Ed가 이번 주에 더 똑똑해졌어요 (5월 22일 업데이트) — 어디가 달라졌나

Edgen | 2026-05-26

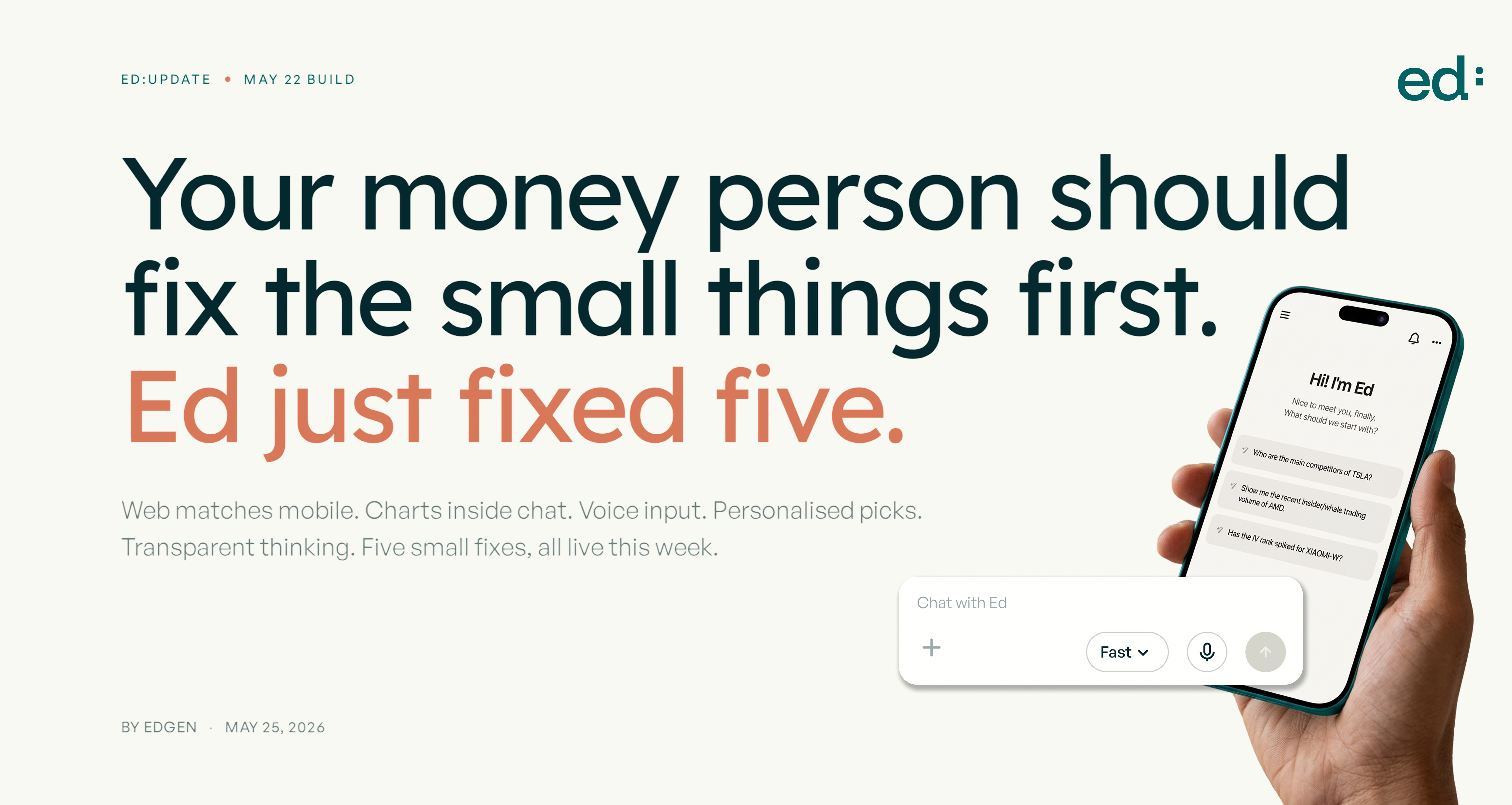

money person이라면 일단 소소한 불편부터 없애줘야겠죠. 이번 주 Ed가 그중 다섯 가지를 정리했어요 — 데스크톱이랑 모바일이 따로 노는 느낌, 데이터 답변이 밋밋한 느낌, Ed가 뭘 하는 중인지 안 보이는 답답함, 이동 중에 긴 질문 타이핑하기 귀찮은 부분, 그리고 홈 화면이 내 취향을 모르는 부분. 다섯 군데 모두 손봤습니다.

1. 이제 어디서 켜도 같은 Ed

웹이 모바일 앱에 이미 있던 브랜드 컬러, 깔끔한 카드 레이아웃, 종 모양 알림까지 그대로 따라왔어요. 아침에 폰으로 열든 점심에 노트북으로 열든 하나의 제품처럼 느껴지고, 알림도 양쪽 다 도착합니다.

2. 숫자 대신 차트로 보여줘요

주가, 시총 구성, 전년 대비 추이 같은 걸 Ed한테 물어보면 이제 답변 안에 깔끔한 차트가 같이 옵니다. 같은 데이터지만 숫자 벽을 머릿속에서 그림으로 변환할 필요 없이, 한눈에 들어와요.

3. Ed가 뭘 하고 있는지 보여요

Ed는 proactive AI예요 — 최종 답변만큼이나 지금 나를 위해 뭘 하고 있는지가 중요하죠. 그 과정이 이제 한 줄로 깔끔하게 보입니다: "Goldman Sachs의 최신 Micron 리포트를 대신 읽고 있어요…", "오늘 시장을 움직인 헤드라인을 정리 중…", "야간에 포트폴리오 모니터링 중…" 같은 식으로요. 멀티 에이전트 로그가 우르르 쏟아지는 게 아니라, 사람 속도로 Ed가 일하는 모습을 그대로 볼 수 있어요.

4. 그냥 말로 물어보세요

채팅 입력창의 마이크 아이콘을 누르고 음성으로 질문하면 됩니다. 출근길, 운전 중, 커피 한 손에 들었을 때 — 긴 질문을 손으로 치기 귀찮을 땐 그냥 말로 하세요.

5. 홈이 이제 나를 알아요

Ed를 열면 홈 화면의 Ed's Picks부터 Ask Ed 안에 미리 떠 있는 질문들까지, 전부 내 것 느낌으로 바뀌어 있어요. 내가 추적 중인 종목, 그동안 물어본 주제에 맞춰서 자동으로 맞춰집니다. 누구한테나 똑같은 피드는 이제 안녕.

다섯 가지 모두 지금 바로 써볼 수 있어요. 웹에서 Ed를 열어보거나, 들고 다니고 싶다면 iPhone 다운로드 또는 Android 다운로드 어느 쪽이든 됩니다. 피드백이나 새로 보고 싶은 기능 있으세요? 답글 남겨주세요 — 전부 읽고 있어요.

Edgen 팀의 제품 업데이트 안내입니다. 투자 권유가 아니며, 기능과 제공 여부는 변경될 수 있어요.