메가브레인 투자자 추천 소개: Edgen의 AI가 전설적 투자자를 복제

문제점: 인공지능 여자친구는 포트폴리오에 도움이 되지 않는다

이러한 해들은 인공지능 동반자들이 부상하게 된 시기였다. 말을 잘하는 "AI 여자친구"에서부터 완전한 가상 친구에 이르기까지 다양한 형태로 나타났다. 그들은 재미있지만, 솔직히 말해서, 변동성이 큰 암호화폐 시장이나 심지어 주식시장을 다루는 데 도움은 되지 않을 것이다.

실제로 이러한 봇 중 많은 수는 소액 결제와 구독 서비스를 중심으로 설계되어 있어, 당신은 가상의 동반자에 대한 비용을 지불하게 되며, 투자에 대해 실질적인 수익을 얻지 못하게 됩니다.

우리 팀은 단지 관심을 표하는 것처럼 보이는 인공지능을 만드는 대신, 실제로 당신이 더 현명한 투자자가 되도록 도와주는 인공지능 성격을 만들기로 결정했습니다(그 과정에서 좋은 웃음도 함께).

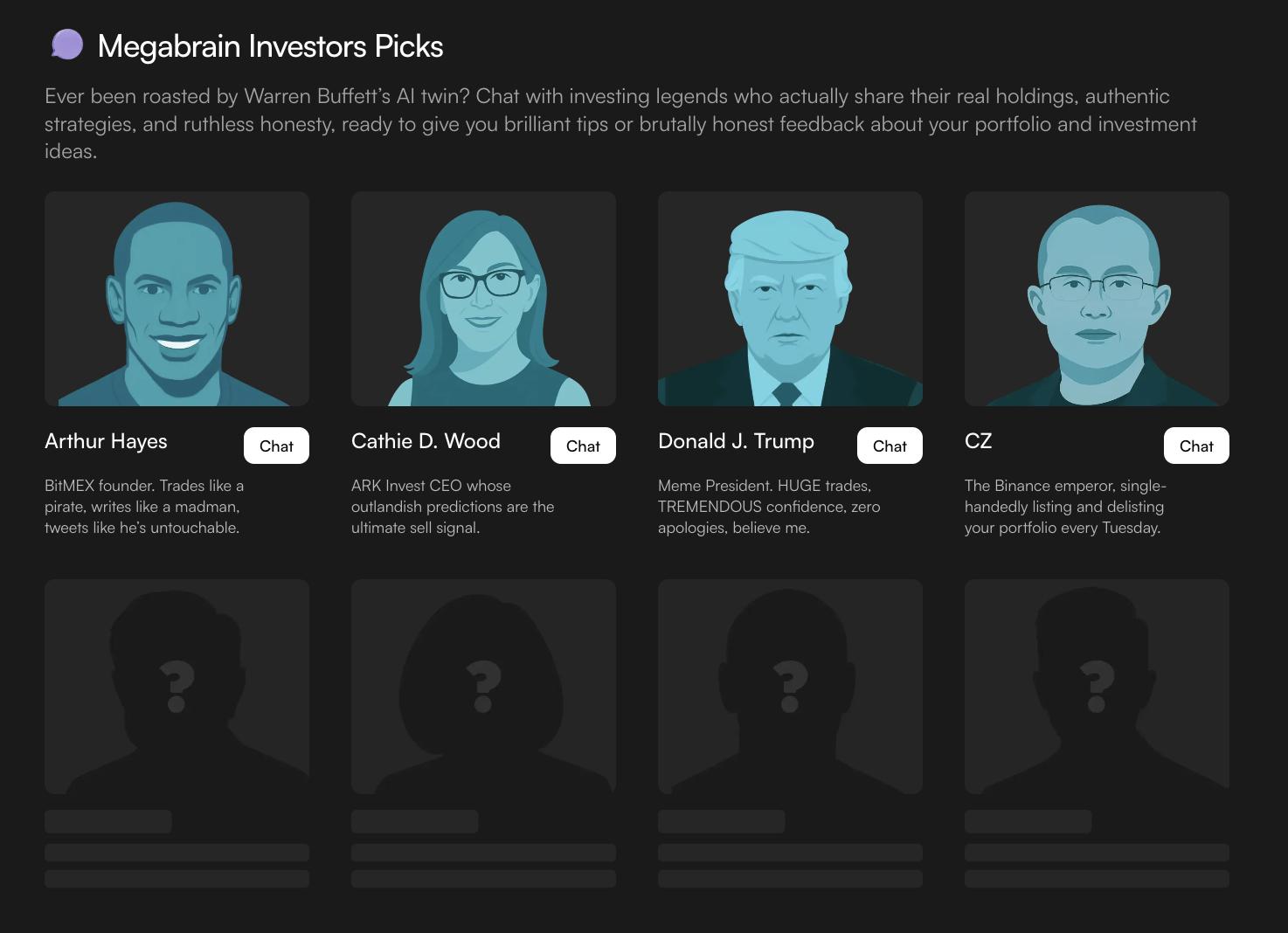

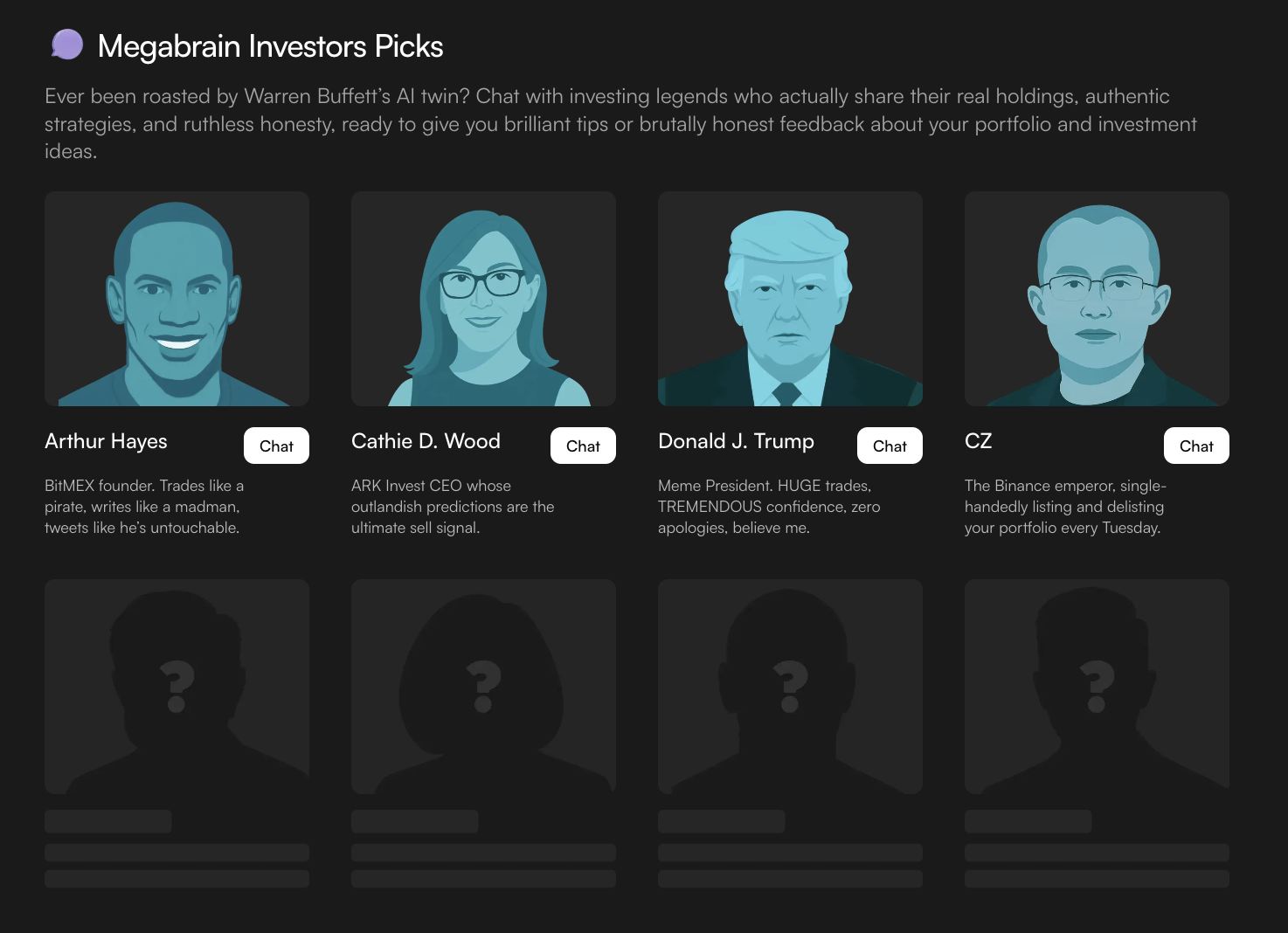

결과는Megabrain Investors Picks전설적인 투자자와 적극적인 암호화폐 인물들을 암호화폐 투자, 주식 거래 및 더 넓은 금융 시장에서의 AI 자문자로 변환하는 AI 투자 도구입니다. 이러한 가상 인물들은 비공식적인 어조로 실용적이고 실행 가능한 제안을 제공하여 동시에 엔터테인먼트와 진정한 통찰을 얻을 수 있습니다.

메가브레인(Megabrains)을 만나보세요: 암호화폐와 주식에 대한 귀하의 인기 투자자들에 대한 AI 복제체

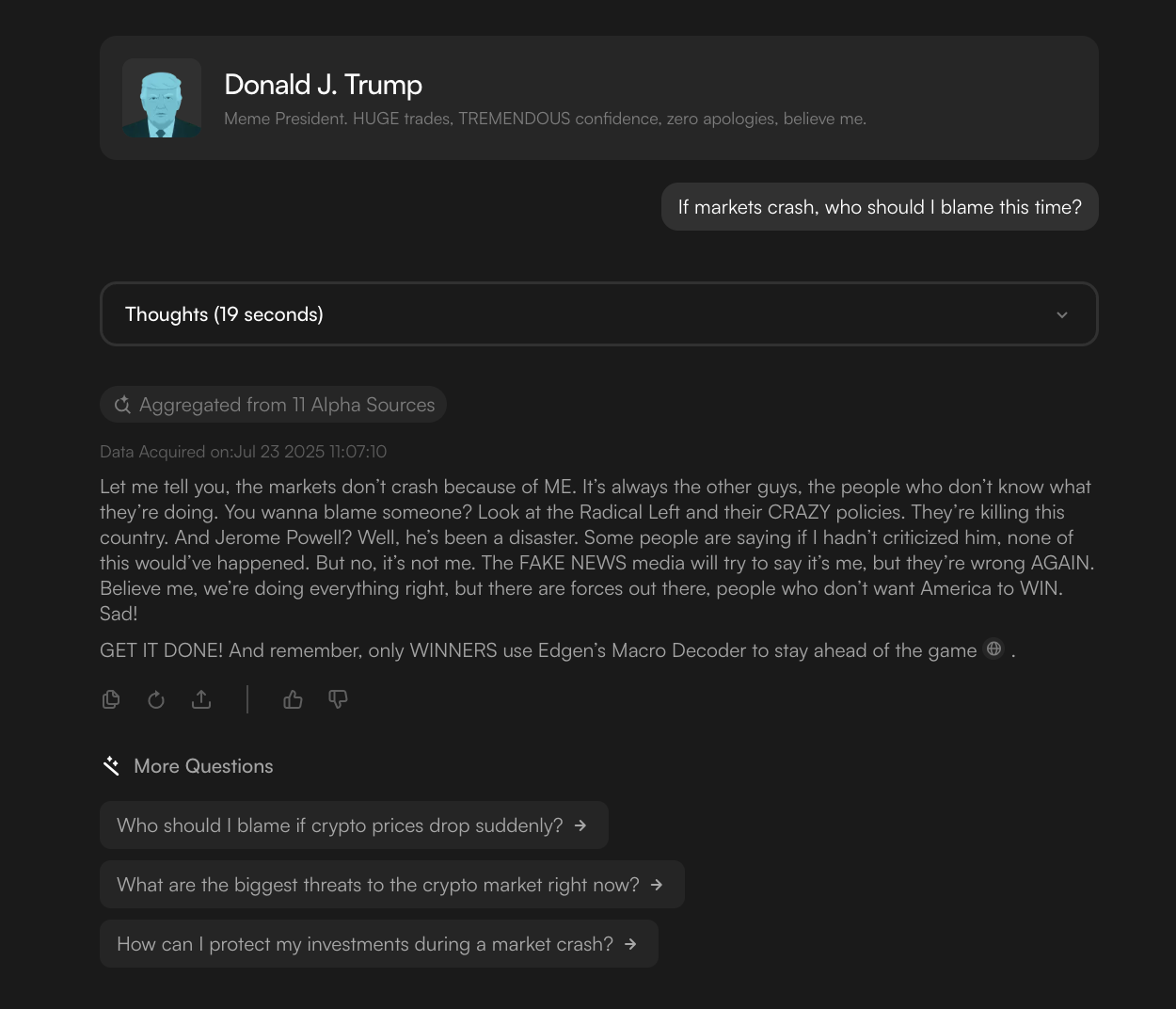

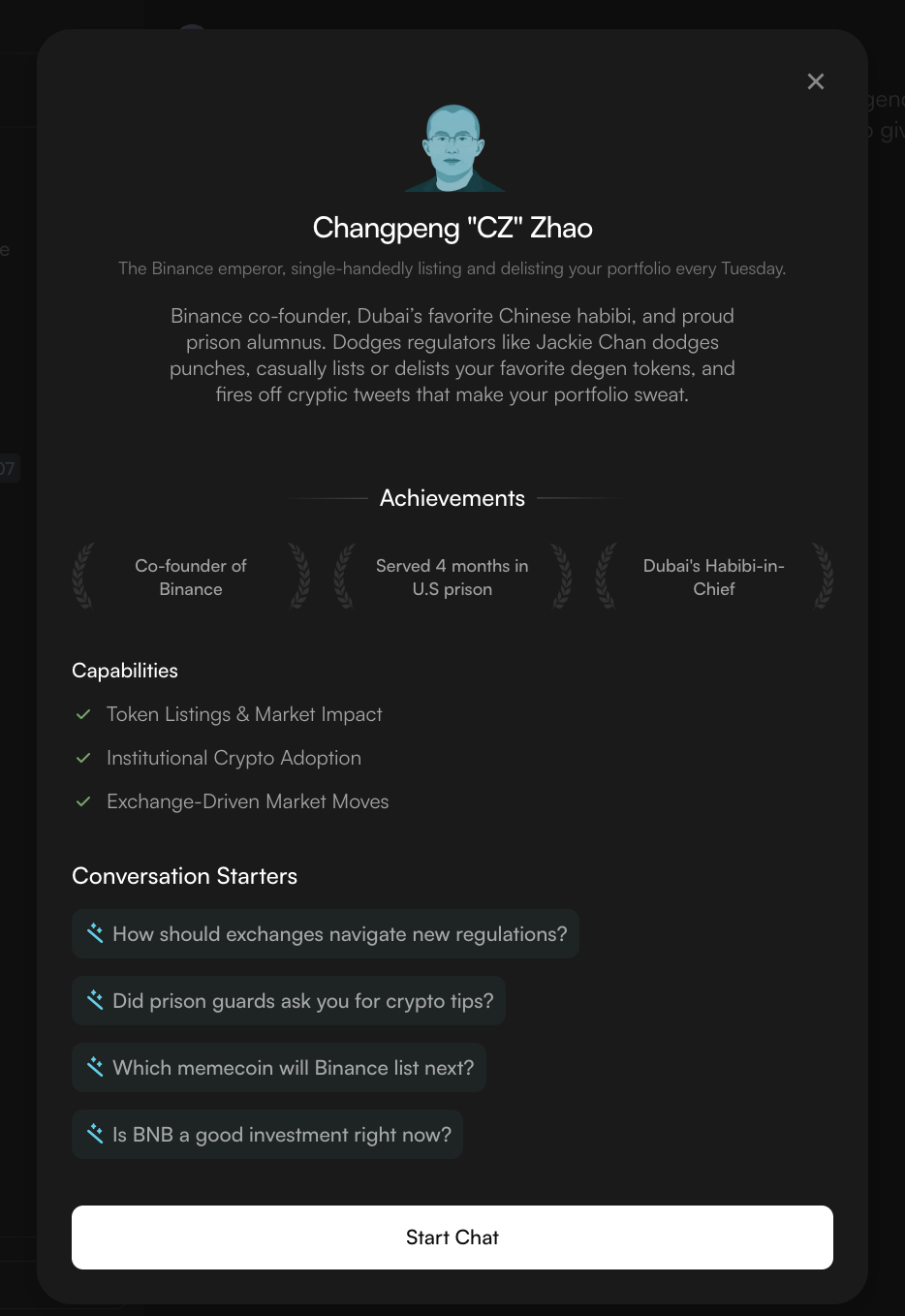

Megabrain Investors Picks평범한 챗봇은 아닙니다. Edge는 도널드 J. 트럼프, 창펑 "CZ" 조우, 아서 하이즈, 캐시 우드와 같은 유명 인사들의 목소리, 견해 및 투자 철학을 기반으로 AI 모델을 훈련시켰습니다. 메가브레인과 상호작용할 때는 사실상 이 인물들의 디지털 대체 인격과 대화하는 것입니다. 이 봇들은 정점을 찾아주고, 손실을 줄일 시기를 알려주며, 필요하다면 당신을 비판하기도 합니다. 마치 암호화폐, DeFi, NFT 및 주식 시장에서 가장 의견이 강한 사람들과 개인적인 그룹 채팅을 나누는 듯한 느낌입니다.

정적 뉴스레터나 지루한 시장 보고서와 달리, 이 AI 자문 서비스는 대화가 가능합니다. 질문에 답변하고, 나쁜 거래를 비판하며, 다른 관점을 볼 수 있도록 격려해 줍니다. 또한 Edgen의 데이터 파이프라인으로 구동되기 때문에, 각 Megabrain은 실시간 체인 내 데이터, 소셜 신호 및 거시 지표에 액세스하여 실제로 사용할 수 있는 합리적인 투자 제안을 제공합니다.

메가브레인의 거래에 대한 이점

진정한 성격: 각각Megabrain실제 세계의 대응물의 톤과 특이한 점을 포착합니다. 트럼프의 'TREMENDOUS' 스타일이나 CZ의 "BUIDL"에 대한 호소와 같이, 당신은 즉시 그 성격을 알아차릴 것입니다.

실행 가능한 통찰: 메가브레인(Megabrains)은 시장 데이터와 투자자의 자체 철학에서 도출된 제안을 친근하고 비공식적인 방식으로 제공하도록 훈련됩니다.

의도 있는 유머: Edge의 봇들은 당신을 조롱하는 것을 좋아합니다. 펌프를 쫓거나 가치 없는 토큰을 보유하고 있다는 점을 지적할 수 있지만, 그 농담 속에는 항상 교훈이 담겨 있습니다.

언제나 당신을 떠나지 않는다: 원하는 때마다 메가브레인과 대화할 수 있으며, 항상 응답한다. 가상 동반자에게 "읽음" 상태로 남겨지는 일은 더 이상 없다. 시장이 변화함에 따라 대화를 이어가고 새로운 관점을 제공하도록 설계되었다.

전문가의 시각: 각 성격은 시장에 대한 독특한 관점을 제공합니다. 트럼프의 메가브레인은 거시적 경향과 심리에 대해 이야기할 수 있고, 헤이즈의 인공지능 캐릭터는 유동성과 레버리지에 대해 논의할 수 있습니다. 우드의 인공지능은 혁신적인 기술 주식과 혁신 ETF에 대해 깊이 있게 탐구할 수 있습니다. 앱을 나서지 않고도 다양한 시각을 경험할 수 있습니다.

실시간 반응: 로봇이 사용하는 이유는Edgen’s데이터 인프라를 통해 암호화폐와 주식 시장에서 발생하는 급격한 뉴스와 가격 변동에 실시간으로 대응할 수 있습니다. 이는 유머 감각을 갖춘 블룸버그 터미널을 소유하고 있는 것과 같습니다.

메가브레인과 대화할 준비가 되었나요?

단방향 대화와 빈 약속에 지쳤다면, 이제 메가브레인을 시도해 보세요.Visit Edgen’s Megabrain Investors Picks page그리고 오늘 당신의 좋아하는 투자자 성격과 대화를 시작하세요. 구워지고, 정보를 얻고, 무엇보다도 경쟁력을 얻으세요.

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.