Comment utiliser l'IA pour des investissements cryptos plus intelligents

Comment utiliser l'IA pour des investissements cryptos plus intelligents

∙ Titre SEO : Comment utiliser Edgen AI pour des investissements cryptos plus intelligents

∙ Description : Découvrez comment Edgen AI combine l'analyse on-chain, les signaux prédictifs et l'intelligence de portefeuille pour aider les investisseurs crypto à prendre des décisions plus rapides et basées sur les données.

∙ Mots-clés : Edgen AI, investissement crypto, analyse blockchain, co-pilote d'investissement IA, intelligence on-chain, signaux prédictifs, optimisation de portefeuille, découverte d'alpha, prévision de marché

L'avenir de l'investissement crypto intelligent

Le succès dans la cryptomonnaie dépend du timing, des données et de la clarté. Les prix changent en quelques secondes, le sentiment se retourne du jour au lendemain, et les opportunités disparaissent aussi vite qu'elles apparaissent. Les investisseurs qui restent en tête sont ceux qui comprennent avant que le marché ne réagisse.

Edgen a été conçu dans ce but. Il unifie l'analyse IA, les données blockchain et l'intelligence sociale en un système adaptatif unique. Grâce à des agents tels que Technical Signals, Pre-TGE Detector et Trading Mindshare, il transforme le bruit du marché en informations structurées.

Ce guide explique comment utiliser l'écosystème d'Edgen pour prendre des décisions plus pertinentes, gérer la volatilité et découvrir des opportunités dans l'ensemble du paysage des actifs numériques.

II. Comprendre l'écosystème d'Edgen

1. Qu'est-ce qui rend Edgen différent ?

Edgen AI fusionne l'apprentissage automatique, la transparence de la blockchain et les données comportementales pour offrir aux investisseurs une image complète du marché. Son système intégré fournit :

- Des informations sur le marché en temps réel

- La génération de signaux alpha

- L'analyse prédictive des risques

- Le suivi du sentiment du marché

- Des outils d'optimisation de portefeuille

Tous les modules fonctionnent en synchronisation au sein de l'application Edgen, de sorte que les mises à jour restent cohérentes sur tous les appareils.

2. Utiliser l'IA pour des décisions plus intelligentes

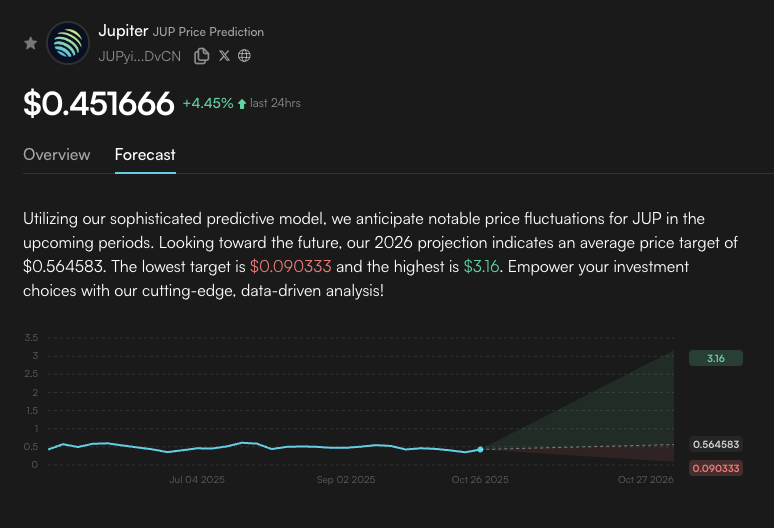

Les algorithmes d'Edgen détectent les inefficacités avant qu'elles ne deviennent visibles. Le rapport 360° agrège les indicateurs techniques et fondamentaux, produisant des prévisions et des analyses de tendances en temps réel.

Pour les nouveaux utilisateurs, le centre d'apprentissage d'Edgen offre une voie de démarrage claire pour l'intégration d'outils prédictifs dans les flux de travail quotidiens.

3. Intégrer l'analyse On-Chain et les signaux de marché

L'On-Chain Sniper d'Edgen surveille l'activité de la blockchain pour identifier les mouvements de baleines et les tendances d'accumulation précoce. Combiné aux signaux Alpha, il convertit les données de transaction en points d'entrée et de sortie exploitables.

Le Pre-TGE Detector met en évidence les lancements de tokens à venir, aidant les utilisateurs à se positionner tôt avant une plus large connaissance du marché.

4. Gérer les risques dans des conditions volatiles

La volatilité des cryptomonnaies est à la fois une opportunité et un risque. La suite de gestion des risques d'Edgen permet aux utilisateurs de définir des alertes personnalisées et des règles d'automatisation pour les baisses de prix ou les inversions de sentiment.

Lors des récentes fluctuations du marché, ce système a fourni des avertissements en temps réel qui ont aidé les traders à verrouiller les gains ou à réduire l'exposition avant des changements soudains.

III. Fonctionnalités avancées qui redéfinissent la connaissance du marché

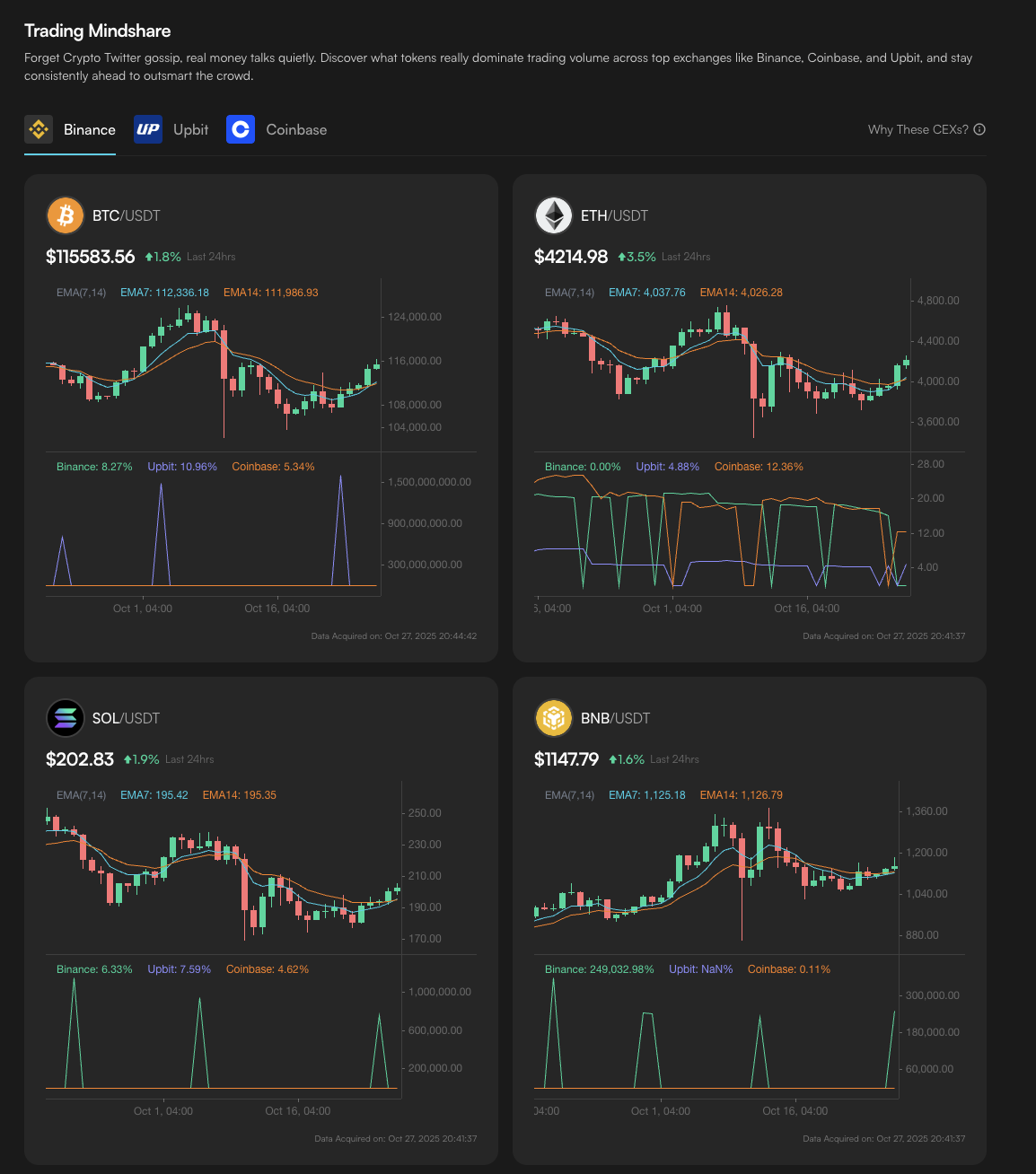

1. Part de marché des opérations (Trading Mindshare)

Cet agent mesure les flux de liquidités en analysant les données des principales bourses. Il interprète les changements dans le ton et le niveau d'intérêt de la communauté, fournissant une première indication de l'humeur concrète du marché au-delà du sentiment social.

2. Signaux techniques

Edgen évalue des indicateurs tels que le RSI, le MACD et les bandes de Bollinger par le biais de l'apprentissage automatique. Chaque résultat est vérifié par rapport au comportement historique du marché pour garantir sa fiabilité.

3. Diagnostics de portefeuille

Le rapport 360° intègre les positions, les métriques de sentiment et le positionnement on-chain dans un résumé de performance continue. Associé à Pivot Alert, il permet une gestion proactive du portefeuille grâce à des avertissements précoces et des recommandations de rééquilibrage.

IV. Rester informé grâce aux nouvelles intégrées

Edgen regroupe les mises à jour vérifiées provenant de plusieurs sources du marché.

Les utilisateurs peuvent suivre :

- L'analyse du réseau Bitcoin et Ethereum

- Les rapports du secteur DeFi et les flux de tokens

- Les développements du marché NFT

- Les changements réglementaires et macroéconomiques affectant les actifs numériques

Ce flux garantit que les décisions reposent sur un contexte précis et à jour.

V. Construire une routine d'investissement intelligente

La force d'Edgen réside dans la connexion de toutes les couches de l'intelligence du marché en une seule boucle de rétroaction.

- L'analyse on-chain montre ce que font les grands détenteurs.

- Les signaux techniques révèlent où les tendances se renforcent ou s'affaiblissent.

- Les données de sentiment expliquent comment les récits évoluent.

- Les diagnostics de portefeuille traduisent tout cela en recommandations claires.

Plus vous utilisez Edgen de manière cohérente, plus ses modèles s'adaptent rapidement à vos habitudes d'investissement, affinant les alertes et les prévisions selon votre stratégie personnelle.

VI. Maîtriser le marché avec Edgen

Les données sont l'actif le plus précieux dans le trading. Edgen AI donne aux investisseurs la capacité d'interpréter ces données avec précision et confiance.

Grâce à l'analyse prédictive, la découverte d'alpha et le contrôle des risques, il transforme l'information en avantage stratégique.

Commencez à utiliser Edgen AI today pour découvrir comment l'intelligence, la clarté et le timing peuvent définir la prochaine étape de votre parcours d'investissement crypto.

Investir, enfin, tu n'es plus seul.

Essaie Ed gratuitement. Sans carte, sans engagement.