Edgen x Pudgy Penguins - 문화와 함께하는 지능 🐧 (2단계)

시장은 진지한 사업입니다. 펭귄도 마찬가지입니다.

하지만 때로는 둘을 함께하는 것이 가장 현명한 움직임입니다.

몇 주 동안(11월 14일 ~ 30일) 두 단계에 걸쳐, Edgen은 Web3에서 가장 마음 중심적인 브랜드인 Pudgy Penguins와 협력하여 모든 주기를 통해 침착함을 유지하는 방법을 세상에 가르쳐 온 커뮤니티에 보상을 제공합니다.

귀여운 아바타에 AI 스마트 마인드를 부여하기

Pudgy는 인터넷에서 커뮤니티가 여전히 의미 있다는 드문 감각과 함께, 온체인 및 오프라인 수집품을 통해 살아있는 문화를 구축했습니다.

Edgen은 외부에서 무슨 일이 벌어지고 있는지 파악하기 위해 만들어졌습니다: 데이터, 흐름, 시장 뒤의 신호 (네, 펭귄이 있는 시장도 포함해서요).

세계에서 가장 사랑받는 펭귄이 시장을 해석하는 AI를 만났을 때, 새로운 일이 발생합니다: 수집의 즐거움이 이해의 명확성으로 보상받습니다.

이 협력은 Pudgy 커뮤니티에 시장에 대한 접근과 통찰력을 제공합니다.

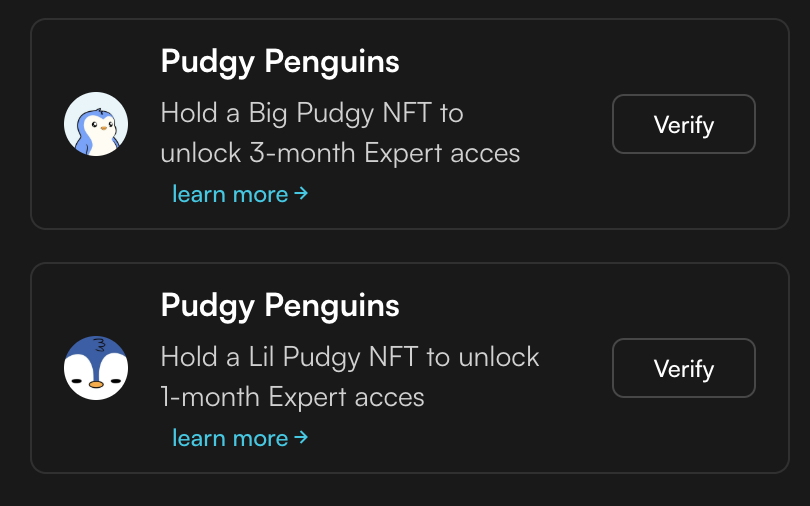

Pudgy NFT로 청구할 수 있는 내용 (1단계 - 종료)

11월 14일 주부터 Ethereum에서 시작됩니다:

🐧 Big Pudgy NFT 보유자: 3개월 Edgen Expert (가치 $150)

🐧 Lil Pudgy NFT 보유자: 1개월 Edgen Expert (가치 $50)

스냅샷 시간: 11월 13일 00:00UTC

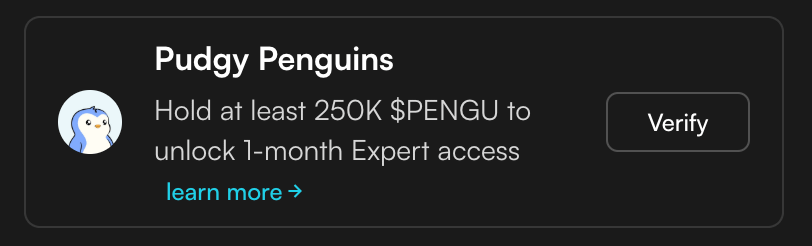

$PENGU로 청구할 수 있는 내용 (2단계 - 현재)

11월 24일 주부터 Solana에서 시작됩니다:

🐧 250,000 $PENGU 이상 보유자: 1개월 Edgen Expert (가치 $50)

스냅샷 시간: 11월 24일 00:00UTC

Edgen Expert는 시장을 위한 개인 AI입니다: 토큰, 주식, 내러티브(NFT 포함)를 실시간으로 분석하며, 귀하의 거래 및 사고 방식에 맞춰 맞춤화됩니다.

Edgen에 가입하는 방법

- Edgen 내의 Aura 페이지로 이동합니다 (왼쪽 메뉴).

- 지갑을 연결합니다 (Pudgy NFT의 경우 ETH, $PENGU의 경우 SOL). 저희 시스템이 Pudgy 보유량을 자동으로 확인합니다.

- Expert 액세스가 활성화됩니다.

🧭 여기에서 시작하세요: https://www.edgen.tech/app/crypto

문화의 지능은 여기에서 시작됩니다 🐧

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.