我跟不上這個荒謬的市場了,所以我創辦了Edgen。

我不是專業寫作者。誠實說,我甚至不確定自己是否應該寫這段話。但我想要親自告訴你我們為什麼要打造Edgen,因為這對我個人來說意義重大。

我進入加密貨幣大概也是出於和你相同的原因did:我想要自由,我想有機會成功,而且,我誠實地告訴你,我想賺一些錢。這沒什麼不對的。

我一直在交易加密貨幣,但一年份現在,我並不陌生於這個領域,並在其中度過了不少樂趣。我一直在Everest Ventures Group (EVG)工作,支持並打造了有前景的DeFi與SocialFi亞洲的專案,經歷過牛皮市場與熊市,並建立了一個我認為是專業的網絡還算可以根據大多數標準,我會說我屬於相當有關係的在這空間裡,我不能說謊。

但最近,連我也開始感到壓力很大。多年來,我學到加密貨幣交易比看起來要困難得多,即使是在牛市場(牛市)中也一樣。實際上「小丑」加密貨幣市場。如果你曾經有過這種煩人的經驗,在凌晨3點查看你的投資組合,結果發現自己是對的,但卻又進場太晚(再次),你就完全明白我在說什麼了。

加密貨幣現在的流動速度比以往任何時候都更快。快得過頭了。遠遠地太快了。每天都有數以百計的token出現。迷因幣那些每小時放大100倍的資訊、過夜改變的敘事、我從未聽過的鯨魚錢包中的隱藏訊號……噪音從不停止。無論你多有經驗,或你的研究與人脈多麼優秀,跟上這一切根本是不可能的。

我錯過了好的交易機會,錯失了機會,總是發現自己在努力趕上。即使擁有我的資源和人脈,試圖保持領先確實令人感到非常疲憊。而我並不認為自己是一個特別差的交易員。

現在我已經結婚並有孩子了。我覺得自己又老又累。而如果像我這樣擁有廣泛人脈和多年經驗的人,都會感到如此不堪重負,那麼普通的、更謙遜的首次交易者就更不用說了。必須有時會更明顯,甚至帶來戲劇性的後果。

加密貨幣原本被視為通往成功的金鑰,並讓所有人站在同一起跑線上。它本質上是關於給予每個人都公平的機會,無論你是誰或你最初擁有多少錢。但我們現在所處的現實呢?一點也不公平,感覺像是被操縱的。這就是我決定我們必須打造一些東西來改變這種狀況的原因。

我為一般用戶(因為我)建立Edgen,有點是其中之一

Edgen 是我本身極度需要的東西,以免變得瘋狂。我想要一個能立即從加密貨幣的每個角落、Crypto Twitter、智能錢包、鏈上信號、開發者活動、近期風險投資等蒐集集體智慧的工具。募資,以及明確且迅速地傳給我。

一件能過濾掉無用的貼文和地毯,讓我及時看到真正重要的事情。

所以我們打造了一個具備人工智慧的市場洞察平台,簡單到任何人都能使用,卻又足夠聰明以應對複雜的需求。實際上有幫助我無法保證你每次交易都能賺錢,沒有人能做出這樣的承諾,任何這樣說的人都是在騙你。但我可以保證的是,你再也不會盲目交易了。

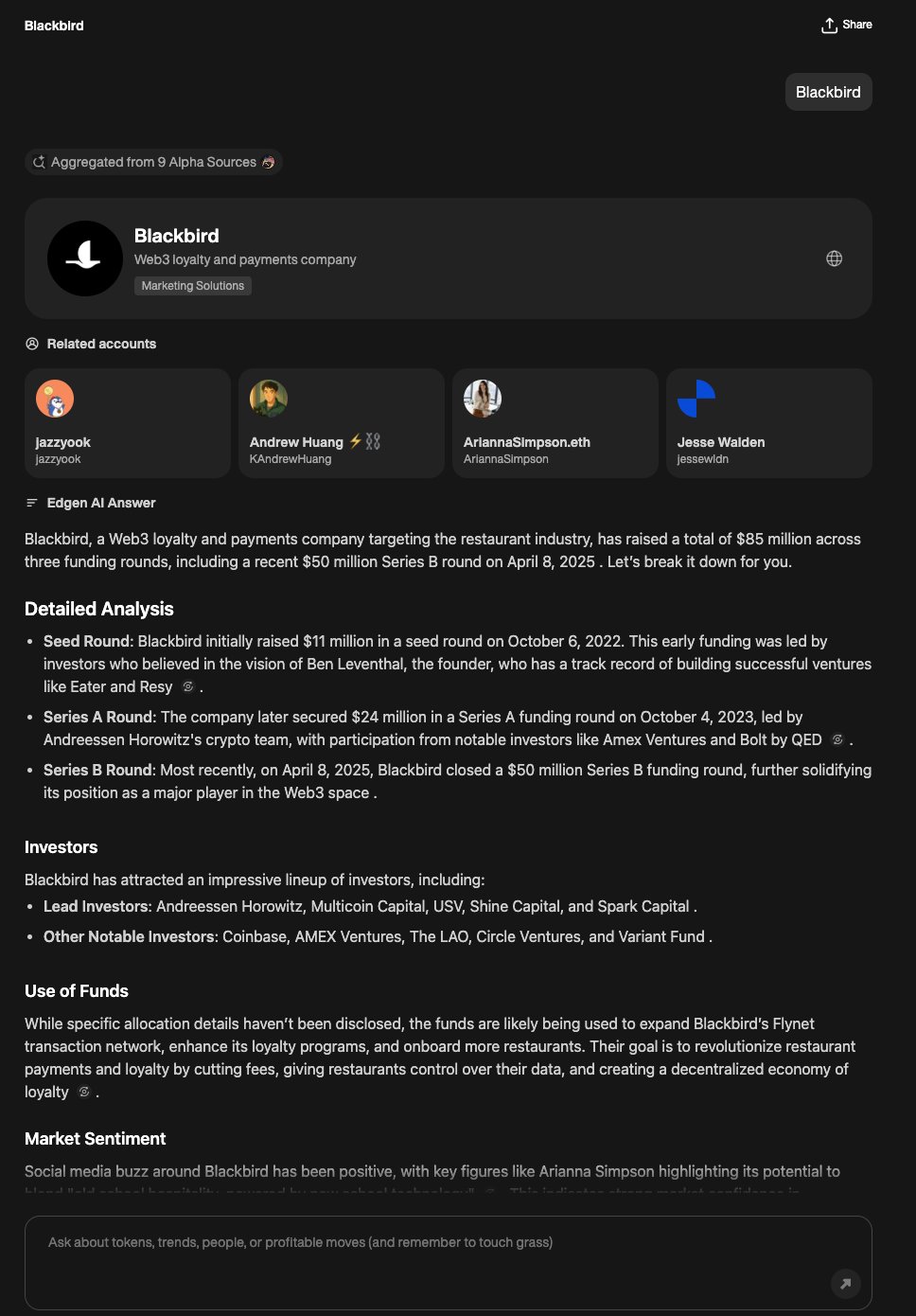

所以我們將從兩個簡單而強大的工具開始。感謝我們耗費無數小時累積和精煉的專屬社會與市場數據,Edgen 定製的 AI 在提供精準洞察方面無可比擬——無論您是在研究藍籌代幣,還是新興的項目,迷因幣具影響力的市場參與者,或最新的募資交易。

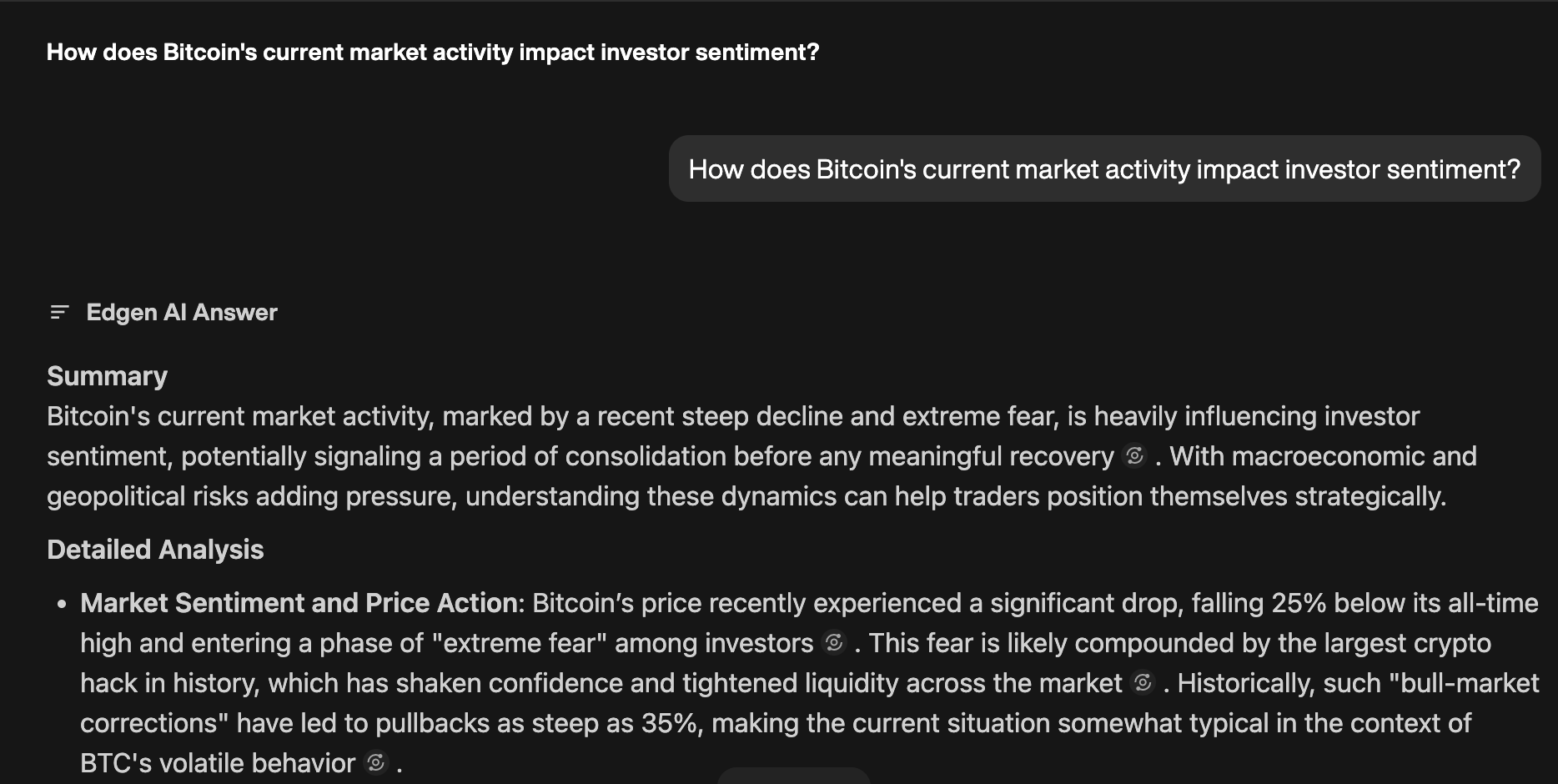

Edge搜尋:

提出任何您對加密貨幣的疑問,無論是複雜還是簡單,都能立即獲得來自即時數據的可操作見解。不再需要深夜不斷滑動瀏覽負面資訊。我們自訂訓練的大型語言模型能精準地過濾雜訊,迅速呈現整個加密貨幣領域中的訊號與機會。甚至擴展至股票市場。

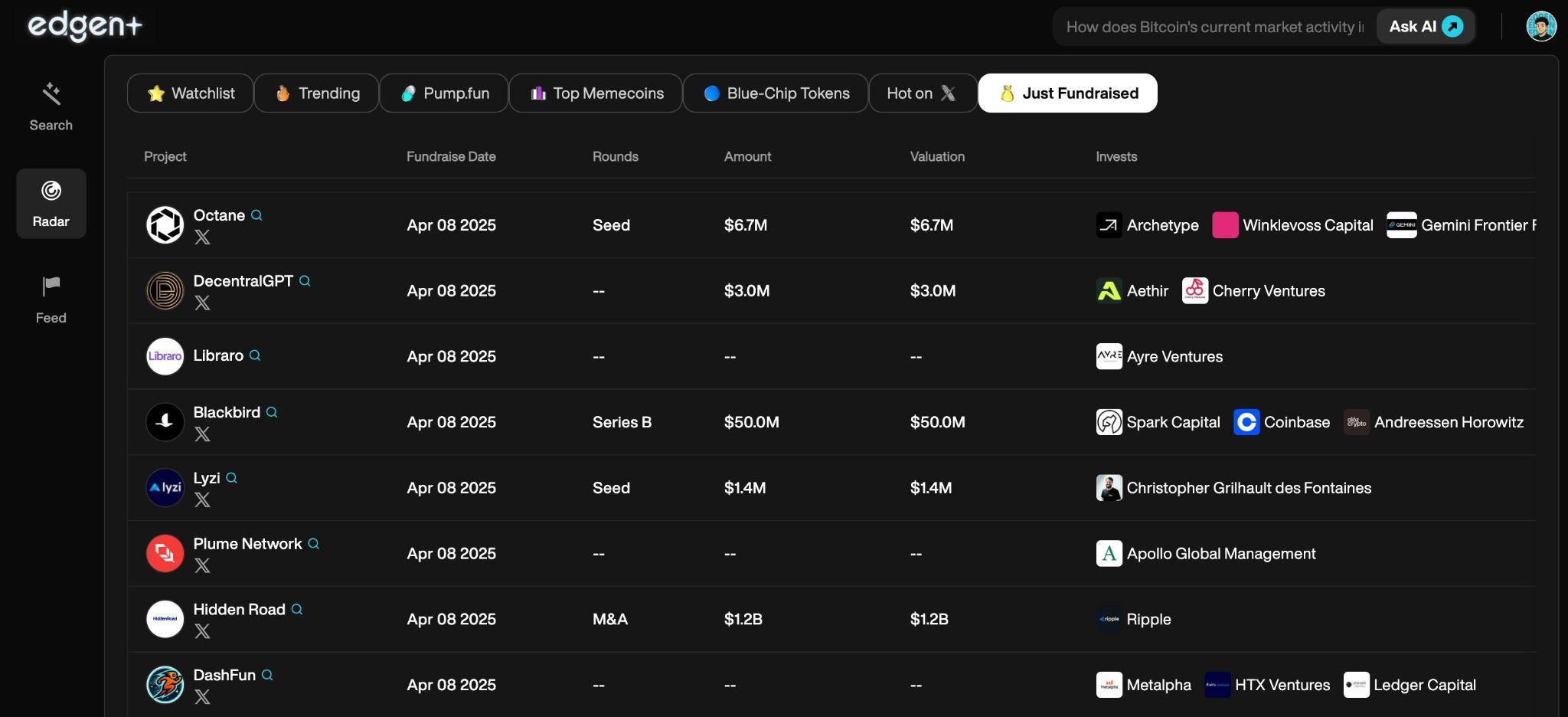

EdgeRadar:

雷達作為您的個人探測儀表板。它持續掃描各種代幣,包括主流代幣,pump.fun畢業生,月球目標代幣,熱門代幣,等等並在有有趣事件發生時通知您,例如智能錢包的買賣、社群熱潮,或關鍵影響者悄悄地透過追蹤代幣來轉移他們的關注。

繼續開始搜尋吧!問它你最愚蠢的加密貨幣問題,你得到的回應要麼是毫不客氣的誠實答案,要麼就是完全好笑的回覆 😂

我們即將推出更多工具,例如 Feed 和特別的 Aura,但這個故事要留到另一天再說。不過我現在可以稍微透露一下。

光環:辨識你真正可以信任的人

我在此阻止你:Aura 不是代幣。它是一個聲譽系統。但這幾乎是一樣的,因為在這個經濟體系中,聲譽就是貨幣。Aura 是你的證明優勢分數。

每次Edgen社群中的成員在Twitter上分享有價值的見解,例如準確的市場預測、發現新興趨勢或做出正確的預測時,他們都能獲得Aura,並訓練Edgen的AI逐漸變得更聰明。隨著時間的推移,Aura能精確顯示誰是值得信賴的,誰持續提供真正的Alpha(超額回報),以及誰是你應該關注的人。

換句話說,Edgen幫助你理解發生什麼事了,也能理解信任誰在這個嘈雜的市場中。

在我們之前累積的獨家且專有資料基礎上,使Edgen有別於其他大型語言模型,Aura將讓我們針對特定用途設計的大型語言模型日益變得更聰明,這種方式是其他地方無法複製的。

你們中的一些人可能從我開始的這段旅程中認識我。OpenSocial. Edgen 是實際上是 a從...的重大升級OpenSocial建立在相同的核心理念之上:為社會資本和影響力提供真正可衡量的價值與真實的所有權。透過 Edgen,我們將這項使命進一步推進,將社會洞察與集體智慧轉化為明確且可執行的市場優勢。這就是一切。OpenSocial旨在成為,而且遠遠不止。這是考慮到目前市場的自然演進。

Edgen 是市場的偉大平衡者

我建立Edgen的原因是,加密貨幣不應該只讓內部人士或那些總是線上的人受益。當然,並不是每個人都能一直賺錢,這並不現實。但只要能及時且清楚地獲得正確資訊,任何人都有公平的機會賺錢。

我的夢想是讓 Edgen 成為加密貨幣交易中的偉大平衡者。如果我們正確地完成自己的工作,來自世界各地、各種背景的普通交易者將不再需要一直覺得自己處於劣勢。

這就是我的故事。我並不是一位有華爾街背景的專業交易員,我……肯定沒有完美地寫出這句話。我只是一個熱愛它的男人。加密貨幣,以及想要更好的東西。

所以,這就是我建造 Edgen 的真正原因。我自己需要它。我相信它也能幫助你。

感謝您給這個機會。

蕭恩·陶,Edge共同創辦人

投資這事,終於不用一個人了

免費試用 Ed。不用信用卡,不綁約