De los fundamentos a las "Pumpamentals": Cómo el sentimiento social mueve ahora los mercados

El Mercado Se Desplazó de Números a Narrativas

Los mercados financieros han cambiado. Los informes de ganancias, los estados de situación financiera y los indicadores tradicionales ya no dominan los movimientos de precios. Las redes sociales son ahora Wall Street. Una publicación de un influencer poderoso, un meme viral, puede hacer subir el precio de una acción en minutos.

Los inversores tradicionales están acostumbrados a seguir estados de resultados, EBITDA y ratios de deuda. Los traders modernos siguen el sentimiento social, los movimientos de billeteras de blockchain y las narrativas de mercado virales.Edgen AI facilita a los operadores leer en tiempo real la sentimiento del mercado, capturando los cambios antes de que ocurran.

Fundamentos vs.PumpamentalsUna Nueva Realidad

¿Qué son los Fundamentos Financieros?

La inversión tradicional se enfoca en métricas de salud de la empresa:

- Rentabilidad

- Crecimiento de ingresos

- Estabilidad financiera

En resumen, los inversores analizan los informes trimestrales, los niveles de deuda y la calidad de la administración.

PumpamentalsEl auge de la especulación impulsada por la euforia

Luego llegaron las acciones de memes. GameStop (GME), AMC y activos similares subieron sin ganancias sólidas. Los precios subieron bruscamente debido al impulso de las redes sociales.

Comunidades en línea generaron olas masivas de compras, impulsadas por hype y sentimiento de la multitud. Este fenómeno (pumpamentals) es ahora una realidad del mercado, convirtiendo la atención en movimientos de precio.

El Rol Crucial de la IA enPumpamentals

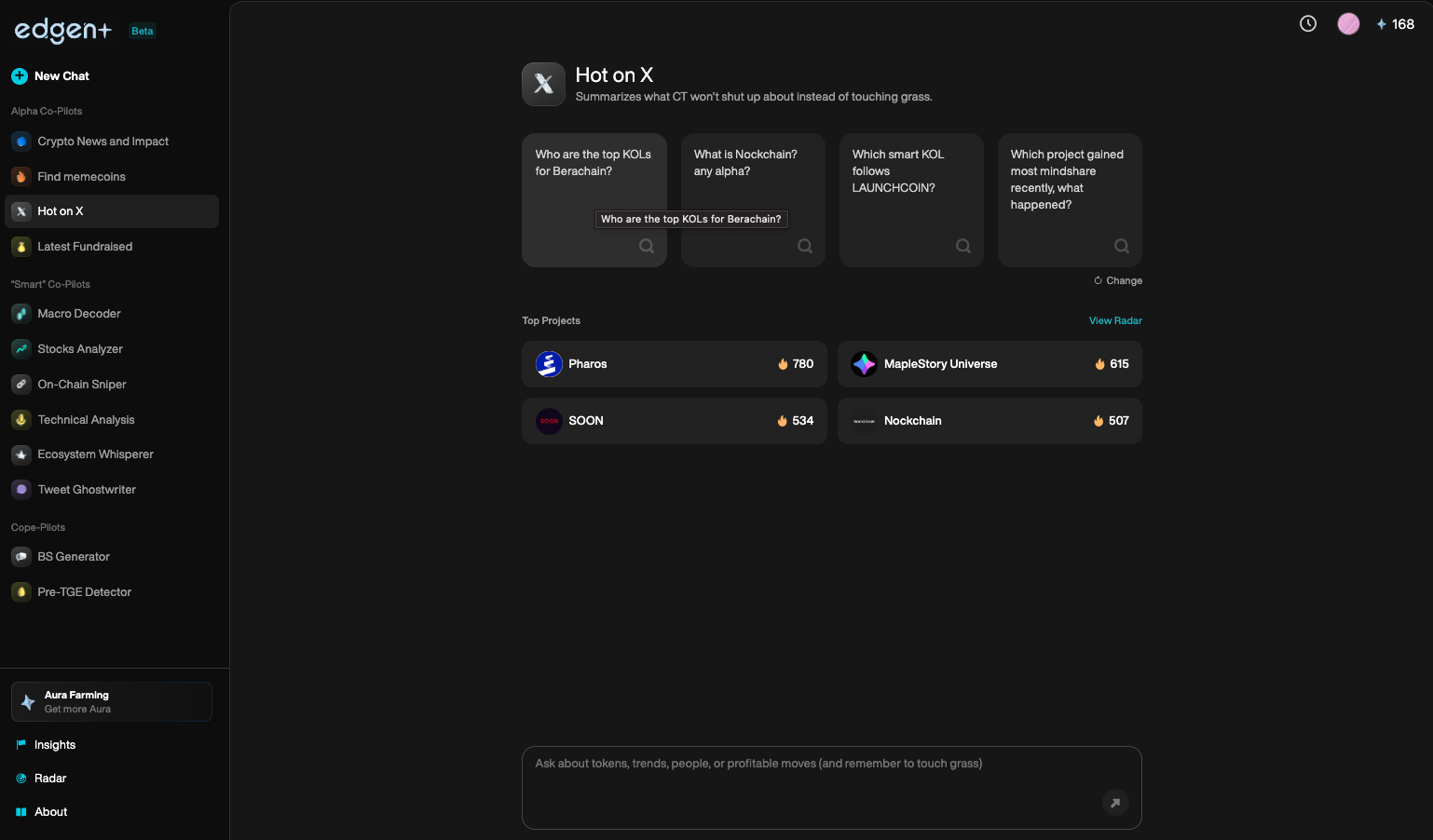

La IA se convirtió en esencial para el seguimiento y la predicción del sentimiento social. Edgen AI aprovecha:

- Tendencias de consenso de Twitter/X

- Actividad en tiempo real de billeteras de blockchain (alertas de ballenas, dinero inteligente)

- Narrativas de mercados emergentes sobre activos de memes

Negociar sin herramientas de IA significa perder señales de alpha.Edgen AIayuda a los comerciantes a anticipar cambios en el mercado con anticipación.

La Potencia del Sentimiento Social

Definición del Sentimiento Social

La sentimiento social refleja la entusiasmo o negatividad en línea hacia activos específicos. Los traders que observan Twitter, Reddit y foros en línea ven reacciones en los precios más rápidamente que a través de los medios tradicionales.

¿Por qué el Sentimiento Impulsa los Precios Ahora

- Información Inmediata: Las redes sociales transmiten señales de inmediato, más rápido que las noticias financieras tradicionales.

- Influencia del Retail: Los inversores individuales se organizan en línea, desafiando a la finanza tradicional.

- Innovaciones impulsadas por IA: Edgen AI monitorea los cambios en el sentimiento de inmediato, proporcionando señales tempranas cruciales.

Seguimiento de Sentiment con IA

El AI Edgen escanea continuamente las redes sociales y las transacciones de blockchain. Los traders obtienen una ventaja al:

- Identificar tendencias virales temprano

- Monitoreo de carteras influyentes (dinero inteligente y ballenas)

- Evaluar el impacto de líderes de opinión clave (KOLs)

El trading con IA es esencial para la inversión moderna.

Acciones de Meme y el Fenómeno de Inversión Viral

Acciones de Meme, definición

Las acciones de memes suben rápidamente debido a la euforia social en lugar de fundamentos. Los inversores minoristas se coordinan a través de comunidades como r/WallStreetBetscreando olas de compra explosivas.

La subida histórica de precios de GameStop

GameStop (GME) cotizó a niveles bajos hasta que las comunidades de Reddit se movilizaron.Masivo coordinadola compra desencadenó una cobertura corta, haciendo que las acciones subieran de $20 a $500 en días.

La lógica financiera tradicional no logró predecir esto. El impulso impulsado por la sociedad dominó.

Finanzas Conductuales: ¿Por qué los inversionistas siguen a la multitud

Impulsores Psicológicos Detrás dePumpamentals

La finanza conductual explica las decisiones del mercado impulsadas por emociones en lugar de lógica:Explore key behavioral biases and their impact on financial decisions.

- Miedo a Perderse algo (FOMO): Los inversores se apresuran a comprar activos que están en tendencia al alza.

- Comportamiento Memético: Las personas siguen la sentimiento popular, ignorando las advertencias tradicionales.

- sesgo de confirmación: Los inversores favorecen la información que se alinea con las creencias existentes, ignorando los riesgos.

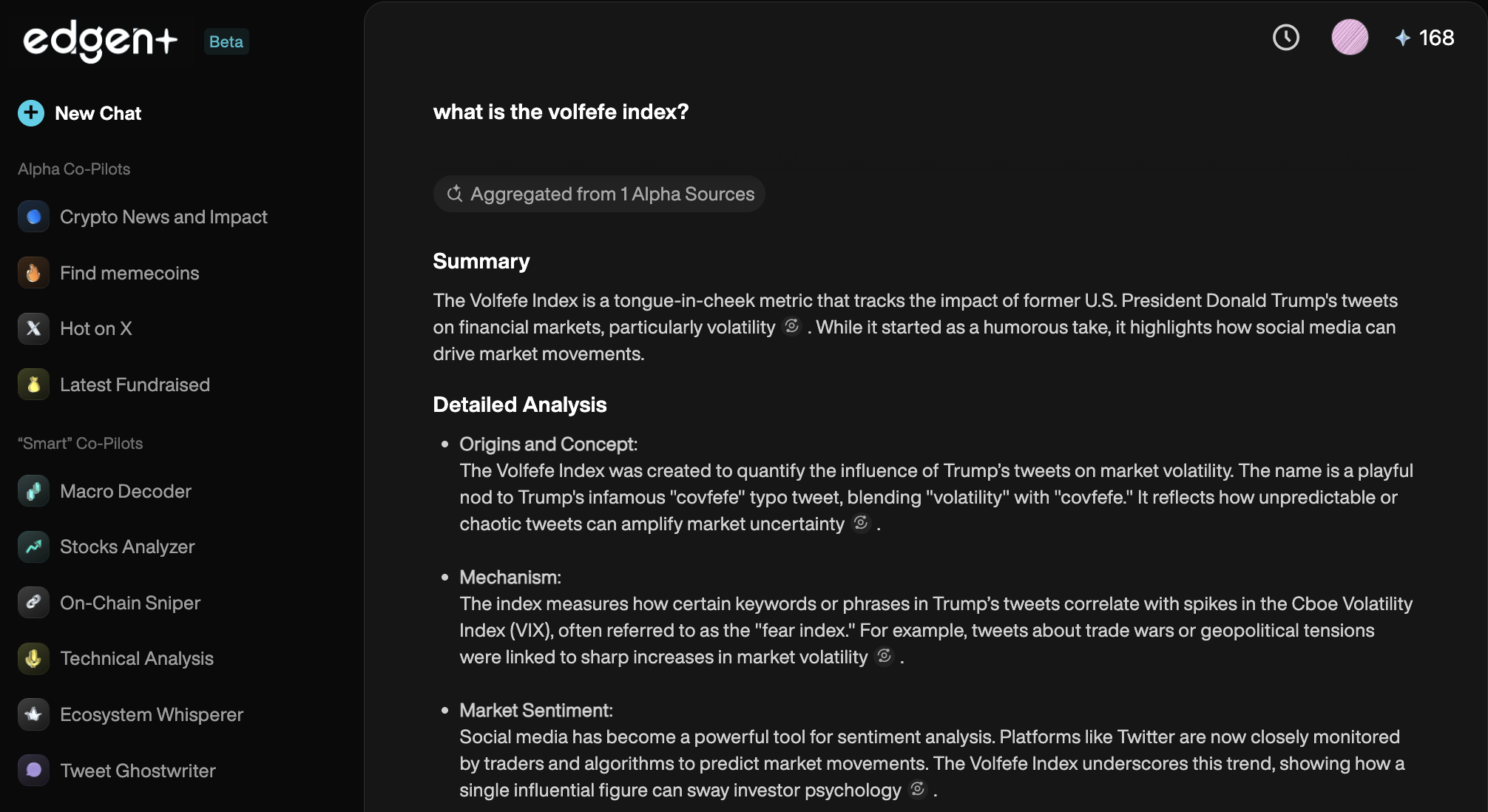

ElVolfefeÍndice: Medición de la Influencia Social

Los influencers como Elon Musk impactan significativamente en los precios de los activos. Los tweets de Musk solamente causaron oscilaciones drásticas en Dogecoin y Tesla. LaVolfefeEl índice rastrea el impacto en el mercado de las publicaciones sociales influyentes, subrayando la importancia de las analíticas sociales impulsadas por IA, como Edgen AI.

Datos Alternativos y Análisis de Sentimiento Mejorado con IA

Comprensión de los Datos Alternativos

La inversión tradicional utilizaba estados financieros y informes trimestrales. Ahora los traders aprovechan:

- Tendencias de las redes sociales

- Transacciones criptográficas en cadena

- Análisis de búsqueda de Google

- Datos de sentimiento del mercado impulsados por IA

Los datos alternativos revelan oportunidades en el mercado antes de que se reflejen en la acción del precio.

Edgen AI: Modelando el futuro del comercio

Cómo Edgen AI da a los traders la ventaja

El AI Edgen proporciona una infraestructura completa para negociación del lado comprador, rastreando simultáneamente:

- Movimientos de billetera inteligente (ballenas y figuras influyentes)

- Consenso social y narrativas virales (Twitter/X)

- Cambios de sentimiento impulsados por IA

Comercio hoy sinInsights impulsados por IAes como invertir con los ojos vendados.

Características principales de Edgen AI:

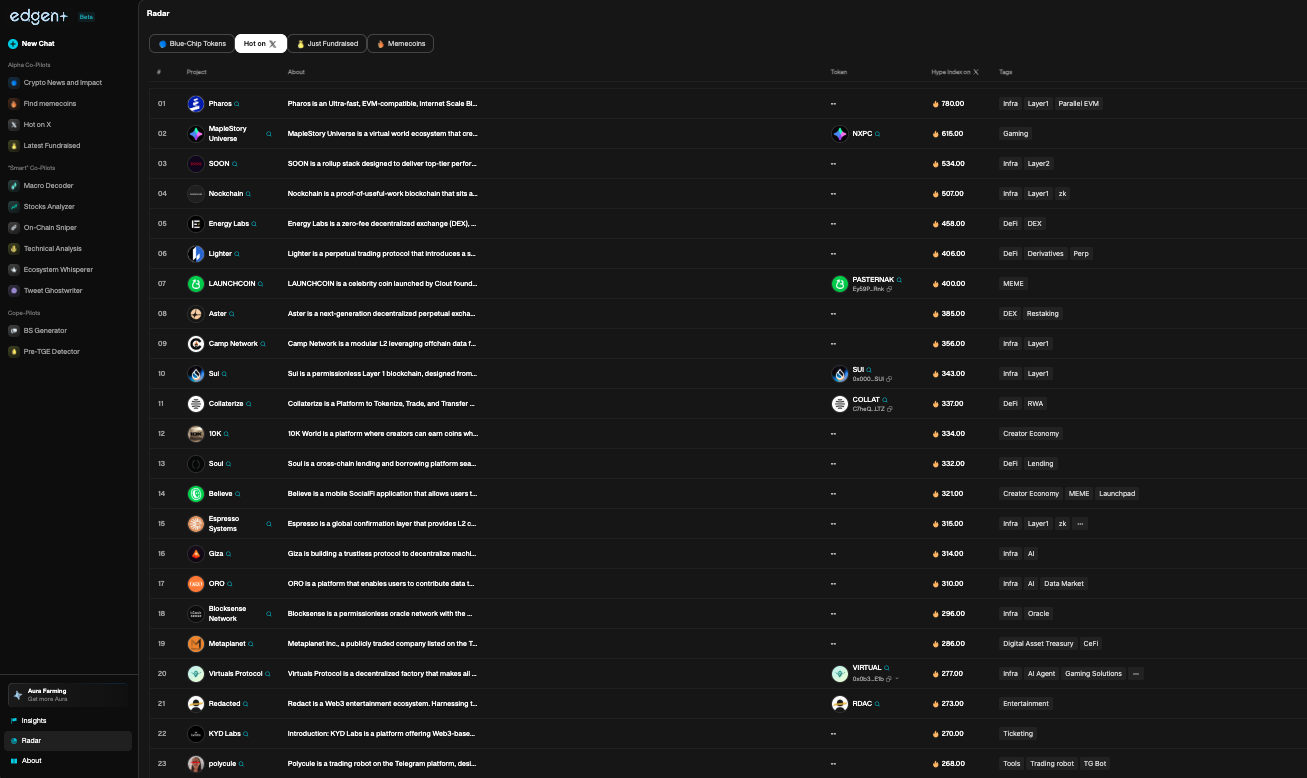

- Edgen RadarMonitoreo en tiempo real de la sentimiento del mercado y tendencias.

- Edgen SearchRespuestas inmediatas respaldadas por perspectivas orientadas al mercado.

- Edgen InsightsInteligencia de mercado oportuna y de origen comunitario.

¿Por qué es importante esto

Los activos de memes y los mercados de criptomonedas prosperan en ciclos de euforia. Plataformas comoWallStreetBetsmostró que el impulso social supera a los indicadores financieros tradicionales en los movimientos de precio.

Edgen AIayuda a los comerciantes a identificar y actuar sobre estospumpamentalstemprano, capturando el alpha antes de que surjan completamente las tendencias.

Adaptarse o Quedarse Obsoleto

El panorama de la inversión evolucionó. Los informes financieros solamente ya no impulsan los mercados. En su lugar, el sentimiento en las redes sociales, las narrativas de los influencers y el análisis impulsado por inteligencia artificial moldean el trading.

El AI Edgen equipa a los traders para:

- Seguimiento y respuesta a cambios de sentimiento en tiempo real

- Monitorear los movimientos del dinero inteligente

- Reacciona con decisión a las narrativas del mercado emergente

Los comerciantes que ignoran las perspectivas impulsadas por la inteligencia artificial enfrentan a oponentes que comercian más rápido, más inteligentemente y mejor informados.

El futuro ha llegado. El éxito en el comercio ahora depende de tu capacidad para aprovechar las herramientas de inteligencia artificial. La era deEdgen AIcomenzó el comercio. Permanezcaadelante, oQuédese atrás. Su movimiento.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Edgen gratis. Sin tarjeta, sin compromiso.