对 Orange Cap Games 旗下的 Moonbirds 进行评估,重点关注战略、执行、合作关系和估值情景。您可以在此处找到 Moonbirds 指南:

TL;DR

- OCG 正在应用一套经过验证的 IP 复兴策略,从社区到品牌再到产品,已经将关注度转化为活动和需求。

- 精英投资者的支持、Kaito AI 社交赚取等实际效用、Otherside 头像以及合作伙伴空投,为 Moonbirds 带来了强劲的势头,并提供了实现持久价值的清晰路径。

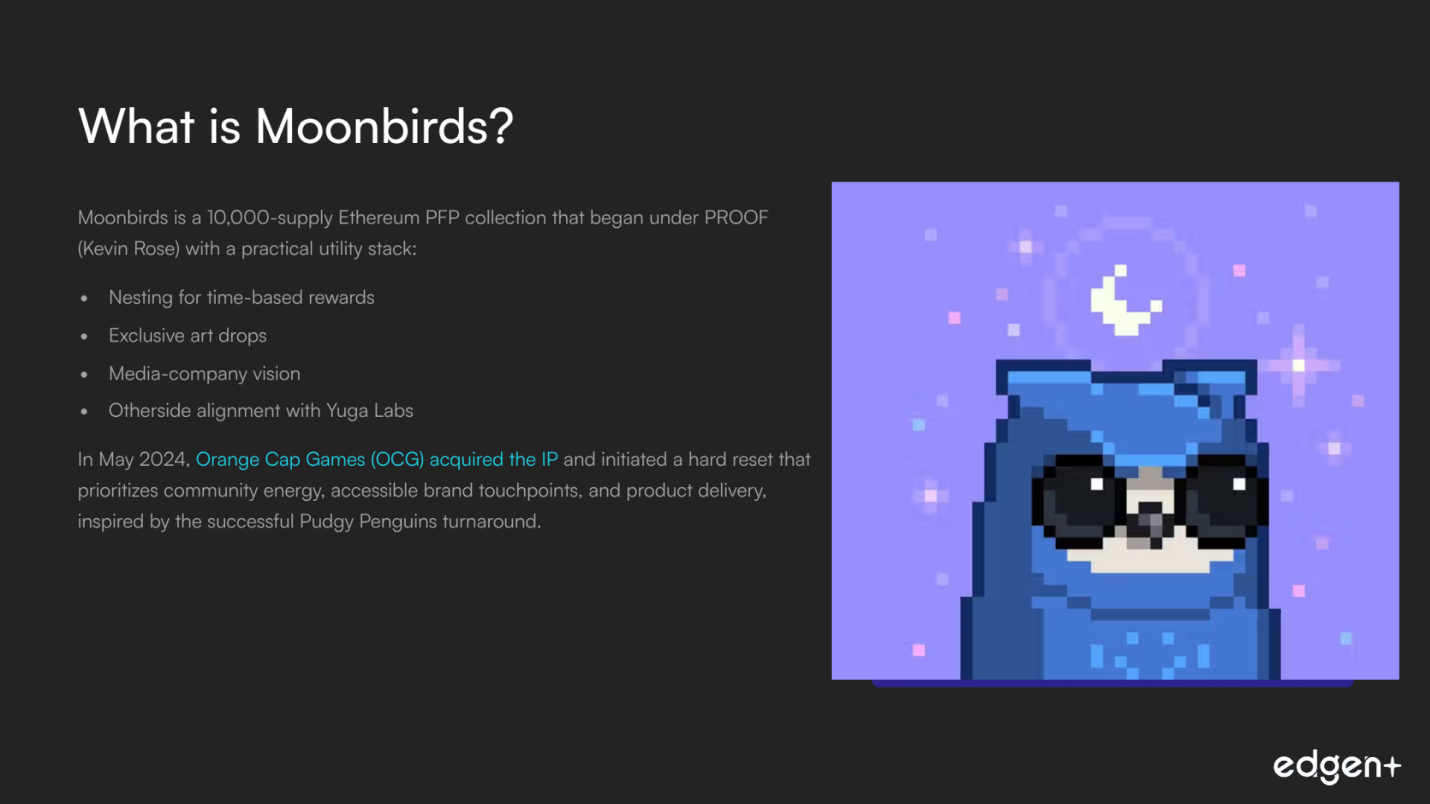

什么是 Moonbirds

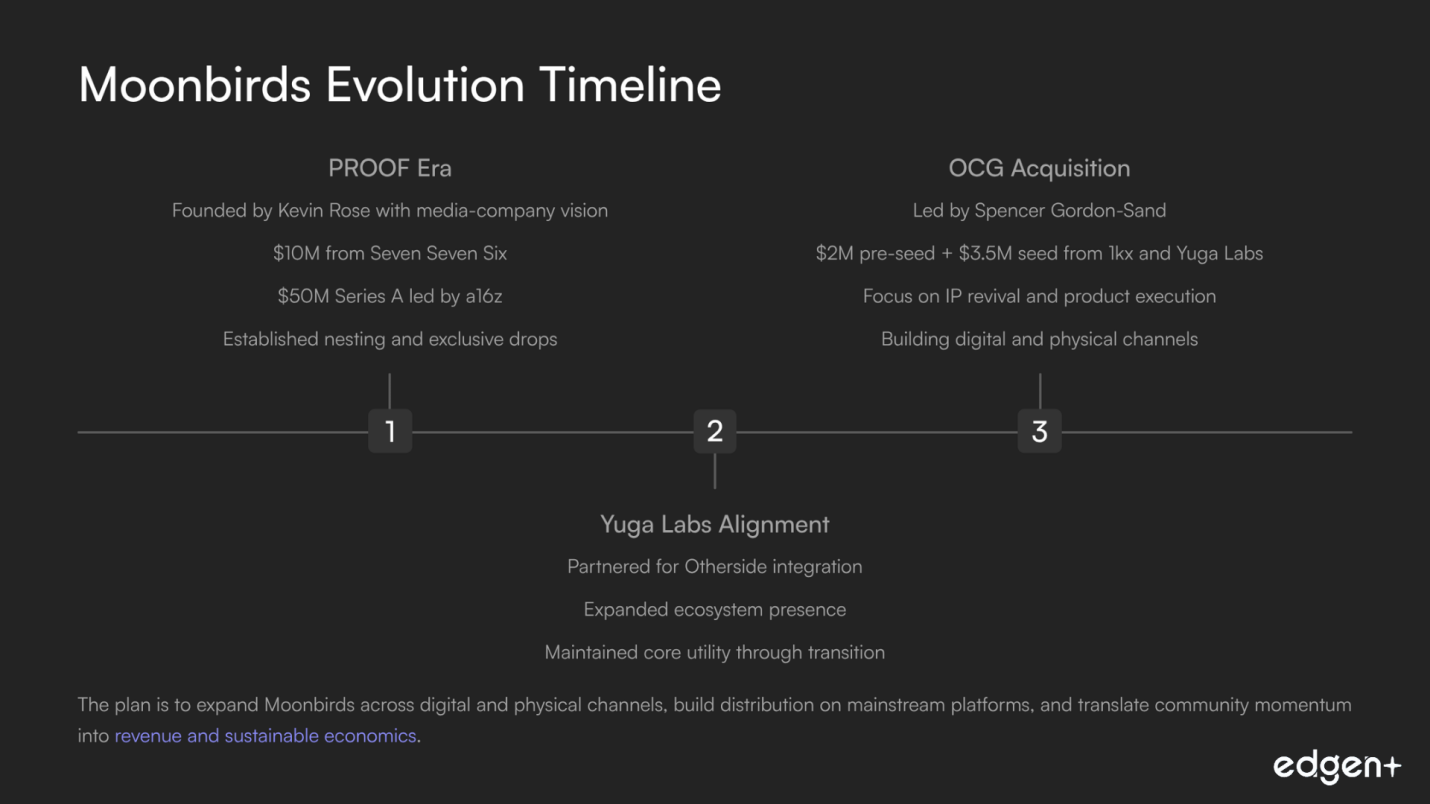

Moonbirds 是一个拥有 10,000 个供应量的 Ethereum PFP 系列,最初由 PROOF(Kevin Rose)发起,具有实际的实用堆栈:通过“筑巢”获得基于时间的奖励、独家艺术品掉落以及媒体公司愿景。后来,它与 Yuga Labs 合作开发 Otherside。2025 年 5 月,Orange Cap Games(OCG)收购了该 IP,并启动了一项硬性重置,优先考虑社区活力、可访问的品牌接触点和产品交付,灵感来自于 Pudgy Penguins 成功的转型。

由 Spencer Gordon-Sand 领导的 OCG 带来了加密原生信誉和产品执行经验,包括 Vibes 集换式卡牌游戏。该计划旨在通过数字和物理渠道扩展 Moonbirds,在主流平台建立分销,并将社区势头转化为收入和可持续的经济效益。与 Kaito AI(社交赚取)等合作伙伴关系以及 Monad 和 Towns 等项目的空投访问权限,为持有者增加了即时价值,同时团队致力于构建更广泛的 IP 和游戏平台。

凭借新的领导层、高知名度的支持者和清晰的运营模式,Moonbirds 有望从一个传奇的 NFT 系列发展成为一个持久的、以实用性为基础的品牌。

一、基础与战略分析

1. 愿景与投资者一致性

战略在三个时代不断演变,从 PROOF 到 Yuga 再到 OCG,最终聚焦于一个使命:复兴 IP,激活社区,并交付产品。

投资者支持也反映了这一历程,从 a16z 支持 PROOF 的媒体理论,到 1kx 和 Yuga Labs 共同牵头 OCG 的种子轮融资,使资本与转型计划保持一致。

2. 卓越的团队和执行力

- 由首席执行官 Spencer Gordon-Sand 领导的运营执行,他是一位早期的 NFT 投资者和著名的社区领导者,拥有丰富的实际产品经验。

- Vibes TCG 展示了实体和数字执行能力,以及通过亚洲制造能力实现生产和规模化的运营路径。

3. 资本实力和认可

历史融资包括 Seven Seven Six 提供的 1000 万美元,以及由 a16z 牵头并有顶级参与者加入的 5000 万美元 A 轮融资。

如今,OCG 获得了 1kx 和 Yuga Labs 提供的 350 万美元种子轮融资(此前还有 200 万美元 Pre-seed 轮融资)的支持,并辅以 Vibes 的收入。这为其提供了健康的、以执行为重点的发展空间。

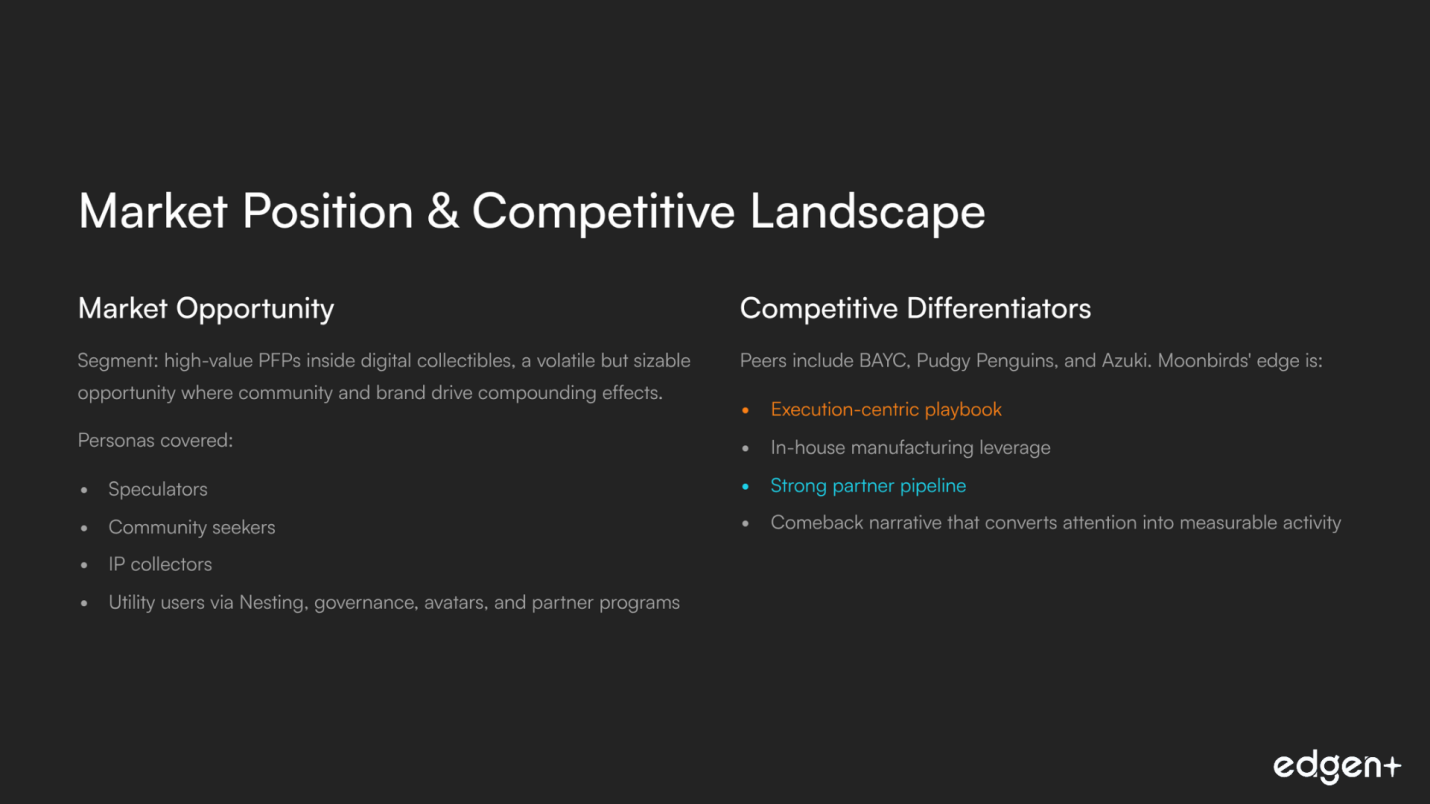

4. 市场机遇和契合度

- 细分市场:数字收藏品中的高价值 PFP,这是一个波动但规模可观的机会,社区和品牌在此推动复合效应。

- 覆盖人群:投机者、社区寻求者、IP 收藏者和通过“筑巢”、治理、头像和合作伙伴计划的实用工具使用者。

5. 竞争格局与差异化

同行包括 BAYC、Pudgy Penguins 和 Azuki。Moonbirds 的优势在于以执行为中心的策略、内部制造优势、强大的合作伙伴渠道以及一个将关注度转化为可衡量活动的回归叙事。

基础结论: 卓越的基础实力,拥有目标一致的投资者、务实的运营者和产品主导的路线图。

二、预发布生态系统与上市策略

1. 社区与叙事势头

OCG 的收购催化了叙事转变。持续的领导层沟通和 Kaito AI 等切实可行的实用工具公告,重新激发了社交和链上活动。信号表明参与质量正在提高,持有者基础反应积极。

2. 链上足迹

一个规模庞大且具有韧性的持有者基础为产品和代币机制提供了强大的启动平台。长期持有行为、重新活跃的二级市场活动和子收藏品支持访问,同时保持品牌地位。

3. 增加实用性的合作伙伴关系

- Kaito AI 社交赚取将内容转化为奖励,将被动持有转化为主动参与和发现。

- Monad 和 Towns 等空投渠道奖励持有者并吸引寻求高质量分销的合作伙伴;Otherside 就绪的 3D 头像扩展了跨生态系统的实用性。

4. 代币经济学和价值积累(当前)

- “筑巢”创造了基于时间的奖励,支持持有行为,并为未来的 $TALONS 代币做好准备。

- 通过 Lunar Society 进行的治理将影响力与核心 NFT 和金库联系起来,从而增强了参与者与品牌之间的长期一致性。

上市准备度结论:非常有前景。以实用性为导向的合作关系和交付纪律构成了坚实的基础。代币 TGE 准备度将受益于持续的运营和法律准备。

三、前瞻性分析(催化剂和机会)

短期(≤1个月)

Kaito AI 激活增强了创作者循环,提高了发现度,并支持粘性互动,从而促进交易和合作伙伴兴趣。

中期(1-3个月)

OCG 时代的首款产品发布可以巩固超越叙事的基本面,并验证运营模式。

长期(6个月以上)

$TALONS TGE 为更广泛的经济确立了公开定价,实现了 DeFi 和可组合性,并增加了与合作伙伴的合作空间。

前瞻性观点: 存在重大机遇,执行节奏是 TGE 将动力转化为持久价值的主要杠杆。

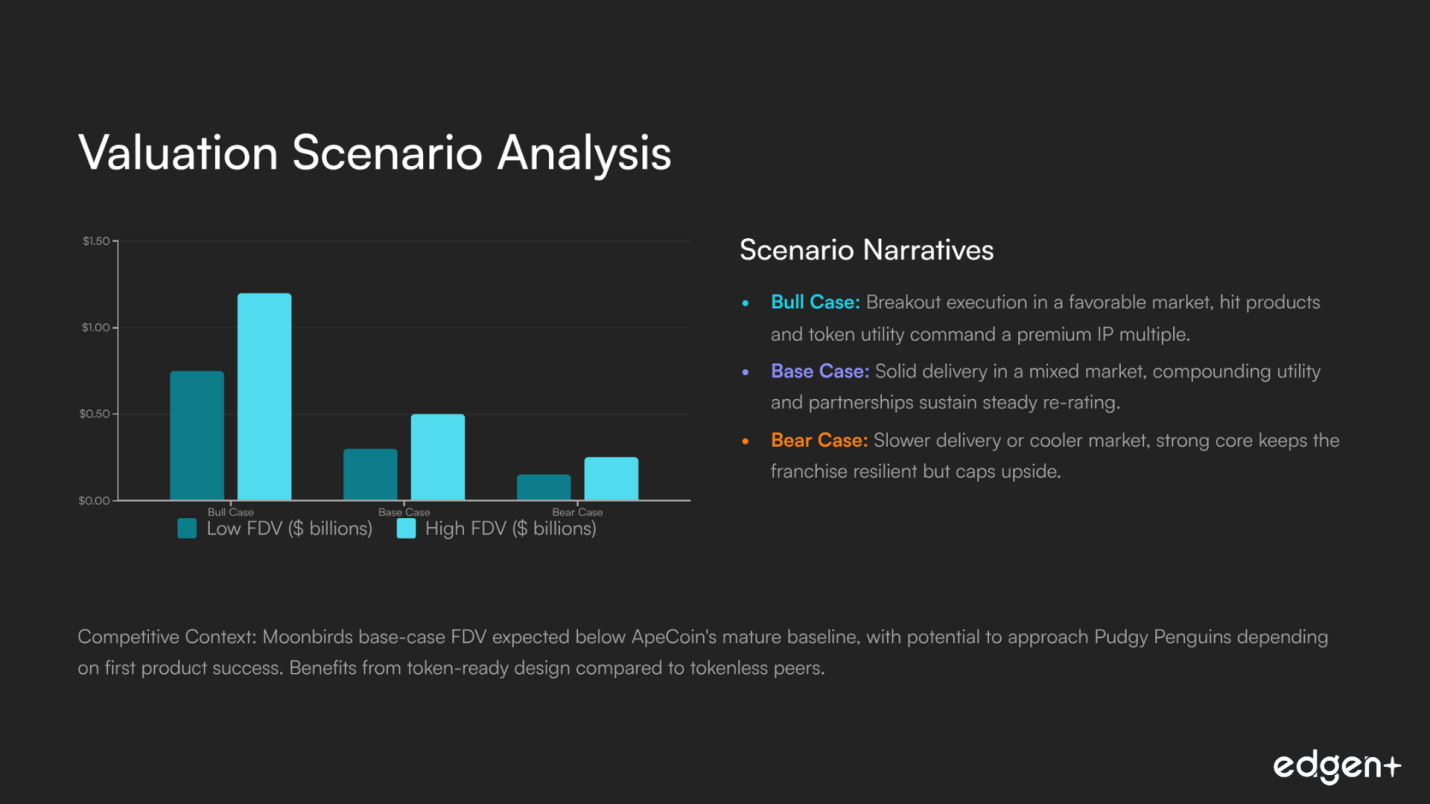

四、估值情景分析 (TGE FDV)

情景 | 完全稀释估值 (FDV) (数十亿美元) | 简要说明 |

牛市情景 | 0.75 – 1.20 | 在有利的市场中取得突破性执行,热门产品和代币效用带来了高溢价的 IP 倍数。 |

基础情景 | 0.30 – 0.50 | 在混合市场中稳健交付,复合效用和合作伙伴关系维持稳定重估。 |

熊市情景 | 0.15 – 0.25 | 交付缓慢或市场降温,强大的核心使特许经营权保持韧性,但限制了上涨空间。 |

竞争对手格局(TGE 时或临近 TGE 的代币视角)

项目 | 代币 | TGE/代币视角 | 持有者关联 | 分发方式 | 与 Moonbirds 的定位(基础情景) |

ApeCoin / Otherside | 生态系统效用和治理 | BAYC 关联 | 空投加上市 | Moonbirds 基础情景的 FDV 预计低于 $APE 的成熟基线,与 Yuga 的战略联系是增值的。 | |

Pudgy Penguins | IP、玩具和游戏飞轮 | Penguin 持有者 | 社区导向 | Moonbirds 基础情景的 FDV 接近或低于 $PENGU,取决于首个产品的成功。 | |

Azuki | (无) | 品牌和动漫导向的 IP | 收藏驱动 | 不适用 | 无代币的同类基准,Moonbirds 受益于为额外价值积累而设计的代币化。 |

最终结论

Moonbirds 作为一项专业运营的 IP 复兴项目,具有真实的社区根基和实际的产品路径,显示出巨大的潜力。凭借精英投资者的支持和早期的效用吸引力,该项目看起来非常有前景。执行的速度和质量仍然是解锁估值范围上限的关键。

教育内容,非财务建议。

投资这事,终于不用一个人了

免费试用 Ed。不用信用卡,不绑约