Edgen × Kaito 360° 챌린지: 시장을 압도하세요!

[업데이트] Kaito의 공개 리더보드 및 X의 플랫폼 정책 변경으로 인해 Kaito의 리더보드가 종료되었습니다. 이는 Edgen에 영향을 미치지 않습니다. Aura 및 Edgen 리더보드는 완전히 독립적으로 운영되며, 향후 퀘스트는 포트폴리오를 더 잘 관리하고 정보에 입각한 투자 결정을 내리는 데 중점을 둘 것입니다.

모두가 뜨거운 견해를 가지고 있지만, 모두가 통찰력을 가지고 있는 것은 아닙니다.

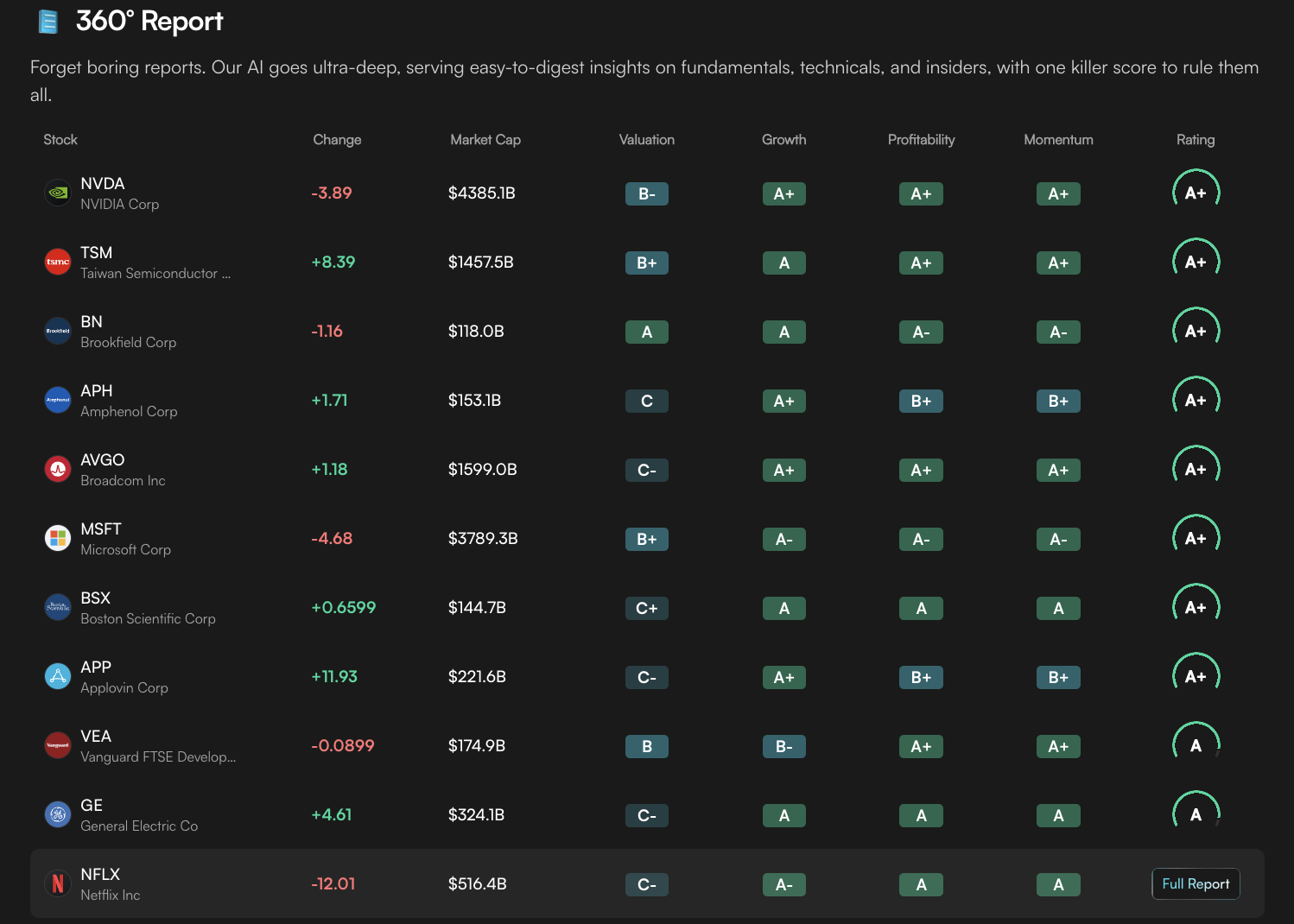

Edgen은 360° 보고서와 예측 페이지를 통해 주식과 암호화폐를 하나의 화면에 통합하여 이러한 통찰력을 제공합니다.

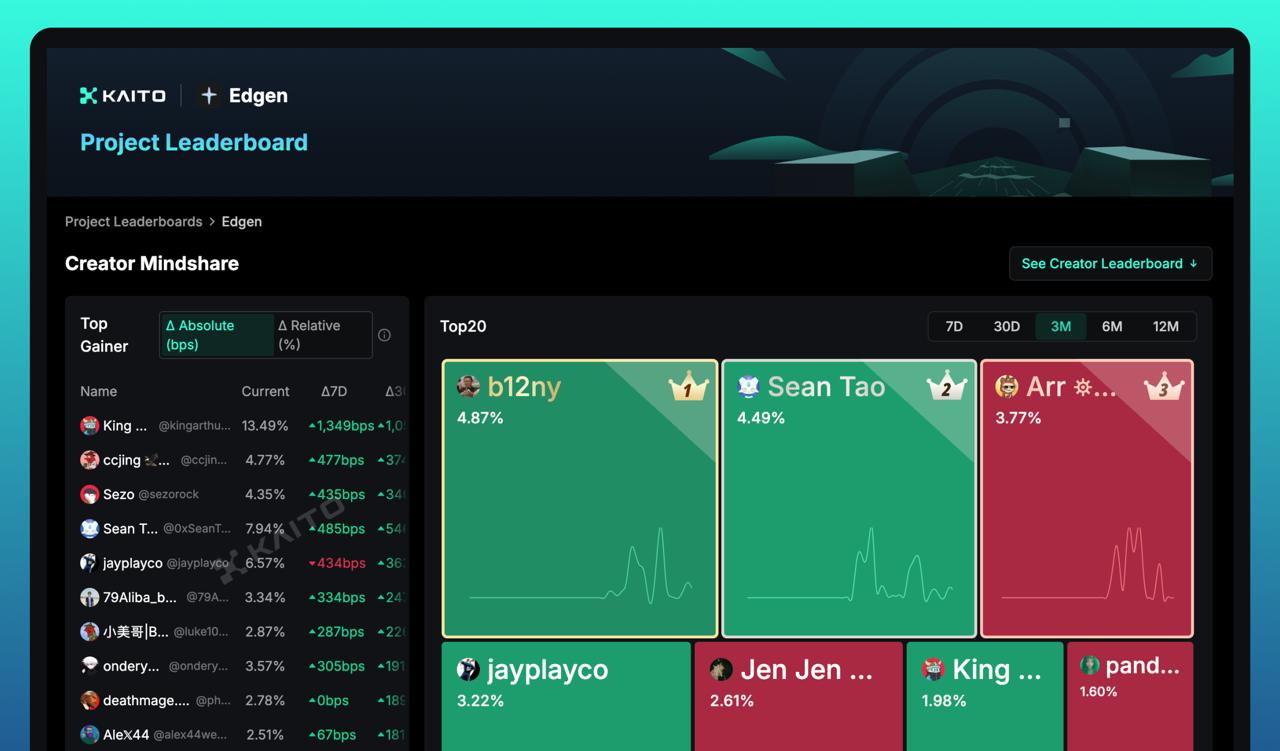

Kaito는 의견을 모읍니다: 실시간으로 커뮤니티 기여를 추적하고 순위를 매겨 사려 깊은 게시물이 상단에 노출되도록 합니다.

가장 설득력 있는 분석을 기념하기 위해 일주일간의 챌린지를 시작합니다.

AI 심사위원, 인간의 목소리: 360° 통찰력이 중요한 이유

Kaito의 Yapper 리더보드는 모든 브랜드 또는 주제에 대한 기여도를 추적하고 순위를 매기는 공개 대시보드입니다. 이는 참여를 장려하고, 모든 사람에게 공정한 기회를 제공하며, 커뮤니티 참여를 즐거운 경험으로 만듭니다. 사람들은 이 리더보드를 사용하여 고품질 크리에이터를 부각시키고 공로에 기반한 기여를 보상합니다.

이러한 접근 방식은 Edgen의 사명과 일치합니다. 우리의 360° 보고서는 사람들이 기본, 기술 및 모멘텀 전반에 걸쳐 매우 깊이 있게 분석하고, 비트코인, Solana 또는 우량주와 같은 각 자산에 대한 모든 것을 단일 점수로 압축하도록 돕습니다.

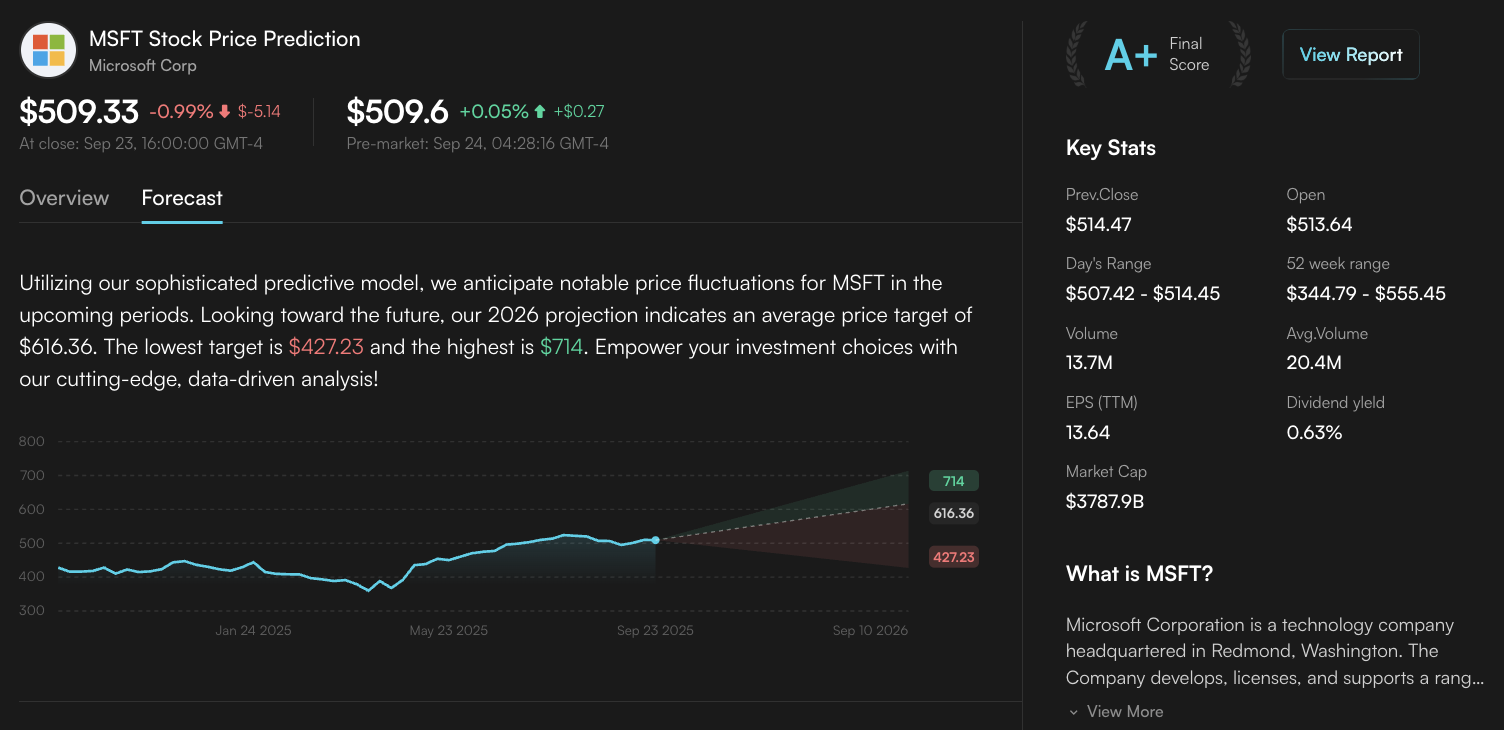

저희의 예측 페이지는 예측 모델을 적용하여 미래 가격 범위를 예측하고 사람들이 시장 판단을 내릴 수 있도록 돕습니다. 평균, 저점 및 고점 목표를 제공합니다. Edgen의 데이터를 Kaito의 AI 랭킹과 결합하면 분석이 가시성과 인정을 얻게 됩니다.

경기장으로 입장: 360° 관점을 보여주세요

⏰ 기간: 2025년 9월 24일 ~ 2025년 9월 30일 (캠페인 마감 시간은 UTC 15:59:59)

🎯 주제: 관심 있는 자산을 선택하고 360° 보고서 또는 예측 페이지를 엽니다. 이 한 페이지 자료를 사용하여 X에 대한 자신만의 견해를 작성하세요. 눈에 띄는 점을 강조하고, 지표를 연결하거나, 앞으로 예상되는 촉매제를 언급하세요. 암호화폐든 주식이든 선택은 당신의 몫입니다!

📌 참여 방법:

- Edgen X 커뮤니티 내에 분석 내용을 게시하고 팔로워들도 볼 수 있도록 하세요

- @EdgenTech를 태그하여 집계되도록 하세요

- 참여 양식을 작성하여 전문가 테이블에 앉을 기회를 얻으세요

품질이 가장 중요합니다. 리더보드는 양보다는 독창성과 사려 깊은 분석에 보상을 제공합니다.

자신만의 관점을 제시하고, 시장 전반의 통찰력을 연결하며, 데이터가 당신에게 무엇을 의미하는지 설명하세요.

전문가 테이블의 자리

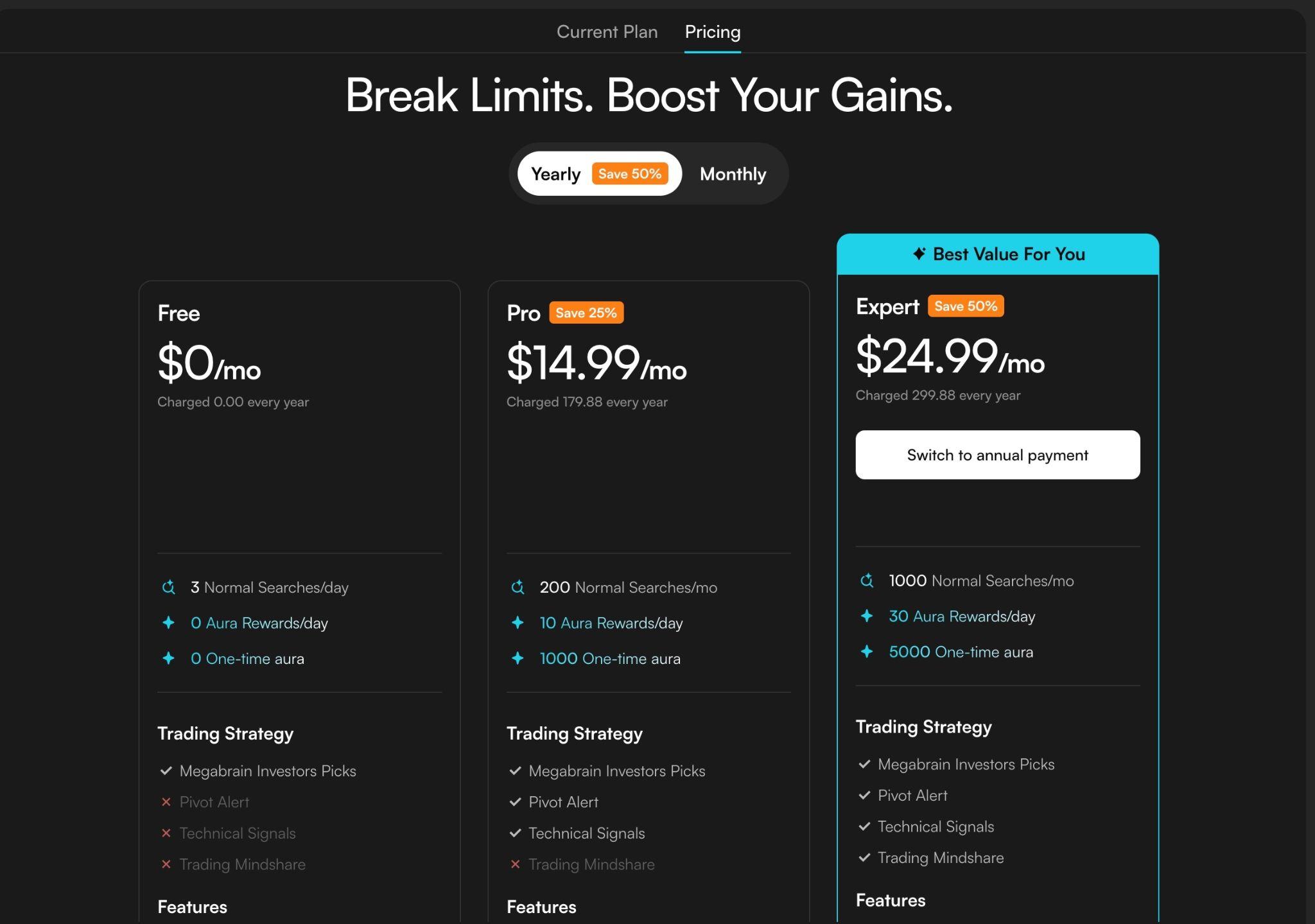

그 주가 끝나면 Edgen 연간 전문가 플랜에 참여할 세 명의 뛰어난 기여자를 선정할 것입니다. 전문가 회원은 새로운 기능에 대한 조기 접근, 더 빠른 Aura 처리, 더 심층적인 분석 및 고급 에이전트 접근 권한을 얻습니다. 이는 귀하의 투자 여정을 위한 터보 버튼입니다.

리더보드 순위 상승

- 독창성을 유지하세요: Yapper 리더보드는 독특한 관점을 제시하는 크리에이터를 부각시킵니다.

- 전체적인 시각을 가지세요: 360° 보고서는 기본 분석, 토큰 경제학, 모멘텀 및 심리를 다룹니다. 이들이 어떻게 연결되는지 보여주세요.

- 미래를 생각하세요: 예측 페이지의 가격 범위를 자신만의 논리를 위한 발판으로 활용하세요. 이 예측에 동의하십니까? 동의하거나 동의하지 않는 이유는 무엇입니까?

- 참여하고 격려하세요: 다른 게시물에 댓글을 달고, 질문하고, 대화 성장에 기여하세요. 리더보드는 상호 작용을 통해 발전합니다.

이제 당신의 차례: 대화에 참여하세요

이 챌린지는 당신의 생각을 보여주고, 시장에 대한 이해를 날카롭게 하며, 이에 대한 인정을 받을 수 있는 기회입니다. 당신의 목소리가 연간 전문가 플랜을 얻게 하고 거래자들이 매일 가장 먼저 확인하는 것이 될 수 있습니다.

Edgen X 커뮤니티로 가서 360° 보고서 또는 예측 페이지를 선택하고, 당신의 견해를 공유하고, @EdgenTech를 태그한 후, 양식을 통해 즐거움에 동참하세요. 당신이 무엇을 가져올지 기대됩니다.

가자, Ledgens!

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.