Analyse crypto en chaîne : Comment l'IA aide les traders à rester en avance sur le marché

Les marchés cryptographiques ont évolué, l'analyse traditionnelle est restée en arrière

Les marchés cryptographiques évoluent rapidement. Les méthodes d'analyse traditionnelles ne parviennent pas à fournir des informations précises à temps. Pour rester compétitifs, les traders ont besoin d'analyses en chaîne et de stratégies pilotées par l'intelligence artificielle.

Edgen AIcombine les analyses de la blockchain, l'intelligence artificielle et les signaux sociaux en une solution claire. En analysant les données en temps réel, Edgen élimine les points aveugles, permettant aux traders de saisir des opportunités lucratives dès le début.

Alors que l'IA dépasse les capacités humaines de traitement des données, les vrais avantages sur le marché résident dans les activités liées au blockchain et aux réseaux sociaux "les fondamentaux de la pompe« plutôt que des graphiques techniques seuls »,

Comprendre l'analyse crypto sur la chaîne

L'analyse sur chaîne consiste à suivre les transactions de la blockchain en temps réel pour anticiper les tendances du marché futur. MIT Sloan explains this wellmontrant comment la transparence des systèmes de blockchain aide les investisseurs à prendre de meilleures décisions et pourquoi cette visibilité réforme le marché des cryptomonnaies.

Comme les actifs cryptographiques fonctionnent sur des registres publics transparents, les traders peuvent surveiller avec précision des indicateurs critiques, tels que :

- Transactions du Porte-monnaie Intelligent : Les grands transferts indiquent des changements potentiels de valeur des actifs.

- Entrées et sorties d'échange : Pressions d'achat et de vente identifiées clairement par les activités d'échange.

- Engagement des contrats DeFi : L'activité dans les contrats de finance décentralisée signale des tendances émergentes.

- Signaux d'humeur sociale : Les comptes influents sur les plateformes comme X (anciennement Twitter) ont un impact important sur l'humeur du marché crypto.

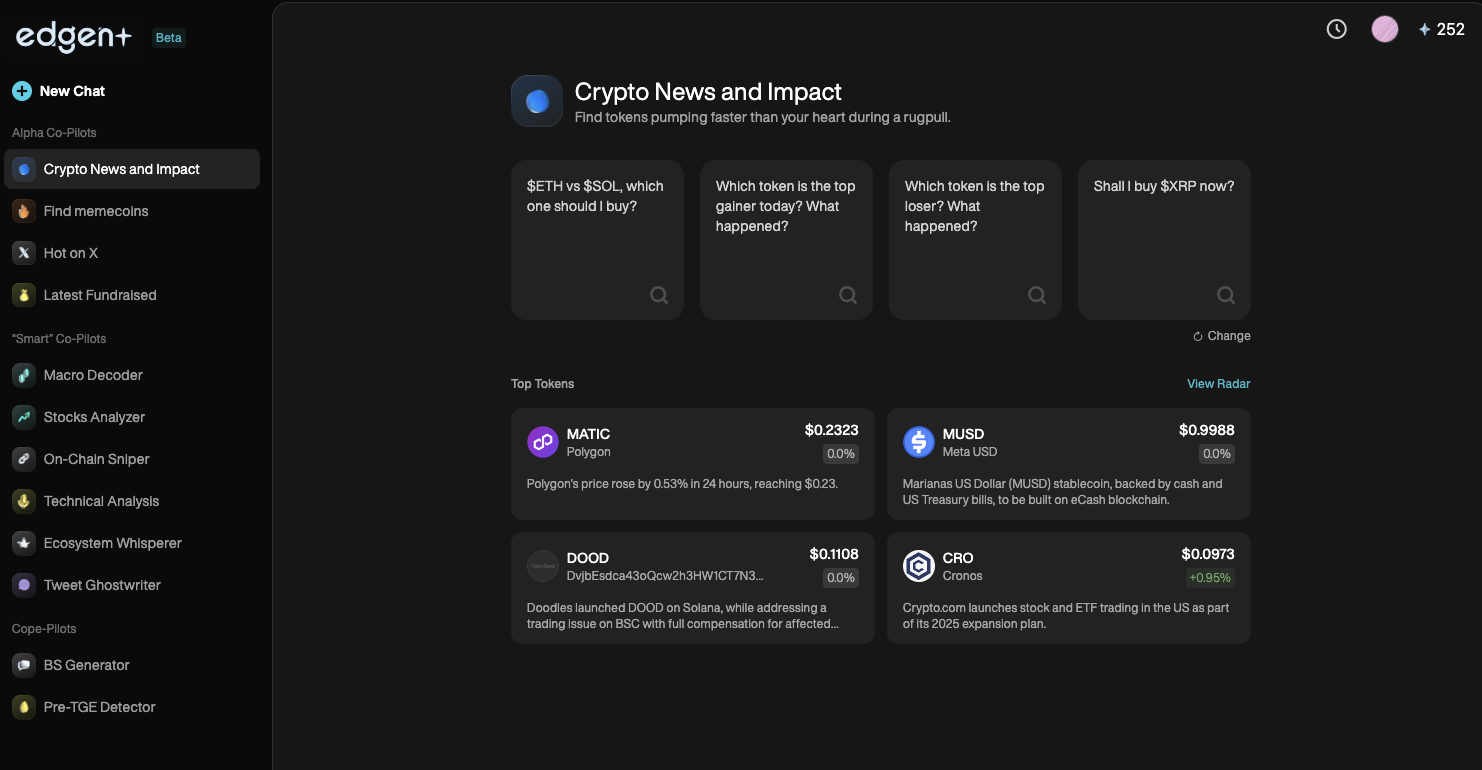

Pour repérer ces changements tôt, vous avez besoin d'outils qui fonctionnent plus vite que vous. Edgen Feedvous tient informé des récits en direct, de la dynamique sociale et de l'activité des portefeuilles en tendance, en temps réel.

Pourquoi l'IA transforme le succès du trading de cryptomonnaies

L'IA dépasse les capacités humaines pour traiter rapidement et avec précision de grandes quantités de données. L'IA d'Edge exploite les forces de l'IA pour fournir des analyses du marché précises et claires, offrant aux utilisateurs un avantage distinct en trading :

1. Précision des prévisions du marché

IA identifie les opportunités de trading avant que les prix ne les reflètent. Edgen AI surveille en continu les mouvements de la blockchain et l'humeur sociale, offrant aux traders des analyses prédictives bien à l'avance.

2. Surveillance en temps réel sur la chaîne de blocs

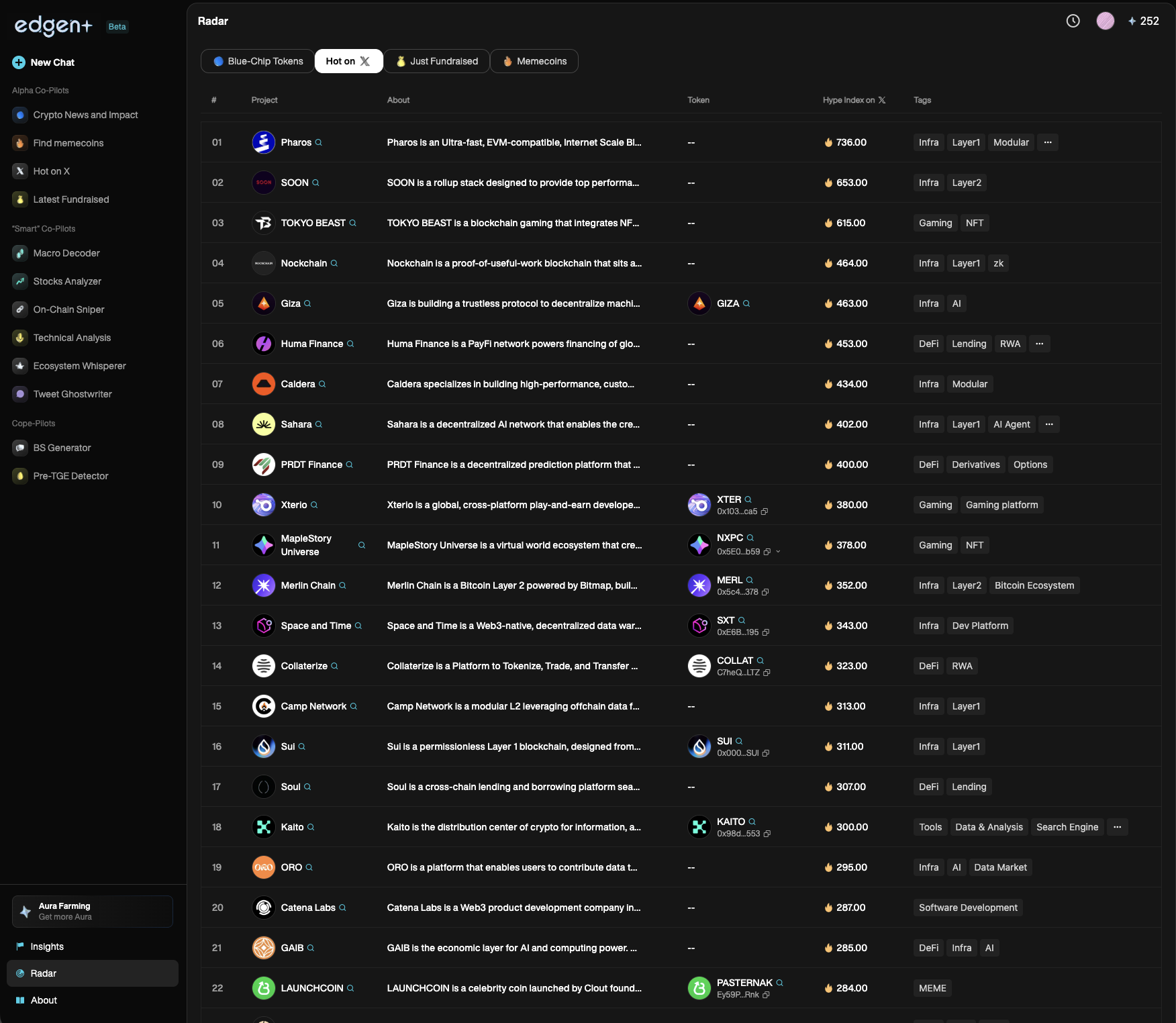

Les marchés ne dorment pas. Votre alimentation de données non plus. Edgen AI scanne en permanence les transactions à haut impact, les mouvements DeFi et les changements de liquidité. Des outils comme Edgen Radarrévéler les jetons en tendance et l'activité des contrats avant que l'action du prix n'atteigne les grandes bourses.

3. Intégration des données sociales et de la blockchain

Les mouvements du marché crypto résultent à la fois d'influences techniques et sociales. Edgen AI intègre l'analyse blockchain et le suivi en temps réel de l'opinion publique, mettant en évidence des signaux alpha précieux que d'autres ignorent.

Le trading sans IA risque de ne pas offrir une visibilité complète. Edgen AI permet aux traders de voir clairement chaque signal important.

Alpha Signals : Votre clé pour les profits en cryptomonnaies

Les traders réussis s'appuient sur des signaux alpha, qui sont des indicateurs anticipés qui prédisent les opportunités du marché avant que la majorité n'en prenne conscience.

Comment Edgen AI détecte clairement les signaux alpha :

- Analyse de l'activité du portefeuille : L'IA identifie et suit les portefeuilles de « whales » et d'insiders grâce aux données de la blockchain et au comportement sur les réseaux sociaux.

- Surveillance des contrats intelligents : les tendances DeFi deviennent claires grâce aux interactions de contrat avant d'apparaître dans les mouvements de prix.

- Social "Pumpamentals: L'IA reconnaît instantanément les tendances sociales émergentes sur des plateformes comme X/Twitter, anticipant les impacts sur les prix avant qu'ils ne atteignent leur pic.

Voulez-vous un avantage de départ ? Edgen Searchvous donne accès aux flux de portefeuille, aux tendances des contrats et au buzz social dans une seule interface rapide, donc vous n'êtes jamais en retard à la fête de l'alpha.

Plateforme d'analyse crypto alimentée par l'IA

Pour rester compétitifs, les traders ont besoin d'une plateforme alimentée par l'intelligence artificielle qui fournit des informations claires et en temps réel sur le blockchain :

Edgen AI intègre les données de blockchain et les signaux sociaux sur une plateforme complète, offrant des signaux d'avantage clairs associés à une exécution pilotée par l'intelligence artificielle.

Edgen AI intègre de manière unique l'analyse blockchain, l'intelligence artificielle et l'analyse en temps réel des sentiments sociaux au sein d'une solution de trading unifiée.

Le futur du commerce appartient à l'IA : Êtes-vous prêt ?

Le trading de cryptomonnaies implique désormais les fondamentaux de la blockchain, le sentiment social et l'exécution immédiate grâce à l'intelligence artificielle.

Points clés pour les traders :

- L'analyse de blockchain pilotée par l'intelligence artificielle dépasse clairement les méthodes traditionnelles.

- Social "les fondamentaux de la pompepoussent les marchés cryptos de manière significative.

- Edgen AIfournit la seule solution de trading du marché qui intègre clairement les données blockchain, les perspectives sociales et l'exécution par l'intelligence artificielle en même temps.

- Les traders utilisant l'intelligence artificielle dominent désormais les mouvements du marché à venir.

Souhaitez-vous savoir comment fonctionne Edgen en arrière-plan ? Visitez Edgen's About page et découvrez pourquoi les meilleurs traders passent à l'intelligence artificielle maintenant.

Ne restez pas en arrière

Les crypto-monnaies évoluent rapidement. Les traders qui réussissent sont ceux qui utilisent des outils qui voient plus vite, pensent plus intelligemment et agissent plus tôt. Avancez. Négociez plus intelligemment.

UtilisezEdgen AI.

Investir, enfin, tu n'es plus seul.

Essaie Edgen gratuitement. Sans carte, sans engagement.