Una evaluación de Moonbirds bajo Orange Cap Games, centrada en la estrategia, ejecución, asociaciones y escenarios de valoración. Puede encontrar la guía de Moonbirds aquí:

En resumen

- OCG está aplicando un manual probado de reactivación de IP que se mueve de la comunidad a la marca y a los productos, ya convirtiendo la atención en actividad y demanda.

- La alineación con inversores de élite, la utilidad tangible como Kaito AI social-to-earn, los avatares de Otherside y los airdrops de socios dan a Moonbirds un fuerte impulso con caminos claros hacia un valor duradero.

Qué es Moonbirds

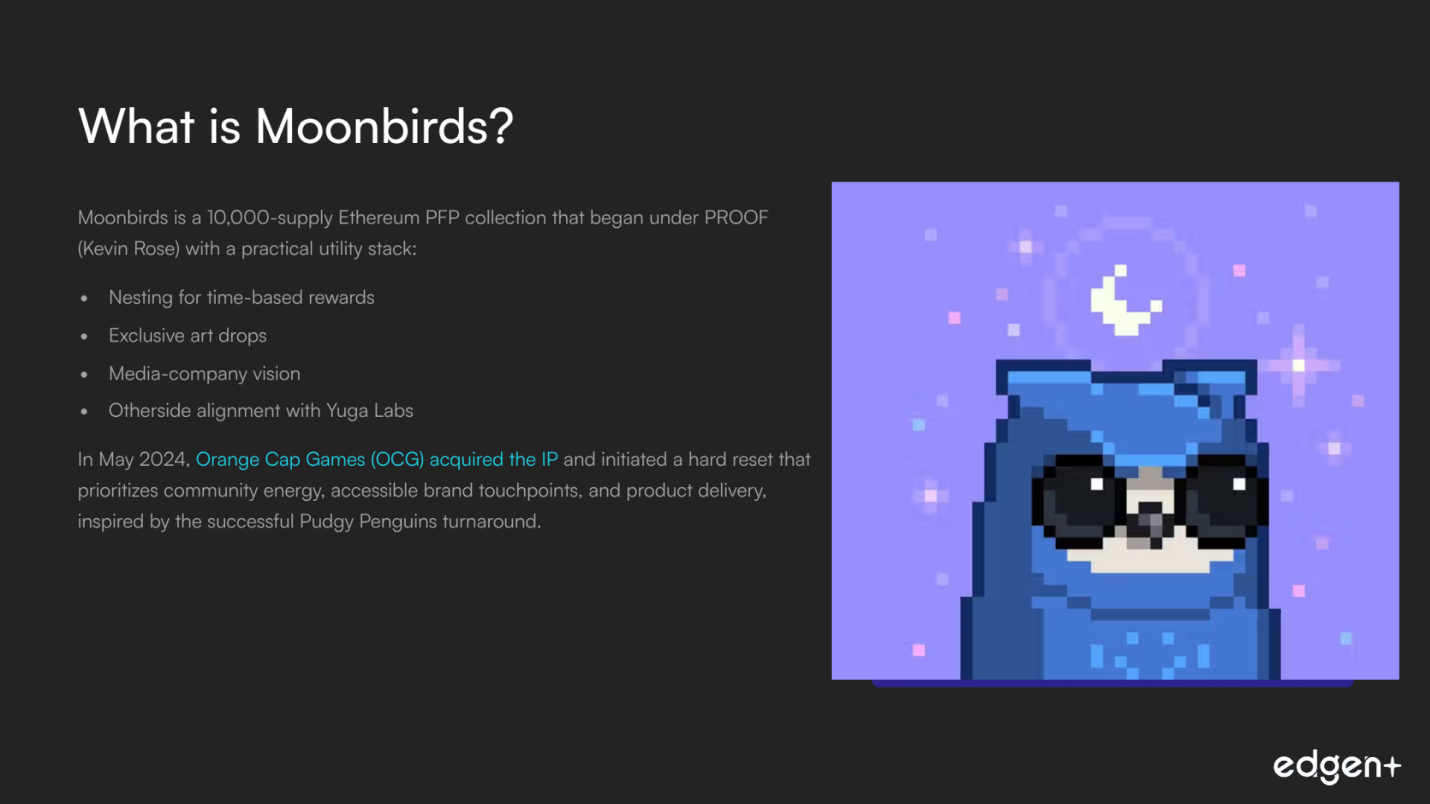

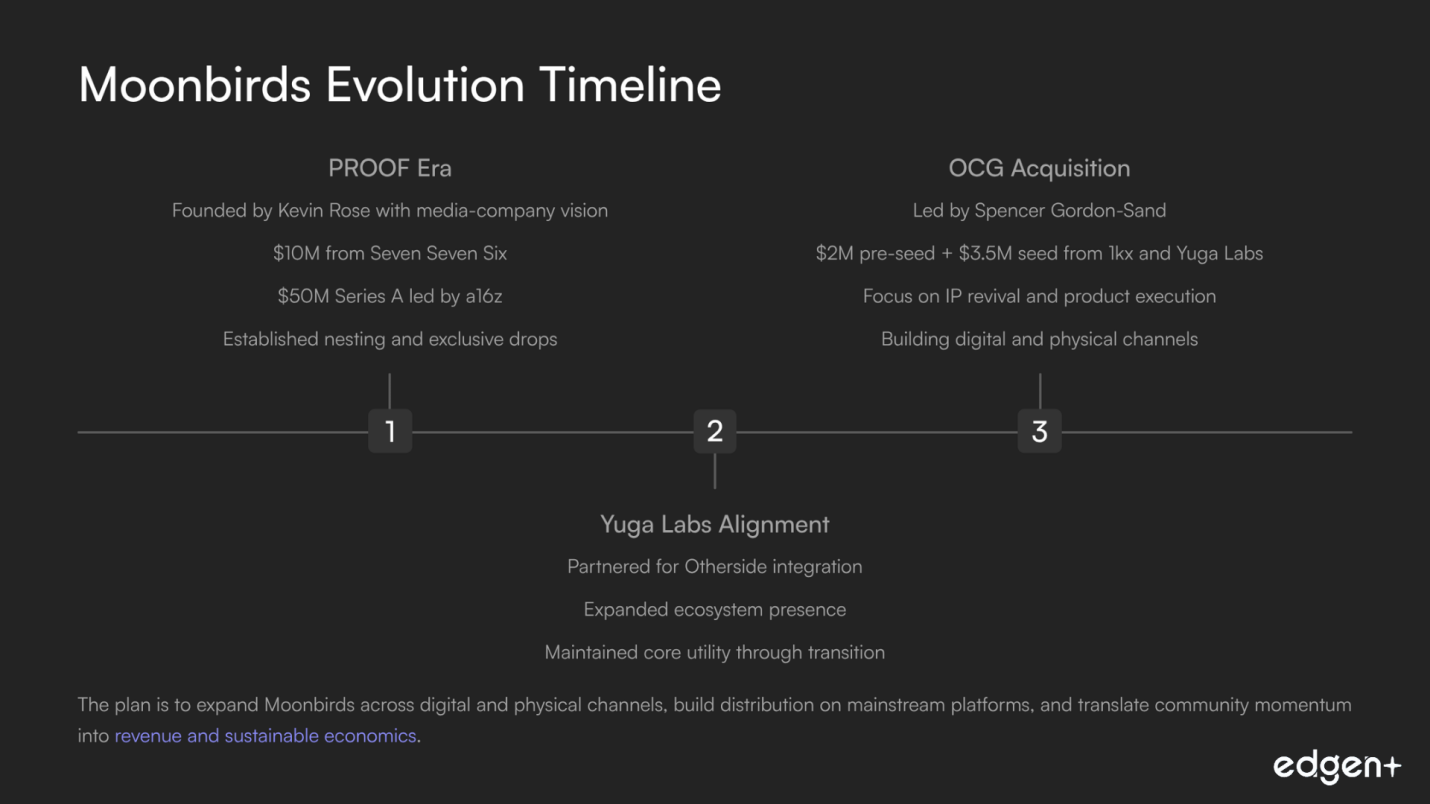

Moonbirds es una colección de PFP de Ethereum con un suministro de 10,000 unidades que comenzó bajo PROOF (Kevin Rose) con un conjunto de utilidades prácticas: Nesting para recompensas basadas en el tiempo, lanzamientos de arte exclusivos y una visión de empresa de medios. Más tarde se alineó con Yuga Labs para Otherside. En mayo de 2025, Orange Cap Games (OCG) adquirió la IP e inició un reinicio completo que prioriza la energía de la comunidad, los puntos de contacto de marca accesibles y la entrega de productos, inspirado en el exitoso cambio de Pudgy Penguins.

Dirigido por Spencer Gordon-Sand, OCG aporta credibilidad cripto-nativa y experiencia en la ejecución de productos, incluido el juego de cartas coleccionables Vibes. El plan es expandir Moonbirds a través de canales digitales y físicos, construir la distribución en plataformas convencionales y traducir el impulso de la comunidad en ingresos y una economía sostenible. Asociaciones como Kaito AI (social-to-earn) y el acceso a airdrops con proyectos como Monad y Towns añaden valor inmediato a los poseedores mientras el equipo trabaja en una plataforma de IP y juegos más amplia.

Con un liderazgo renovado, patrocinadores de alto perfil y un modelo operativo claro, Moonbirds está posicionada para evolucionar de una colección de NFT histórica a una marca duradera y anclada en la utilidad.

I. Análisis fundamental y estratégico

1. Visión y alineación con los inversores

La estrategia ha evolucionado a lo largo de tres eras, desde PROOF hasta Yuga y OCG, hacia una misión enfocada: revivir la IP, energizar la comunidad y lanzar productos.

El apoyo de los inversores refleja este arco, desde el respaldo de a16z a la tesis mediática de PROOF hasta 1kx y Yuga Labs co-liderando la ronda semilla de OCG, alineando el capital con el plan de cambio.

2. Equipo excepcional y capacidad de ejecución

- Ejecución liderada por el CEO Spencer Gordon-Sand, un inversor temprano en NFT y un líder comunitario visible, con experiencia práctica en productos.

- Vibes TCG demuestra ejecución física y digital, además de un camino operativo hacia la fabricación y escala a través de capacidades con sede en Asia.

3. Solidez de capital y respaldos

Las recaudaciones históricas incluyen 10 millones de dólares de Seven Seven Six y una Serie A de 50 millones de dólares liderada por a16z con participantes de primer nivel.

Hoy, OCG cuenta con el apoyo de una ronda semilla de 3.5 millones de dólares de 1kx y Yuga Labs, tras una pre-semilla de 2 millones de dólares, y se ve aumentada por los ingresos de Vibes. Esto crea una base sólida y orientada a la ejecución.

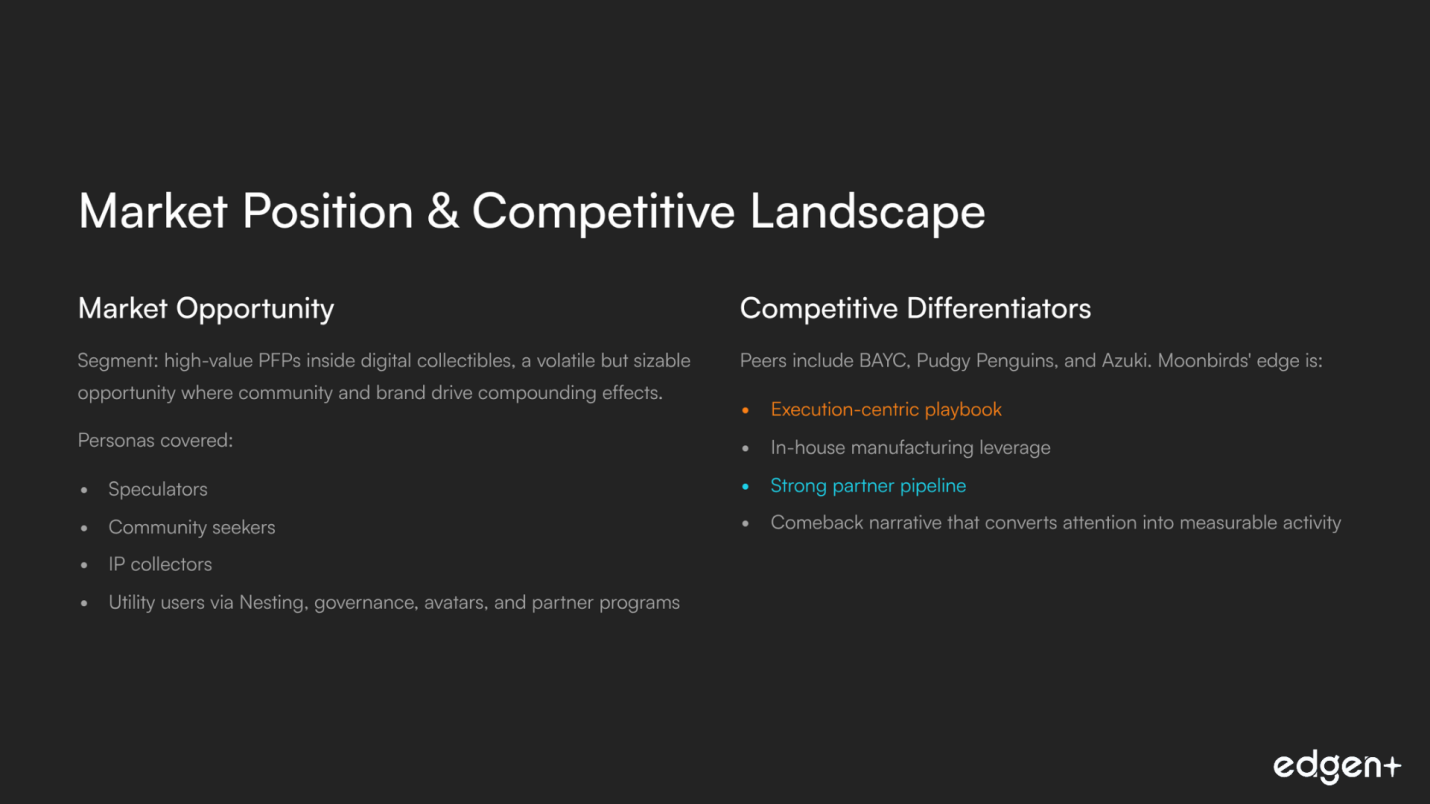

4. Oportunidad y ajuste del mercado

- Segmento: PFP de alto valor dentro de los coleccionables digitales, una oportunidad volátil pero considerable donde la comunidad y la marca impulsan efectos compuestos.

- Personas cubiertas: especuladores, buscadores de comunidad, coleccionistas de IP y usuarios de utilidad a través de Nesting, gobernanza, avatares y programas de socios.

5. Panorama competitivo y diferenciadores

Entre sus pares se encuentran BAYC, Pudgy Penguins y Azuki. La ventaja de Moonbirds es una estrategia centrada en la ejecución, el apalancamiento de la fabricación interna, una sólida cartera de socios y una narrativa de resurgimiento que convierte la atención en actividad medible.

Conclusión fundamental: notable solidez fundamental con inversores alineados, operadores prácticos y una hoja de ruta impulsada por el producto.

II. Ecosistema de pre-lanzamiento y estrategia de salida al mercado

1. Impulso narrativo y de la comunidad

La adquisición de OCG catalizó un cambio narrativo. La comunicación constante del liderazgo y los anuncios de utilidad tangible, como Kaito AI, han revitalizado la actividad social y en la cadena. Las señales apuntan a una mejora en la calidad del compromiso y una base de poseedores receptiva.

2. Huella en la cadena

Una base de poseedores considerable y resiliente proporciona una sólida plataforma de lanzamiento para productos y mecánicas de tokens. El comportamiento de tenencia a largo plazo, la actividad secundaria renovada y las subcolecciones apoyan el acceso mientras se preserva el estatus de la marca.

3. Asociaciones que añaden utilidad

- Kaito AI social-to-earn convierte el contenido en recompensas, transformando la tenencia pasiva en participación activa y descubrimiento.

- Rutas de airdrop como Monad y Towns recompensan a los poseedores y atraen a socios alineados que buscan una distribución de calidad; los avatares 3D listos para Otherside amplían la utilidad interecosistema.

4. Tokenomics y acumulación de valor (hoy)

- Nesting crea recompensas basadas en el tiempo que apoyan el comportamiento de tenencia y prepara el sistema para un futuro token $TALONS.

- La gobernanza a través de la Sociedad Lunar vincula la influencia a los NFT principales y a una tesorería, reforzando la alineación a largo plazo entre los participantes y la marca.

Conclusión sobre la preparación para el GTM: Muy prometedora. Las asociaciones orientadas a la utilidad y la disciplina de entrega forman una base sólida. La preparación del TGE del token se beneficiará de una preparación operativa y legal continua.

III. Análisis prospectivo (Catalizadores y oportunidades)

Corto plazo (≤1 mes)

La activación de Kaito AI potencia el ciclo de los creadores, mejora el descubrimiento y favorece un compromiso duradero que puede fluir hacia el trading y el interés de los socios.

Mediano plazo (1-3 meses)

El primer lanzamiento de producto de la era OCG puede anclar los fundamentos más allá de la narrativa y validar el modelo operativo.

Largo plazo (6+ meses)

El TGE de $TALONS establece precios públicos para la economía en general, permite DeFi y la composabilidad, y aumenta la superficie para los socios.

Visión a futuro: Oportunidades significativas, con la cadencia de ejecución como palanca principal que convierte el impulso en valor duradero.

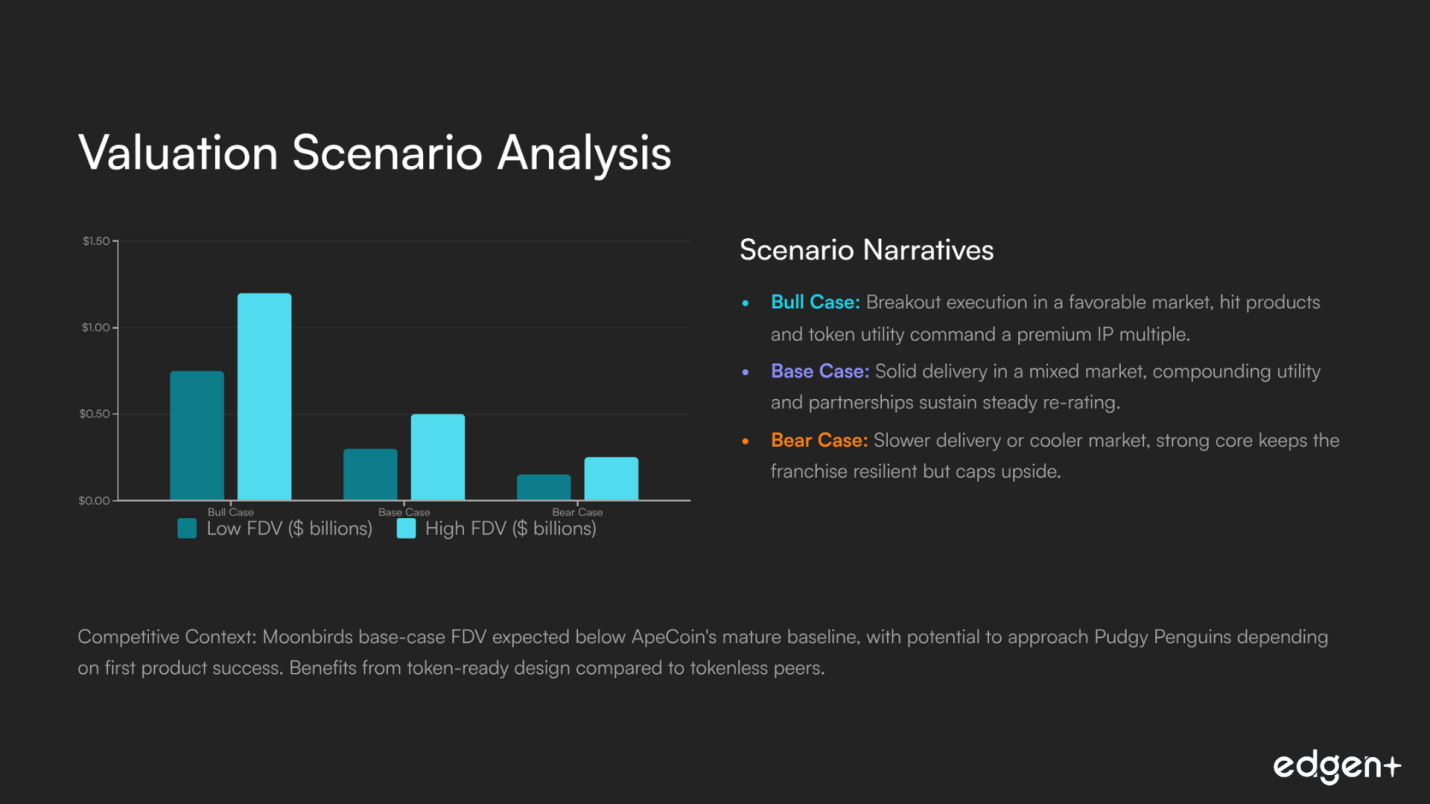

IV. Análisis de escenarios de valoración (FDV de TGE)

Escenario | FDV (miles de millones de USD) | Breve narrativa |

Caso alcista | 0.75 – 1.20 | Ejecución destacada en un mercado favorable, productos exitosos y utilidad del token que generan un múltiplo IP premium. |

Caso base | 0.30 – 0.50 | Entrega sólida en un mercado mixto, utilidad compuesta y asociaciones que mantienen una revalorización constante. |

Caso bajista | 0.15 – 0.25 | Entrega más lenta o mercado más frío, un núcleo fuerte mantiene la franquicia resiliente pero limita el potencial de crecimiento. |

Panorama de competidores (Ángulo del token en o cerca del TGE)

Proyecto | Token | Ángulo TGE/Token | Vínculo con el poseedor | Estilo de distribución | Posición frente a Moonbirds (Caso base) |

ApeCoin / Otherside | Utilidad y gobernanza del ecosistema | Alineación BAYC | Airdrop más listados | El FDV de Moonbirds en el caso base se espera que esté por debajo de la línea base madura de APE; los lazos estratégicos con Yuga son aditivos. | |

Pudgy Penguins | IP, juguetes y volante de juegos | Poseedores de Penguin | Alineado con la comunidad | El FDV de Moonbirds en el caso base está cerca o por debajo de PENGU, dependiendo del éxito del primer producto. | |

Azuki | (ninguno) | IP de marca y orientada al anime | Impulsado por la colección | N/A | Referente par sin token, Moonbirds se beneficia del diseño listo para tokens para una acumulación adicional. |

Conclusión final

Moonbirds muestra un fuerte potencial como un proyecto de reactivación de IP gestionado profesionalmente con raíces comunitarias auténticas y caminos de productos prácticos. Con la alineación de inversores de élite y una tracción temprana de utilidad, el proyecto parece muy prometedor. La velocidad y calidad de la ejecución siguen siendo clave para desbloquear los rangos superiores de la valoración.

Contenido educativo, no asesoramiento financiero.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Ed gratis. Sin tarjeta, sin compromiso.