Aura 101: 시장 통찰력을 영향력과 보상으로 바꾸는 방법

TLDR

- Aura는 Edgen 내에서 의미 있는 행동(퀘스트, 구독, 추천)을 완료하여 획득됩니다.

- 크레딧은 Edgen의 AI 기능(시장 정보, 보고서, 알림)을 구동합니다.

- 높은 Aura 점수는 초기 기능, 특별 보상 및 리더보드 순위를 잠금 해제합니다.

- 승수(최대 100배)는 플랜 등급에 따라 Aura 획득 속도를 가속화합니다.

Aura란 무엇인가요?

Edgen의 Aura는 Edgen 내에서 실질적이고 실제적인 이점을 제공합니다.

Aura 점수가 높아질수록 초기 기능 출시, 독점 베타 프로그램 및 향후 이벤트와 관련된 잠재적 보상에 액세스할 수 있습니다.

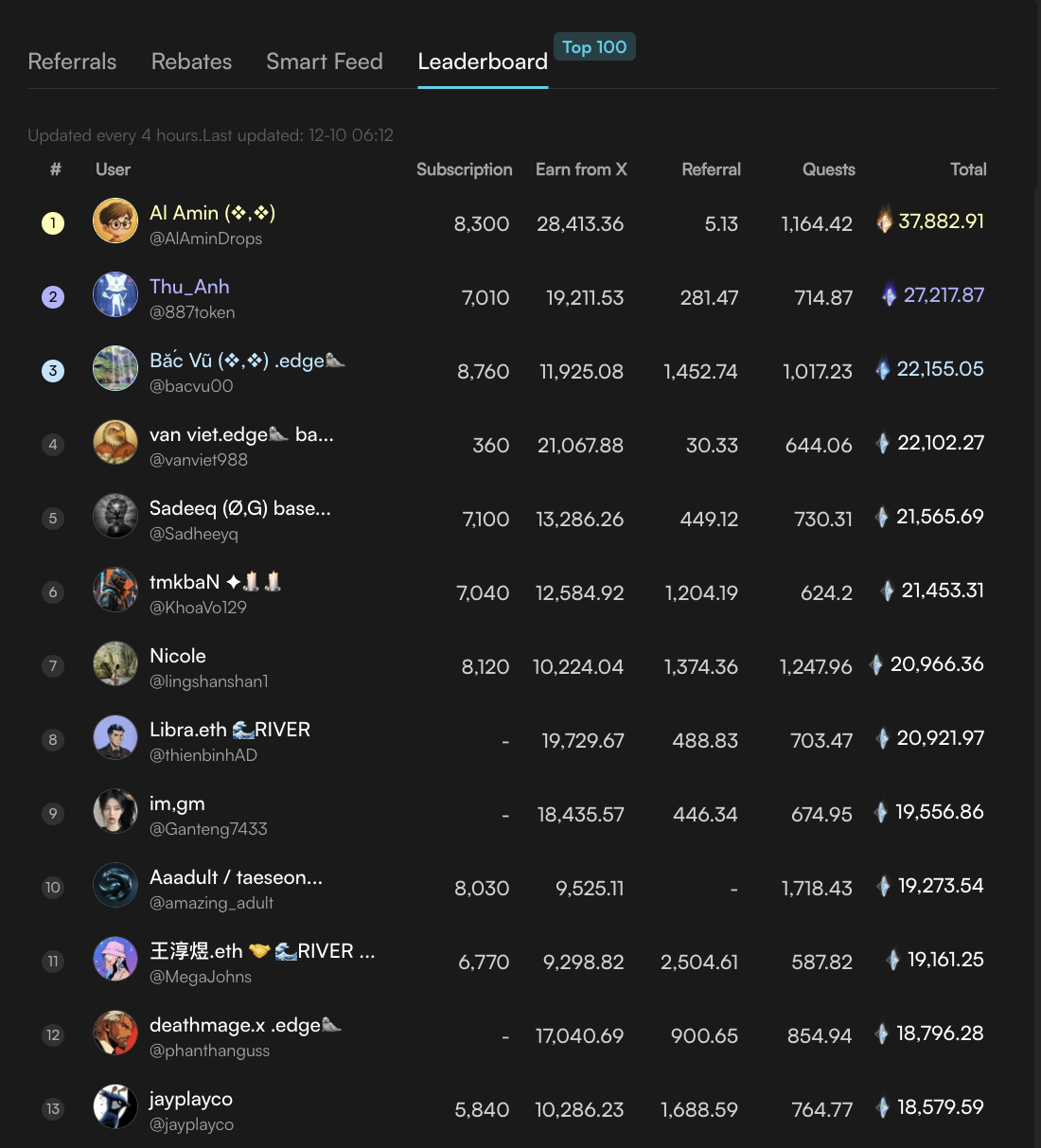

Aura에는 리더보드가 있습니다. 리더보드에 오르면 다른 수준의 트레이더가 됩니다. 더 높이 올라갈수록 특별 보상, 고유한 특권 및 다른 사람들은 볼 수 없는 액세스 권한에 더 가까워집니다.

Aura는 또한 다른 트레이더들이 커뮤니티에 대한 귀하의 헌신을 인식하도록 돕습니다. 간단히 말해, Aura는 Edgen에서의 귀하의 존재를 지속적인 가치로 전환합니다.

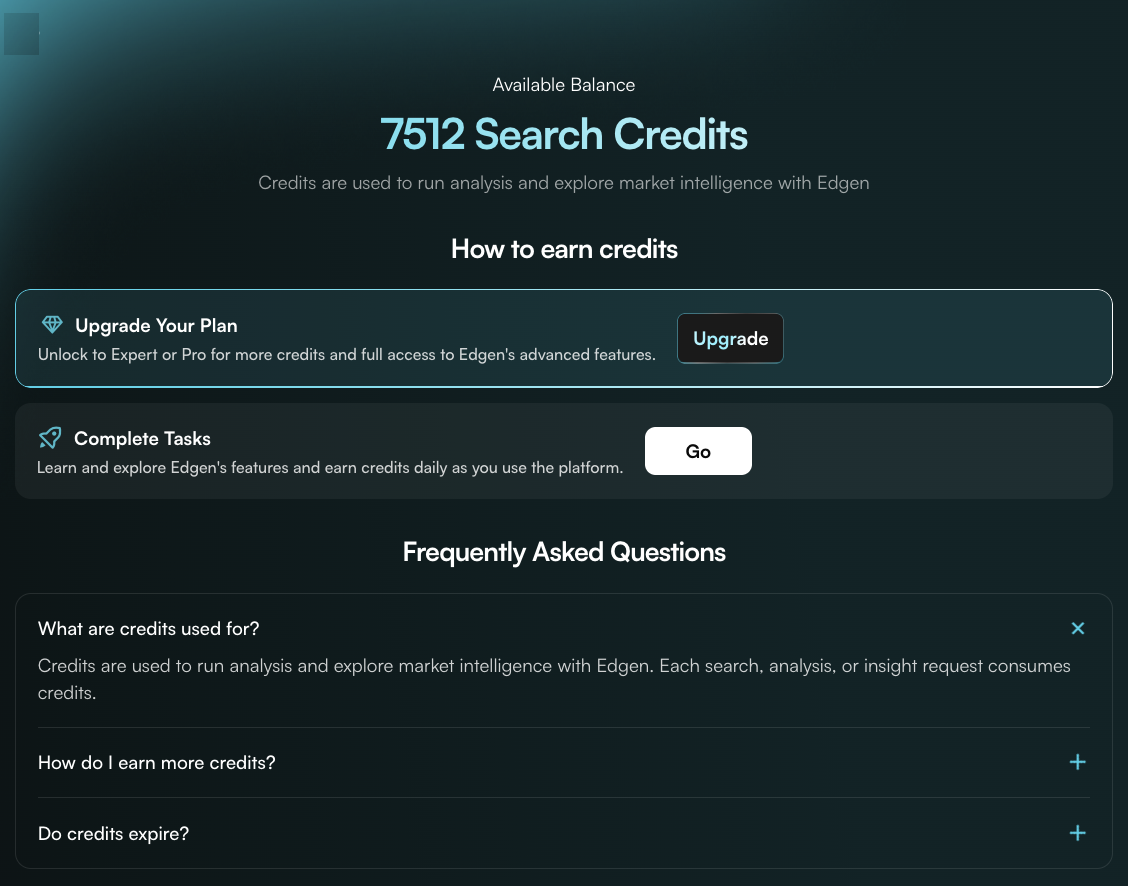

크레딧이란 무엇인가요?

크레딧은 Edgen의 AI를 사용하는 방법입니다.

시장 정보, 포트폴리오 및 360º 보고서, 스마트 알림은 모두 크레딧으로 구동됩니다. 이를 Edgen 도구를 위한 연료라고 생각하십시오.

작업 센터에서 작업을 완료하여 크레딧을 무료로 얻거나, 구독 등급을 통해 더 많이 얻을 수 있습니다.

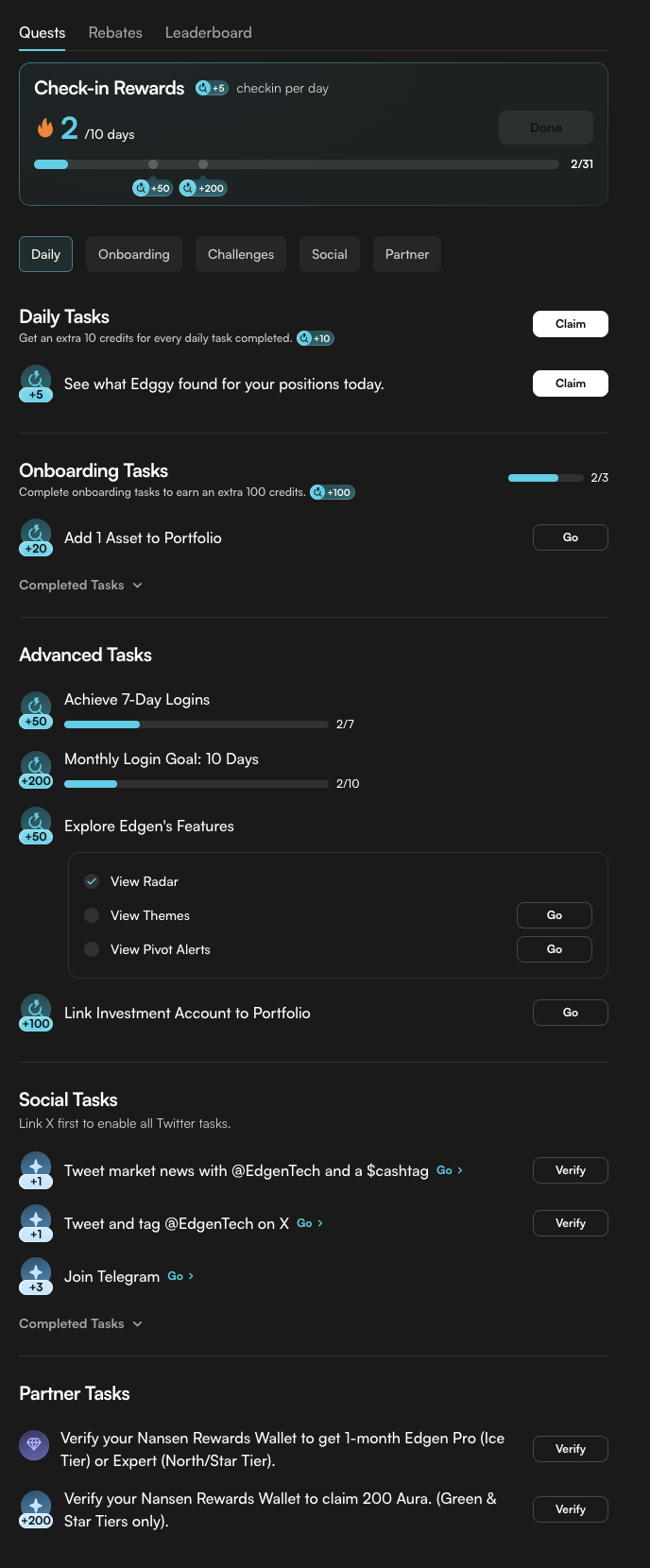

작업 센터: 획득 방법

작업 센터는 Aura와 크레딧을 모두 얻을 수 있는 허브입니다.

5가지 퀘스트 유형이 있습니다.

- 일일: 체크인, 보상 청구

- 온보딩: 포트폴리오 설정, 시장 우위 강화

- 챌린지: 목표 달성, 보너스 잠금 해제

- 소셜: 시장 분석 또는 뉴스 공유

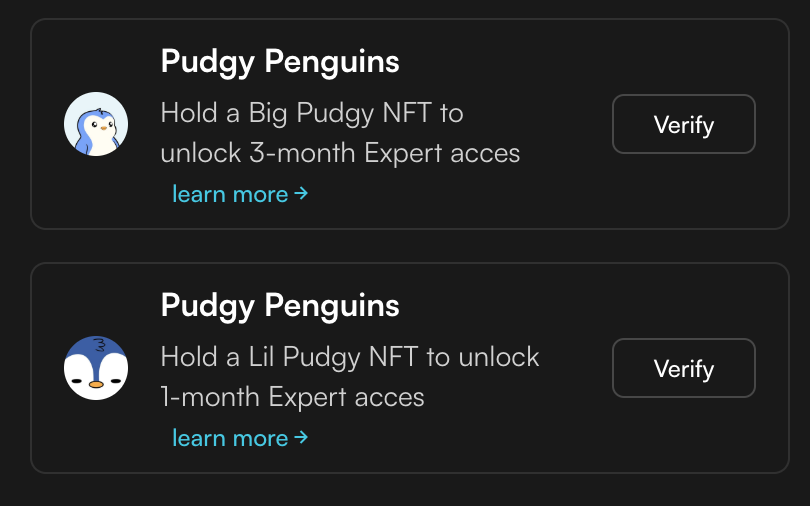

- 파트너: Nansen, Pudgy Penguins 등과 같은 프로젝트와의 한정 시간 협업

일부 작업은 크레딧을 얻습니다. 일부 작업은 Aura를 얻습니다.

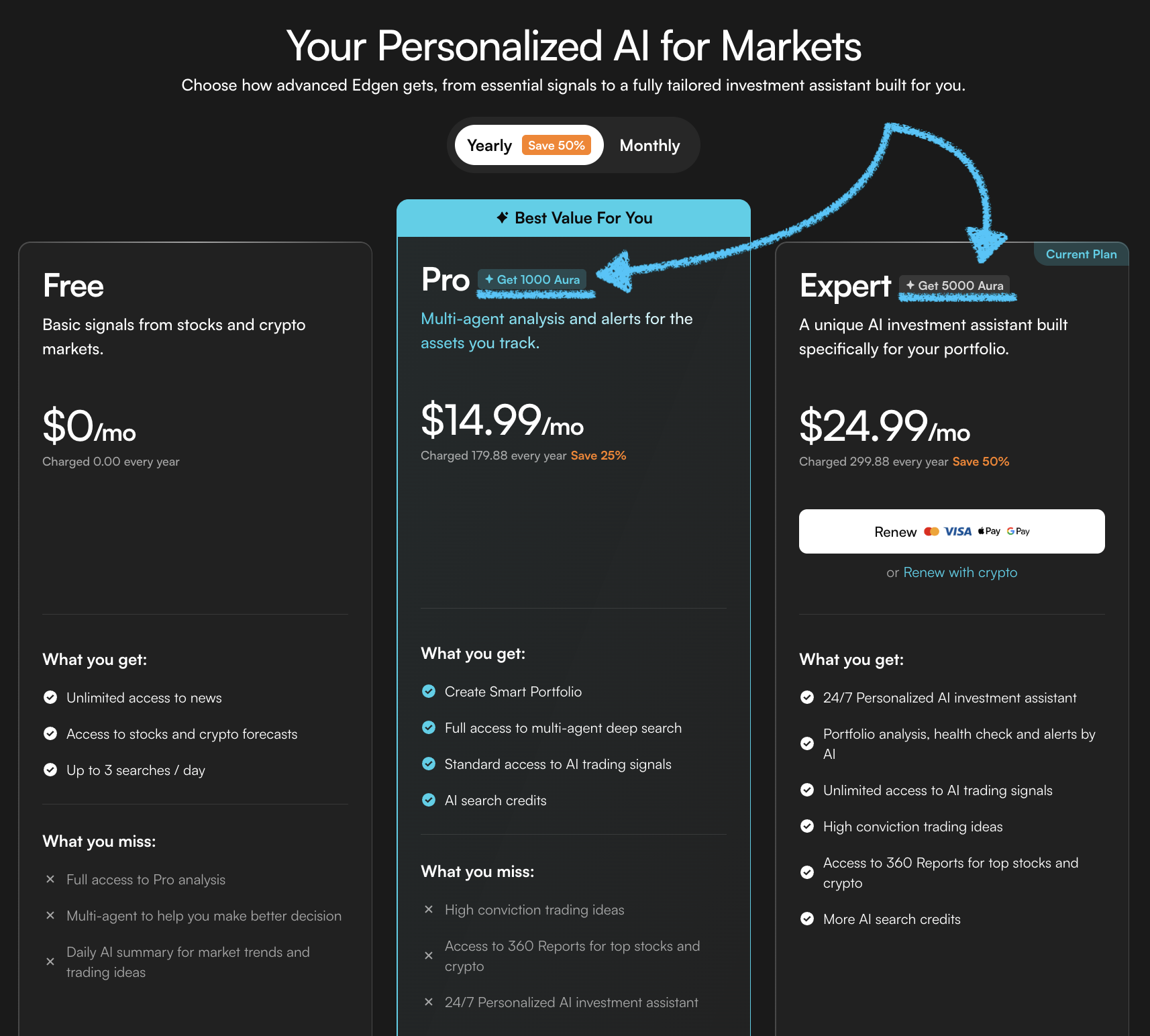

승수: 더 빠르게 획득

귀하의 플랜 등급과 기간(월별/연간)은 작업에서 Aura를 얼마나 빨리 얻는지 결정합니다.

- 무료 = 1배

- 프로 = 20-30배

- 전문가 = 80-100배

동일한 작업이지만 매우 다른 보상을 제공합니다.

승수는 작업에서 획득한 Aura에 적용되므로, 플랜을 업그레이드하는 것은 기능만 잠금 해제하는 것이 아니라 리더보드에서의 위치를 가속화합니다.

구독 Aura

프로 또는 전문가 플랜을 구독하면 Edgen의 AI 도구에 대한 전체 액세스 권한이 부여됩니다. 그러나 구독은 Aura 혜택도 제공합니다.

- 구독이 시작될 때 일회성 Aura 보너스를 받습니다.

- 구독 기간 동안 매일 체크인하면 Aura를 얻습니다.

이러한 꾸준한 보상은 시간이 지남에 따라 Aura 점수를 지속적으로 높이는 데 도움이 됩니다.

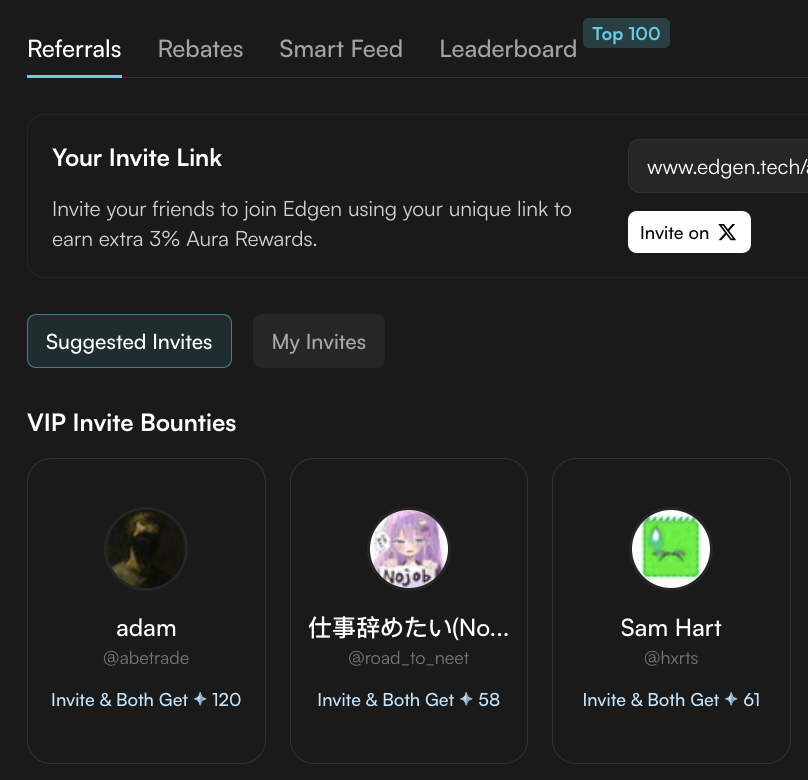

추천 Aura

친구를 초대하여 Edgen에 가입하세요. 친구가 가입하고 온보딩을 완료하면 귀하와 친구 모두 Aura를 얻습니다.

Edgen은 보너스를 극대화하기 위해 초대할 친구를 제안합니다.

추천한 친구가 프로 또는 전문가 구독자가 되면, 리베이트를 통해 그들의 구독료 일부를 얻을 수도 있습니다.

파트너 퀘스트

때때로 Edgen은 신뢰할 수 있는 프로젝트와 협력하여 한정판 퀘스트를 출시합니다.

파트너 작업을 완료하면 추가 Aura 또는 무료 전문가 액세스와 같은 특전을 얻을 수 있으며, Edgen에 연결된 새로운 도구 및 생태계를 발견할 수 있습니다.

지금 시작하기

Aura는 오늘날에도 귀중한 혜택을 제공하며, 생태계가 확장됨에 따라 그 중요성은 더욱 커질 것입니다。

일찍 Aura를 구축하면 미래 기회에 대비하여 강력한 위치를 확보할 수 있습니다.

오늘 시작하세요: 퀘스트를 완료하고, 도구를 탐색하고, 필요에 맞다면 구독하거나, 친구를 초대하세요. 모든 행동은 Aura를 증가시키고, 모든 점수는 Edgen 내에서 귀하의 정체성의 일부가 됩니다。

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.