Cómo Edgen AI está revolucionando el trading de criptomonedas con análisis impulsados por IA

El futuro del trading de criptomonedas es impulsado por inteligencia artificial

El trading de criptomonedas es una bestia implacable. Los precios fluctúan en cuestión de segundos, influenciados por todo, desde los movimientos de grandes tenedores (whales) y operaciones institucionales hasta tweets virales y aumentos repentinos en la sentimiento del mercado. Ningún ser humano, sin importar cuán habilidoso sea, puede analizar a la vez todos los datos en cadena, el ruido social y los patrones de trading.

IngreseEdgen AIel asistente para trading de criptomonedas construido precisamente para este caos.

Edgen AI aprovecha analíticas en tiempo real sobre cadenas de bloques, inteligencia artificial de vanguardia y inteligencia social profunda para identificar oportunidades rentables en criptomonedas antes de que el resto del mercado reaccione. Las herramientas tradicionales de trading podrían obsesionarse con gráficos de precios históricos e indicadores técnicos, pero Edgen va más allá: procesa actividad en cadena de bloques en vivo, sentimiento social y perspectivas impulsadas por inteligencia artificial, ofreciendo una ventaja clara en el trading.

Este artículo explica exactamente cómo Edgen AI transforma el trading de criptomonedas y por qué las perspectivas impulsadas por inteligencia artificial representan el siguiente salto en los mercados financieros.

¿Qué es Edgen AI? Negocia con más inteligencia, no con más esfuerzo

Una infraestructura de trading de inteligencia artificial de próxima generación

Edgen AIes una infraestructura de trading de inteligencia artificial para el lado comprador de próxima generación, diseñada específicamente para traders de criptomonedas que necesitan precisión, velocidad y claridad en tiempo real. Combina:

- Real-time On-chain AnalysisRastrea instantáneamente las transacciones de blockchain, los movimientos de whales, los flujos de liquidez y las actividades críticas de tokens.

- Informes del Mercado Potenciados por IA:Identifica oportunidades ocultas de comercio antes de que se vuelvan obvias.

- Seguimiento de la Inteligencia SocialMonitorea a influencers, líderes de opinión clave (KOLs) y el sentimiento de la comunidad en tiempo real para detectar narrativas emergentes.

Con Edgen AI, los traders pueden navegar con confianza las complejidades del mercado de criptomonedas y capturar consistentemente alpha.

¿Por qué las herramientas tradicionales no pueden competir con Edgen AI

Las herramientas tradicionales de cripto principalmente dependen de datos históricos de precios, tendencias básicas y indicadores técnicos. Aunque estos métodos podrían ser suficientes en mercados más lentos, no son adecuados en el actual entorno en constante evolución impulsado por la inteligencia artificial.

Edgen AI rompe este enfoque de antaño mediante:

- Analizar instantáneamente datos en cadena en vivodescubrir movimientos ocultos en el mercado antes de que los traders tradicionales los noten.

- Seguimiento del sentimiento social en tiempo realpara entender la psicología del mercado y la comunidad criptográfica "impulsada por la comunidad"pumpamentals."

- Impulsar la toma de decisiones basada en inteligencia artificialpara que los comerciantes puedan ejecutar estrategias rápidamente, respaldadas por datos en lugar de instintos.

Usar Edgen AI se traduce directamente en estrategias más inteligentes, perspectivas más profundas y ejecución de comercios acelerada.

La potencia de la IA en el trading de criptomonedas: La ventaja injusta de Edgen

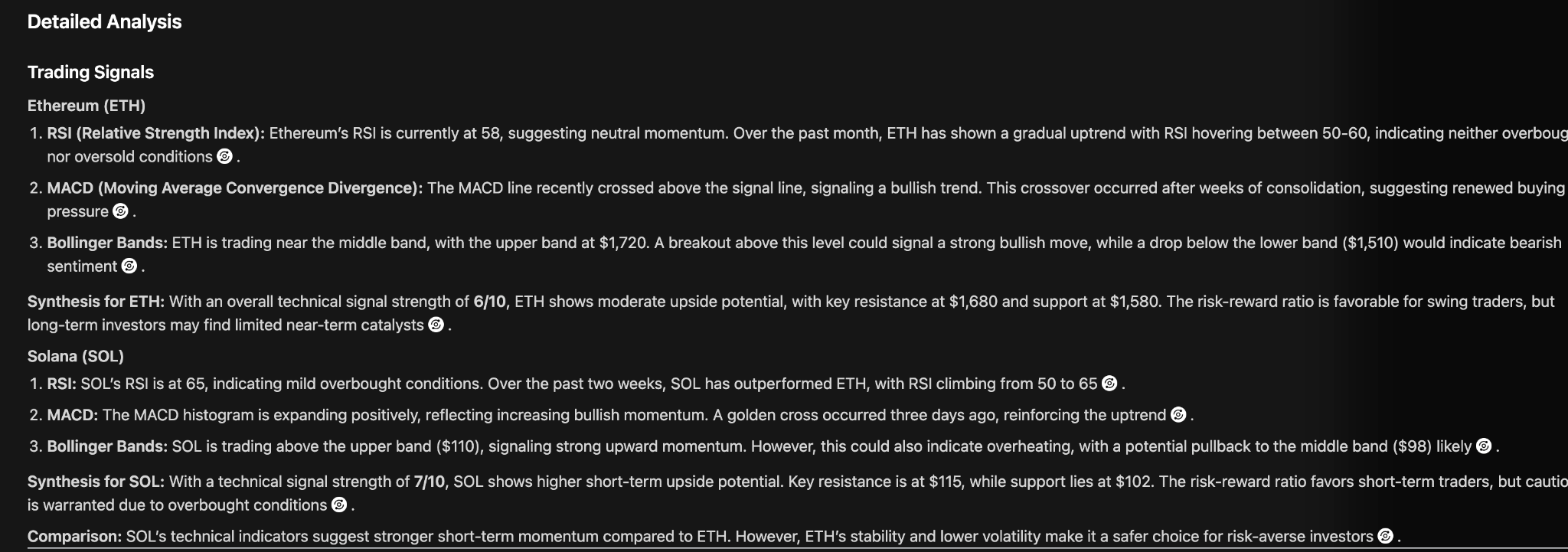

1. Análisis predictivo impulsado por IA

Los mercados de criptoactivos pueden parecer aleatorios... hasta que introduces la inteligencia artificial. Edgen AI utiliza análisis predictivo sofisticado para descubrir patrones ocultos que los humanos no pueden detectar con suficiente rapidez:

- Escaneando millones de puntos de datos por segundo para predecir movimientos en los precios.

- Detectar tendencias y anomalías en mercados emergentes antes de que se conviertan en principales.

- Seguimiento del sentimiento social para identificar narrativas y ciclos de euforia que mueven el mercado.

Con Edgen AI, los traders se mantienen proactivos en lugar de perseguir las noticias de ayer.

2. Análisis del Mercado en Tiempo Real con Datos de Cadena

Ignorar los costos de datos de blockchaincomerciantesvaliosas oportunidades. Edgen AI se adentra en la actividad en cadena en tiempo real para descubrir:

- Movimientos de ballenaDetectando instantáneamente transacciones grandes que indican movimientos significativos en el precio.

- Interacciones con Contratos InteligentesDetección de interacciones críticas con carteras en protocolos DeFi.

- Desplazamientos de liquidezPredecir los cambios en los precios monitoreando los flujos de liquidez de las tokens entre las bolsas.

Visite Edgen Radarexplorar analíticas en tiempo real de blockchain.

3. Trading Asistido por IA vs. Trading Manual

El trading manual es agotador, emocional y propenso a errores costosos. Edgen AI elimina este adivinar mediante:

- Escaneando constantemente los mercados 24/7, sin perder un solo ritmo.

- Ejecutar operaciones automáticamente basadas en señales precisas y orientadas a datos.

- Eliminando por completo los sesgos emocionales, enfocándose estrictamente en los datos y la estrategia.

Los comerciantes que utilizan estrategias impulsadas por inteligencia artificial superan consistentemente a aquellos que dependen únicamente de la intuición.

Características Clave que Diferencian a Edgen AI

1. Análisis Integral del Mercado en Tiempo Real

- Procesamiento inmediato de datos en cadena y fuera de la cadena.

- Monitoreo continuo de liquidez, movimientos de whales y actividades de carteras clave.

- Seguimiento de sentimientos en crypto Twitter, Telegram y redes de influencers.

Explorar Edgen's real-time Feedmonitorear la actividad del mercado.

2. Señales de Trading Potenciadas por IA

- Alertas en tiempo real que identifican oportunidades de trading con alta probabilidad.

- Análisis predictivo que identifica tempranamente tokens subvalorados.

- Algoritmos avanzados que revelan señales de compra y venta ocultas mucho antes de la aceptación general.

3. Herramientas de Gestión Inteligente de Riesgos

- Evaluaciones de riesgo impulsadas por IA para señalar movimientos potencialmente riesgosos.

- Recomendaciones inteligentes de stop-loss y tamaño de posición adaptadas a las condiciones del mercado.

- Perfiles de riesgo flexibles adaptables a las preferencias del trader.

4. Estrategias de Trading Automatizado

- Ejecución de comercio impulsada por IA en tiempo real basada en perspectivas del mercado en tiempo real.

- Comercio sin emociones, eliminando decisiones impulsivas.

- Monitoreo continuo que garantiza que aproveche cada oportunidad posible.

Empiece con Edgen searchpara descubrir señales de trading y oportunidades en el mercado.

El Futuro de la IA en el Trading de Criptomonedas: La Visión de Edgen

1. Predicciones Mejoradas del Mercado con Inteligencia Artificial

En los próximos años, las plataformas impulsadas por IA como Edgen lo harán:

- Predecir con precisión las tendencias del mercado aún con más antelación.

- Descubre señales de alpha ocultas que los traders humanos simplemente no pueden detectar.

- Reduzca aún más los riesgos de trading con modelos predictivos más avanzados.

2. Datos en cadena convirtiéndose en esenciales

- La IA estandarizará el seguimiento rápido de tendencias DeFi, transacciones de whales y sentimiento social.

- Transparencia deblockchain datase convertirá en fundamental para las estrategias exitosas.

3. Dominancia del Trading de IA Automatizado

- Los bots de trading impulsados por IA se convertirán en la norma en lugar de la excepción.

- El comercio manual disminuirá significativamente a medida que la IA demuestre constantemente una mayor eficiencia.

Edgen AI está perfectamente posicionada para liderar esta transformación.

Comercie de forma más inteligente, comenzando ahora con Edgen AI

El trading de criptomonedas está evolucionando rápidamente, y el futuro claramente pertenece a los traders impulsados por inteligencia artificial. Edgen AI te da las herramientas necesarias para:

- Descubra perspectivas más profundas del mercado, mejorando la toma de decisiones y las ganancias.

- Aproveche el análisis en tiempo real de blockchain para estar un paso adelante.

- Elimina las emociones del comercio, dejando que los datos guíen el camino.

No negocies más: negocia con más inteligencia.Acepta el futuro impulsado por IA de la negociación de criptomonedas hoy con Edgen AIy siempre mantén la delantera en el mercado.

Fortalezas de SEO del artículo

✅Título y descripción meta fuertes:

- El título es rico en palabras clave y atractivo.

- La meta descripción es concisa y atractiva, resumiendo los puntos clave mientras incluye palabras clave relevantes como"Insights impulsados por IA","comercio de criptomonedas", etc.

✅Uso efectivo de encabezados (H1, H2, H3, etc.)

- El artículo está bien estructurado con títulos claros.

- Cubre temas clave en un orden lógico, lo que mejora la legibilidad y el SEO.

✅Optimización de palabras clave:

- El artículo incluye palabras clave de alto valor relacionadas con criptomonedas y inteligencia artificial, como:

- "Insights impulsados por IA,"

- "en-datos de la cadena",

- "alfaseñales de trading,

- "análisis de mercado en tiempo real,"

- Estas palabras clave ayudan a mejorar el posicionamiento para búsquedas relacionadas con el trading de criptomonedas impulsado por inteligencia artificial.

✅Profundidad del Contenido y Experiencia:

- El artículo ofrece perspectivas detalladas, estudios de caso y explicaciones, indicando autoridad sobre el tema.

- Google favorece el contenido bien investigado y profundo para el posicionamiento en motores de búsqueda.

✅Legibilidad y Participación:

- Párrafos cortos y un lenguaje simple y directo mejoran la experiencia del usuario y el tiempo de permanencia.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Ed gratis. Sin tarjeta, sin compromiso.