Portföyler: Varlıklarınızı İzlemenin Daha Akıllı Bir Yolu

Piyasalar, herhangi bir yatırımcının işleyebileceğinden daha fazla bilgi üretir. Her fiyat hareketi, kazanç güncellemesi ve zincir üstü veri, zaten doymuş bir akışa gürültü ekler.

Çözüm eskiden geleneksel hisse senedi veya token izleme listeleriydi. Bunlar fiyatları ve borsa sembollerini gösterir. Ancak bu sayıların ne anlama geldiği ve hangi eylemlerin yapılması gerektiği hakkında çok az bilgi verirler.

Bugün Edgen, Portföyler'i sunuyor: oluşturduğunuz listelerdeki varlıklara çoklu aracı akıl yürütmeyi uygulayan, portföye özel bir yardımcı.

Her liste, anlatılar ve şoklar her ikisi arasında hareket ettiğinden, aynı anda hisse senetleri, tokenlar veya hem hisse senetleri hem de tokenlar içerebilir.

Varlıkları Takip Etmenin Yeni Bir Yolu

Takip etmek kolaydır. Anlamak daha zordur.

Portföyler, listelerinizi, Edgen'in uzman temsilcileri sayesinde anında net olan kişiselleştirilmiş bir biçimde varlıklarınızı düşünen, neyin önemli olduğunu analiz eden ve sunan aktif bir zeka katmanına dönüştürür. Bunu, portföyünüze gömülü, tarzınıza göre ayarlanmış ve sürekli çalışan bir analist olarak düşünün.

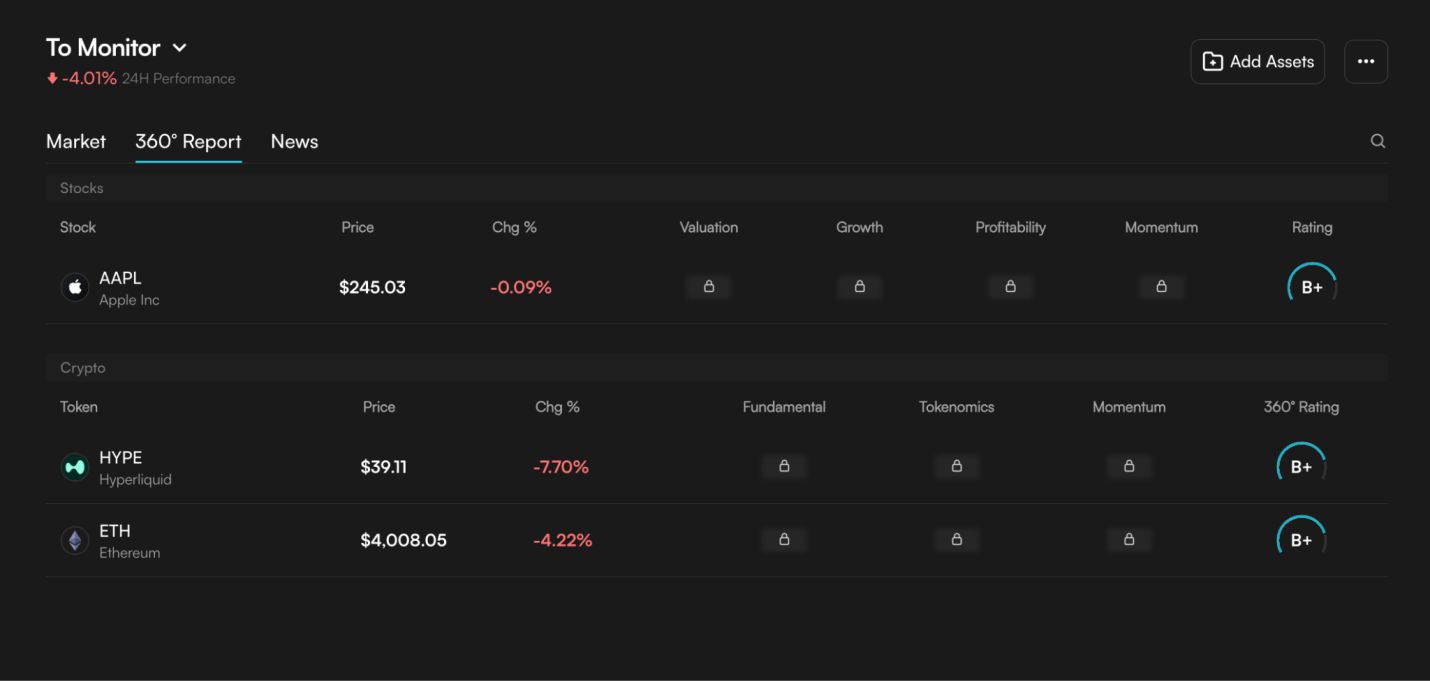

Hisse senetleri ve kripto genelinde takip ettiğiniz her varlık, sürekli teşhisler, harf notu değerlendirmeleri (A'dan F'ye) ve gerçek zamanlı olarak gelişen açıklamalar alır.

İzleme listeniz, gerçek zamanlı olarak temel hareketleri yorumlayan, puanlayan ve vurgulayan canlı bir sistem haline gelir. Yatırım ritimlerinizi, tercih ettiğiniz sektörleri, kovaladığınız modelleri, tolere ettiğiniz riskleri öğrenir ve bu sinyaller etrafında içgörüleri ince ayar yapar.

Ne kadar çok kullanırsanız, rehberlik o kadar keskinleşecektir.

Piyasalar sizi beklemez. Edgen Portföyleri, dikkatinizin en önemli yere odaklanmasını sağlar.

Edgen Portföyleri Nasıl Çalışır?

Sahne arkasında, Edgen'in uzman aracı ağı, birden çok piyasa verisi boyutunda eşzamanlı olarak çalışır:

- Teknikler: fiyat kalıpları, oynaklık ve momentum.

- Temeller: kazançlar, token veya öz sermaye metrikleri ve temel iş verileri.

- Momentum: akış, duyarlılık ve hacim dinamikleri.

- Makro: çapraz varlık korelasyonları ve daha geniş piyasa güçleri.

Edgen'in rehberlik modeli (EDGM), bu aracıları koordine eder, girdileri doğrular ve bunları listenizde görünen net ve kişiselleştirilmiş tek bir çıktıya birleştirir.

Sonuç, hem hisse senetleri hem de kripto genelinde takip ettiğiniz her varlığı kapsayan, koşullar değiştikçe otomatik olarak güncellenen, birleşik ve açıklanabilir bir görünümdür.

- Bunu canlı portföyünüz olarak veya gözünüzde olan varlıklar için bir izleme listesi olarak kullanabilirsiniz.

- Ayrıca bir sektör veya anlatı sepeti (Yapay Zeka, Perp DEX, ETH tutan hisse senetleri) oluşturabilir ve favori tokenleriniz ile hisse senetlerinizdeki sinyallerin nasıl hizalandığını izleyebilirsiniz.

- Ayrıca, fikirleri stres test etmek ve piyasalar değiştikçe derecelendirmelerin nasıl geliştiğini görmek için bir tez kum havuzu tutabilirsiniz.

- Ayrıca, risk profilinize uyan pozisyonlar için yüksek veya düşük riskli bir liste belirleyebilirsiniz.

- Türbülanslı piyasa aşamalarında güç gösteren güvenli liman varlıklarını takip etmek için bir hedge panosu oluşturun.

Gördüğünüz gibi, sınırlar gökyüzü kadardır.

Edgen'de Portföyler Nasıl Kullanılır?

Sol taraftaki menüde

Yatırım yapmak artık yalnız bir iş değil.

Ed'i ücretsiz dene. Kart yok, taahhüt yok.