从表情包币到股票:AI交易如何重塑全球市场

AI正在重塑游戏规则

金融市场已经发生了变化。从模因币到股票交易时,交易已经超越了图表和人工分析。传统策略已显不足,使交易者停留在过去。

由AI驱动的工具,以……为主导Edgen AI实时解码市场情绪、社交动量和链上行为。这一优势意味着比以往任何时候都更敏锐、更智能、更快地交易。

为什么AI交易现在主导市场

人工智能在解读市场趋势方面超越了人类交易员。人工智能可即时处理数十亿个数据点,以无与伦比的速度捕捉市场变化、影响者信号和隐藏的叙事。

基于人工智能的交易意味着:

- 预测分析:在他人注意到之前看到市场叙事的形成。

- 算法交易:以微秒级执行交易。

- 情感分析:立即捕捉推特热度和网红趋势。

- 高级风险管理:在下跌信号出现前加以识别。

底线:AI 预测市场。人类做出反应;AI 进行预测。

边缘:能察言观色的AI

Edgen AI 融合实时链上数据和社会“泵基础,并将深度市场情报转化为可操作的见解。它能识别关键意见领袖(KOLs),监控智能钱包,并在大众之前带来超额收益。

核心功能:

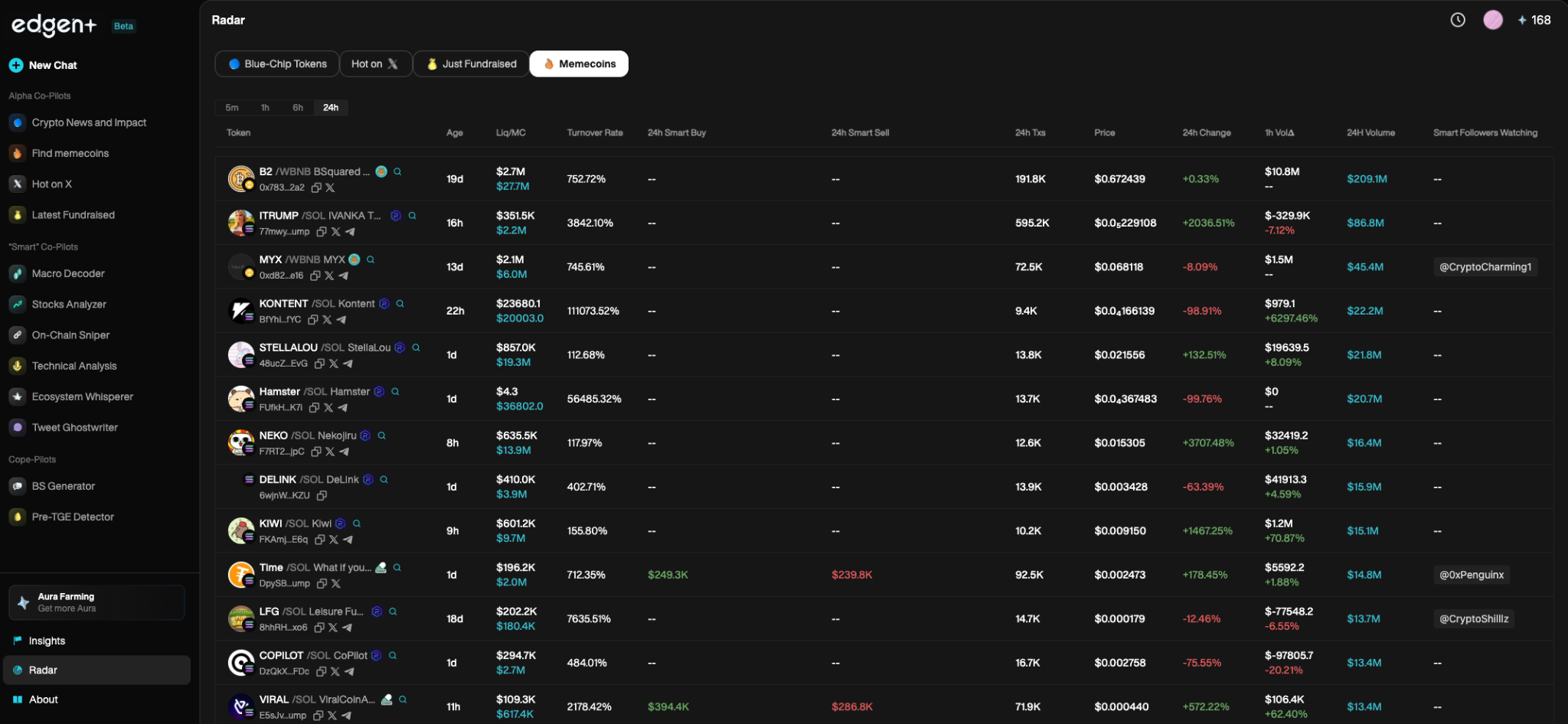

- 实时资产监控:Edgen Radar跟踪价格走势与社交情绪。

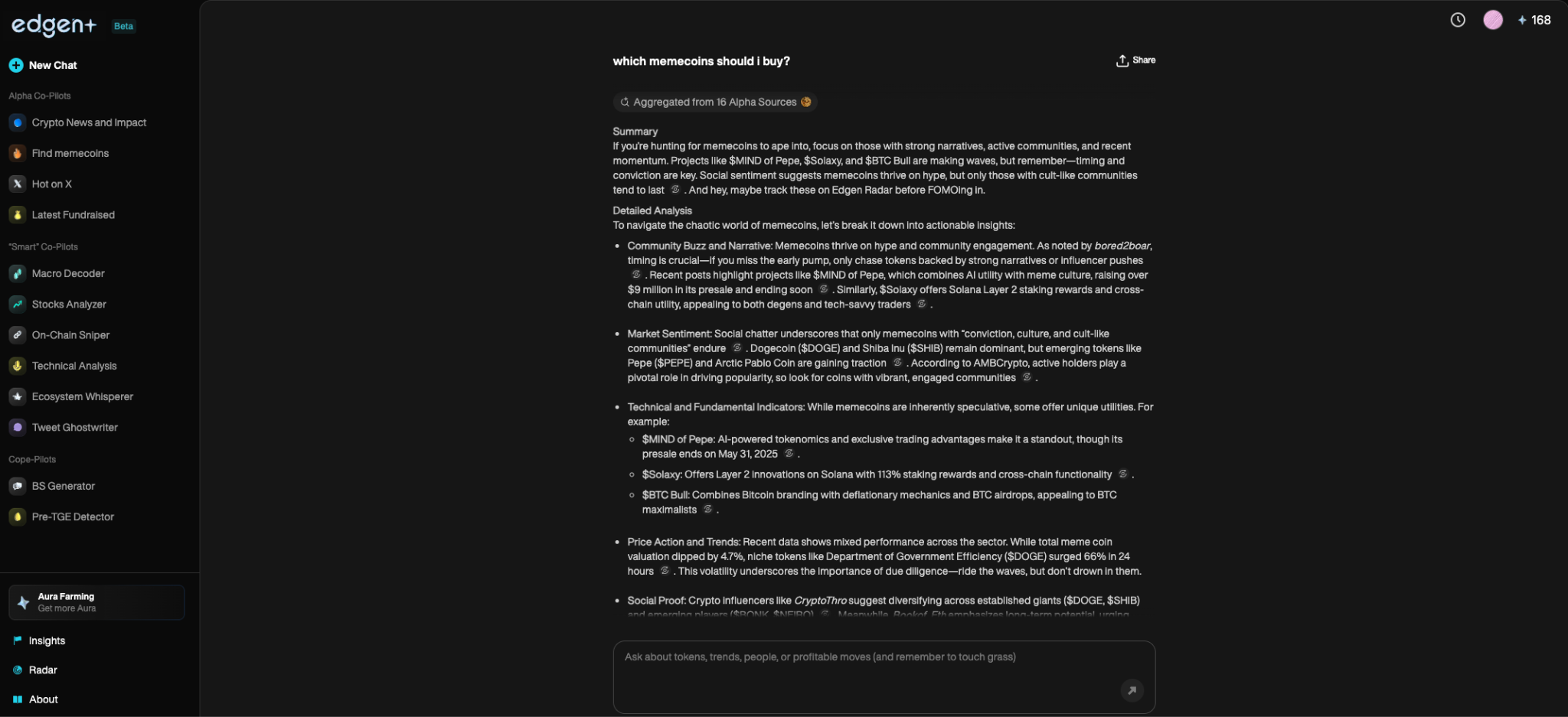

- AI驱动的搜索:Edgen Search从聚合数据中提供即时的市场情报。

- 社区驱动分析:Edgen Feed提供实时的众包α信号。

Edgen AI把握市场脉搏,了解推动每笔交易的集体心态。

迷因币人工智能:天生一对

模因币超越传统的估值。价格波动跟随炒作、社区参与和病毒式传播的势头。

AI 在这种环境中蓬勃发展。Edgen AI 具备独特优势,能够处理迷因币利用实时情感追踪来捕捉快速的市场变化。

Edgen AI 硕士模因币通过以下方式交易:

- 情感分析:扫描推特/X的即时拉升信号。

- 链上洞察:实时追踪鲸鱼钱包和网红活动。

- 阿尔法检测:在价格暴涨前发现隐藏的指标。

迷因币平均波动性和无情的竞争。没有人工智能,交易者将毫无胜算。

人工智能与现代投资策略

市场已超越基本面。社会情绪、预测分析和链上交易定义了现代策略。

人工智能在智能投资中的作用:

- Alpha发现:在市场波动前发现信号。

- AI管理的投资组合:基于人工智能的基金提供优化的风险管理。

- 区块链集成:监控钱包活动以追踪智能资金。

Edgen Radar 树立了新标准,对整个市场生态系统进行解读,而非孤立的指标。

解决交易的三体问题

大多数交易者都是部分盲目交易:

- 一些项目追踪链上数据但忽略了社交叙事。

- 其他人追逐炒作,却忽视流动性变化。

- 许多交易者坚持使用技术图表,忽视影响市场的新闻故事。

Edgen AI通过整合三个维度来解决这种复杂性:

- 链上分析:实时智能资金追踪。

- 社会情绪:捕捉炒作周期和社区驱动的行动。

- 人工智能驱动的执行:在他人发现机会之前,战略性交易。

这种统一的方法使Edgen交易者在“PvP”、竞争性、零和市场中具有决定性的优势。

人工智能在金融市场中的未来

人工智能将推动交易的未来。忽视这一事实的交易者可能会永久落后。

接下来是什么:

- 自学习人工智能机器人:人工智能即时适应新兴市场趋势。

- 自动化阿尔法发现:在人类识别之前发现隐藏的机会。

- 高级社会智能:即时解读网红驱动的叙事。

- 全人工智能驱动的基础设施:Edgen AI正在演变为一个全面的投资平台。

来自该研究的University of Michigan highlights how AI and algorithmic systems are transforming modern financial markets这进一步巩固了像Edgen AI这样的平台所采取的方向。

Edgen AI已经构建了这一现实,将人工智能塑造为一种基本的市场力量。

人工智能交易革命已经来临

AI重塑了全球金融市场:迷因币股票、加密货币、外汇。从高频交易到阿尔法检测,人工智能定义了交易的成功。

Edgen AI引领这场革命,为交易者在激烈的市场中提供战略优势。没有AI的交易者将面对行动更快、思维更清晰、执行更完美的对手。

市场发生了演变。人与人之间的交易消失了。如今是人工智能与人工智能之间的较量。

准备就绪与否,这将是…Edgen AI 时代已经到来!

投资这事,终于不用一个人了

免费试用 Ed。不用信用卡,不绑约