Edgen AI : Votre copilote pour un trading de cryptomonnaies plus intelligent

Edgen AI : Votre copilote pour un trading de cryptomonnaies plus intelligent

Titre SEO : Naviguez sur les marchés crypto avec Edgen AI Copilot

Description : Découvrez comment Edgen AI vous sert de copilote intelligent, fournissant des données en temps réel, des signaux de trading et des informations sur le portefeuille pour un investissement crypto en toute confiance.

Mots-clés : Edgen AI, trading crypto, données de marché, signaux de trading, aperçus de portefeuille, copilote d'investissement IA, analyse prédictive, intelligence on-chain, plateforme d'intelligence de marché

I. L'essor des compagnons IA dans l'investissement crypto

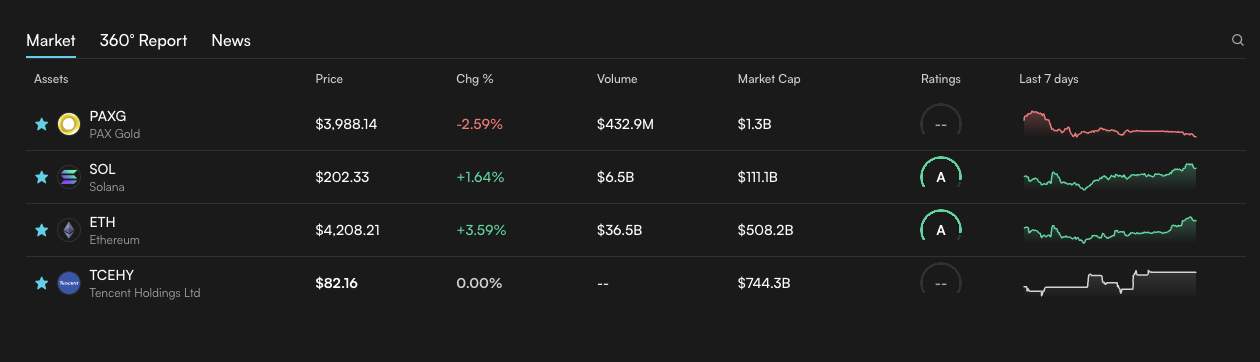

Les marchés crypto ne s'arrêtent jamais. Les prix réagissent en quelques secondes, les récits changent en quelques minutes, et les traders sont confrontés à un déluge de données provenant des exchanges, des blockchains et des réseaux sociaux. Le véritable défi est de savoir quelles informations méritent attention.

Edgen a été conçu pour relever ce défi. Il fonctionne comme un compagnon intelligent qui transforme les données éparses en une compréhension exploitable. Grâce à l'analyse en temps réel, à la modélisation prédictive et aux informations personnalisées, il permet aux investisseurs d'agir avec clarté plutôt qu'avec émotion.

Que vous gériez un portefeuille DeFi ou que vous tradiez des paires majeures, Edgen apporte de la structure à un marché qui est rarement immobile.

II. Comment Edgen AI soutient chaque décision

Edgen combine plusieurs couches d'intelligence en un système adaptatif qui apprend des mouvements du marché et du comportement des utilisateurs. Il interprète l'activité on-chain, les signaux techniques et le sentiment en temps réel pour guider les décisions sur chaque type de portefeuille.

Fonctionnalité clé | Description de la fonctionnalité | Comment cela aide les traders |

|---|---|---|

Données de marché en temps réel | Collecte des données on-chain, d'échange et de sentiment provenant de plusieurs réseaux. | Fournit des informations instantanées et des réactions plus rapides. |

Signaux de trading | Analyse les modèles historiques, le RSI, le MACD et les relations de volatilité. | Met en évidence les zones d'entrée et de sortie favorables. |

Informations sur le portefeuille | Suit la diversification, l'allocation et la concentration des risques. | Améliore l'équilibre et la résilience du portefeuille. |

Alertes prédictives | Détecte les anomalies et les retournements potentiels précocement. | Réduit l'exposition aux fortes corrections. |

Ces capacités sont alimentées par l'agent de signaux techniques d'Edgen, qui recalibre continuellement ses modèles à mesure que de nouvelles données arrivent, maintenant la précision sur des marchés volatils.

III. Du bruit à la clarté

Les marchés fonctionnent en permanence. Pour les investisseurs, le volume d'informations brutes est à la fois une opportunité et un obstacle. Edgen filtre et structure ces informations via un moteur de données unifié qui scanne des centaines de plateformes centralisées et décentralisées.

Ses modèles d'apprentissage automatique prévoient les mouvements à court et moyen terme en étudiant les flux de liquidité, l'activité du réseau et les interactions de sentiment. Ce processus convertit les données complexes de la blockchain et des exchanges en visuels lisibles qui révèlent les premiers signaux avant que les récits ne se mettent en place.

IV. Supervision de portefeuille avec la précision de l'IA

Chaque portefeuille a son propre rythme de risque et de récompense. Le rapport 360° d'Edgen offre une vue complète des avoirs, de la santé des actifs et des niveaux de concentration.

Les utilisateurs peuvent :

- Surveiller l'exposition du portefeuille en temps réel.

- Comparer les performances par rapport aux repères sectoriels ou de marché.

- Recevoir des suggestions guidées par l'IA pour le rééquilibrage et la diversification.

Grâce à ces informations, les investisseurs passent de la réaction à la préparation, ce qui permet un positionnement à long terme au lieu de suppositions à court terme.

V. L'avantage stratégique

La conception d'Edgen simplifie la complexité tout en approfondissant le contexte. Les investisseurs bénéficient :

- D'une interface unifiée qui centralise l'intelligence de marché.

- De cadres de décision plus intelligents basés sur des analyses vérifiées.

- D'une veille prédictive des changements de liquidité et de sentiment.

- De diagnostics continus du portefeuille pour la résilience et l'optimisation.

- D'une perspective communautaire de Trading Mindshare, intégrant les signaux sociaux et comportementaux.

Chaque composant fonctionne de concert pour aligner l'analyse, l'exécution et l'adaptation selon un rythme cohérent.

VI. L'avenir de l'investissement intelligent

Les marchés crypto seront toujours volatils, mais l'expérience de leur navigation peut être calme et méthodique. Edgen AI apporte cette discipline grâce à l'apprentissage adaptatif et à la prévision précise.

Il offre un environnement complet pour comprendre ce qui fait bouger les marchés et comment chaque mouvement affecte votre portefeuille.

Avec Edgen comme copilote, vous investissez avec conscience, structure et objectif.

Commencez à explorer Edgen aujourd'hui et découvrez comment l'IA transforme l'information en confiance.

Investir, enfin, tu n'es plus seul.

Essaie Ed gratuitement. Sans carte, sans engagement.