Le trading Alpha en crypto : comment l'IA révèle les signaux cachés du marché

Les marchés cryptos récompensent la vitesse et la précision

Le trading de cryptomonnaies évolue rapidement. Les opérations rentables dépendent fortement de la capacité à repérer clairement et tôt les tendances du marché. Les traders humains passent fréquemment à côté de signaux critiques en raison de la vitesse et de la portée limitées de leur analyse.

L'intelligence artificielle traite instantanément de grands ensembles de données, identifiant clairement les mouvements et les signaux du marché cachés avant que d'autres ne les remarquent.

Cela définit le « trading alpha » : voir clairement les opportunités du marché en premier et exécuter avant les concurrents.Edgen AIétablit cette nouvelle norme, en donnant aux traders des informations exploitables et opportunes.

Le trading sans IA laisse les investisseurs en retard. Voici pourquoi l'IA définit l'avenir du trading crypto et comment Edgen AI le rend accessible aujourd'hui.

Comprendre le trading Alpha en cryptomonnaie

Le trading alpha consiste à obtenir des perspectives claires et anticipées sur des opportunités rentables avant que la majorité n'en prenne conscience. Les marchés cryptographiques restent très volatils, fonctionnant en continu, ce qui exige une surveillance constante et précise.

L'IA fournit une analyse continue et en temps réel, clairement :

- Données sur la chaîne :Surveiller les transactions de la blockchain en temps réel.

- Tendances du marché :Identifier les schémas rentables avant qu'ils ne deviennent largement évidents.

- Sentiment social :Analyser les données de X (anciennement Twitter), Telegram, des sources d'actualité et des sujets tendances.

Contrairement aux outils d'analyse traditionnels, Edgen AI va au-delà des données historiques, révélant clairement l'humeur du marché actuel :

- Suivre les influenceurs clés (KOL) influents sur des plateformes comme X.

- Surveillance des transactions importantes des portefeuilles intelligents.

- Analyser «Pumpamentals« la dynamique sociale qui fait monter les prix des cryptomonnaies ».

Pourquoi Alpha Trading est plus important que jamais

Dans le Web3, les indicateurs financiers traditionnels offrent des perspectives incomplètes. Les marchés cryptographiques modernes reposent sur le sentiment social et les activités blockchain, visibles en temps réel.

- Achats et ventes intelligents :L'argent intelligent se déplace rapidement. L'IA repère instantanément leurs transactions regroupées.

- La perception des traders de détail :Les tendances sociales émergent rapidement. L'IA identifie et exploite ces tendances avant que la dynamique virale ne commence.

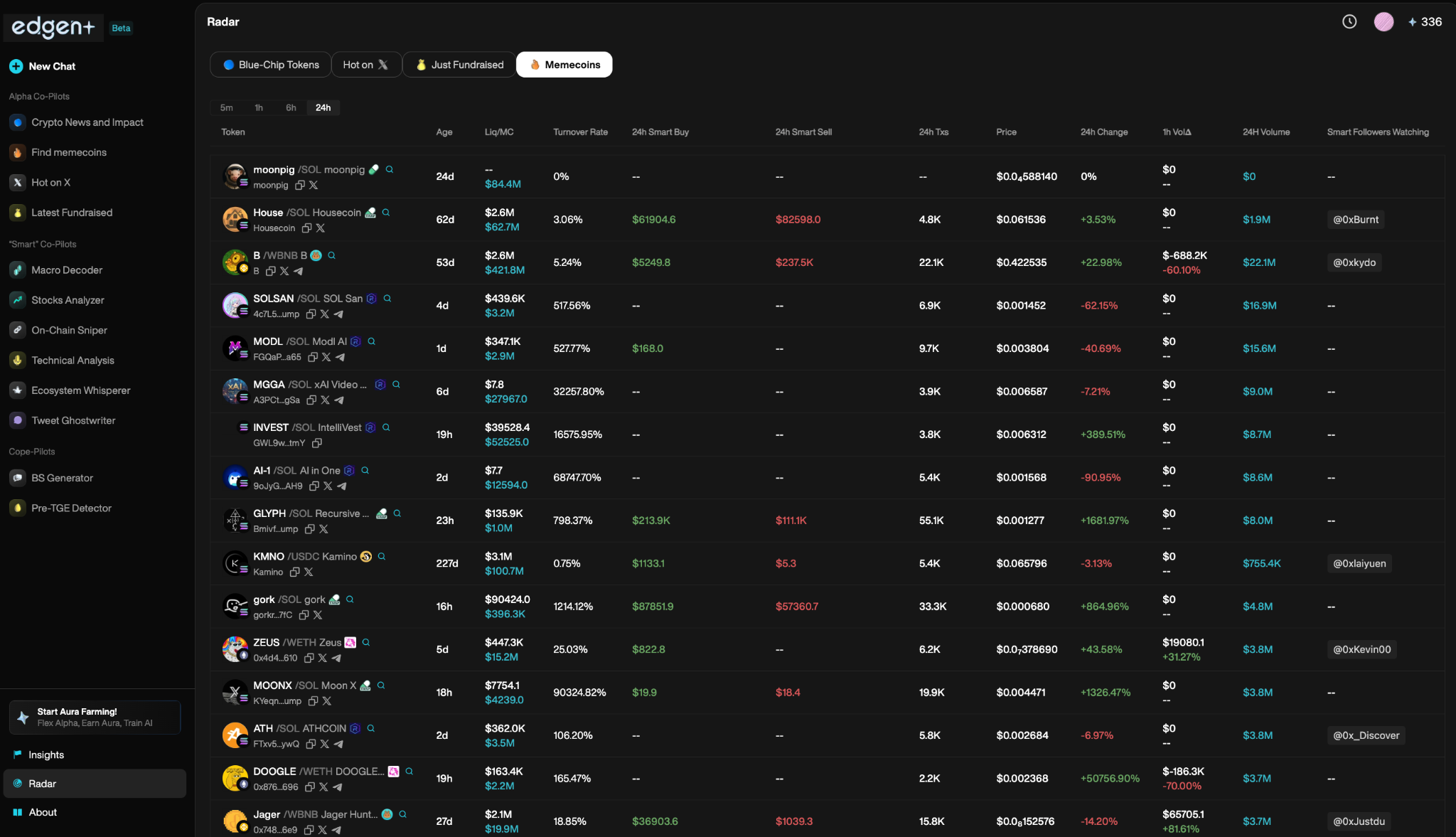

Edgen RadaretEdgen Searchassurer aux traders qu'ils repèrent immédiatement ces changements marquants sur le marché.

Comment l'IA révèle clairement des signaux de marché cachés

L'intelligence artificielle révolutionne le trading de cryptomonnaies, traitant instantanément des millions de points de données et capturant des signaux subtils que les traders humains ignorent.

1. Signaux de trading en temps réel avec l'IA

Edgen AI génère instantanément des signaux de trading clairs et exploitables en analysant :

- Évolutions des prix :Les schémas historiques indiquant des positions rentables.

- Variations du volume de trading :Détection immédiate des pics d'activité marchande anormaux.

- Dynamique des tendances sociales :Mesurer l'engagement de la communauté et l'excitation pour anticiper les mouvements de prix.

Edgen Radarvisualise clairement le paysage du marché social et technique pour des actions de trading précises.

2. Analyse de sentiment en temps réel

L'IA analyse en continu les données provenant de X et des médias, en lisant l'orientation du marché avant qu'elle n'affecte clairement les mouvements des prix.

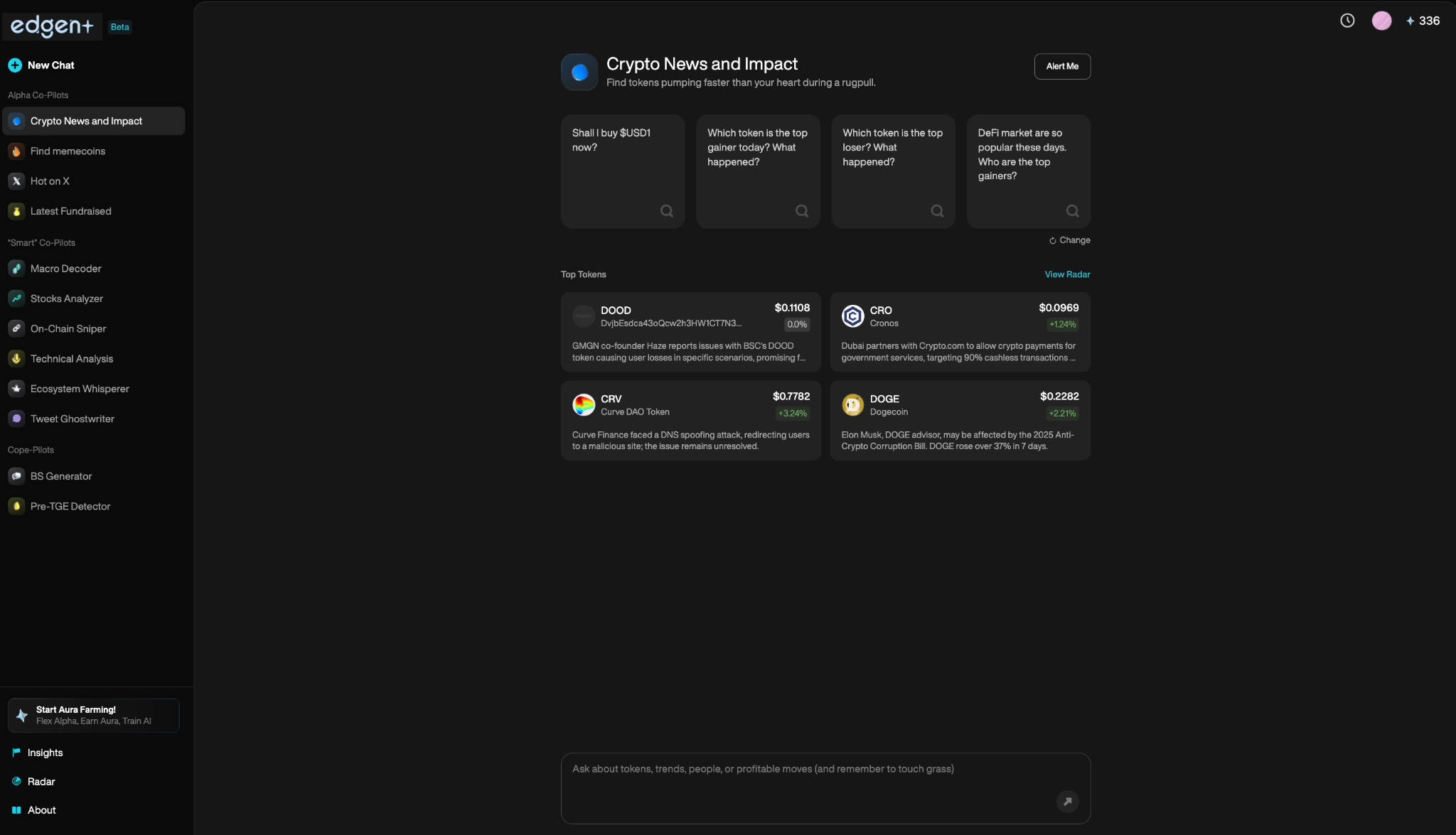

Les traders utilisentEdgen Searchposant des questions en temps réel et recevant des réponses immédiates, appuyées sur des données.

3. Surveillance continue des données du marché

Les marchés fonctionnent en permanence. L'IA suit sans relâche :

- Transactions de baleine : Surveillance immédiate des activités des portefeuilles influents.

- Vigilance Sociale : Détection précoce des pompes alimentées par la communauté et des changements d'opinion.

- Variations de volume : Alertes instantanées pour les changements critiques de liquidité du marché.

Les traders d'Edgen AI reçoivent des alertes en temps réel, permettant clairement des décisions d'achat/vente immédiates et éclairées.

L'impact de l'intelligence artificielle sur la précision et l'exactitude du trading

Le trading crypto rentable exige une analyse précise et dépourvue d'émotions. L'IA assure clairement l'exactitude en :

- Éliminer les décisions émotionnelles : l'IA prend ses décisions strictement sur la base de données, et non sur des sentiments subjectifs.

- Filtrage des signaux manipulateurs : identifier clairement et éviter les pompes frauduleuses entraînées par des bots.

- Prévoir les changements du marché : repérer clairement les tendances émergentes de l'opinion, avant les réactions généralisées du marché.

Selon leInternational Monetary Fund,L'IA redéfinit les marchés financiers mondiaux, les rendant plus efficaces, mais aussi plus sensibles à la volatilité alimentée par les données.

Edgen AI combine l'analyse blockchain, les données sociales et des insights clairs en intelligence artificielle, assurant aux traders d'agir uniquement sur des signaux authentiques.

L'avenir : Comment l'intelligence artificielle façonnera le trading alpha

Le rôle de l'intelligence artificielle dans les cryptomonnaies continue d'évoluer, apportant des avantages clairs aux stratégies de trading :

1. Optimisation du portefeuille améliorée par l'IA

Les traders utiliseront de plus en plus l'intelligence artificielle pour gérer automatiquement les portefeuilles, optimisant ainsi clairement les rendements à long terme.

2. Analyse avancée des blockchain

L'IA fournira des analyses plus approfondies des activités des contrats intelligents et du comportement des portefeuilles de « whales » avec une précision accrue. Edgen Radar offre déjà un suivi clair des portefeuilles influents et de leurs impacts sur le marché.

3. Analyse avancée des marchés prédictifs

La prévision par l'IA deviendra plus claire et plus précise, permettant aux traders de planifier des opérations avec confiance plusieurs semaines ou mois à l'avance.

4. Suivi du sentiment du marché raffiné

L'analyse des sentiments sociaux continuera d'évoluer, alertant clairement les traders instantanément lorsque l'enthousiasme du marché commence à croître. Edgen AI mène cette évolution, intégrant de manière transparente l'intelligence artificielle, les données blockchain et l'intelligence sociale.

L'IA définit l'avantage ultime pour le trading de cryptomonnaies

L'intelligence artificielle a redéfini les marchés cryptographiques. L'IA identifie clairement les signaux d'alpa, automatiser les échanges avec précision et améliore de façon significative la précision des décisions.

Edgen AI reste en tête, intégrant clairement l'analyse de la blockchain, l'intelligence du marché instantanée et les informations sociales en temps réel dans une solution complète de trading.

Les traders de cryptomonnaies utilisant l'intelligence artificielle dominent aujourd'hui clairement le paysage du marché de demain.

Restez clairement en tête. Adoptez le trading alimenté par l'intelligence artificielle avecEdgen AI

Investir, enfin, tu n'es plus seul.

Essaie Ed gratuitement. Sans carte, sans engagement.