실시간 AI 시장 인사이트: 모든 트레이더가 필요한 에드진 트레이딩 레이더

암호화폐는 빠르게 움직인다. 따라가지 않으면 뒤처질 수밖에 없다.

암호화폐 시장은 쉬지 않습니다. 가격은 빠르게 상승하고 하락하며 방향을 바꿉니다. 즉각적이고 최신의 시장 인사이트가 없으면 당신의 거래 전략은 순전히 추측에 불과합니다.

타이밍은 모든 것입니다. 암호화폐 시장은 전통적인 시장보다 더 적극적으로 움직입니다. 한 번 늦은 거래는 수익을 잃는 것이 됩니다. 성공적인 트레이더들은 즉각적이고 실행 가능한 데이터에 의존합니다.

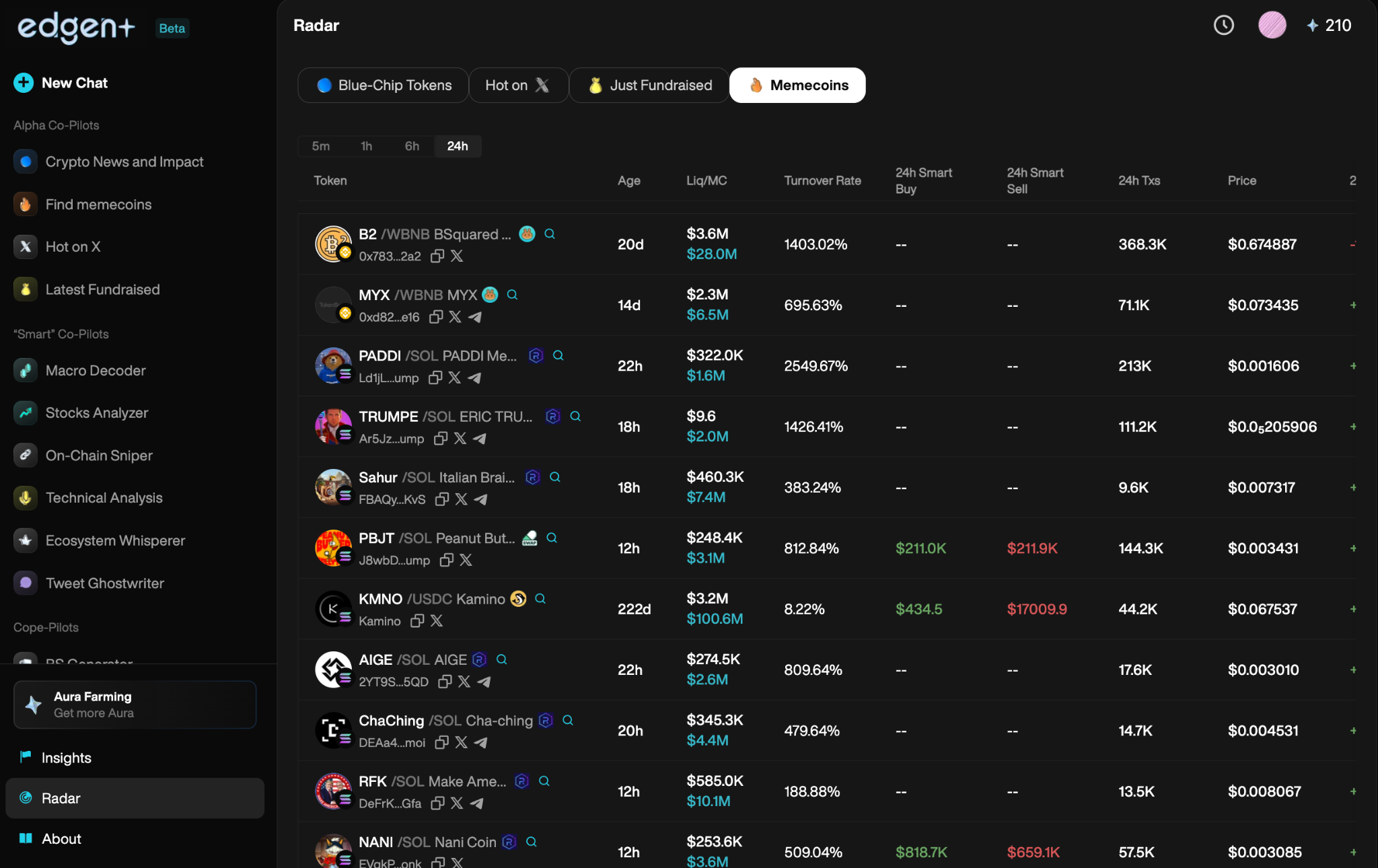

Edgen Radar체인 내 통찰력, 소셜 감정 추적, 강력한 알파 신호를 결합한 실시간 AI 분석을 제공하며, 모든 내용이 단일 플랫폼에서 명확하게 표시됩니다.

추측 없음. 망설임 없음. 실시간 거래의 명확함.

실시간 시장 통찰: 왜 중요한가

실시간 신호를 통한 암호화폐 거래 now

차트는 더 이상 전체 이야기를 전하지 못합니다. 시장 동인은 변경되었습니다:

- 소셜 미디어 화제

- 고래 지갑 이동

- 체인 내 거래

실시간 인사이트를 통해 시장 동인을 즉시 확인하여 시장 상황이 변하기 전에 수익성 있는 거래를 할 수 있습니다.

전통적인 투자자는 과거의 추세에 의존하지만, 암호화폐는 현재를 명확히 읽는 사람에게 보상을 줍니다.

트레이딩 블라인드는 돈을 잃는 것을 의미한다.

지연된 데이터? 최적의 진입 및 청산 시점을 놓치게 됩니다.

구식 신호? 추세에 뒤처져 거래하게 됩니다.

가짜 홍보에 속아요? 그 대가를 치르게 됩니다.

실시간 인사이트는 더 현명한 결정, 더 빠른 반응, 일관된 수익성을 가능하게 합니다.

에지엔 AI 레이더가 트레이더에게 최고의 우위를 제공하는 방법

Edgen Radar고급 인공지능, 세부적인 블록체인 분석 및 정확한 사회적 감정 분석을 결합하여 강력한 실시간 거래 도구로 제공합니다. 미시건 경제학 저널(Michigan Journal of Economics)에 따르면, AI is transforming financial markets by enhancing speed, efficiency, and precision in trading and market prediction.LSA Technology Services

주요 특징:

- AI 기반 시장 분석: 대규모 데이터 세트를 즉시 스캔하여 주요 트렌드를 식별하고 실행 가능한 통찰을 제공합니다.

- 실시간 블록체인 추적: 홀 월렛 활동, 유동성 이동 및 중요한 토큰 이동에 대한 즉시 알림.

- 소셜 감정 스캐너: 인플루언서, KOL, 그리고 급상승 중인 코인에 대한 실시간 모니터링

- 알파 신호 탐지: 가격 상승 전에 저평가 자산을 포착하는 AI가 선별한 거래 신호

- 즉시 알림: 주요 시장 변동이 발생하기 전 실시간 경고 알림

알파 신호: 내부자처럼 시장을 보다

알파 신호 정의

알파 신호는 대중이 이를 인지하기 전에 수익성 있는 거래의 조기 지표를 제공하며, 시장 변화를 명확하게 보여줍니다.

엣지나 AI의 알파 우위:

- 필터링을 통해 시장의 소음을 제거하고 수익성 있는 기회를 정확히 파악합니다.

- 상승하는 사회적 화제를 일찍 포착합니다.

- 고래의 축적 및 분포 신호를 빠르게 감지합니다.

추측하지 마세요. 알파 신호를 사용하여 자신 있게 거래하세요.

실시간 인사이트가 필수적인 이유, 선택이 아닌 이유

그들 없이 거래하는 것은 위험합니다:

- 지연된 진입으로 인해 수익성 있는 거래를 완전히 놓치다.

- 조작된 시장 홍보의 희생이 되다.

- 적극적으로 거래하기보다는 항상 반응하면서, 손실된 이익을 초래하게 된다.

엣지엔 AI는 명확한 이점을 제공합니다:

- 시장 전망: 가격에 반영되기 전에 시장 동향을 파악하세요.

- 정밀 실행: AI 기반의 통찰은 확신 있는 결정을 의미합니다.

- 초기 우위: 주류 거래자가 반응하기 전에 큰 가격 변동을 포착하라.

실시간 데이터는 전문가 수준의 거래입니다. 없으면 성공은 닿을 수 없습니다.

AI와 실시간 데이터: 거래 혁명이 도래했다

시장은 매일 더 지능적이고 유연하며 경쟁력 있는 방향으로 성장하고 있다. 성공적인 트레이더들은 자신의 우위를 유지하기 위해 인공지능(AI) 기반 도구를 활용한다.

엣지 레이더는 이 엣지를 명확하게 제공합니다.

에지너 레이더의 거래의 미래에 대한 비전

전통적인 지표와 정적 차트를 넘어서는 미래의 거래가 있다. 인공지능 기반 분석, 실시간 데이터 추적 및 자동 실행이 거래를 정의할 것이다.

명확하게 보는 것을 상상해보세요:

- 모든 중요한 시장 움직임은 인공지능(AI)에 의해 즉시 식별됩니다.

- 토큰이 급등할 것으로 예상되는 것이 조기에 발견됨.

- 소셜 감정 및 블록체인 활동 기반의 실시간 알림.

엣지언 AI는 이 미래를 정확히 구축하고, 엣지언 레이더를 사용하는 트레이더는 그 일부가 됩니다.

무역. 빠르게 행동하라. 꾸준히 승리하라.

거래를 한 단계 업그레이드하세요. 시도해 보세요Edgen Radar 오늘.

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.