Analyse du marché de l'IA en temps réel : pourquoi tout trader a besoin du Radar Edgen

Les crypto-monnaies évoluent rapidement. Restez à jour ou restez en arrière.

Les marchés cryptographiques ne connaissent jamais de pause. Les prix montent, baissent et changent rapidement. Sans des analyses de marché immédiates et à jour, votre stratégie de trading devient pure spéculation.

Le timing est tout. Le crypto-marché évolue plus rapidement que les marchés traditionnels ; une transaction retardée signifie une perte de profit. Les traders réussis s'appuient sur des données immédiates et exploitables.

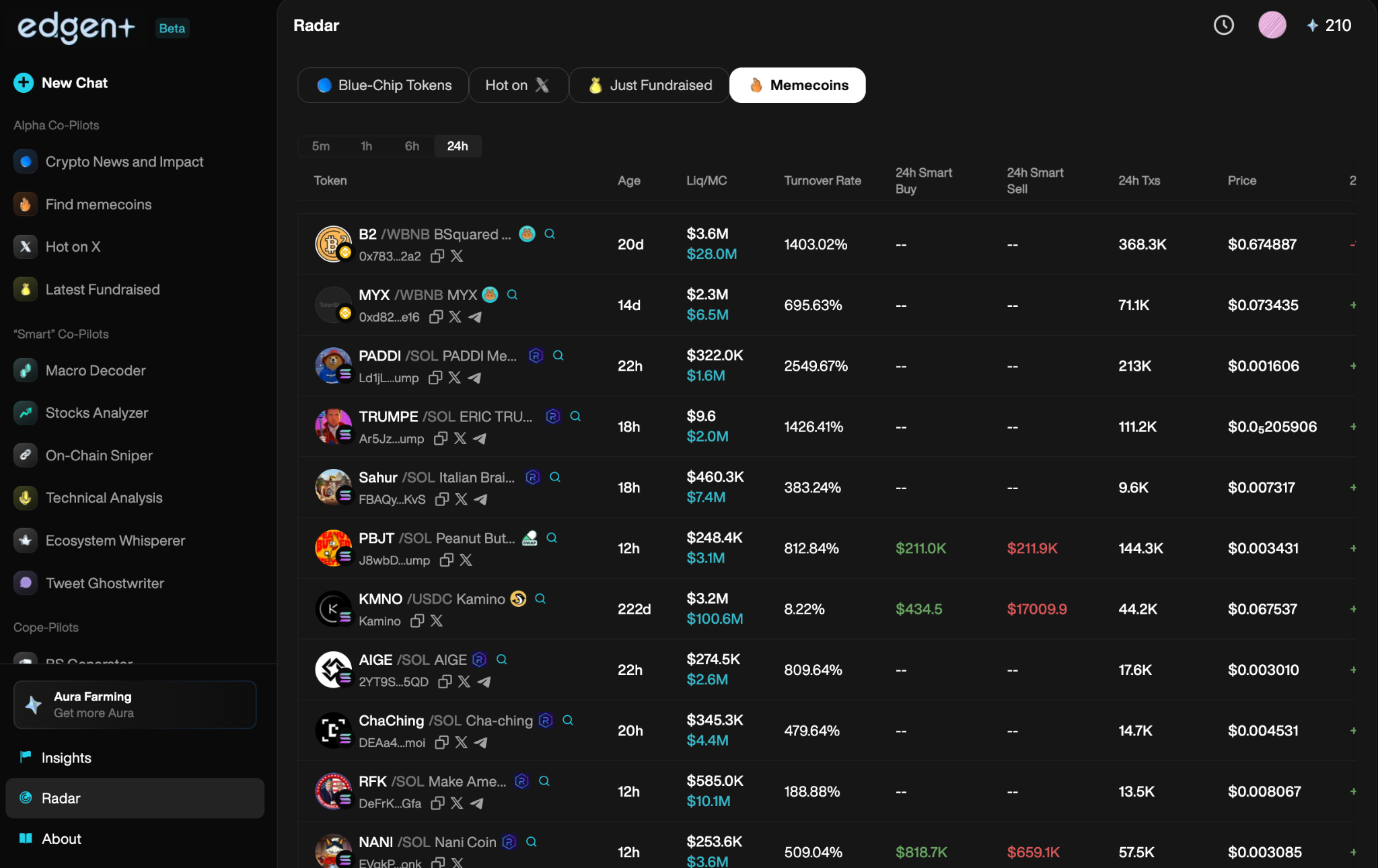

Edgen Radaroffre des analyses en temps réel par l'intelligence artificielle, en combinant des informations sur les chaînes de blocs, le suivi de l'opinion publique et des signaux d'alpha puissants, tous clairement présentés sur une seule plateforme.

Aucune supposition. Aucune hésitation. Clairvoyance du trading en temps réel.

Des informations en temps réel sur le marché : pourquoi elles sont importantes

Les échanges de cryptomonnaies sur des signaux en temps réel maintenant

Les graphiques ne racontent plus l'histoire complète. Les moteurs du marché ont changé :

- La Ferveur des Réseaux Sociaux

- Déplacements du portefeuille baleine

- Transactions sur la chaîne (blockchain)

Des analyses en temps réel vous permettent de voir les facteurs d'entraînement du marché instantanément, permettant ainsi des opérations rentables avant que les conditions du marché ne changent.

Les investisseurs traditionnels s'appuient sur les tendances passées, mais le crypto récompense ceux qui comprennent clairement le présent.

Négocier à l'aveugle signifie perdre de l'argent

Des données retardées ? Vous manquez les points d'entrée et de sortie optimaux.

Des signaux obsolètes ? Vous tradez à la traîne.

Tomber pour le faux hype ? Vous en payez le prix.

Des informations en temps réel permettent des décisions plus intelligentes, des réactions plus rapides et une rentabilité constante.

Comment le Radar AI Edgen donne aux traders un avantage ultime

Edgen Radarintègre une IA avancée, des analyses approfondies sur la chaîne de blocs et une analyse précise du sentiment social en un outil de trading puissant et en temps réel. Comme l'a noté le Michigan Journal of Economics, AI is transforming financial markets by enhancing speed, efficiency, and precision in trading and market prediction.LSA Technology Services

Caractéristiques principales :

- Analyse du marché alimentée par l'IA : scanne instantanément de grands ensembles de données, identifie les tendances clés et fournit des informations exploitables.

- Suivi en temps réel sur la chaîne : Alertes immédiates concernant l'activité des portefeuilles de whales, les changements de liquidité et les mouvements importants de tokens.

- Scanneur d'Opinion Sociale : Surveillance en temps réel des influenceurs, KOL et des cryptomonnaies en hausse.

- Détection des signaux Alpha : des signaux de trading sélectionnés par l'IA qui identifient les actifs sous-évalués avant une hausse de prix.

- Notifications en temps réel : Alertes en temps réel avant que des mouvements majeurs du marché ne se produisent.

Alpha Signals : Voyez le marché comme un professionnel

Définition des signaux Alpha

Les signaux Alpha fournissent des indicateurs précoces des opérations rentables, montrant clairement les changements du marché avant que la masse ne s'en rende compte.

L'avantage Alpha d'Edgen AI :

- Filtre le bruit du marché, identifiant les opportunités rentables.

- Capture les débuts de la hype sociale.

- Détecte rapidement les signaux d'accumulation et de répartition des baleines.

Arrêtez de deviner. Négociez en toute confiance grâce aux Signaux Alpha.

Pourquoi les analyses en temps réel sont-elles essentielles, et non facultatives

Le risque de trader sans eux :

- Manquer entièrement des opérations rentables en raison d'un entrée retardée.

- Devenir victime de la hype du marché manipulé.

- Réagir constamment au lieu de trader de manière proactive, entraînant des pertes de gains.

Edgen AI offre des avantages clairs :

- Prévision du marché : Connaître les mouvements du marché avant qu'ils ne se reflètent dans les prix.

- Exécution précise : des analyses pilotées par l'IA permettent des décisions assurées.

- Avantage initial : Capturer les mouvements importants de prix avant que les traders principaux ne réagissent.

Les données en temps réel équivalent au trading de niveau professionnel. Sans cela, le succès reste hors de portée.

IA et données en temps réel : la révolution du trading est arrivée

Les marchés deviennent plus intelligents, plus agiles et plus compétitifs chaque jour. Les traders performants utilisent des outils alimentés par l'intelligence artificielle pour conserver leur avantage.

Le Radar Edgen le délivre clairement.

La vision d'Edgen Radar pour l'avenir du trading

Les marchés futurs dépasseront les indicateurs traditionnels et les graphiques statiques. L'analyse guidée par l'intelligence artificielle, le suivi des données en temps réel et l'exécution automatisée définiront le trading.

Imaginer clairement voir :

- Chaque mouvement important du marché est identifié immédiatement par l'IA.

- Des jetons sur le point de bondir repérés tôt.

- Notifications en temps réel basées sur le sentiment social et l'activité de la blockchain.

Edgen AI construit précisément cet avenir, et les traders utilisant Edgen Radar en deviennent partie intégrante.

Commerce. Agissez rapidement. Gagnez constamment.

Montez votre trading au niveau supérieur. EssayezEdgen Radar aujourd'hui.

Investir, enfin, tu n'es plus seul.

Essaie Edgen gratuitement. Sans carte, sans engagement.