Edgen Pro & 전문가 플랜 출시: 지금 거래 수준을 높이세요

이것은 매일 발생하는 일입니다: 손에 빙수를 들고 시장을 보며 다음 거래를 결정하려고 노력하고 있습니다. 주변에서는 모든 사람이 코인, 차트, 이익에 대해 이야기하고 있습니다. 화면은 소음으로 가득 차 있고, 수익은 전혀 없습니다. 당신은 명확함을 필요로 합니다. 빠르게.

당신의 고통을 느낍니다. 그리고 우리는 그것을 고쳤습니다.

Edge Pro 및 전문가구독 계획이 공식적으로 오픈되었습니다. 그리고 그건 더 지능적이고 빠른 거래를 위한 티켓입니다.

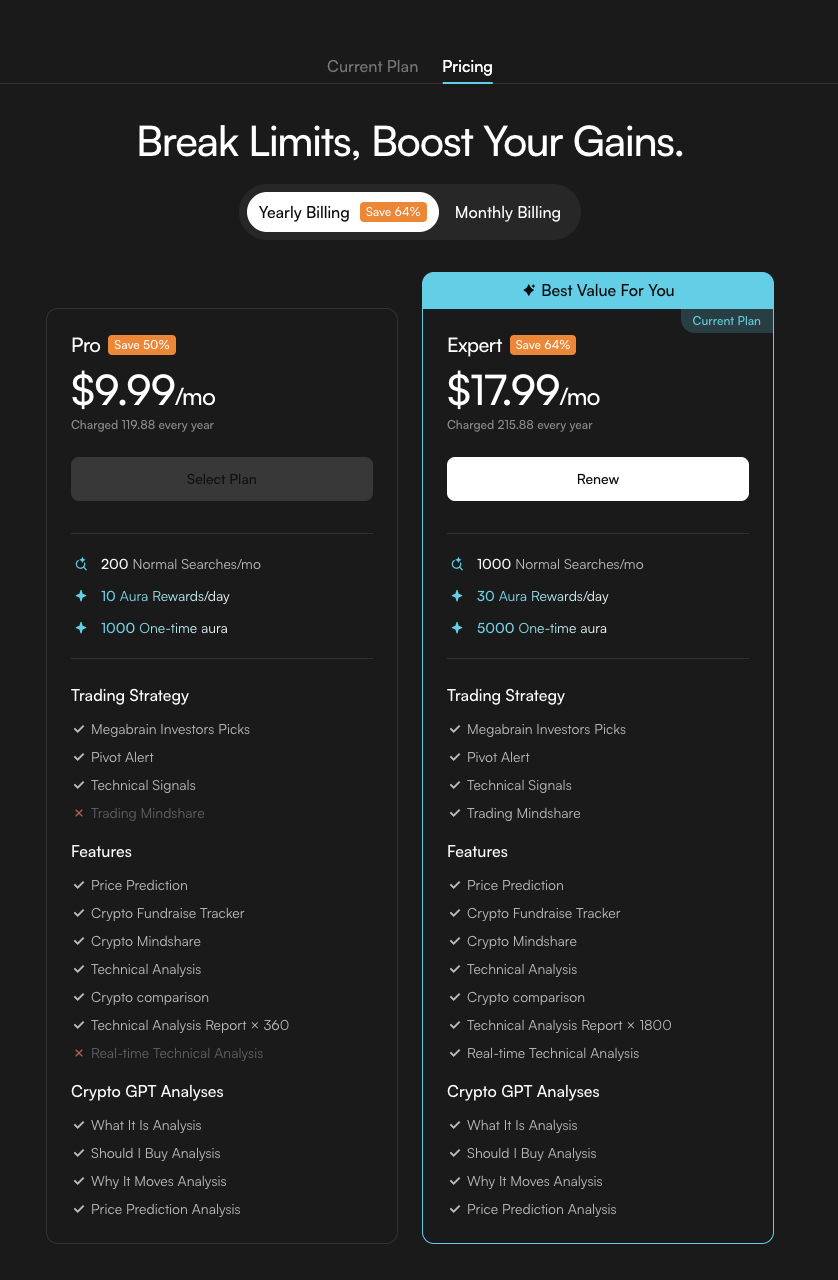

트레이딩이 더 쉬워졌습니다: 2가지 강력한 계획 ✨

간단히 하죠. Edgen은 두 가지 구독 계획을 제공합니다:

Edge Pro ($9.99/월)

더 현명하게 거래하려는 분에게 완벽한:

- 🔎월간 200건의 시장 조사:정확하게 원하는 것을 빠르게 찾아보세요. 시간을 낭비하지 마세요.

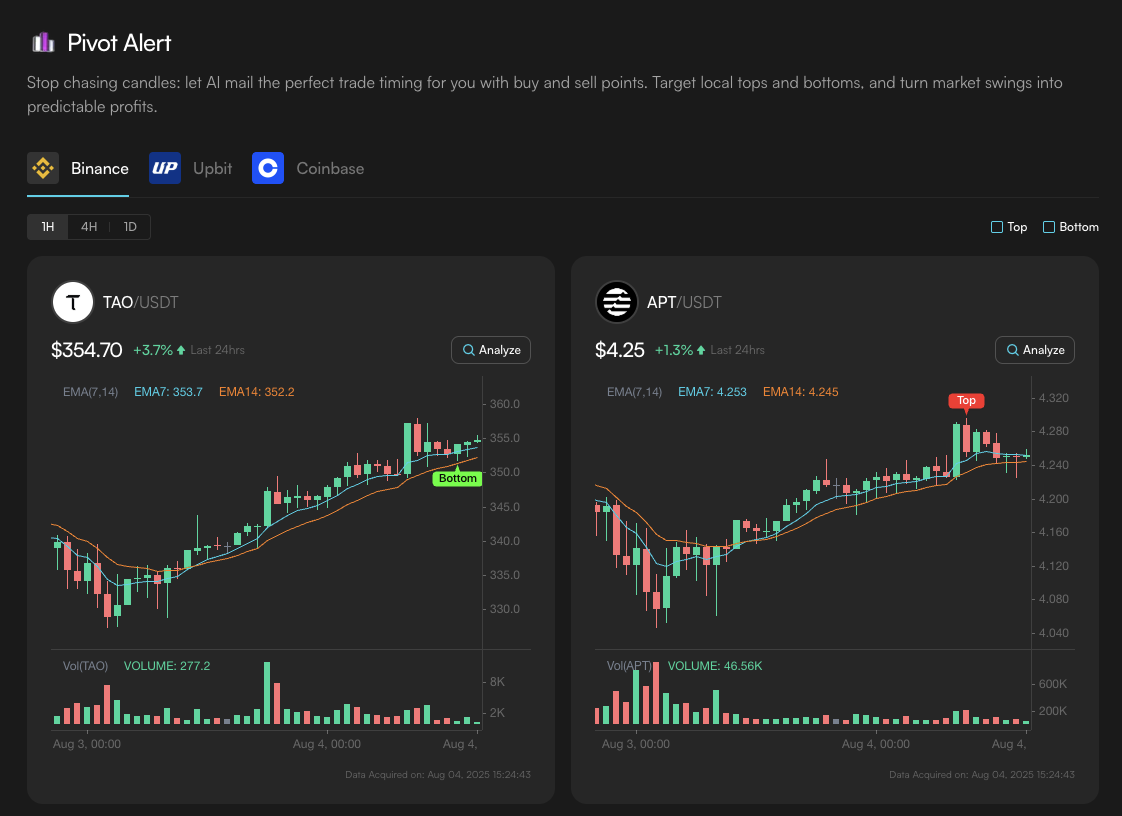

- 📈무제한 피벗 알림 및 기술적 신호 에이전트:다른 사람들이 패닉에 빠질 때도 확신을 갖고 거래하세요.

- 💎1000 아우라 부스트(단일 사용) + 에드진에서 체크인 시 제공되는 10일 간의 아우라 보상:강하게 시작하고, 로그인하여 쉽게 커뮤니티 등급을 높이세요. 간편한 플렉스.

네, Pro는 괜찮아. 하지만 Expert? Expert는 야수야.

Edge 전문가 ($17.99/월)

수익과 신뢰에 진정으로 열중하는 트레이더를 위해 만들어졌습니다:

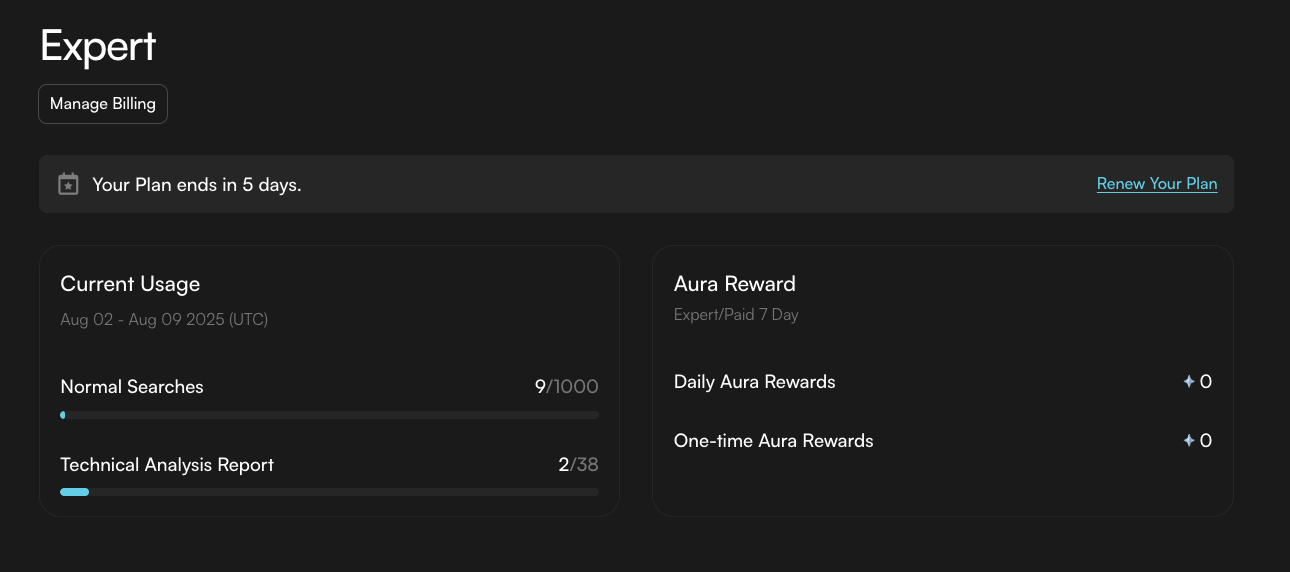

- 🚀월간 1000회 시장 조사:기본적으로 u무한한 가능성, 즉시적인 통찰.

- ⚡️실시간 기술적 분석:시장의 명확함을 즉시 얻으세요, 기다리는 것은 패배자만을 위한 것입니다.

- 🧠모든 프로 에이전트 + 트레이딩 마인드셰어:다른 거래소의 최고 투자자들이 알고 있는 것을, 다른 이들보다 먼저 알아보세요.

- 🌟5000 아우라 부스트(일회성) + 30 일일 아우라 보상:거대한 오라 농사 능력. 더 많은 오라 = 더 많은 신뢰 = 더 많은 알파.

간단히 말해, 전문가란 게임을 끝내야 한다는 뜻이다.

당신의 거래는 더 나은 것을 받을 자격이 있습니다. $1로 시작해보세요 🪙

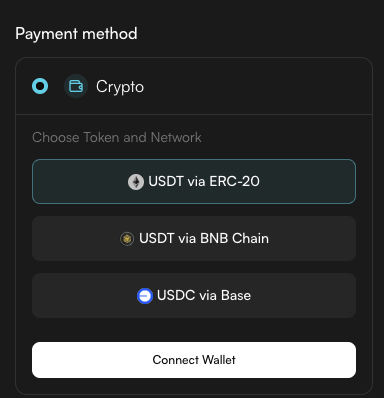

아직 확신이 안 드시나요? 간단하게 해볼게요. 시도해보세요Edgen Pro 또는 Expert만 $1그렇습니다, 단지 1달러입니다. 페이트 또는 암호화폐로 지불할 수 있습니다.

생각해보세요: 즉시 더 현명하게 거래를 시작할 수 있는 1달러입니다. 즉각적인 명확성, 강화된 오라, 그리고 더 현명한 결정을 위한 1달러입니다. 만약 이것이 오늘 당신이 내리는 가장 쉬운 결정이 아니라면, 아마도 잘못된 기사를 읽고 계실 것입니다.

준비가 되었나요? Click here and start your subscription now.

트레이딩이 더 쉬워지고, 더 지능적으로, 그리고 훨씬 더 수익성이 있게 되었습니다. 당신의 새로운 트레이딩 현실을 환영합니다: UP ONLY.

(진지하게, 링크를 클릭하세요. 당신의 미래 버전이 감사할 것입니다.)

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.