Cách giao dịch token AI và memecoin: Hướng dẫn cho người mới bắt đầu đầu tư tiền mã hóa thông minh

Tương lai của Giao dịch Tiền mã hóa Là Trí tuệ Nhân tạo: Giới thiệu Edgen AI

Giao dịch tiền mã hóa thay đổi với tốc độ ánh sáng. Nháy mắt, bạn sẽ bỏ lỡ điều gì đó lớn tiếp theo. Gần đây, hai xu hướng đã thống trị các tiêu đề: các loại tiền mã hóa được hỗ trợ bởi AI vàtiền xu memegiao dịch. Những thứ này là gì và tại sao bạn nên quan tâm?

Các token được hỗ trợ bởi AI sử dụng trí tuệ nhân tạo để dự đoán các chuyển động trên thị trường, phát hiện xu hướng và thực hiện giao dịch với độ chính xác cao.Tiền mã hóa Memecoins, đồng thời, là các loại tiền mã hóa vui nhộn được lấy cảm hứng từ các trào lưu mạng xã hội và văn hóa trực tuyến. Chúng thường bắt đầu như những trò đùa nhưng thỉnh thoảng lại bùng nổ thành các khoản đầu tư nghiêm túc (nhìn về phía bạn, Dogecoin).

Với các nền tảng nhưEdgen AI, các nhà giao dịch có phân tích thị trường thời gian thực, theo dõi mọi thứ từ tâm lý xã hội đến dữ liệu trên chuỗi. Nếu bạn là người mới, hãy chuẩn bị: hướng dẫn này giải thích chính xác những loại token vàmemecoingiao dịch là gì, cách hoạt động như thế nào và làm thế nào để đầu tư thông minh và an toàn.

Giao dịch Tiền mã hóa được hỗ trợ bởi Trí tuệ nhân tạo là gì?

Nói đơn giản, giao dịch được hỗ trợ bởi AI sử dụng các thuật toán tiên tiến để phân tích giao dịch tiền mã hóa thông minh và nhanh hơn. Nó được thúc đẩy bởi dữ liệu, mô hình dự đoán và học máy.

Tại sao Trí tuệ nhân tạo (AI) lại quan trọng trong giao dịch tiền mã hóa:

- Khả năng xử lý dữ liệu:AI phân tích hàng núi dữ liệu thị trường một cách tức thời.

- Độ chính xác dự đoán:Các biến động giá cả trước đàn gia súc.

- Giao dịch vô cảm:Loại bỏ thiên vị của con người và sai lầm do hoảng loạn.

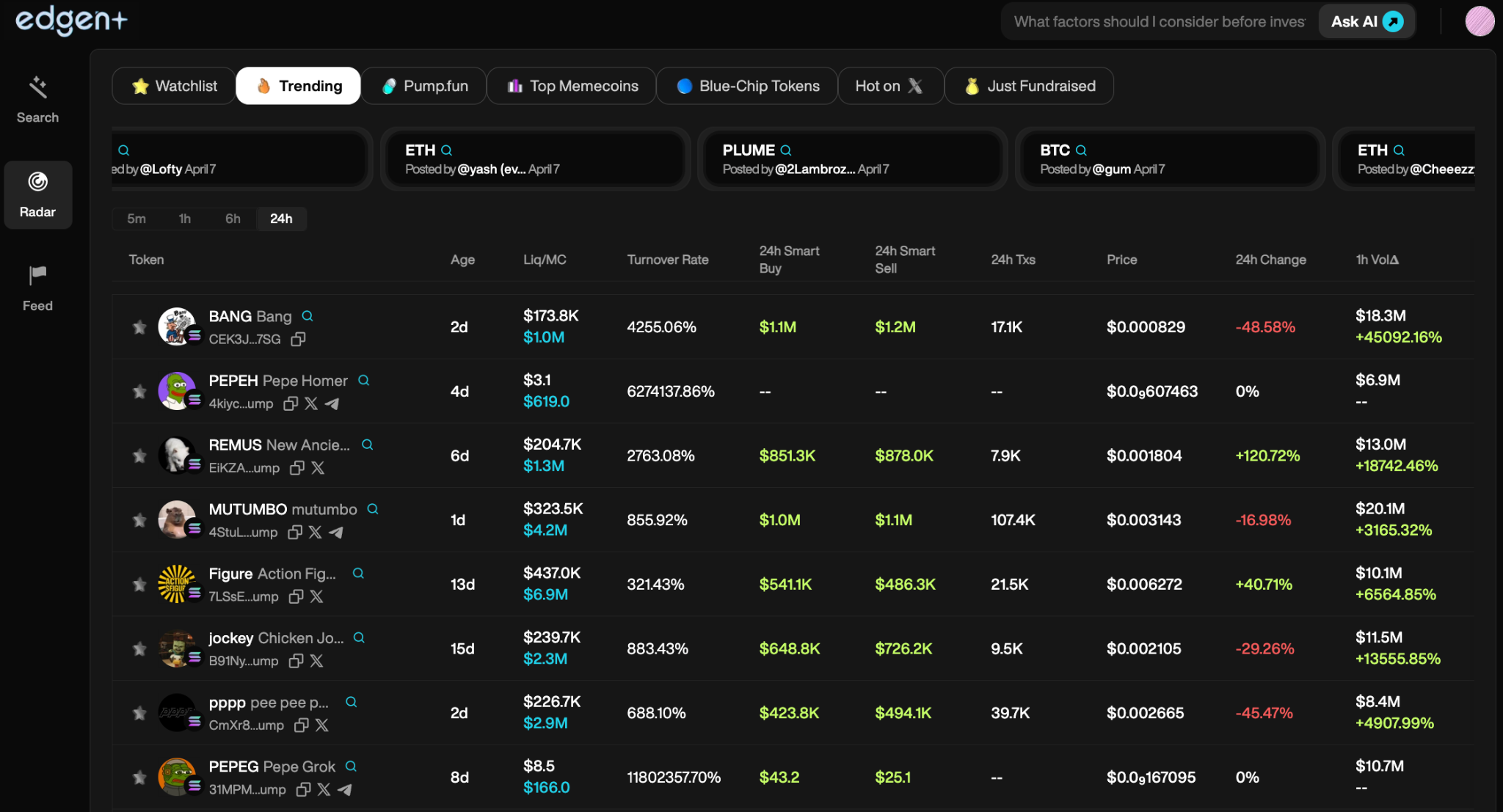

- Theo dõi Cảm xúc Xã hội:Phát hiện tăng huyết áp sớm bằng các công cụ như Edgen Radar

Giao dịch tiền mã hóa mà không có AI? Thật dễ thương... nhưng đã lỗi thời rồi.

Tiền mã hóa MemecoinsGiải thích: Nhiều Hơn Chỉ Là Những Câu Nói Đùa?

Tiền mã hóa Memecoinslà các loại tiền tệ mã hóa bắt chước văn hóa và hài hước trên mạng internet, biến sự phổ biến lan truyền thành giá trị tiền mã hóa. Ra đời từ các trào lưu, chúng phát triển nhờ sự hào hứng của cộng đồng và xu hướng lan truyền.

Nổi tiếngTiền mã hóa Memecoins:

- Dogecoin (DOGE):Vui lòng dịch đoạn văn tiếng Anh sau sang tiếng Việt. Giữ nguyên cấu trúc và thuật ngữ kỹ thuật chính xác. Tránh dịch quá mức.memecoin, được sinh ra từ một trò đùa, nay là một người chơi nghiêm túc.

- Shiba Inu (SHIB):Kẻ địch phổ biến của Dogecoin, cộng đồng lớn, biến động mạnh.

- Pepe Coin (PEPE):Lấy cảm hứng từ meme Pepe the Frog nổi tiếng, đã nhanh chóng trở thành một hiện tượng cult.

Tại sao nên đầu tư vàoTiền mã hóa Memecoins?

- Tăng trưởng do cộng đồng dẫn dắt:Tiền mã hóa Memecoinsnổ tung khi sự hào hứng gặp FOMO.

- Tiềm năng thưởng cao:Lợi nhuận (và tổn thất) nhanh chóng thường xuyên xảy ra.

- Vui nhộn Văn hóa:Đầu tư vàotiền xu memethường có nghĩa là tham gia vào một cộng đồng sôi động.

Nhưngtiền xu memeđi kèm với cảnh báo rủi ro cao: chúng biến động và không thể dự đoán. Sử dụngEdgen Radar, các nhà buôn có thể theo dõi xu hướng xã hội theo thời gian thực, mang lại lợi thế trong việc điều hướng sự kiện.memecoinkệ trượt.

Cách AI đang cách mạng hóa giao dịch tiền mã hóa

AI không chỉ là một tiện nghi; đó là tiêu chuẩn mới trong đầu tư hiện đại. Từ dự báo thị trường đến thực thi tự động, AI giúp các nhà giao dịch hoạt động chính xác. Nếu bạn muốn khám phá cách những công nghệ này đang thay đổi tài chính truyền thống, hãy truy cập vào CFA Institute’s report on AI in asset managementHãy dịch đoạn văn tiếng Anh sau sang tiếng Việt. Giữ nguyên cấu trúc và thuật ngữ kỹ thuật chính xác. Tránh dịch quá mức.

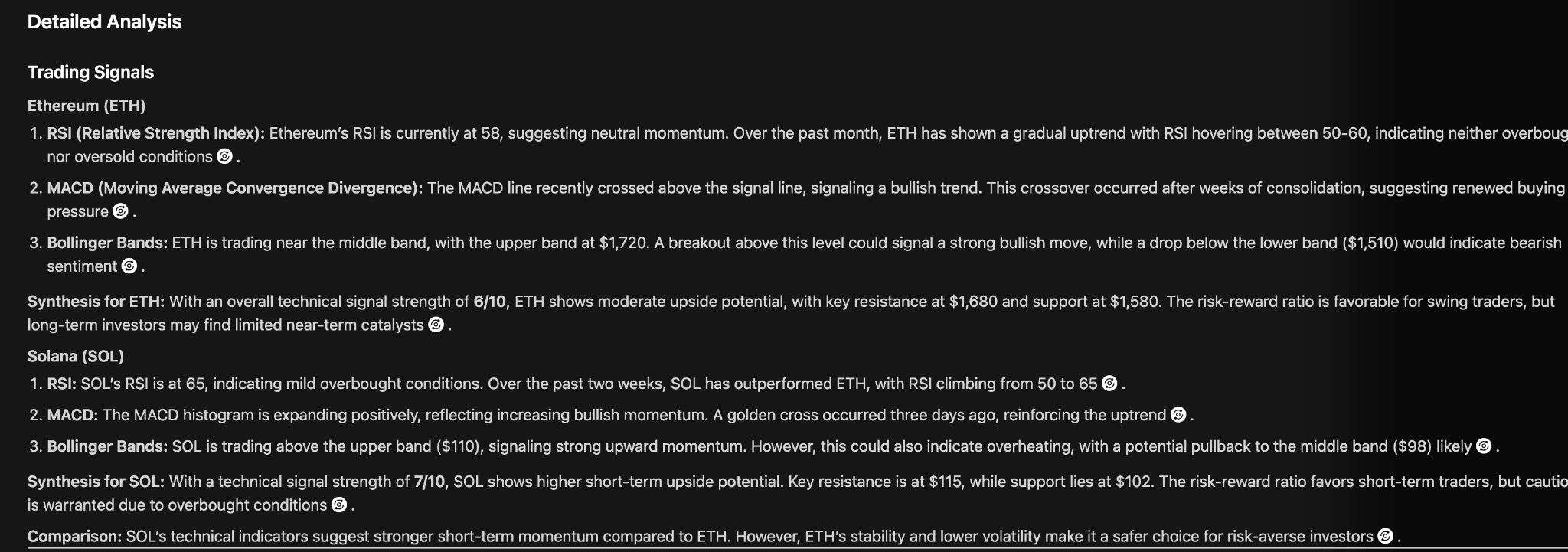

Phân tích thị trường dự đoán

AI phân tích các mô hình và dự đoán biến động thị trường nhanh hơn các nhà giao dịch con người có thể phản ứng.

2. Bot giao dịch tự động

Các bot AI thực thi chiến lược 24/7, tối ưu hóa hiệu quả giao dịch của bạn mà không có thời gian nghỉ.

3. Cảm xúc Thời gian Thực ("Pumpamentals")

Edgen AItheo dõi các tài khoản thông minh, KOLs và làn sóng mạng xã hội. Bạn sẽ phát hiện ra xu hướng tiếp theo đang lan truyềnmemecoinsớm, không muộn.

4. Loại bỏ cảm xúc

Con ngườisự hoảng loạn,AI thì không. Các quyết định giao dịch được thực hiện dựa trên dữ liệu, có kỷ luật và đáng tin cậy.

5. An ninh được nâng cao

AI phát hiện gian lận, hoạt động đáng ngờ và các vụ lừa đảo nhanh hơn, giúp tài sản kỹ thuật số của bạn an toàn hơn.

Hướng dẫn từng bước: Đầu tư vào Tiền tệ vàTiền mã hóa MemecoinsVới AI

Sẵn sàng giao dịch thông minh hơn? Đây là sách hướng dẫn của bạn:

Bước 1: Nghiên cứu như một chuyên gia

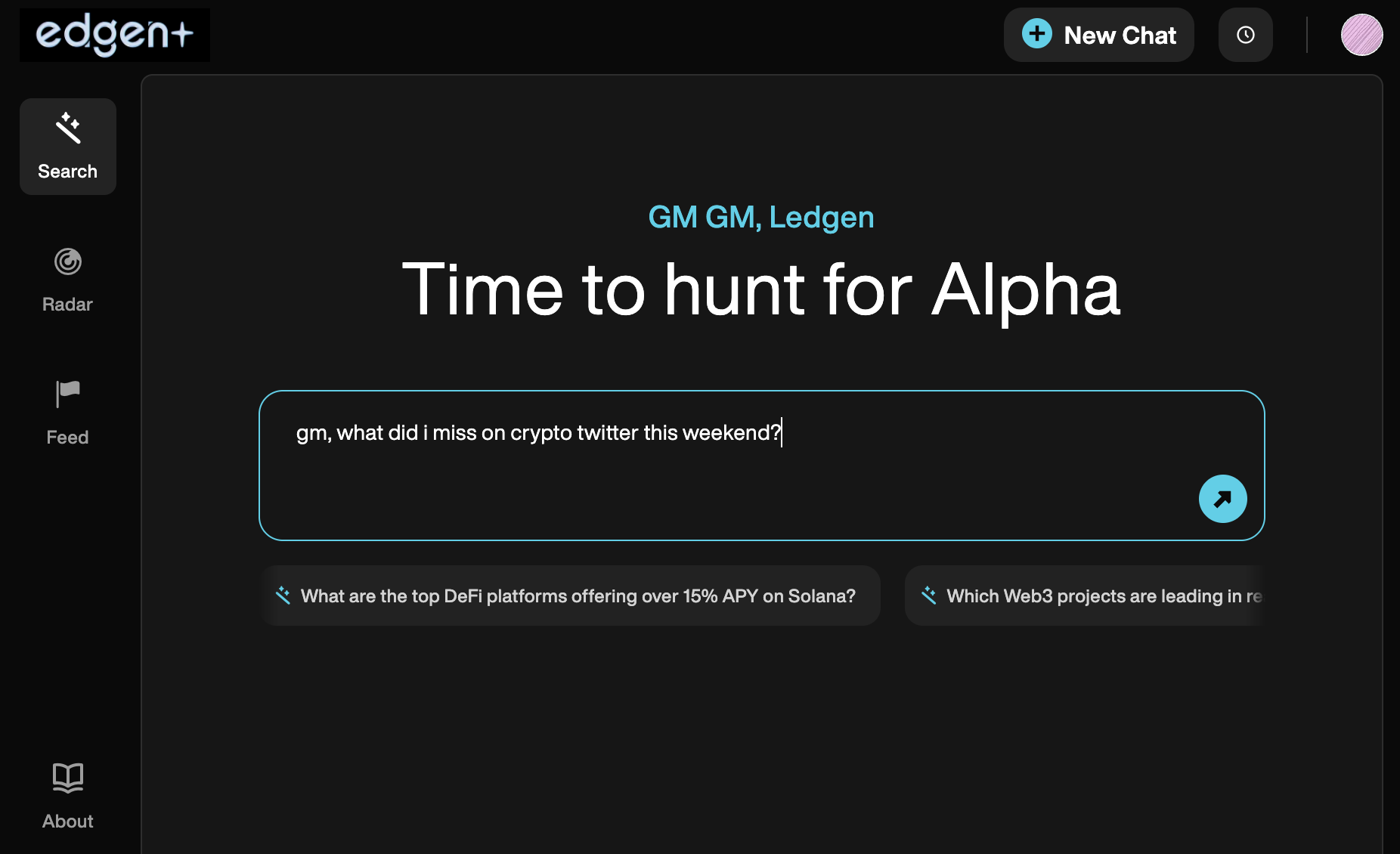

Sử dụngEdgen Searchđể khám phá sâu hơn về lịch sử token, các trường hợp sử dụng, xu hướng thị trường và sự sôi động trên mạng xã hội.

Bước 2: Chọn một sàn giao dịch đáng tin cậy

Chọn DEX uy tín (Uniswap,Pancakeswaphoặc CEX (Binance, Coinbase, Kraken) sau khi kết nối liền mạch đếnEdgen RadarHãy dịch đoạn văn tiếng Anh sau sang tiếng Việt. Giữ nguyên cấu trúc và thuật ngữ kỹ thuật chính xác. Tránh dịch quá mức.

Bước 3: Mua Tiền mã hóa của bạn

Nộp tiền vào, đổi token của bạn và lưu trữ chúng một cách an toàn.

Bước 4: Giám sát thị trường bằng trí tuệ nhân tạo

Sử dụng đòn bẩyEdgen Radarđể tín hiệu thị trường thời gian thực, theo dõi cả các hoạt động trên chuỗi và xu hướng xã hội.

Bước 5: Quản lý rủi ro một cách khôn ngoan

Đầu tư có trách nhiệm. Cả hai loại tiền tệ vàtiền xu memelà có nguy cơ cao,thưởng caocác trò chơi. Đừng YOLO toàn bộ số tiền tiết kiệm của bạn.

Rủi ro và Thực tế: Điều mà Mọi Nhà giao dịch Nên Biết

Thú vị không? Chắc chắn rồi. Không rủi ro không? Chắc chắn là không. Đây là những điều cần lưu ý:

1. Biến động cực đoan

Thị trường tiền mã hóa không thể dự đoán được, và ngay cả trí tuệ nhân tạo cũng không thể bắt kịp mọi tình huống bất ngờ.

2. Lừa đảo và Rút Thẻ (Rug Pulls)

Luôn kiểm tra các dự án trước khi đầu tư. Sử dụng Edgen Searchloại bỏ gian lận.

3. Trí tuệ nhân tạo không phải là phép thuật

AI dựa vào dữ liệu lịch sử, điều này không luôn luôn dự đoán chính xác 100% các xu hướng trong tương lai.

4. Rủi ro về quy định

Các hành động của chính phủ có thể thay đổi nhanh chóng bức tranh thị trường tiền mã hóa chỉ trong một đêm.

Các Câu Hỏi Thường Gặp: Những Câu Hỏi Thường Được Người Mới Hỏi Nhất

1.Giao dịch token với AI có phải là một khoản đầu tư tốt không?

Có thể, điều đó mang lại những cái nhìn dựa trên dữ liệu và thực hiện giao dịch nhanh nhưng vẫn tiềm ẩn rủi ro thị trường. Luôn nghiên cứu kỹ lưỡng.

2.Các bot giao dịch AI hoạt động như thế nào?

Các bot phân tích dữ liệu thị trường và xã hội thời gian thực, sau đó tự động hóa các giao dịch ngay lập tức. Các nền tảng nhưEdgen Radartheo dõi ví thông minh và xu hướng thị trường, giúp bạn luôn đi trước.

3.Bạn là aimemecoinrủi ro?

Tiền mã hóa Memecoinsrất biến động và mạo hiểm. Giá cả bị chi phối bởi cộng đồng và sự hào hứng thay vì các yếu tố cơ bản vững chắc. Cảnh giác với các kế hoạch bơm và rút vốn cũng như lừa đảo.

4.AI có thể dự đoán chính xác giá tiền mã hóa không?

AI cải thiện đáng kể các dự đoán, nhưng tiền mã hóa vẫn còn bất ngờ. Tuy nhiên, các yếu tố bên ngoài (quy định, tin tức, sự kiện lớn) vẫn có thể làm bất ngờ thị trường.

5.Người mới bắt đầu nên đầu tư như thế nào?

Sử dụng Edgen Search, chọn một sàn giao dịch tốt, đầu tư an toàn và theo dõi hành trình của bạn qua Edgen FeedHãy dịch đoạn văn tiếng Anh sau sang tiếng Việt. Giữ nguyên cấu trúc và thuật ngữ kỹ thuật chính xác. Tránh dịch quá mức.

Lời kết luận: AI +MemecoinCách mạng Thương mại

Tương lai của giao dịch tiền mã hóa kết hợp trí tuệ nhân tạo và sự lan tỏa do cộng đồng thúc đẩy. Trí tuệ nhân tạo giúp các nhà giao dịch vượt qua sự phức tạp, trong khitiền xu memecung cấp các khoản đầu tư văn hóa hấp dẫn, dù có rủi ro.

Các nền tảng nhưEdgen AIdẫn dắt cuộc cách mạng này, kết hợp các thông tin trực tiếp trên chuỗi khối với phân tích xã hội. Đó là về việc nhìn rõ hiện tại một cách thông minh và nhanh hơn mọi người khác.

Sẵn sàng đón nhận các loại tiền tệ được hỗ trợ bởi AI vàtiền xu memeBắt đầu nhỏ, giao dịch thông minh, giữ cho mình cập nhật và hãy đểEdgen AIgiúp bạn thống trị thị trường tiền mã hóa năng động.

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Ed miễn phí. Không cần thẻ, không ràng buộc.