Edgen AI : Comment l'IA alimente la prochaine vague de trading crypto à haut risque et haut rendement

Bienvenue dans l'avenir du trading de crypto-monnaies à haut risque "Degen"

Imaginez posséder un weapon secret qui prédit les mouvements du marché des cryptomonnaies, découvre des pierres précieuses cachées et vous aide à saisir des profits en temps réel. C'est précisément ce queEdgen AIlivre, en transformant la manière dont les traders de cryptomonnaies naviguent dans le monde volatil des actifs numériques.

Les crypto-monnaies évoluent plus rapidement que jamais. Les traders performants ne s'appuient plus uniquement sur des graphiques traditionnels ou sur leur intuition ; ils ont besoin d'analyses plus approfondies sur ce qui motive le marché, comme l'activité des whales, les tweets des influenceurs ou la discussion sur les réseaux sociaux. C'est ici que Edgen AI brille : en combinant une analyse de données rigoureuse avec un suivi avancé de l'opinion publique. Il s'agit d'une technologie pointue, autrefois réservée uniquement aux fonds spéculatifs de premier plan.

Ensemble, Degen AI et Edgen AI aident les traders à anticiper les mouvements du marché, à éliminer le biais émotionnel et à réaliser des profits supérieurs aux rendements habituels du marché.

Qu'est-ce que Edgen AI exactement ?

Edgen AIest une plateforme avancée de trading cryptographique alimentée par l'intelligence artificielle, conçue spécifiquement pour les environnements cryptographiques à haut risque. Elle identifie les opportunités de trading "Alpha" rentables en analysant en temps réel les données blockchain sur chaîne et les signaux des réseaux sociaux.

Contrairement aux méthodes de trading traditionnelles, qui reposent souvent fortement sur l'intuition humaine et l'analyse technique basique, Degen AI traite rapidement des montagnes de transactions blockchain et de modèles du marché pour repérer des signaux cachés que la plupart des traders manquent complètement.

Pourquoi l'intelligence artificielle révolutionne-t-elle le trading de cryptomonnaies

Voici comment l'intelligence artificielle change fondamentalement le paysage du trading :

- Vitesse et efficacité :L'IA analyse instantanément de grands ensembles de données, plus rapidement qu'un trader humain ne le pourrait jamais.

- Reconnaissance de motifs :Repère les tendances et anomalies du marché cachés sur des milliers de paires de trading.

- Gestion des risques :Identifie les menaces et les irrégularités potentielles avant qu'elles ne déclenchent un chaos sur le marché.

Edgen AI ne se limite pas aux analyses. Il intègre égalementl'analyse des sentiments sociauxpour compléter le tableau, révélant les forces émotionnelles et narratives derrière les mouvements des prix.

Selon le Blockchain Council, l'IA transforme le trading algorithmique en cryptomonnaie en permettant l'optimisation en temps réel des stratégies, la détection d'anomalies et une automatisation plus intelligente, devenant ainsi un actif essentiel dans les environnements de trading modernes.

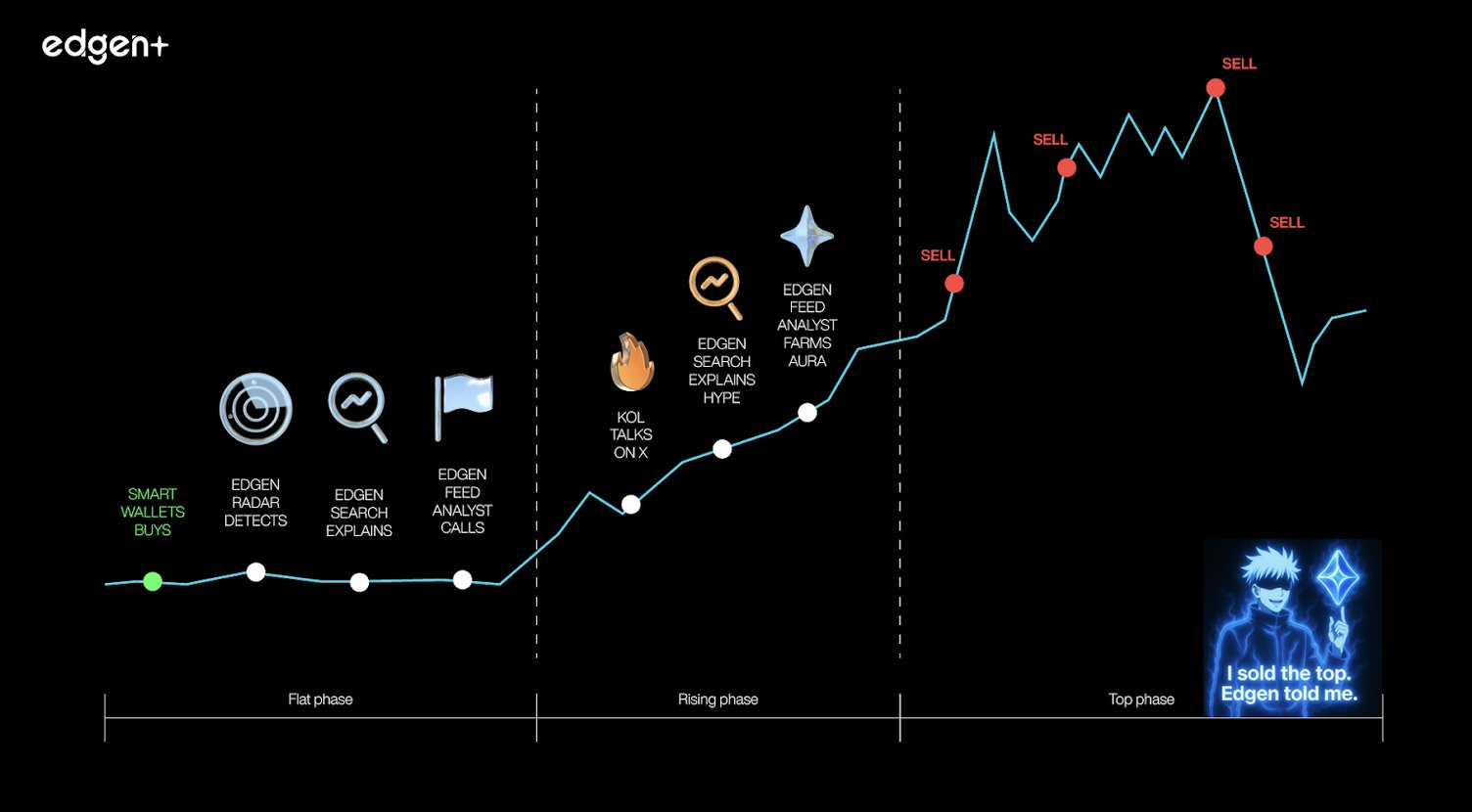

Souhaitez-vous explorer comment Edgen analyse les signaux ? Consultez Edgen Radardécouvrir ce qui est actuellement à la mode sur les marchés cryptos.

Comment Edgen AI génère des alpha

Comprendre le trading Alpha

Dans le trading, « Alpha » signifie battre le marché et trouver des opportunités que les autres ignorent ou ne connaissent pas encore. Si vous suivez uniquement les tendances du marché, vous n'êtes qu'un autre suiveur. Avec l'intelligence artificielle, vous anticipez les tendances avant qu'elles ne se concrétisent.

Les signaux Alpha d'Edgen AI

Degen AI identifie les opportunités alpha en analysant :

- Premiers mouvements de portefeuille intelligentRepérez les grandes achats et ventes avant qu'elles n'affectent les prix.

- Modèles de blockchainDétecter les tendances émergentes sur la chaîne qui indiquent des changements de prix.

- Corrélations dans les données de marchéAffiner les prévisions de trading pour une précision maximale.

Curieux des signaux riches en alpha ? Rendez-vous sur leEdgen Searchscanner les actifs par volume, sentiment ou activité sur la chaîne.

Des stratégies de trading alimentées par l'IA avec Edgen AI

Edgen AI utilise des stratégies diverses optimisées par une analyse pilotée par l'intelligence artificielle :

- Suivre les tendancesCyclant les tendances haussières ou baissières de manière stratégique.

- Réversion à la moyenneIdentifier les actifs qui s'écartent de manière significative des moyennes historiques.

- ArbitrageProfiter des écarts de prix entre les échanges.

- Le trading par momentumSauter sur les jetons en mouvement rapide avant que les prix ne se stabilisent.

Ce sont des outils puissants, mais Edgen AI les rend plus intelligents en les combinantdonnées de marchéavecle sentiment socialCela permet d'obtenir des informations basées sur des récits, aidant les traders à agir avant que le buzz ne atteigne son pic.

Vous pouvez explorer le Feedpour voir comment les récits et le sentiment en temps réel influencent les conditions du marché en direct.

Pourquoi les données sur la chaîne et sociales sont-elles essentielles pour le trading d'IA

L'Importance des données sur la chaîne

Les données sur la chaîne incluent des activités critiques du blockchain telles que :

- Enregistrements de transactions.

- Les mouvements du portefeuille intelligent indiquant une accumulation ou une pression de vente.

Edgen AI excelle dans l'analyse de ces informations blockchain, mais Edgen AI pousse le trading plus loin en ajoutant un contexte critique issu de l'ambiance sociale et des récits.

Le rôle crucial du sentiment social

Le marché cryptographique est plus que jamais guidé par des récits—memecoins, les tendances des NFT et les tweets des influenceurs peuvent tous déclencher des hausses de prix. Edgen AI surveille :

- Hype communautaire.

- Le sentiment des influenceurs.

- Suivi des mots-clés et des tendances (mèmes)

Cette prise de conscience aide les traderssuivre la vague du récitavant qu'il ne s'écrase. Le Radarest un outil très utile pour identifier où la hype sociale est à son maximum.

L'avenir du trading crypto piloté par l'IA : Edgen AI

L'avenir de la crypto est informé par les données et conscient des récits. Les traders réussis de demain utiliseront des outils combinant précision quantitative et analyses qualitatives.

Intégration du trading en intelligence sociale avec l'IA

L'écosystème de trading à la prochaine génération intègre les analyses sur la chaîne de Edgen AI avec son intelligence sociale, permettant aux traders de :

- Réagissez instantanément avec des alertes de trading basées sur des données en temps réel.

- Obtenez des informations à partir des tendances sociales et des avis des influenceurs, et non seulement des données blockchain.

- Automatisez les décisions de trading pilotées par l'IA, réduisant ainsi les erreurs liées au trading émotionnel.

Principales tendances du trading crypto alimenté par l'IA

Les progrès futurs en intelligence artificielle se concentreront sur :

- Analyse en temps réelL'IA interprète instantanément les changements du marché, réduisant ainsi considérablement les retards de réaction.

- Gestion automatisée des fondsDes stratégies dynamiques, entièrement automatisées, pilotées par l'analyse en temps réel de la sentiment social et des marchés.

- Poussé par le socialTokenonomieImplantation communautaire soutenue par des incitations et récompenses basées sur l'intelligence artificielle.

- Le système « Aura » d'Edgen AILes utilisateurs apportent leurs perspectives, affinant ainsi la compréhension de l'IA sur l'humeur du marché et améliorant l'intelligence collective en matière de trading.

Explorez comment vous pouvez contribuer et àen savoir plusclick here!

Pourquoi cela est-il important pour les traders de cryptomonnaies

En combinant la puissance analytique d'Edgen AI et son intelligence émotionnelle, les traders ne sont plus en retard sur les mouvements du marché. Ils anticipent activement les opportunités, évitent les pics de prix manipulés et profitent des vagues rentables dès le début.

Cette combinaison améliore et redéfinit le trading. Les traders qui adoptent ces outils auront un avantage indéniable par rapport aux traders manuels.

FAQ : Questions fréquentes sur le trading avec Edgen AI

Quel avantage l'IA offre-t-elle aux traders de cryptomonnaies ?

L'IA analyse rapidement de grandes quantités de données, révélant des tendances cachées et optimisant l'exécution des échanges, dépassant nettement les méthodes de trading manuel.

Pourquoi l'analyse des sentiments sociaux est-elle importante ?

Les prix des cryptomonnaies sont de plus en plus influencés par les récits sociaux, les influenceurs et les cycles de hype. Edgen AI capte ces tendances en conjonction avec les données sur la chaîne pour des analyses complètes.

Peut-être que l'intelligence artificielle remplacera-t-elle complètement les traders humains ?

Pas entièrement. Mais l'IA améliore grandement la prise de décision, en éliminant les points aveugles et en automatisant les analyses complexes. Les meilleurs traders combinent les informations fournies par l'IA avec leur expérience personnelle.

Comment l'intelligence artificielle aide-t-elle les traders à gérer la volatilité du marché ?

L'IA fournit des analyses du marché en temps réel, en suivant les données sur la chaîne, les schémas de trading et l'opinion du marché, aidant les traders à adapter rapidement leurs stratégies lors de conditions volatiles.

Comment puis-je commencer à utiliser l'IA pour le trading de cryptomonnaies ?

Utilisez Degen AI pour des analyses quantitatives puissantes et Edgen AI pour des insights sur le sentiment social. Ensemble, ces outils vous aident à maximiser les opportunités et à exécuter des transactions avec confiance.

Déverrouiller le plein potentiel de l'intelligence artificielle dans le trading de cryptomonnaies

L'avenir appartient à ceux qui adoptent l'intelligence artificielle.

Edgen AI allie précision des données et intelligence narrative, vous donnant le pouvoir de prédire, d'agir et de gagner sur le marché.

AvecDegen AIrepérer les mouvements de l'argent intelligent etEdgen AIcapturer l'opinion du communautaire, vous obtenez un système hybride conçu pour le trader moderne. Quel que soit votre statut deà enjeux élevés dégenou un stratège prudent, c'est la meilleure façon de trader.

La révolution de l'IA dans le crypto est déjà là. Êtes-vous prêt à suivre la vague ?

Commencez à explorer les opportunités Alpha maintenant

Accédez aux données en temps réel sur la chaîne, aux actifs en tendance et aux analyses de sentiment puissantes.

Discover what’s hot on Edgen Radar!

Investir, enfin, tu n'es plus seul.

Essaie Ed gratuitement. Sans carte, sans engagement.