Des fondamentaux aux « Pumpamentals » : comment l'opinion publique influence désormais les marchés

Le Marché s'est déplacé des chiffres vers les récits

Les marchés financiers ont changé. Les rapports de résultats, les bilans et les indicateurs traditionnels ne dominent plus les mouvements des prix. Les réseaux sociaux sont maintenant Wall Street. Un seul tweet d'un influenceur puissant, un seul mème viral, peuvent faire monter le cours d'une action en quelques minutes.

Les investisseurs traditionnels sont habitués à suivre les états de revenus, l'EBITDA et les ratios de dette. Les traders modernes suivent l'humeur sociale, les mouvements des portefeuilles blockchain et les récits de marché virals.Edgen AI permet aux traders de lire en temps réel l'orientation du marché, en capturant les changements avant qu'ils ne se produisent.

Fondamentaux vs.PumpamentalsUne nouvelle réalité

Qu'est-ce que les fondamentaux financiers ?

L'investissement traditionnel se concentre sur les indicateurs de la santé d'une entreprise :

- Rentabilité

- Croissance des revenus

- La stabilité financière

En bref, les investisseurs analysent les rapports trimestriels, les niveaux de dette et la qualité de la direction.

PumpamentalsL'essor du trading alimenté par le hype

Puis sont apparus les actions de type "meme". GameStop (GME), AMC et des actifs similaires ont connu une forte hausse sans résultats solides. Les prix ont augmenté fortement en raison de la dynamique des réseaux sociaux.

Les communautés en ligne ont généré des vagues d'achats massives, poussées par l'excitation et l'émotion du groupe. Ce phénomène (les fondamentaux de la pompe

Le rôle crucial de l'intelligence artificielle dansPumpamentals

L'IA est devenue essentielle pour le suivi et la prévision de l'opinion publique. Edgen AI utilise :

- Tendances de consensus sur Twitter/X

- Activité en temps réel d'un portefeuille de blockchain (alertes des grands porteurs, argent intelligent)

- Les récits des marchés émergents concernant les actifs de type "mème"

Le trading sans outils d'IA signifie la perte de signaux alpha.Edgen AIaide les traders à anticiper les changements du marché en avance.

La puissance de l'humeur sociale

Définir l'humeur sociale

L'opinion sociale reflète l'enthousiasme ou la négativité en ligne envers des actifs spécifiques. Les traders qui suivent Twitter, Reddit et les forums en ligne perçoivent les réactions des prix plus rapidement que par les médias traditionnels.

Pourquoi les sentiments influencent-ils les prix aujourd'hui

- Informations instantanées : les réseaux sociaux transmettent des signaux immédiatement, plus rapidement que les actualités financières traditionnelles.

- Influence du retail : Les investisseurs individuels s'organisent en ligne, remettant en question la finance traditionnelle.

- Des insights alimentés par l'IA : Edgen AI surveille les changements d'humeur en temps réel, offrant des signaux précoces cruciaux.

Suivi de l'humeur par l'intelligence artificielle

Edgen AI scanne en permanence les réseaux sociaux et les transactions sur la blockchain. Les traders obtiennent un avantage en :

- Repérer les tendances virales tôt

- Surveillance des portefeuilles influents (argent intelligent et baleines)

- Évaluer l'impact des leaders d'opinion (KOL)

Le trading par IA est essentiel pour l'investissement moderne.

Les actions Meme et le phénomène de l'investissement viral

Même Actions, définies

Les actions des entreprises spéculatives montent rapidement en raison de la hype sociale plutôt que des fondamentaux. Les investisseurs individuels se coordonnent via des communautés comme r/WallStreetBetscréant des vagues d'achats explosives.

La montée historique du prix de GameStop

GameStop (GME) a négocié à des niveaux faibles jusqu'à ce que les communautés de Reddit s'organisent.Massif coordonnél'achat a déclenché une couverture à la baisse, poussant les actions de 20 à 500 dollars en quelques jours.

La logique financière traditionnelle n'a pas pu prédire cela. La dynamique motivée par les réseaux sociaux a dominé.

La Finance comportementale : pourquoi les investisseurs suivent la foule

Les moteurs psychologiques derrièrePumpamentals

La finance comportementale explique les décisions du marché motivées par des émotions plutôt que par la logique :Explore key behavioral biases and their impact on financial decisions.

- Crainte de manquer quelque chose (FOMO) : Les investisseurs se précipitent pour acheter des actifs en hausse.

- Comportement mémétique : Les gens suivent l'opinion populaire, en ignorant les avertissements traditionnels.

- Biais de confirmation : Les investisseurs privilégient les informations qui s'alignent avec leurs croyances existantes, en ignorant les risques.

LeVolfefeIndex : Mesurer l'influence sociale

Les influenceurs comme Elon Musk ont un impact important sur les prix des actifs. Les tweets de Musk seuls ont provoqué des variations importantes dans le prix du Dogecoin et de Tesla. LeVolfefeL'indice suit l'impact du marché des publications sociales influentes, soulignant l'importance des analyses sociales alimentées par l'intelligence artificielle, comme Edgen AI.

Données alternatives et analyse du sentiment renforcée par l'intelligence artificielle

Comprendre les données alternatives

L'investissement traditionnel utilisait les états financiers et les rapports trimestriels. Maintenant, les traders utilisent l'effet de levier :

- Les tendances des réseaux sociaux

- Les transactions de crypto monnaie sur la chaîne

- Analyse des recherches Google

- Données de sentiment du marché alimentées par l'IA

Les données alternatives révèlent des opportunités du marché avant qu'elles ne s'expriment dans l'évolution des prix.

Edgen AI : façonner l'avenir du trading

Comment Edgen AI donne aux traders un avantage compétitif

Edgen AI fournit une infrastructure complète pour le trading du côté acheteur, en suivant simultanément :

- Les mouvements des portefeuilles intelligents (les grands détenteurs et les influenceurs)

- Consensus social et récits viraux (Twitter/X)

- Les changements de sentiment pilotés par l'IA

Négocier aujourd'hui sansDes insights alimentés par l'IAC'est comme investir avec des bandeaux sur les yeux.

Caractéristiques principales du Core Edgen AI :

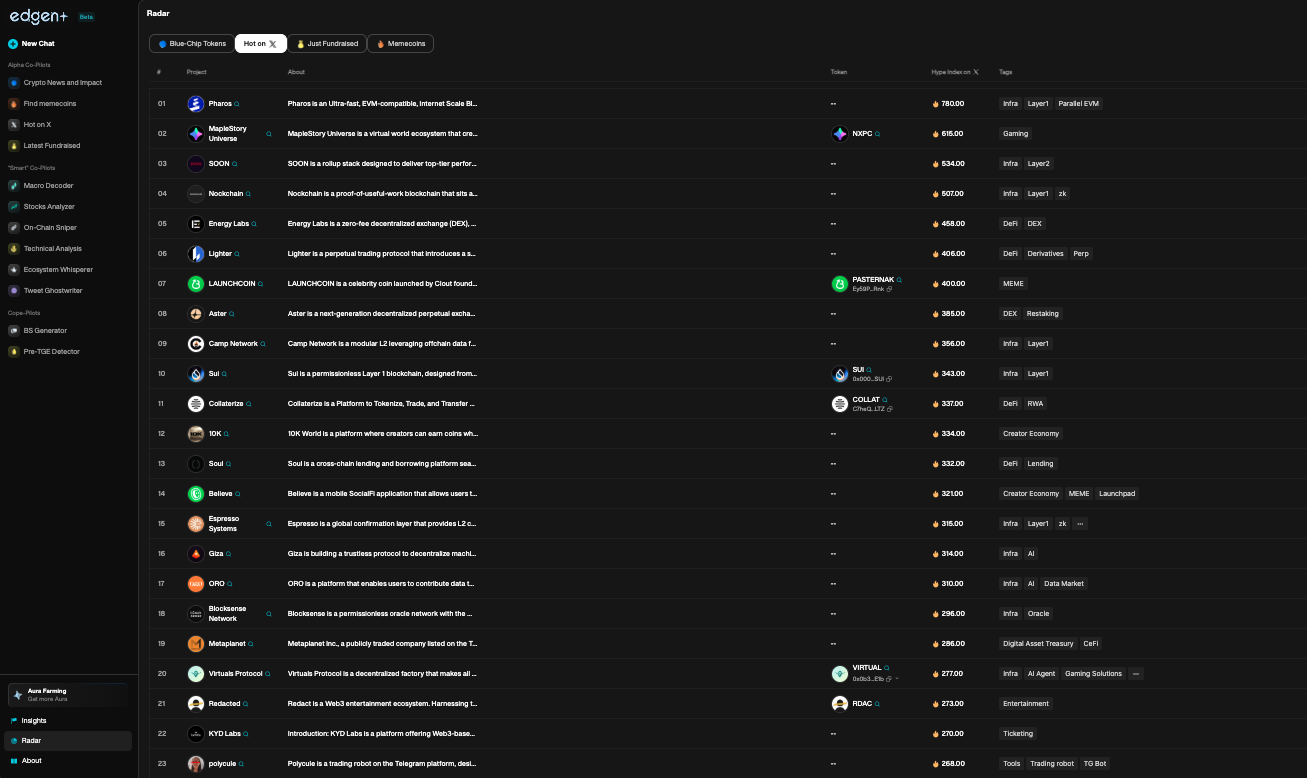

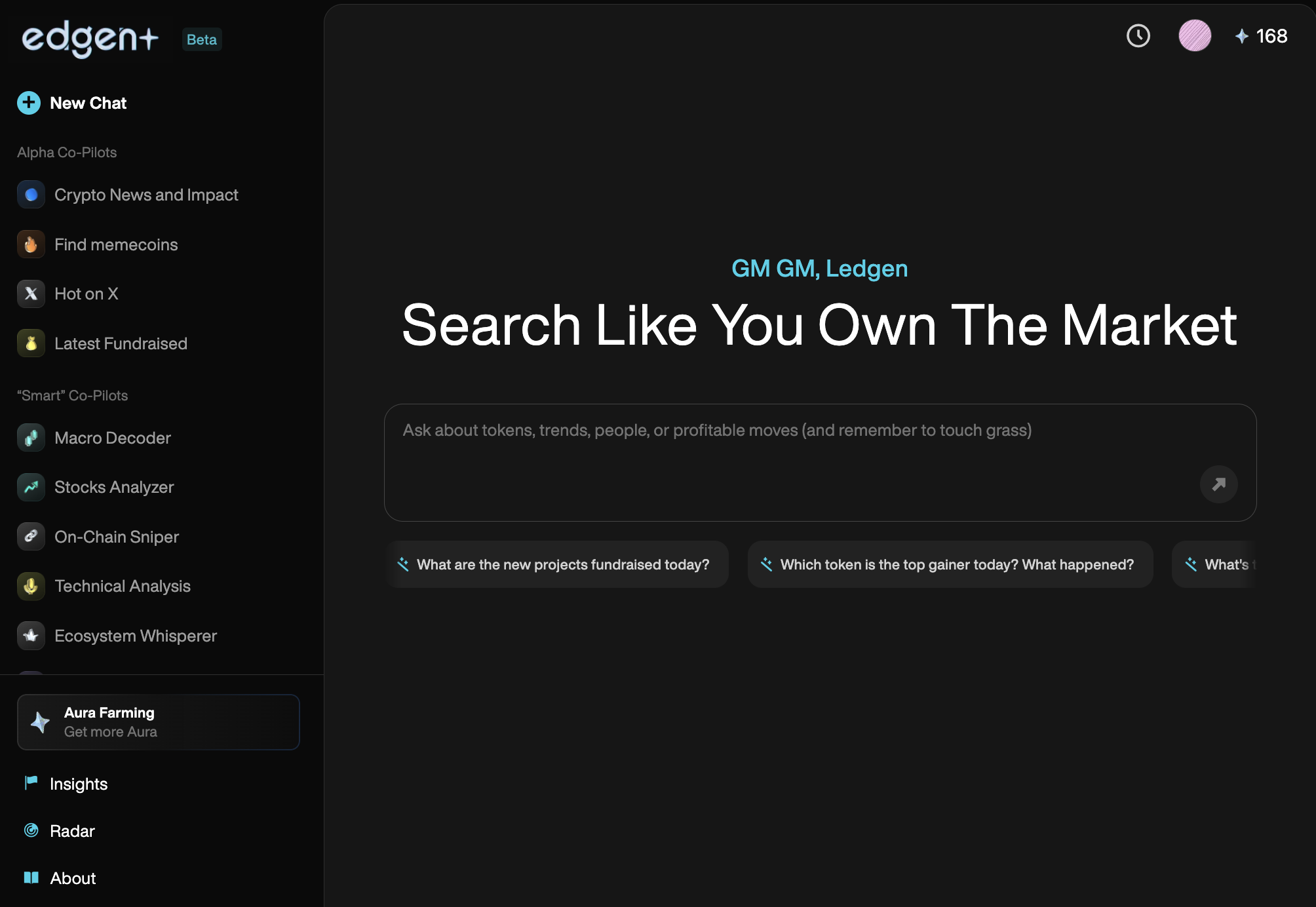

- Edgen RadarSurveillance en temps réel de l'orientation du marché et des tendances.

- Edgen SearchRéponses immédiates appuyées par des analyses orientées marché.

- Edgen InsightsDes informations de marché alpha et opportunes issues du collectif de la communauté.

Pourquoi cela est-il important

Les marchés des actifs numériques et des cryptomonnaies prospèrent également sur les cycles de hype. Les plateformes commeWallStreetBetsa montré que la dynamique sociale l'emporte sur les indicateurs financiers traditionnels dans les mouvements des prix.

Edgen AIaide les traders à identifier et à agir sur cesles fondamentaux de la pompetôt, capturer l'alpha avant que les tendances ne soient pleinement établies.

Adaptez-vous ou devenez obsolète

Le paysage de l'investissement a évolué. Les rapports financiers seuls ne font plus bouger les marchés. À la place, l'opinion sur les réseaux sociaux, les récits des influenceurs et l'analyse guidée par l'intelligence artificielle façonnent le trading.

Edgen AI fournit aux traders les outils pour :

- Suivre et répondre aux changements de sentiment en temps réel

- Surveiller les mouvements de l'argent intelligent

- Réagir de manière décisive aux récits du marché émergent

Les traders qui ignorent les analyses alimentées par l'intelligence artificielle font face à des concurrents qui négocient plus vite, plus intelligemment et mieux informés.

Le futur est arrivé. Le succès dans le commerce dépend maintenant de votre capacité à utiliser les outils d'IA. L'ère deEdgen AIle commerce a commencé. Restezavant, ouReste en arrière. Ton tour.

Investir, enfin, tu n'es plus seul.

Essaie Edgen gratuitement. Sans carte, sans engagement.