Thử thách Edgen × Kaito 360°: Vượt trội hơn thị trường!

[Cập nhật] Do những thay đổi gần đây đối với bảng xếp hạng công khai của Kaito và các chính sách nền tảng của X, bảng xếp hạng của Kaito đã ngừng hoạt động. Điều này không ảnh hưởng đến Edgen: Aura và Bảng xếp hạng Edgen vẫn hoạt động đầy đủ và độc lập, với các nhiệm vụ sắp tới tập trung vào việc giúp bạn quản lý danh mục đầu tư tốt hơn và đưa ra các quyết định đầu tư sáng suốt hơn.

Ai cũng có ý kiến đặc biệt, nhưng không phải ai cũng có được cái nhìn sâu sắc.

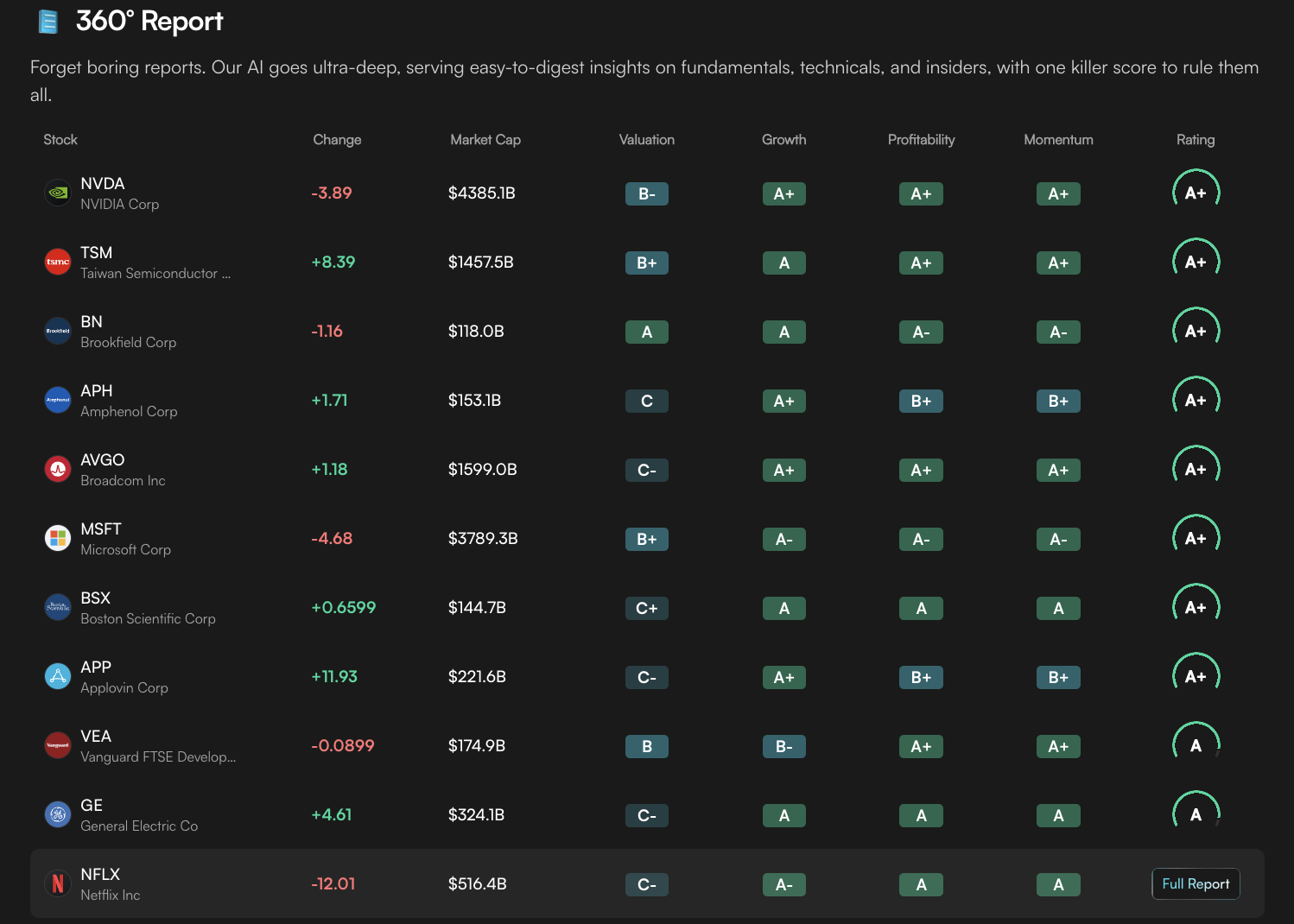

Edgen cung cấp những hiểu biết sâu sắc đó bằng cách hợp nhất cổ phiếu và tiền mã hóa vào một màn hình với Báo cáo 360° và trang Dự báo của chúng tôi.

Kaito mang đến những tiếng nói: nó theo dõi và xếp hạng các đóng góp của cộng đồng trong thời gian thực để những bài đăng sâu sắc được nổi bật.

Cùng nhau, chúng tôi sẽ phát động một thử thách kéo dài một tuần để tôn vinh những phân tích hấp dẫn nhất.

AI Phán xét, Tiếng nói Con người: Tại sao Insight 360° của bạn lại Quan trọng

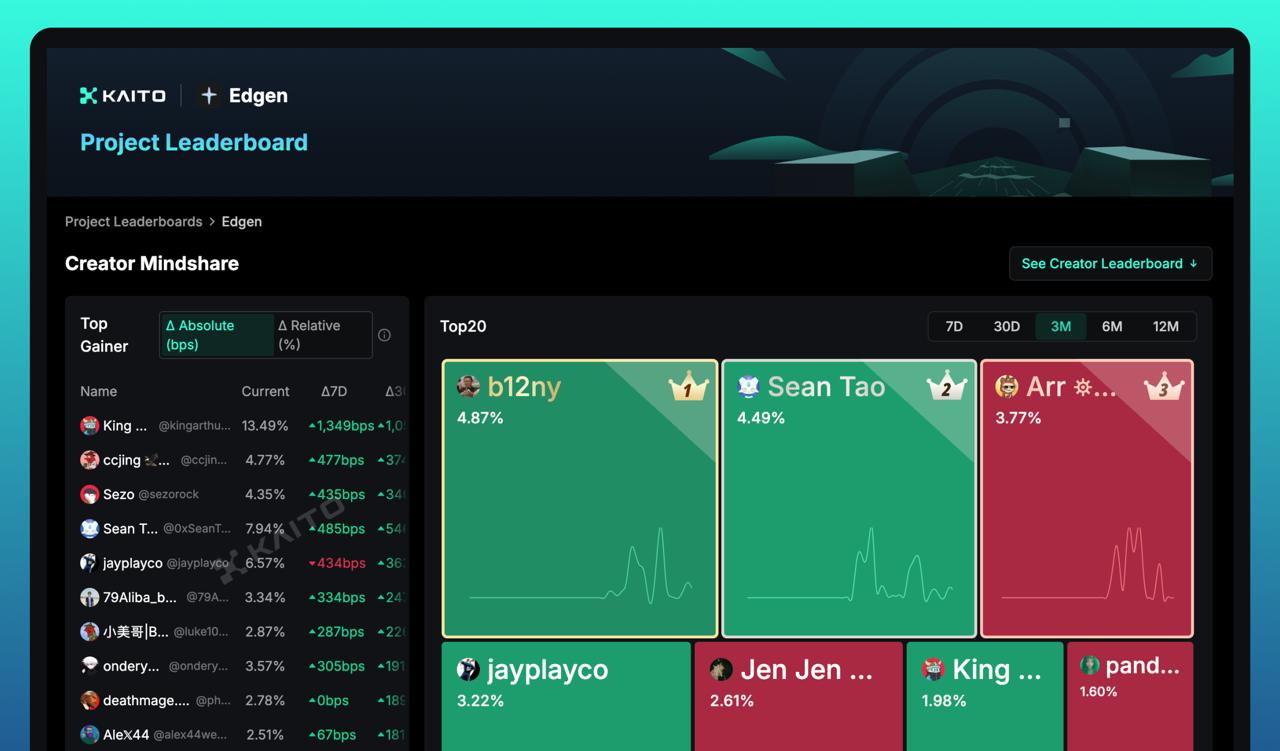

Bảng xếp hạng Yapper của Kaito là một bảng điều khiển công khai theo dõi và xếp hạng các đóng góp cho bất kỳ thương hiệu hoặc chủ đề nào. Nó khuyến khích sự tham gia, tạo cơ hội công bằng cho mọi người và biến việc tương tác cộng đồng thành một trải nghiệm thú vị. Mọi người sử dụng bảng xếp hạng này để tôn vinh những người tạo nội dung chất lượng cao và thưởng cho những đóng góp dựa trên giá trị.

Cách tiếp cận đó phù hợp với sứ mệnh của Edgen. Báo cáo 360° của chúng tôi giúp mọi người tìm hiểu cực kỳ sâu về các yếu tố cơ bản, kỹ thuật và động lực, sau đó cô đọng mọi thứ thành một điểm số duy nhất cho từng tài sản, dù đó là Bitcoin, Solana hay một cổ phiếu blue-chip.

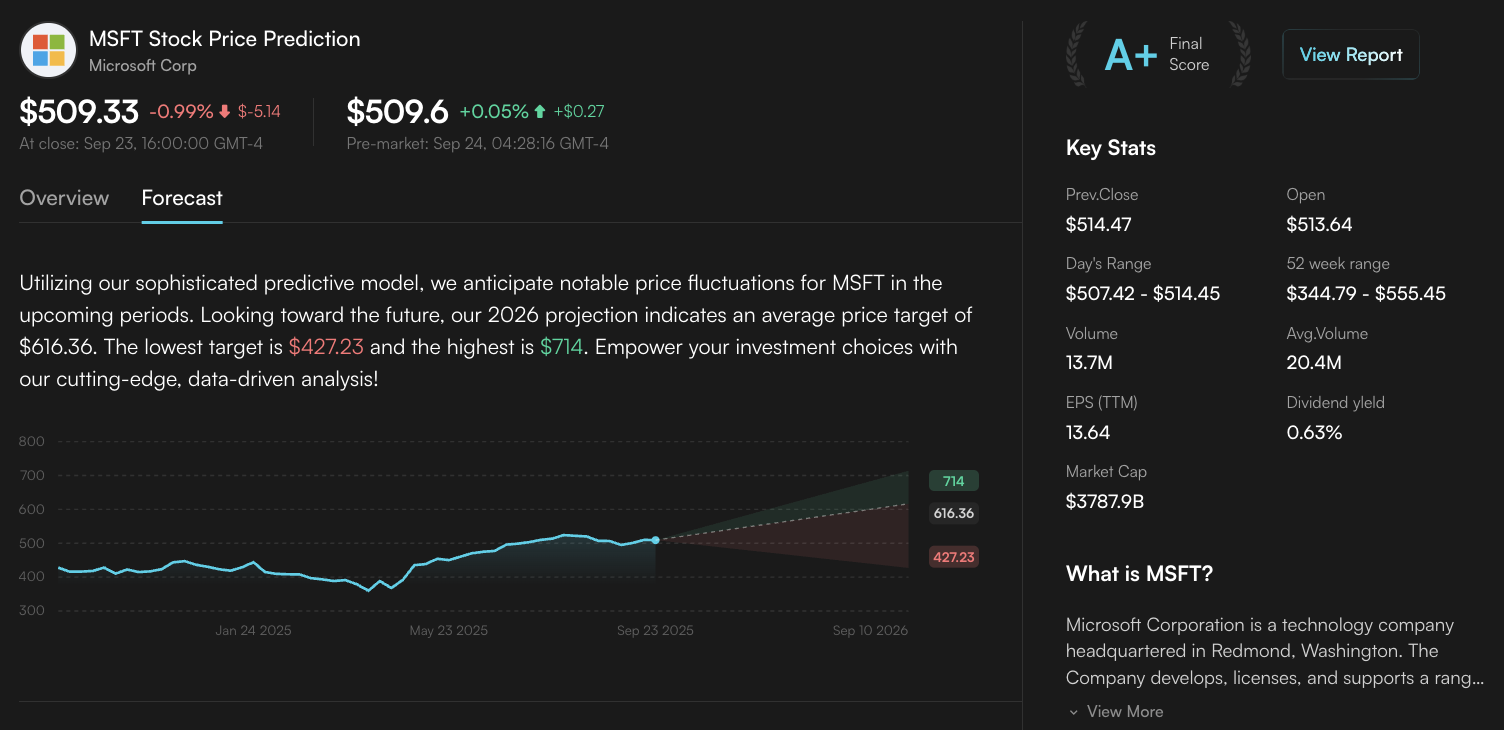

Trang Dự báo của chúng tôi áp dụng các mô hình dự đoán để dự phóng các phạm vi giá tương lai và giúp mọi người đưa ra các nhận định về thị trường, cung cấp mức mục tiêu trung bình, thấp và cao. Khi bạn kết hợp dữ liệu của Edgen với xếp hạng AI của Kaito, phân tích của bạn sẽ được hiển thị và đánh giá cao hơn.

Bước vào Đấu trường: Thể hiện Góc nhìn 360° của bạn

⏰ Thời gian: Từ ngày 24 tháng 9 năm 2025 đến ngày 30 tháng 9 năm 2025 (chiến dịch kết thúc lúc 15:59:59 UTC)

🎯 Chủ đề: Chọn một tài sản bạn quan tâm và mở Báo cáo 360° hoặc trang Dự báo của nó. Sử dụng tài liệu một trang đó để đưa ra ý kiến của riêng bạn trên X: làm nổi bật những điểm nổi bật, kết nối các số liệu hoặc chỉ ra một chất xúc tác bạn thấy trước mắt. Tiền mã hóa hay cổ phiếu, đó là lựa chọn của bạn!

📌 Cách thực hiện:

- Đăng bài phân tích của bạn trong Cộng đồng Edgen X và đảm bảo những người theo dõi của bạn cũng thấy nó

- Gắn thẻ @EdgenTech để đảm bảo bài đăng của bạn được tính

- Điền vào mẫu đăng ký tham gia để có cơ hội giành một chỗ tại bàn Chuyên gia

Chất lượng là quan trọng nhất. Bảng xếp hạng thưởng cho tính độc đáo và phân tích sâu sắc hơn là số lượng.

Đưa ra quan điểm của riêng bạn, liên kết các hiểu biết sâu sắc trên các thị trường và giải thích ý nghĩa của dữ liệu đối với bạn.

Chỗ ngồi tại Bàn Chuyên gia

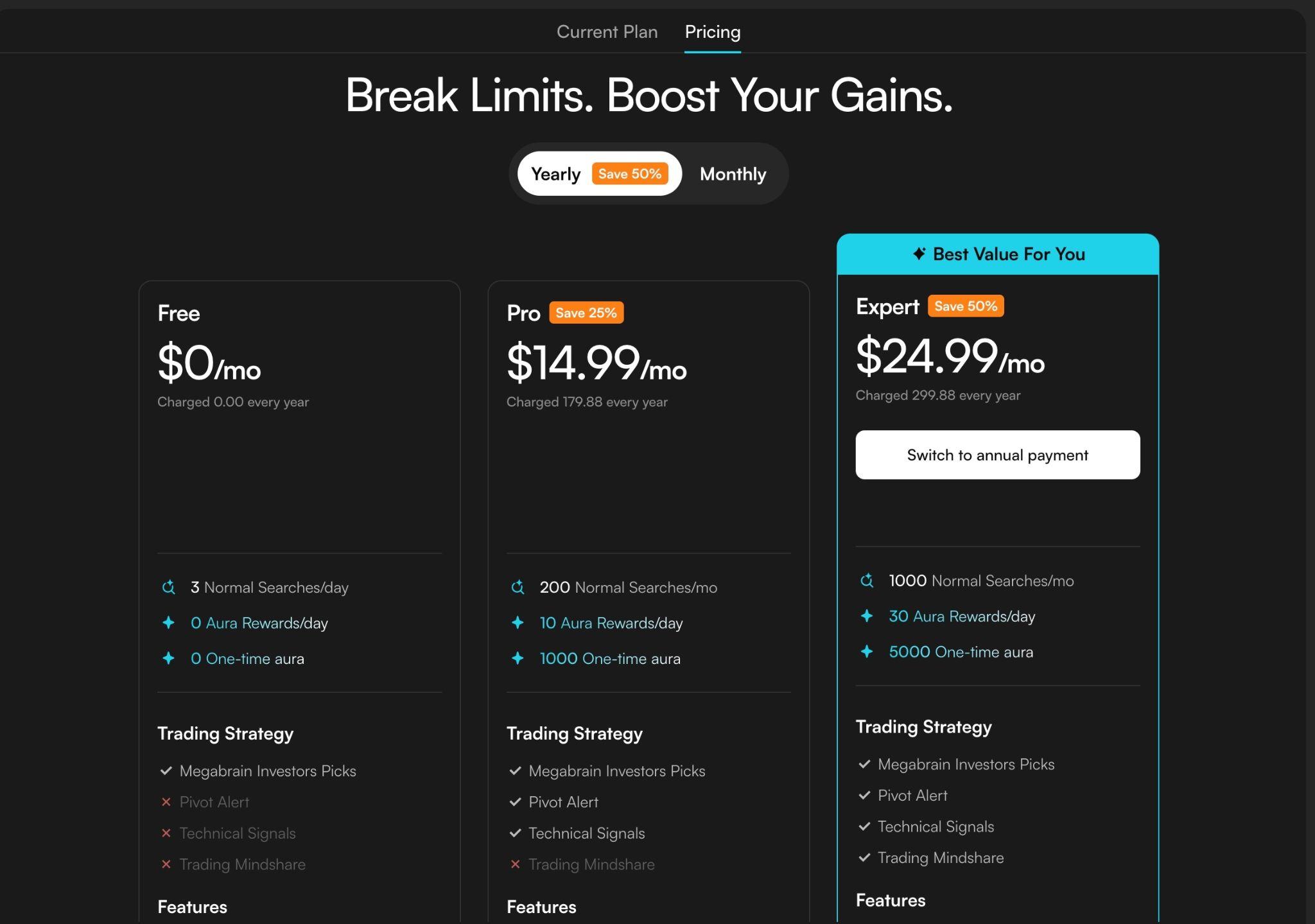

Vào cuối tuần đó, chúng tôi sẽ chọn ba người đóng góp nổi bật để tham gia Gói Chuyên gia Edgen Hàng năm. Thành viên chuyên gia được truy cập sớm các tính năng mới, xử lý Aura nhanh hơn, phân tích sâu hơn và quyền truy cập vào các tác nhân nâng cao. Đây là nút tăng tốc cho hành trình đầu tư của bạn.

Vươn lên bảng xếp hạng

- Luôn độc đáo: Bảng xếp hạng Yapper làm nổi bật những người tạo ra các góc nhìn độc đáo.

- Toàn diện: Báo cáo 360° bao gồm các yếu tố cơ bản, tokenomics, động lượng và tâm lý. Hãy cho thấy chúng liên kết với nhau như thế nào.

- Suy nghĩ tiến bộ: Sử dụng các phạm vi giá của trang Dự báo làm bàn đạp cho luận điểm của riêng bạn. Bạn có đồng ý với dự đoán này không? Tại sao có hoặc tại sao không?

- Tham gia và nâng cao: Bình luận về các bài đăng khác, đặt câu hỏi và giúp phát triển cuộc trò chuyện. Bảng xếp hạng phát triển nhờ sự tương tác.

Đến lượt bạn: Tham gia cuộc trò chuyện

Thử thách này là cơ hội để bạn thể hiện cách tư duy của mình, mài giũa sự hiểu biết về thị trường và được công nhận vì điều đó. Tiếng nói của bạn có thể giúp bạn giành được Gói Chuyên gia Hàng năm và trở thành điều đầu tiên mà các nhà giao dịch kiểm tra mỗi ngày.

Hãy đến Cộng đồng Edgen X, chọn một Báo cáo 360° hoặc trang Dự báo, chia sẻ quan điểm của bạn, gắn thẻ @EdgenTech và tham gia niềm vui thông qua biểu mẫu. Chúng tôi rất mong chờ những gì bạn sẽ mang đến.

LFG Ledgens!

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Ed miễn phí. Không cần thẻ, không ràng buộc.