이 빌어먹을 시장에 뒤처지기 싫어서 에드진을 만들었다.

저는 전문 작가가 아닙니다. 솔직히 말해서, 제가 이 글을 써야 할지조차 확신하지 못합니다. 하지만 저는 에드진(Edgen)을 왜 만들었는지 직접 말씀드리고 싶었습니다. 왜냐하면 이건 제게 개인적으로 매우 중요한 일이기 때문입니다.

나도 아마 너와 같은 이유로 암호화폐에 뛰어들었을 거야did:나는 자유를 원했고, 성공할 기회를 원했으며, 솔직하게 말해서 돈을 벌고 싶었어요. 그런 건 별로 잘못된 일이 아니에요.

나는 암호화폐 거래를 해 왔다년도지금은 내가 이 분야에 익숙하지 않다고 말할 수 없고, 그곳에서 많은 즐거움을 느꼈다. 나는 Everest Ventures Group (EVG)에서 일해 왔으며, 강력한 DeFi 및소셜피(소셜피)아시아의 프로젝트, 버블 기간과 베어 마켓을 넘어서며 구축한 전문가 네트워크를 저는 생각합니다.상당히 괜찮아대부분의 기준에 따르면, 저는 제가라고 말할 수 있습니다.상당히 잘 연결되어 있다공간에서, 나는 솔직하게 말할 수 없다.

하지만 최근에는 나도 무력감을 느끼기 시작했다. 수년 동안, 암호화폐 거래가 보이는 것보다 훨씬 더 어려운 일임을 배웠다. 심지어 상승장에서도 그렇다.실제로 "클라운"암호화폐 시장에서. 당신이 3시에 포트폴리오를 확인하면서 자신이 옳았다는 것을 알게 되었지만, 이미 너무 늦게 진입했다는 사실을 느낀 적이 있다면, 내가 말하는 것을 정확히 이해할 것이다.

오늘날 암호화폐는 전보다 훨씬 빠르게 움직이고 있다. 너무나 빠르게.와이아아아너무 빠르다. 매일 수백 개의 토큰이 나타난다.메모코인시간당 100배로 오르는 것, 밤새 달라지는 서사, 내가 들어본 적 없는 고래 지갑의 숨은 신호들... 소음은 멈추지 않는다. 당신이 얼마나 경험이 풍부하거나, 연구나 네트워크가 얼마나 좋다고 해도 따라잡기는 불가능하다.

좋은 거래를 놓쳤고, 기회를 놓쳤으며, 항상 뒤처지려는 싸움을 하고 있었다. 나의 자원과 관계로도 앞서나가려는 것은 너무나 지치는 일이었다. 나는 특별히 나쁜 트레이더라고 생각하지 않는다.

이제는 결혼해서 자녀도 있고, 나이 들어서 지치고 있다. 그리고 나처럼 넓은 인맥과 오랜 경험을 가진 사람이 이렇게 힘들어한다면, 일반적이면서 더 겸손하고 첫 번째로 거래를 시작하는 트레이더들에게는 더욱 그렇다는 것을 안다.해야 한다더 강하게 느끼게 되며, 때로는 드라마틱한 결과를 초래하기도 한다.

암호화폐는 금의 티켓이었고, 모든 사람을 평등하게 해줄 것이라고 기대되었습니다. 누구든 자신이 누구인지, 처음에 얼마나 많은 돈을 가지고 있던지 상관없이 공정한 기회를 제공하는 것이었다는 것입니다. 하지만 현재 우리가 사는 현실은 전혀 공정하지 않습니다. 부당하다고 느껴집니다. 그래서 저는 우리가 그런 상황을 바꾸기 위해 무언가를 만들어야 한다고 결심했습니다.

나는 작은 사람을 위해 Edgen을 만들었어요 (왜냐하면 저는어느 정도하나입니다

에드진은 내가 미쳐버리지 않기 위해 정말로 필요했던 것이었습니다. 저는 암호화폐의 모든 곳, 크립토 트위터, 스마트 지갑, 체인 내 신호, 개발자 활동, 최신 벤처 캐피탈에서 즉시 집단 지능을 모으는 도구를 원했습니다.모금하고,내게 명확하고 빠르게 전달합니다.

shitposts와 러그를 통과시킬 수 있고, 너무 늦기 전에 진정으로 중요한 것을 보여주는 것이 무엇인가.

그래서우리는 누구나 사용할 수 있을 만큼 간단하지만, 충분히 지능적인 인공지능 기반 시장 정보 플랫폼을 구축했습니다.실제로 도움이 된다모든 거래에서 수익을 얻을 수 있다고 보장해 드릴 수는 없습니다. 누구도 그런 것을 약속할 수 없으며, 그렇게 말하는 사람은 모두 당신을 속이고 있습니다. 하지만 제가 약속드릴 수 있는 것은 이제 절대 맹목적으로 거래하지 않을 것이라는 것입니다.

그래서우리는 시작부터 두 가지 간단하면서도 강력한 도구를 사용할 것입니다. 수많은 시간을 투자해 축적하고 정제한 특허 기반의 사회적 및 시장 데이터 덕분에, 엣지의 맞춤형 AI는 명확한 통찰력을 제공하는 데 뛰어나며, 이는 백업 자산 토큰을 연구하는 경우든 신규 토큰을 탐색하는 경우든 모두 해당됩니다.메모코인영향력 있는 시장 주체, 또는 최신 펀딩 거래.

엣지 검색:

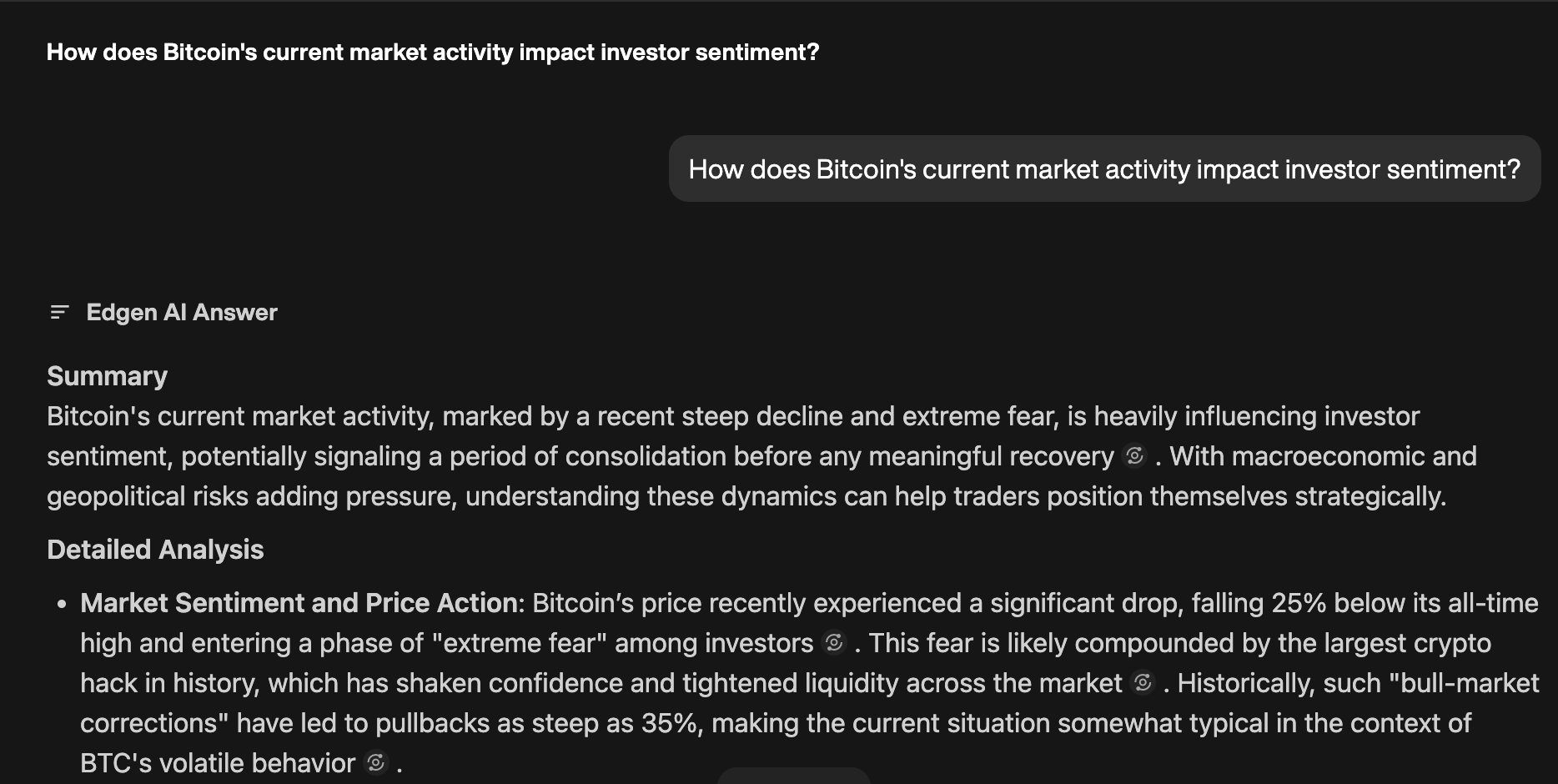

당신의 암호화폐 관련 질문이 복잡하거나 간단하든, 실시간 데이터를 통해 즉시 실행 가능한 통찰을 얻으세요. 더 이상 밤샘 뉴스 스트롤링은 필요 없습니다. 맞춤형으로 훈련된 LLM이 정확하게 소음을 제거하고, 전체 암호화폐 시장에서 신호와 기회를 즉시 파악합니다. 그리고 그 이상으로 주식 시장까지 확장됩니다.

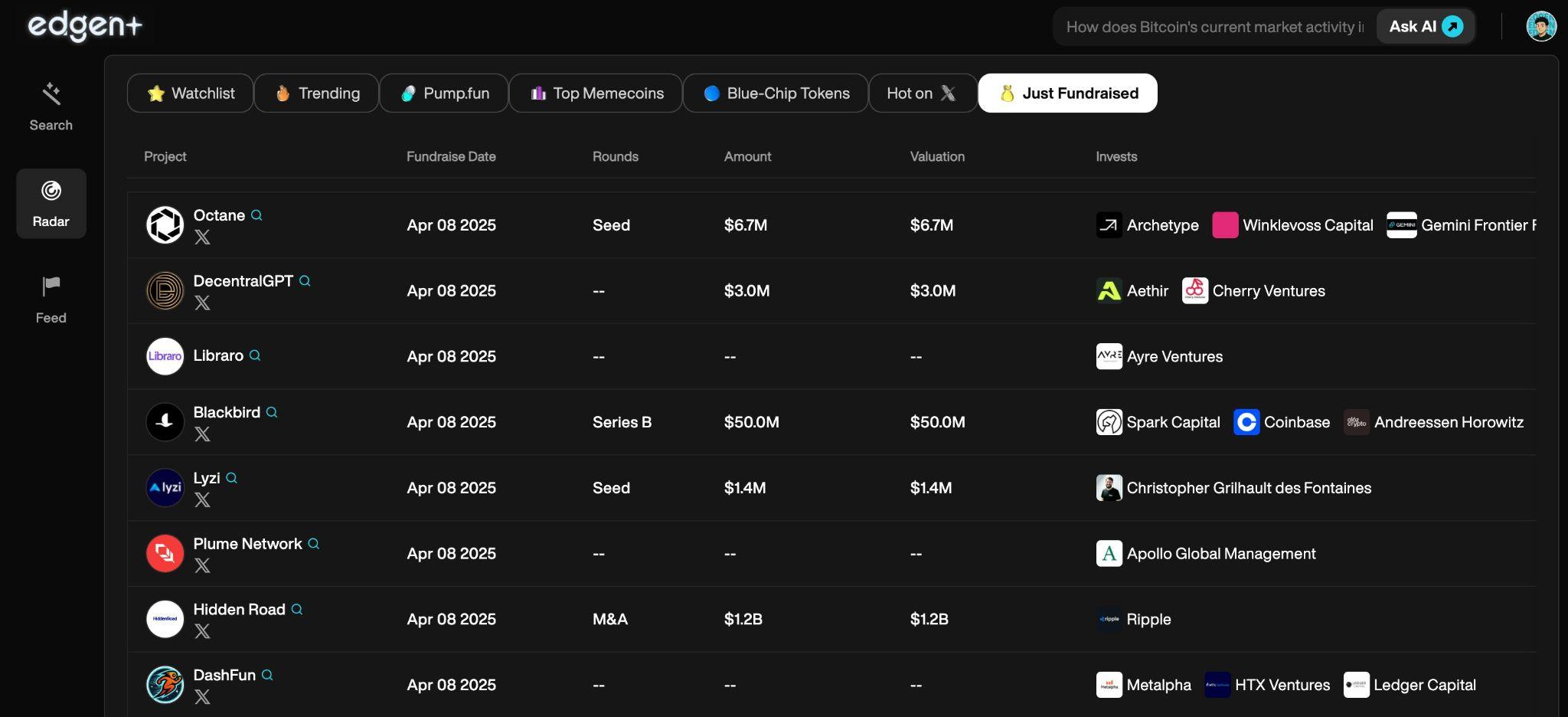

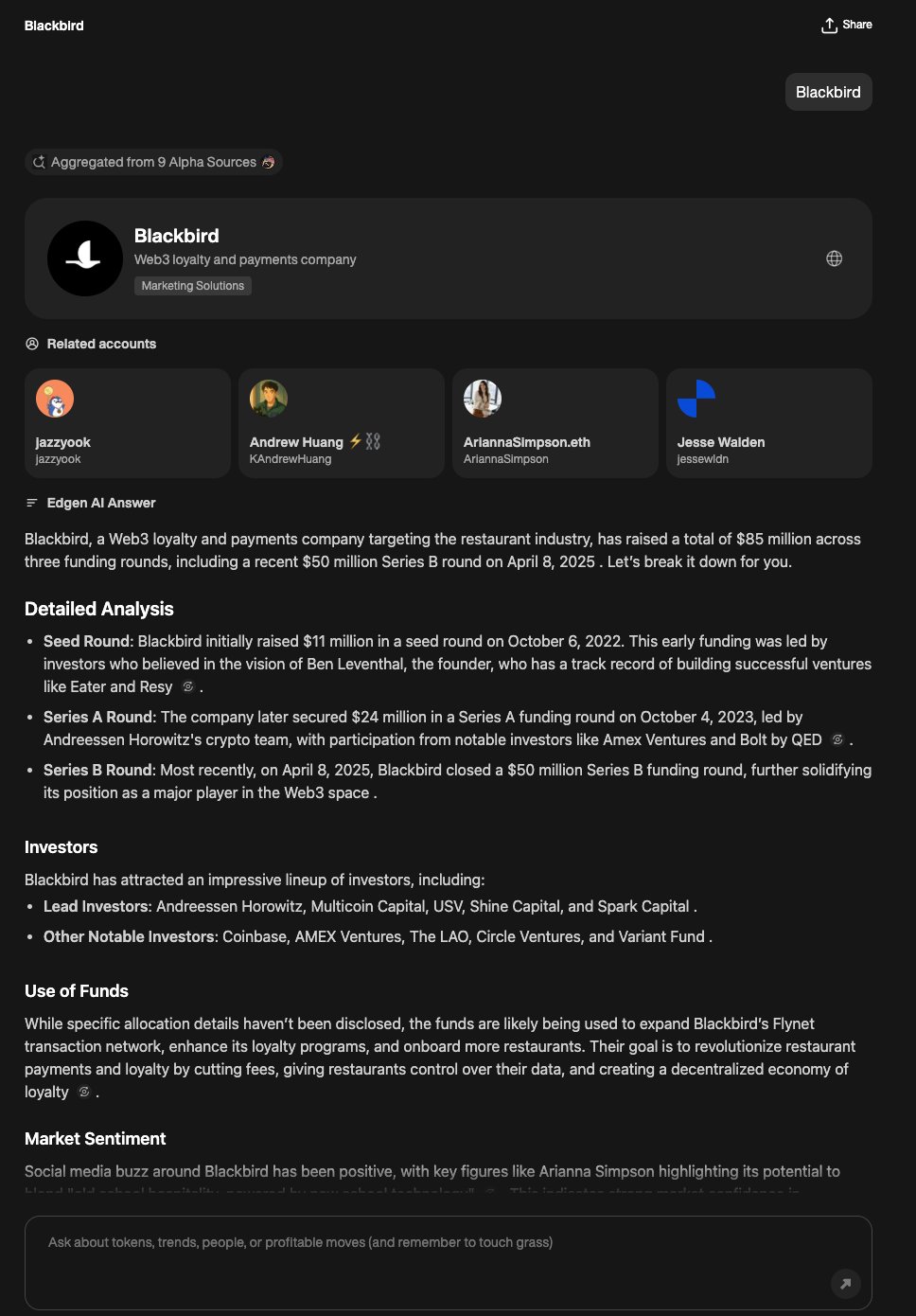

엣지언 레이더:

레이다는 당신의 개인 스카우팅 대시보드입니다. 이는 다양한 토큰, 범부동산,펌프.펑졸업생, 마oonshot 토큰, 인기 토큰,등 등그리고 스마트 지갑의 구매 및 판매, 커뮤니티의 열기, 또는 주요 영향력 있는 인물들이 토큰을 팔거나 따라오는 등 흥미로운 일이 발생할 때 알림을 제공합니다.

시작해 보세요! 검색부터 시작하세요! 당신의 어리석은 암호화폐 질문들을 물어보세요. 받게 될 답변은 혹시 가혹하게 솔직할 수도 있고, 혹은 완전히 웃기고 말 수도 있어요 😂

우리는 곧 더 많은 도구들을 선보일 예정입니다. 예를 들어 피드와, 특히 오라가 있지만, 그 이야기는 다른 날로 미루겠습니다. 하지만 여기서 조금은 힌트를 줄 수는 있습니다.

에이aura: 당신이 진정으로 신뢰할 수 있는 사람을 알아보기

이제 여기서 멈추겠습니다: Aura는 토큰이 아닙니다. 그것은 명성 시스템입니다. 하지만 거의 같은 역할을 하죠, 왜냐하면 이 경제에서는 명성이 화폐이기 때문입니다. Aura는 당신의 알파 점수 증명입니다.

에드진 커뮤니티의 누군가가 트위터에서 정확한 시장 예측, 등장하는 트렌드를 포착하거나 실제로 맞아떨어지는 예측과 같은 가치 있는 통찰을 공유할 때마다 그들은 어우라(Aura)를 수확하고, 에드진의 AI를 매일 더 똑똑하게 훈련시킵니다. 시간이 지남에 따라 어우라는 누구가 신뢰할 수 있는지, 지속적으로 진정한 알파를 제공하는 사람인지, 그리고 당신이 주목해야 할 사람인지 정확히 보여줍니다.

즉, Edgen은 당신이 이해하도록 도와줍니다무슨 일이 일어나고 있는 거야그러나 이해할 수도 있다누구를 신뢰해야 할까요이 소음이 많은 시장에서

이전에 축적한 독점적이고 특허받은 데이터 외에도, Aura는 다른 어떤 곳에서도 복제할 수 없는 방식으로 우리의 전문적이고 목적에 맞게 설계된 LLM을 점점 더 지능적으로 만들 것입니다.

저와 함께한 여정을 시작한 이들 중 일부는 저를 아시겠지만OpenSocial에지언은실제로는주요 업그레이드 fromOpenSocial동일한 핵심 비전에 기반하여, 사회적 자본과 영향력에 실제적이고 측정 가능한 가치 및 진정한 소유권을 부여하는 것입니다. Edgen을 통해 우리는 이 사명을 더욱 앞당기고, 사회적 통찰력과 집단 지능을 명확하고 실행 가능한 시장 알파로 전환하고 있습니다. 그것이 바로 모든 것입니다.OpenSocial그것은 되고자 하는 것이며, 그 이상이다. 오늘날의 시장에 비추어 보면 자연스러운 진화이다.

엣지엔은 대형 시장 균형 조절자입니다.

나는 암호화폐가 단지 내부자나 항상 온라인인 사람들만을 위한 것이 되어서는 안 된다고 생각해서 Edgen을 만들었습니다. 물론 모든 사람이 항상 수익을 낼 수 있는 것은 아닙니다. 그것은 현실적이지 않습니다. 하지만 올바른 정보를 명확하고 빠르게 전달한다면, 누구든 공정한 기회를 가질 수 있습니다.

에드진이 암호화폐 거래에서 큰 균형 잡는 힘이 되기를 바라는 것이 제 꿈입니다. 우리가 올바르게 일한다면, 전 세계의 다양한 배경을 가진 일반 트레이더들은 계속해서 뒤처지는 느낌을 받지 않을 것입니다.

그렇게 제 이야기입니다. 저는 월스트리트 배경을 가진 화려한 트레이더는 아닙니다. 그리고 저는확실히 안 했어이렇게 완벽하게 써줘. 나는 단지 사랑하는 사람일 뿐이야암호화폐, 및더 나은 것을 원했다.

그래서 이것이 내가 Edgen을 만든 진짜 이유입니다. 제가 직접 필요했기 때문입니다. 그리고 저는 이것이 당신에게도 도움이 될 것이라고 믿습니다.

기회를 주셔서 감사합니다.

시안 타오, 에드진 공동 설립자

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.