如何使用 AI 透過 EdgeN Radar 識別有利可圖的加密貨幣交易機會

加密貨幣交易的未來:人工智慧如何改變遊戲規則

加密貨幣交易速度極快,傳統方法無法跟上節奏。

進入AI:你在市場中勝出的最佳夥伴。類似於Edgen Radar運用人工智慧快速識別有利可圖的加密貨幣交易機會,將鏈上數據、社群情緒與AI驅動的分析整合於一個流暢的介面中。

本文將引導您了解人工智慧如何革新加密貨幣交易策略,並特別說明如何 Edgen AI透過即時Alpha訊號、來自區塊鏈趨勢的可操作見解,以及對社群加密貨幣的精確分析,賦予交易者力量泵基礎知識。

1. 為什麼人工智慧對加密貨幣交易至關重要

加密貨幣從來不會睡眠:價格瞬息萬變,手動追蹤每一筆變動是不可能的。這就是為什麼運用AI是一場徹底的轉變。

AI如何提升你的交易決策:

- AI-based sentiment analysis for crypto:即時掃描加密貨幣推特(X)及新聞資訊,識別熱門代幣與社群動態情緒

- Real-Time On-Chain Monitoring:即時監控異常交易、流動性變動及智能錢包活動,於影響代幣價格前採取行動。

- Crypto Alpha Signal powered by Edgen AI:精準鎖定具有潛力動能的被低估資產,於他人注意之前提醒您進行交易。

Edgen 更進一步,獨特地結合加密貨幣分析、人工智慧與社群媒體洞察,確保沒有任何盲點。

2. 獨具威力的AI策略,用於獲利的加密貨幣交易

AI的強大之處在於其能夠快速篩選大量數據集,識別模式,並精確且即時地制定策略,遠超人類的能力。以下是AI如何大幅提升您的加密貨幣交易表現:

1. 情緒分析:利用市場熱潮

加密貨幣市場主要根據炒作和投機而波動。由人工智慧驅動的情緒分析透過分析來檢測多頭或空頭趨勢:

- 代幣提及跨平台如 Twitter (X)

- 參與指標例如來自智慧帳號的轉發、評論和關注。

- 意見領袖情緒來自關鍵意見領袖(KOLs)

Edgen Radar立即標記獲得社交關注的代幣,讓您及早布局以進行有利可圖的操作。

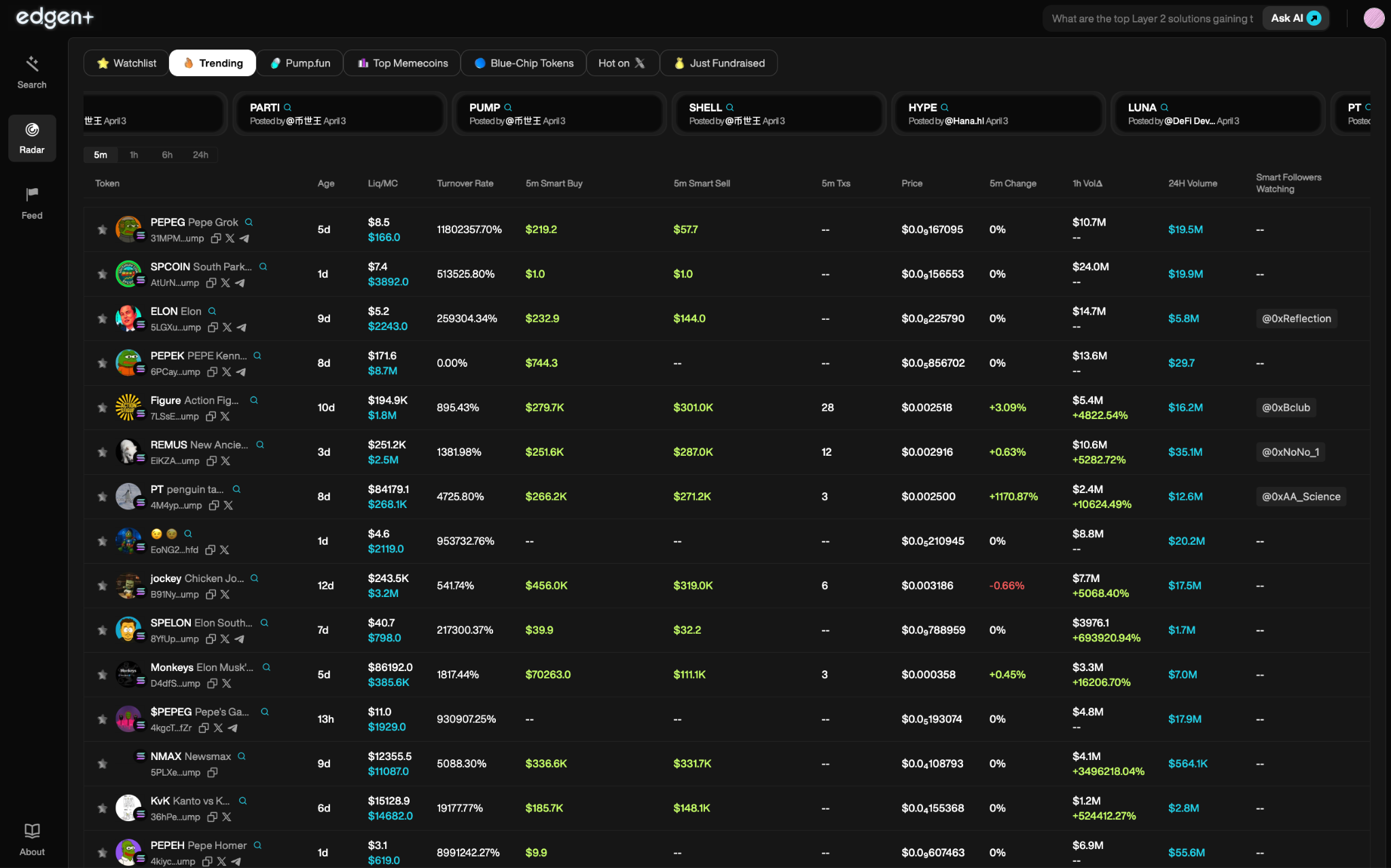

2. 區塊鏈資料洞察:閱讀智慧錢包活動

由 Edgen 提供的 AI 驅動鏈上分析,透過突出顯示關鍵市場變動,協助交易者做出決策:

- 鯨類活動:大型智能錢包的移動通常預示著價格的重大變動。

- 流動性流向:追蹤跨集中式交易所(CEXs)與去中心化交易所(DEXs)的代幣移動情況。

- 智慧錢包訊號:跟蹤去中心化金融(DeFi)協議中的活動、質押行為以及代幣實用指標。

Edgen的全面儀表板提供清晰即時的區塊鏈洞察,消除猜測的需要。

3. 技術與基本面分析:全面的AI驅動洞察

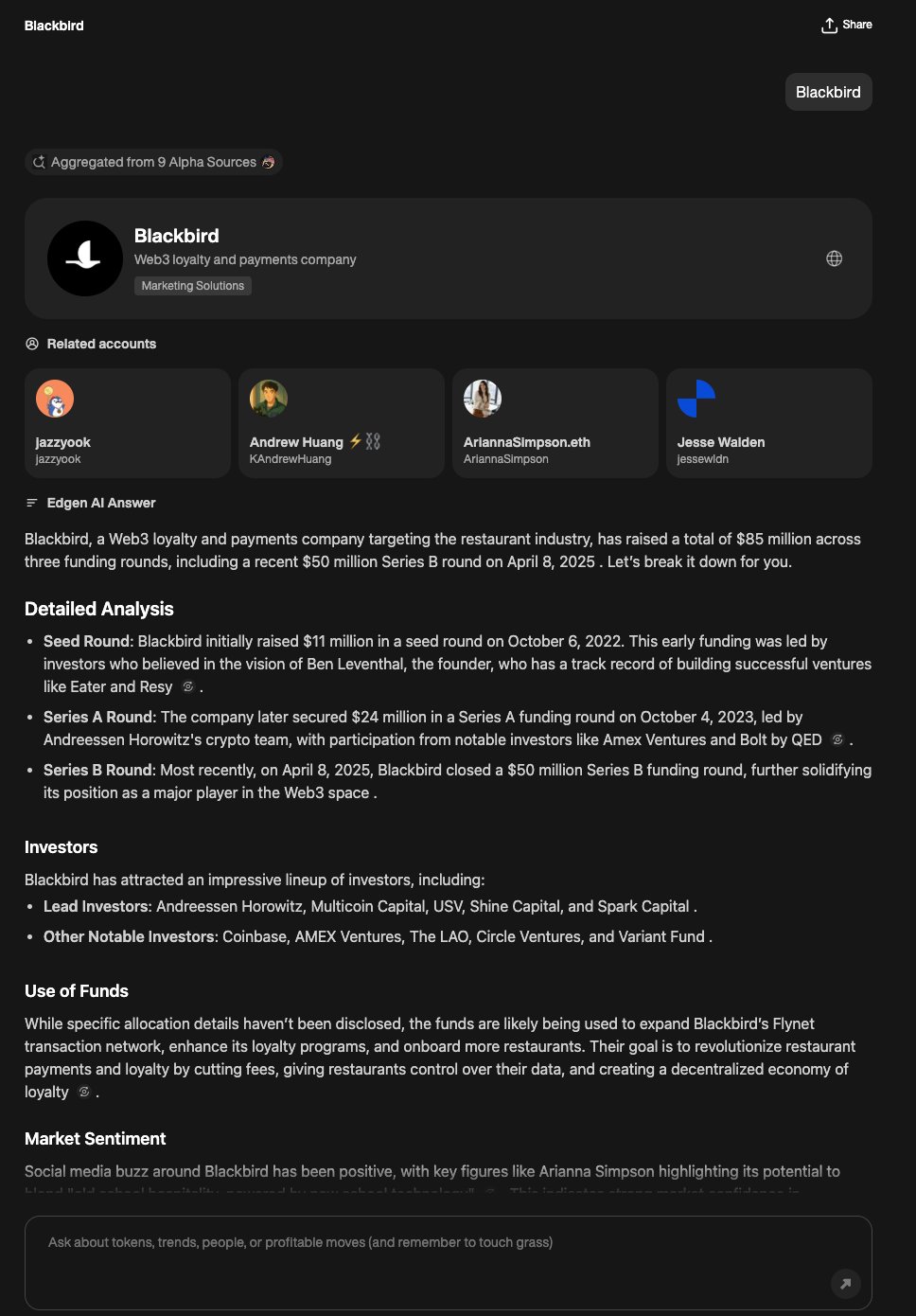

結合技術分析圖形、鏈上數據及社群情緒指標,Edgen AI 的智能演算法可自動識別高行動價值的交易機會。而非浪費時間手動整理混亂且碎片化的市場數據,交易者可以依靠 Edgen Search’s AI-powered crypto trading engine在數秒內提供快速、準確且有數據支持的洞察。該平台的LLM(大型語言模型)技術實現了直覺式的搜尋功能,讓使用者可以輸入問題,例如「哪些代幣正在獲得巨額投資者關注?」或「今天哪些DeFi代幣正在熱門趨勢中?」,並立即獲得即時且詳細的回應。這是一種更智慧的交易方式—專為速度、規模與精準度而設計。

3. 什麼是 Alpha Trading:AI 如何發現隱藏的機會

「Alpha」到底是指什麼?

Alpha 是指在市場基準指標尚未廣為人知之前,持續發現隱蔽的交易機會,從而超越市場基準。

如何識別Alpha訊號:

- 追蹤重要的智慧錢包與巨額帳戶動向。

- 強調低風險、高回報的交易設定。

- 將鏈上基本面與社群驅動的「泵基礎知識。

此外,Edgen引入獨特的「Aura」激勵系統,鼓勵用戶透過分享自己的見解來訓練Edgen的AI,獎勵積極的貢獻,並持續提升平台的預測精準度。

4. 開始使用 Edgen AI 進行加密貨幣交易

準備好透過AI加速你的加密貨幣交易了嗎?以下是開始的方法:

- 註冊:加入類似平台如Edgen Radar並取得AI驅動的市場洞察。

- 監控即時資料:從 Radar 直接追蹤不斷演變的鏈上趨勢和新興的社群情緒。

- 回測策略:使用AI驅動的歷史市場分析來模擬和優化您的策略。

- 風險管理:始終透過設定停損和分散投資組合來保持風險紀律。

記住,AI 只是強化你的策略,但不會取代紀律性的交易原則。AI 儀器強大,但需要智慧的人類監督。 Edgen透過整合持續的即時鏈上與社群監測,協助做出更安全、更智慧的交易決策。

重點是:AI 是加密貨幣交易的未來

在快速變化的加密貨幣世界中,AI 不僅有幫助——它是必需的。隨著 Edgen’s AI crypto tools您將獲得明顯的優勢:精確的alpha信號、即時資料,以及幫助您更聰明且超前於市場趨勢的社交智能。

如果你想深入了解區塊鏈的未來、加密貨幣生態系統,以及類似AI這樣的技術如何與金融創新交會,那麼這篇內容將會是你的最佳選擇。 MIT Digital Currency Initiative提供來自全球頂尖學術機構的尖端研究與領導見解。

準備好更聰明地交易,並更頻繁地獲勝嗎? Start using Edgen today請將以下英文翻譯成繁體中文。保持結構和技術術語準確。避免過度翻譯。

投資這事,終於不用一個人了

免費試用 Ed。不用信用卡,不綁約