嘉年华公司(CCL) 2026年第一季度回顾:衡量去杠杆化势头与燃料波动性

买入 | 目标价 38.00 美元 | 59% 上涨空间 | 首次覆盖

“市场正在以9.5倍的远期市盈率评估一个拥有创纪录预订量、恢复派息并已偿还100亿美元债务的76亿美元EBITDA机器。”

当前价格:23.92 美元 · 2026年3月19日 · Edgen Research

投资摘要

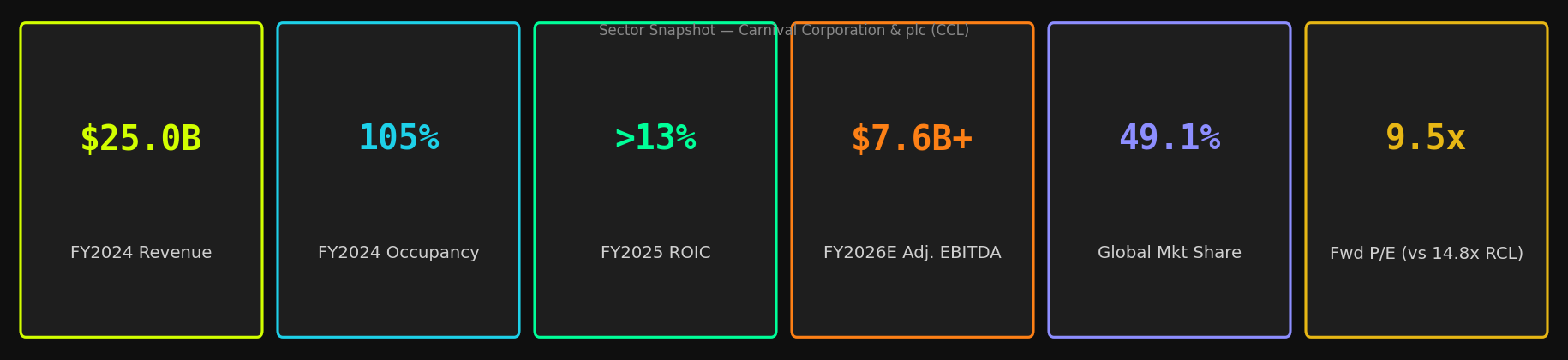

我们首次覆盖嘉年华公司(CCL),给予“买入”评级,12个月目标价为38.00美元,较当前23.92美元的价格有59%的上涨空间。市场严重低估了CCL的转型:该公司已偿还超过100亿美元的峰值债务,恢复了股息,启动了10亿美元的股票回购,并在2025财年实现了72亿美元的创纪录EBITDA,但其股票仍以9.5倍的远期市盈率交易。作为全球最大的邮轮运营商——占据全球邮轮收入的约49%——该公司正在进入股东回报的新阶段,然而估值屏幕却显示这仍是一个困境中的复苏故事。事实并非如此。

该投资论点基于三大支柱。首先,需求结构性强劲:2026年及以后的预订曲线处于历史最高水平,定价处于历史峰值,客户存款余额在2026财年第一季度创下73亿美元的纪录——这是一个已大幅降低风险的领先收入指标。其次,去杠杆化正在加速。截至2025财年末,净债务与EBITDA比率为3.4倍(获得惠誉投资级评级),管理层设定的到2026财年末低于3.0倍的目标是可实现的,并将进一步提升评级。第三,与皇家加勒比(主要的看跌论点)的盈利能力差距正在缩小。2025财年营业利润率扩大250个基点,ROIC近二十年来首次超过13%,且不断增长的高利润船上收入(2026财年第一季度同比增长11%)是损益表尚未完全体现的结构性利好。

看涨情形

• 创纪录的预订量和历史高价提前锁定2026年收入——客户存款达到创纪录的73亿美元

• 2026财年第一季度船上收入同比增长11%,加速增长,是利润率最高的收入流,也是主要的结构性利润率扩张驱动因素

• 截至2026年,年度利息支出较峰值减少超过7亿美元——随着债务偿还,直接流入净利润

• 公司简化(DLC统一投票于2026年4月17日进行)可能释放重新评级和更广泛的机构投资者准入

• 独家目的地“庆典岛”(巴哈马)——前5个月接待100万客人,有望在2026年达到200万,到2028年达到400万

看跌情形

• 未对冲的燃料策略使收益直接受油价飙升影响——这是2026年初负面情绪的关键来源

• 2026年加勒比地区行业产能整体增加约10%可能对嘉年华核心市场的定价能力构成压力

• 2026年3月的IT系统故障导致全船队登船延误——运营风险真实存在且声誉代价高昂

• 忠诚度计划向“嘉年华奖励”(2026年9月)的过渡引发了VIFP会员的强烈客户反弹

行业概览

全球邮轮旅游市场在2026年达到945亿美元的总目标市场(TAM),到2034年以10.2%的复合年增长率增长,这得益于新兴市场可支配收入的增加、全包式价值主张已被证明的韧性以及体验式旅行的长期需求。嘉年华公司在这个结构性增长的寡头市场中是无可争议的领导者,占据全球邮轮收入的约49.1%——在规模上超过其两大主要竞争对手皇家加勒比(RCL,约33%)和挪威邮轮控股(NCLH,约18%)的总和。

财务概览

嘉年华公司在2025财年(截至2025年11月30日)实现了公司历史上最盈利的一年。创纪录的45亿美元营业收入和72亿美元调整后EBITDA——营业利润率同比扩大超过250个基点——标志着从2020-2022年的生存资产负债表危机中完全逆转。2026财年第一季度的业绩报告强化了这一势头:收入达到58.1亿美元(同比增长7.5%),调整后每股收益为0.13美元,较市场普遍预期的(-0.02美元)高出0.15美元,所有超出预期的表现均由运营执行驱动,而非一次性项目。

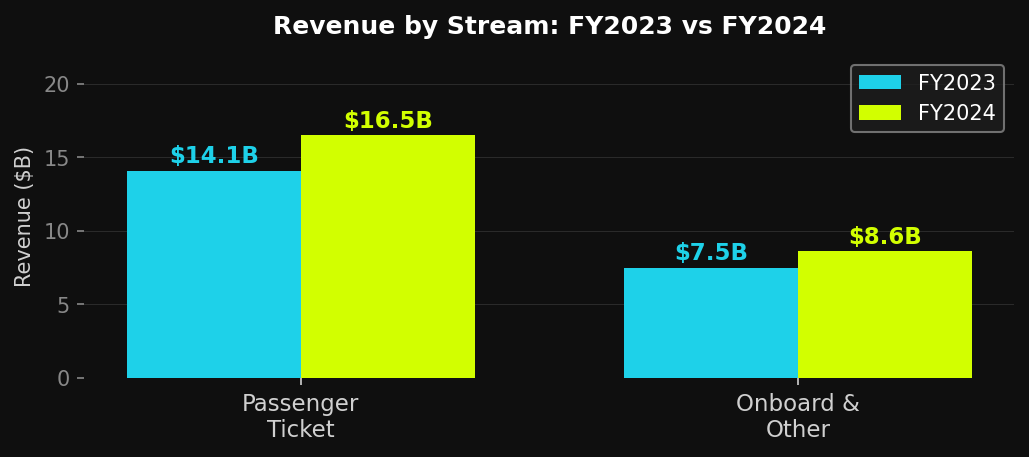

收入构成正在结构性改善。船上及其他收入(其利润率明显高于船票销售)在2026财年第一季度同比增长11%,而船票收入增长5.8%。船上收入目前占邮轮总收入的34%,且正在加速增长。这种相对于船票收入增长的扩大溢价是一个市场尚未完全估值的关键盈利质量信号。随着嘉年华公司继续投资于特色餐饮、娱乐和独家目的地体验,这一收入流将成为未来利润率扩张的主要驱动力。

主要财务指标

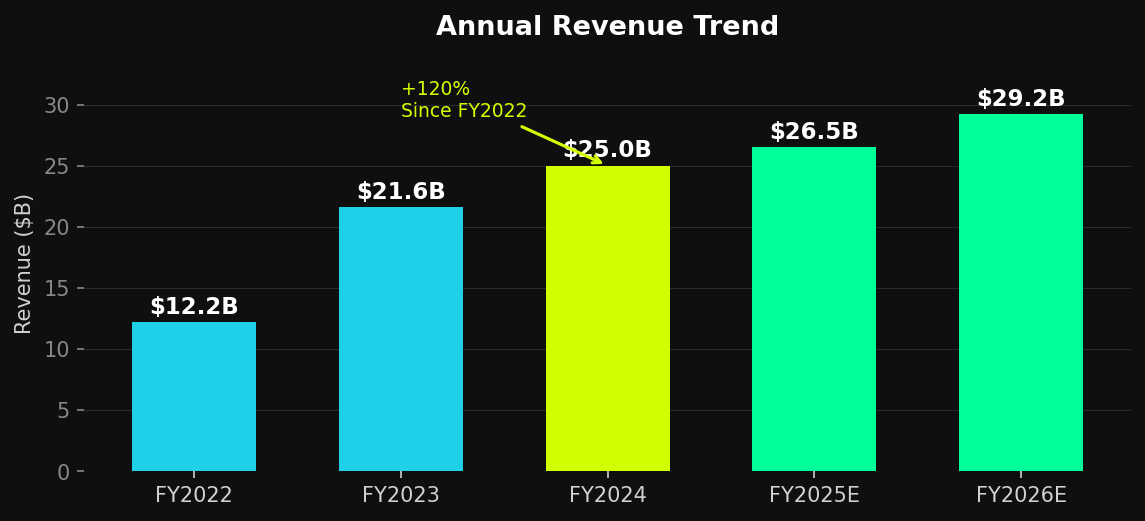

指标 | 2022财年 | 2023财年 | 2024财年 | 2025财年(预期) | 2026财年(共识) |

|---|

总收入(十亿美元) | 12.2 | 21.6 | 25.0 | ~26.5 | ~29.2 |

客运票务收入(十亿美元) | — | 14.1 | 16.5 | ~17.5 | ~19.3 |

船上及其他收入(十亿美元) | — | 7.5 | 8.6 | ~9.0 | ~9.9 |

营业收入(十亿美元) | — | 2.0 | 3.6 | 4.5 | ~5.2 |

调整后EBITDA(十亿美元) | — | — | ~5.8 | 7.2 | 7.6+ |

净利润(十亿美元) | (0.07) | (0.07) | 1.92 | ~3.1 | ~3.45 |

调整后EPS(美元) | — | — | — | ~$2.25 | ~$2.48 |

入住率(%) | 75% | 100% | 105% | 105%+ | ~105% |

ROIC | — | — | 推荐阅读  How to redeem airline miles without wasting themThe single biggest mistake with miles is redeeming them for the easy stuff: gift cards, merchandise, seat upgrades at the gate. Do that and each mile is worth about one cent. Redeem the *same* miles for flights, especially long-haul or premium-cabin flights, and they're often worth two to five cents each, sometimes more. So the real skill isn't earning miles; it's not throwing away their value at the finish line. Here's how to actually use them. A mile has no fixed price; its value depends entirely on what you redeem it for. The way to judge any redemption is simple math: (cash price of the flight) ÷ (miles it costs) = cents per mile. If a flight costs $400 or 20,000 miles, that's 2 cents a mile, a solid deal. If a $90 flight costs 18,000 miles, that's half a cent, which is terrible; pay cash and keep the miles. Run this check before every redemption. It instantly separates a great use from a waste, and it's the one habit that makes miles worth having. As a rule of thumb, most major ai Long-term vs short-term financial goals (and how to plan both)The difference comes down to one thing: time. A short-term goal is money you'll need within roughly three years (an emergency fund, a trip, a wedding, next year's tax bill), so it has to be *safe and reachable*. A long-term goal is five-plus years out (retirement, a house down the road, a kid's education), so it can take market risk, because time smooths the bumps out. Get that match right and you've done most of the work. It's not the size, it's the deadline. A $2,000 goal you need in six months is short-term; a $2,000 goal you won't touch for fifteen years is long-term, and they belong in completely different places. This is the part that actually matters, and where people lose money without realizing it. Short-term money should not be in the stock market. If your emergency fund is in stocks and the market drops 20% the same month your car dies, you're selling at the worst possible time. Short-term goals go somewhere stable and accessible, and a high-yield savings account is the clas Should you buy a house now or wait? How to actually decideThe honest answer: buy when you'll stay put for at least five years and you'll still have an emergency fund left after the down payment. Otherwise, waiting (and renting) is often the smarter money move, not the weaker one. "Rent vs buy" isn't a math problem with one right answer, and it's almost never really about timing the market. It's about your *life*, in three questions. Before the three questions, here's the mid-2026 backdrop — because "now or wait" usually hides a bet on rates and prices, and the data says that bet is a coin flip. The picture: mortgages are still pricey, prices have gone flat (more than half of the 20 big metros saw year-over-year declines in March), and the cheap-money era hasn't returned. So "buy before it runs away" and "wait for the crash" are *both* weak arguments right now. The whole "wait for rates to drop" plan rests on the Fed, and the Fed is split down the middle. In its June 2026 projections, policymakers were divided: 8 expected no change this year,  How to set financial goals you'll actually hitA financial goal you'll actually hit has three things a vague wish doesn't: a number, a date, and one automatic move that happens whether or not you remember it. "Save more" is a wish. "$6,000 in a separate account by next December, $500 auto-transferred on payday" is a goal. The gap between those two sentences is the reason most goals quietly die, and it has almost nothing to do with willpower. Key Takeaways A real financial goal answers three questions: how much, by when, and what for. Drop any one and it stops working. "Pay off debt" has no number and no date, so there's nothing to aim at or measure, while "$8,000 of card debt cleared in 18 months" tells you exactly whether you're on track and the day you're done. The "what for" matters more than people expect. A goal tied to something real (a buffer so a bad month isn't a crisis, a deposit on a first place) survives the months when motivation dips. In our experience reading how people actually use a money tool, the goals that get  Your RSUs Just Vested. Here's What a Money Tool Surfaces First.You just had a big RSU grant vest. Congratulations — and now the awkward part: a six-figure pile of your own company's stock, a vague sense you should "do something," and no one actually telling you what. An advisor, a spreadsheet, and a piece of software each handle this moment differently. Here's what a modern money tool surfaces in a moment like this — using Ed as a worked example — so you can decide what kind of help actually fits. Key takeaways You connect your brokerage and bank through read-only aggregation, so the tool can read balances but can't move a dollar. Ed's framing is simple: precise about your money, blind to your identity. Instead of sorting your lattes into categories, Ed opens on a single Financial Reality Check — a read on whether your money could survive a bad month. For a lot of high earners, that one number lands harder than any budget, because it answers a question the other apps never ask. (If the Reality Check is the numbers side, your money type is the beha SpaceX 6/12 挂牌估值 1.77 万亿美元 冲向 5 万亿美元的 13 个关键日期SpaceX 将于本周四(6 月 12 日)正式在 Nasdaq 挂牌,定价每股 135 美元,估值约 1.77 万亿美元,为史上最大规模的 IPO。相比华尔街热议的"冲向 5 万亿美元"多头目标,真正主宰未来一年股价走势的,是一份结构异常清晰的供给释放时间表。 据 Bloomberg 与 Reuters 报道,本次 IPO 订单簿需求达 2,500 亿美元,约为实际发行量的 3.5 至 4 倍。Goldman Sachs 领衔承销,连同其他 22 家顶级投行共同操盘。值得关注的是,Day 1 仅有 4.2% 股份实际流通交易;Musk 本人持股锁仓长达 366 天,其他内部人须等到第 180 天才完全解锁。换言之,接下来半年市场上可实际交易的股票极为有限,而这份解锁时间表是公开披露的。把这份日历看明白,等于提前掌握下个季度大部分财经评论还在试图解释的市场结构。 近期关于 SpaceX IPO 的报道,有两个说法在仔细审视后并不成立。 第一,所谓"指数基金将被迫一次性大举买入 SpaceX"并非事实。Nasdaq 确实开启快速纳入机制,允许 SpaceX 在挂牌后 15 个交易日内纳入 Nasdaq 100,但同一条规则对低流通标的设下权重上限:以流通量的 3 倍为顶。对流通比例仅 4.2% 的 SpaceX 而言,有效权重约为市值的 12.6%。分析师对整个纳入过程的净流入估算,落在 100 至 200 亿美元之间,属于持续性顺风,而非一次性事件。 第二,S&P 500 纳入不会很快发生。S&P Global 已明确拒绝为旗舰指数修改规则,SpaceX 最快也要等到 2027 年中之后才符合资格,且须先连续四季 GAAP 盈利。考虑到 Starship 一年烧掉 30 亿美元研发、公司营业利益仍为负值,最早实际纳入时点落在 2027 年下半,等于把规模最大的被动买盘事件推迟至 2026 年锁仓悬崖之后。投资这事,终于不用一个人了 免费试用 Ed。不用信用卡,不绑约 |