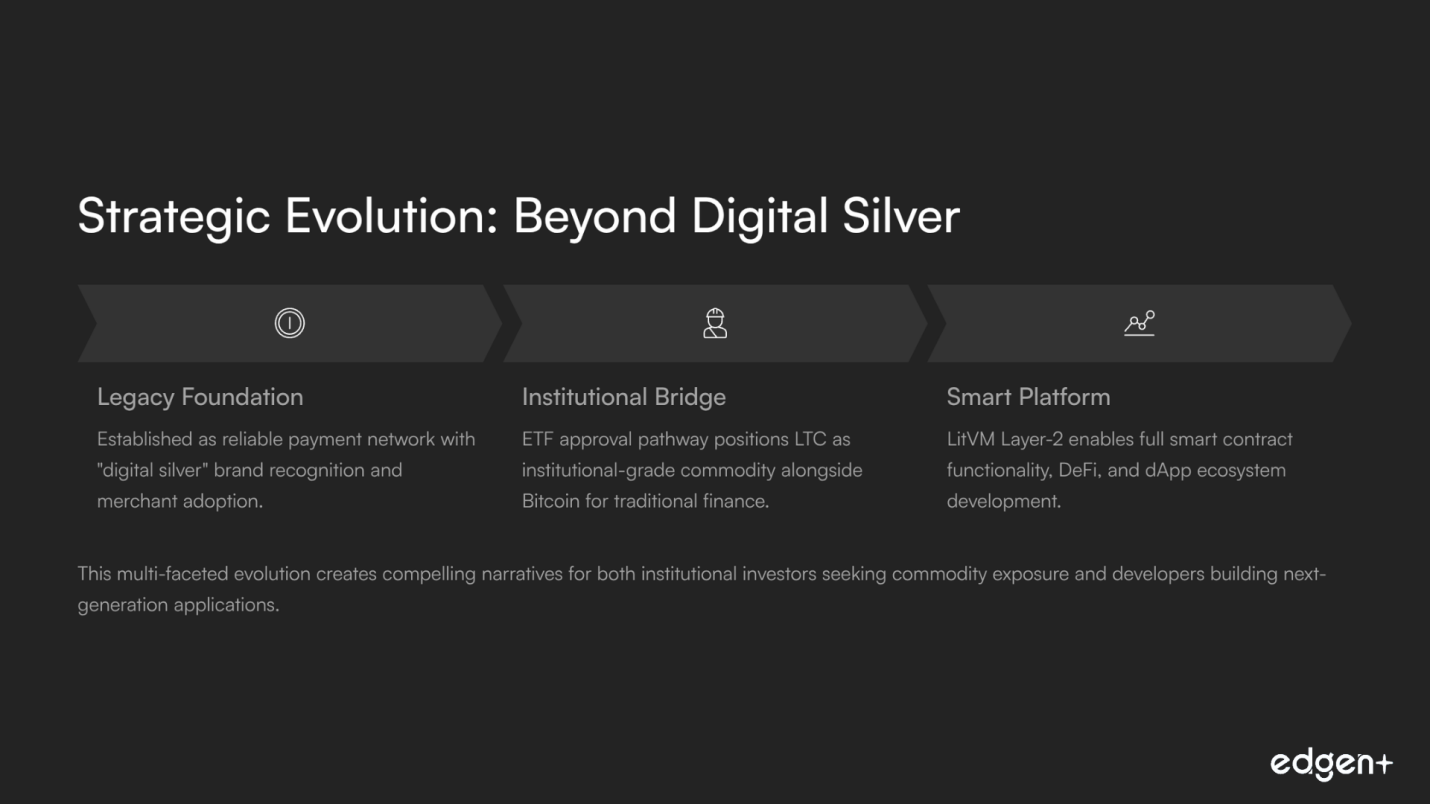

Le narratif stratégique de Litecoin est dans une phase d'évolution passionnante, passant de son identité de longue date d'« argent numérique » à une plateforme axée sur l'utilité avec un potentiel de croissance significatif. Le narratif central du projet reste ancré dans sa relation complémentaire avec Bitcoin en tant que réseau de paiement plus rapide et moins cher. Cependant, un narratif puissant et multifacette émerge, propulsé par deux développements clés :

- Adoption institutionnelle via les ETF : Un narratif externe convaincant a pris de l'ampleur autour de la forte probabilité d'une approbation d'ETF spot Litecoin aux États-Unis. Cela a attiré un intérêt institutionnel significatif, validant sa classification en tant que matière première et ouvrant la voie à des afflux de capitaux substantiels.

- Expansion technologique avec les couches 2 : Un nouveau vecteur stratégique majeur est l'intégration de la fonctionnalité de contrat intelligent via la couche 2 LitVM. Cela représente une amélioration fondamentale de la proposition de valeur de Litecoin, le faisant passer au-delà des paiements vers les domaines à forte croissance de la DeFi, des actifs du monde réel (RWAs) et des dApps.

Maîtrise du produit et de la technologie

La technologie de Litecoin démontre une puissante combinaison de fiabilité prouvée et d'innovation tournée vers l'avenir. Ses fondations en tant que fork modifié de Bitcoin l'établissent comme un réseau PoW hautement sécurisé avec plus d'une décennie de disponibilité impeccable. Des éléments différenciateurs clés comme un temps de bloc de 2,5 minutes et l'algorithme de hachage Scrypt fournissent une base solide. Le réseau a constamment démontré une capacité d'évolution technique, en implémentant SegWit et en étant un pionnier du Lightning Network.

Le développement récent le plus significatif est l'introduction de LitVM, la première solution de couche 2 de Litecoin. Ce ZK-rollup compatible EVM introduit la fonctionnalité de contrat intelligent, permettant le développement d'un écosystème DeFi et dApp moderne. Ce pivot stratégique répond à la limitation historique de la programmabilité et transforme Litecoin d'une simple monnaie de paiement en une plateforme de contrats intelligents polyvalente et complète avec un fort potentiel.

Adoption du marché et activité des développeurs

La performance quantitative de Litecoin montre une base d'utilisateurs résiliente et croissante qui valorise la fiabilité du réseau pour les paiements. Les données on-chain démontrent une utilisation robuste du réseau, avec des utilisateurs actifs quotidiens constamment par centaines de milliers et atteignant des pics de plus de 1,3 million, dépassant parfois même Bitcoin et Ethereum. Cela est puissamment étayé par les données du processeur de paiement BitPay, qui rapporte régulièrement Litecoin comme une cryptomonnaie de premier plan en termes de volume de transactions, soulignant son utilité dans le monde réel.

Le lancement de LitVM présente une opportunité significative de galvaniser la communauté des développeurs. En introduisant la compatibilité EVM, le projet abaisse stratégiquement la barrière à l'entrée pour le vaste bassin de développeurs natifs d'Ethereum, créant un nouveau moteur de croissance prometteur pour l'écosystème.

Équipe et soutiens

La gestion de Litecoin est ancrée par la très respectée Fondation Litecoin et son créateur, Charlie Lee, offrant un leadership stable et visionnaire. Charlie Lee demeure le principal visage public du projet, guidant activement le développement et les partenariats stratégiques. Cette structure de leadership claire permet une exécution décisive et efficace. La gouvernance du projet fonctionne via un processus éprouvé de proposition d'amélioration de Litecoin (LIP), qui a guidé avec succès des mises à niveau majeures comme SegWit et MWEB. Ce modèle combine une direction dirigée par des experts avec le consensus communautaire, assurant que le protocole évolue de manière sécurisée et délibérée.

Longévité de la marque et de l'écosystème

La marque Litecoin est l'une des plus établies et fiables de l'ensemble de l'espace cryptomonnaie, bâtie sur la fiabilité et son célèbre narratif d'« argent pour l'or de Bitcoin ». Cette force de marque est la plus évidente dans son adoption tangible et réelle pour les paiements, se classant constamment parmi les meilleurs choix sur les plateformes majeures comme CoinGate. Le sentiment médiatique est très positif, largement tiré par les perspectives prometteuses d'une approbation d'ETF spot américain. Cela a maintenu Litecoin à l'avant-garde de l'attention institutionnelle et de détail, renforçant sa marque en tant qu'actif numérique de premier ordre. L'écosystème continue de s'étendre avec des initiatives telles que le partenariat de domaine .LTC, démontrant un engagement envers la modernisation et la pertinence à long terme.

Partie II : Analyse On-Chain et de la Profondeur du Marché

Tokenomics durables et accumulation de valeur

La tokenomics de Litecoin est fondamentalement saine, mettant l'accent sur la rareté et un calendrier d'émission prévisible qui reflète le modèle réussi de Bitcoin. Avec une offre fixe de 84 millions de LTC et plus de 90 % déjà en circulation, le risque d'inflation future de l'offre est minimal, un signe distinctif d'une matière première numérique mature. La principale force désinflationniste est l'événement de halving, qui se produit environ tous les quatre ans et réduit systématiquement le taux de nouvelle offre. Cette rareté programmatique est conçue pour améliorer ses propriétés de réserve de valeur au fil du temps. L'introduction de LitVM crée un nouveau mécanisme puissant d'accumulation de valeur, permettant à LTC d'être utilisé pour la première fois comme garantie productive dans un écosystème DeFi en pleine croissance.

Distribution des détenteurs de jetons et métriques On-Chain

L'analyse de la distribution des détenteurs de Litecoin révèle un paysage on-chain mature avec un fort potentiel de stabilité des prix. Alors qu'une part notable de l'offre est détenue par de grandes adresses, qui représentent souvent des dépositaires d'échange sécurisés, l'activité on-chain récente montre un schéma prometteur d'accumulation parmi les grands détenteurs. Cette tendance signale une conviction haussière de la part d'investisseurs sophistiqués, probablement en anticipation de catalyseurs positifs tels que les approbations d'ETF et le lancement de LitVM. Ce flux dynamique de jetons vers les portefeuilles de baleines fournit un signal fort de la confiance des détenteurs et un soutien potentiel des prix, étayant une perspective très prometteuse.

Analyse de la notoriété et de la part de marché

La notoriété de Litecoin sur le marché est exceptionnellement forte, portée par sa réputation durable et de puissants catalyseurs émergents. Le narratif dominant est l'approbation potentielle d'un ETF spot Litecoin, qui génère constamment une couverture médiatique positive et positionne le LTC comme un actif au statut de matière première, au même titre que Bitcoin. Ce narratif capte efficacement l'attention institutionnelle. Simultanément, l'évolution technologique impulsée par LitVM revitalise l'histoire fondamentale du projet, mettant en valeur l'innovation et une stratégie claire pour concourir dans le paysage Web3 moderne. Ces doubles narratifs créent un dossier d'investissement convaincant et largement discuté, avec des opportunités significatives pour une croissance continue de la part de marché.

Partie III : Analyse prospective (Catalyseurs et considérations clés)

Perspectives à court terme (<1 mois)

Les perspectives à court terme sont caractérisées par un fort engagement communautaire et des développements positifs de l'écosystème. Des événements comme le Sommet de la Preuve de Travail, où le fondateur Charlie Lee est un orateur principal, renforcent le statut de Litecoin en tant que pilier de la communauté blockchain sécurisée. Ces événements sont cruciaux pour renforcer le narratif et favoriser les relations avec les développeurs. Une considération clé pour la croissance durant cette période est l'anticipation croissante du marché concernant la décision de l'ETF, qui devrait créer un élan positif et attirer des afflux spéculatifs à mesure que les dates de décision approchent, présentant une configuration très prometteuse.

Perspectives à moyen terme (1-3 mois)

- Approbation d'un ETF spot américain : Les analystes estimant une probabilité pouvant atteindre 95 %, une approbation serait un événement marquant, débloquant un capital institutionnel significatif et consolidant la position de Litecoin en tant qu'actif légitime de niveau institutionnel.

- Lancement de LitVM (Testnet et Mainnet) : Le déploiement prévu du testnet et du mainnet de LitVM est le catalyseur interne le plus important. Un lancement réussi sera une puissante démonstration des capacités innovantes du projet, modifiant le narratif et ouvrant la porte à un écosystème DeFi et dApp dynamique. Cela représente une opportunité significative d'expansion de la valorisation.

Perspectives à long terme (6+ mois)

Les perspectives à long terme de Litecoin présentent une force fondamentale remarquable, axée sur la croissance de l'écosystème et une politique monétaire saine. L'adoption continue de la fonctionnalité de confidentialité MWEB améliore la fongibilité du LTC, renforçant ses propriétés de « monnaie saine ». Le prochain halving de Litecoin en 2027 est un puissant catalyseur, piloté par le protocole, qui réduira davantage l'inflation de l'offre et renforcera le narratif d'« argent numérique ». Une considération clé pour la croissance sera la capacité de l'écosystème LitVM à attirer une valeur totale verrouillée (TVL) significative et une base d'utilisateurs dynamique, ce qui garantirait sa position en tant que blockchain polyvalente de premier plan pour les décennies à venir.

Partie IV : Valorisation et position concurrentielle

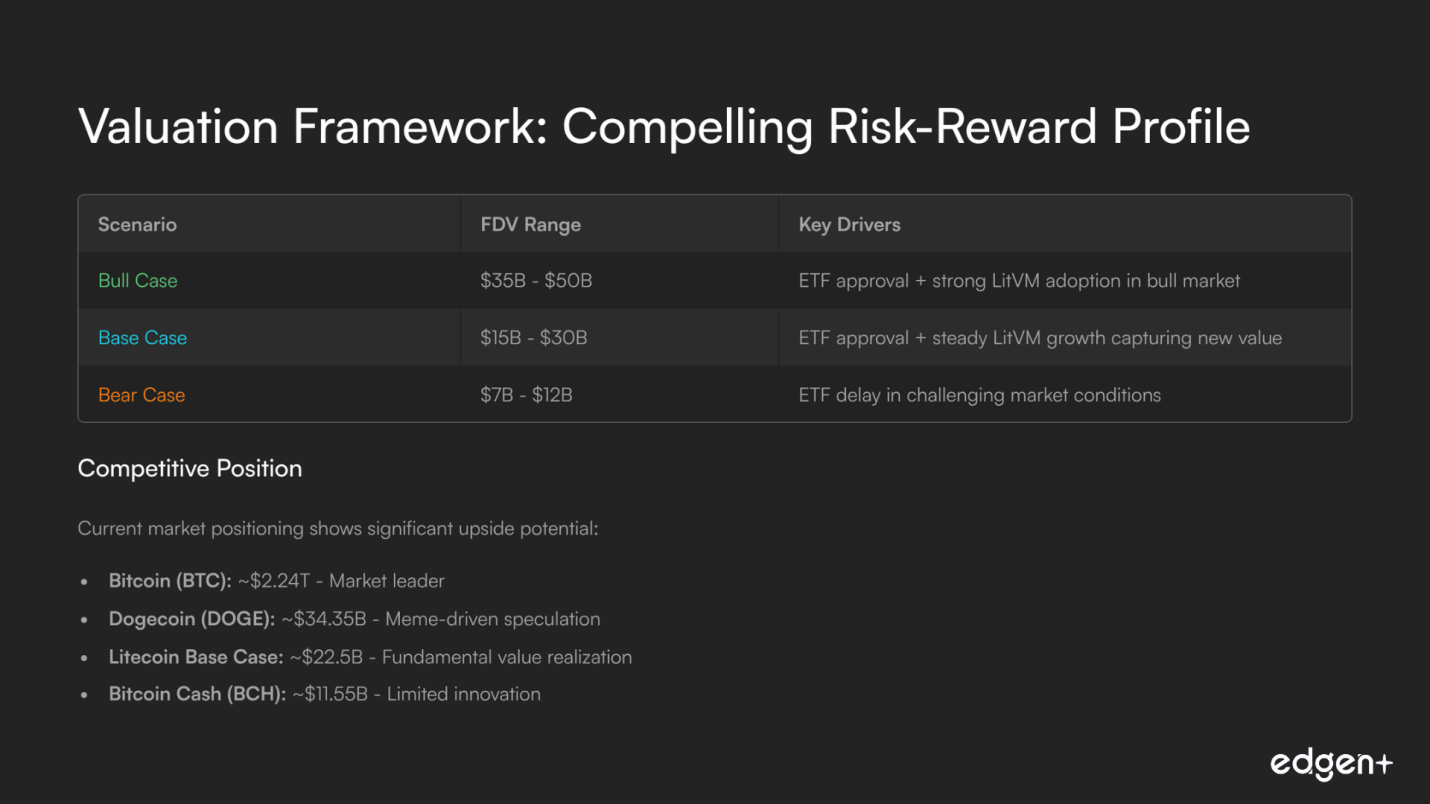

Scénarios de valorisation

Scénario | Gamme FDV (USD) | Justification et narratif |

Cas haussier | 35B$ - 50B$ | Approbation ETF et forte adoption de LitVM dans un marché haussier. |

Cas de base | 15B$ - 30B$ | Approbation ETF et croissance stable de LitVM, capturant de la nouvelle valeur. |

Cas baissier | 7B$ - 12B$ | Retard de l'ETF dans un marché difficile, étouffant l'élan. |

Paysage concurrentiel

Litecoin occupe une position unique et puissante sur le marché. Bien qu'il soit comparé à d'autres pièces de preuve de travail, son expansion stratégique vers la fonctionnalité de couche 2 lui permet de rivaliser sur un nouveau vecteur. La valorisation du cas de base reflète son potentiel à maintenir son statut de PoW de premier plan tout en capturant de la nouvelle valeur de son écosystème de contrats intelligents émergent.

Projet | Symbole | FDV Actuel (environ USD) |

Bitcoin | BTC | ≈ 2.24T $ |

Dogecoin | DOGE | ≈ 34.35B $ |

Litecoin (Cas de base) | LTC | ≈ 22.5B $ |

Bitcoin Cash | BCH | ≈ 11.55B $ |

Thèse finale

Litecoin se trouve à un point d'inflexion crucial et passionnant, prêt à capitaliser sur son héritage de sécurité et de fiabilité de dix ans tout en embrassant un avenir d'utilité élargie. Le projet présente un cas d'investissement convaincant, soutenu par le puissant catalyseur à court terme d'une approbation très probable d'ETF spot et le potentiel transformateur à long terme de son écosystème LitVM Layer-2. Ses tokenomics saines et déflationnistes et sa marque mondiale établie constituent une base remarquable. Litecoin est idéalement positionné pour combler le fossé entre la finance traditionnelle et l'avenir décentralisé, offrant des opportunités significatives de croissance et de leadership durable sur le marché.

Investir, enfin, tu n'es plus seul.

Essaie Ed gratuitement. Sans carte, sans engagement.