Credo Technology tras el acuerdo con DustPhotonics: por qué la compra de fotónica de silicio de 750 millones de dólares de CRDO y la calificación de Compra de Jefferies revalorizan la tesis de redes de IA

Por David Hartley | 2026-04-15 Calificación: Compra | Precio objetivo: 205 $ (30 % de potencial alcista) Sector: Semiconductores — Redes de IA, DSP ópticos, cables eléctricos activos (AEC) Categoría: Tecnología e IA > Semiconductores | Infraestructura de IA | Ticker: $CRDO

Resumen

- Credo Technology (NASDAQ: CRDO) cerró el 14 de abril de 2026 a 157,69 $, un 15 % más intradía, gracias a dos catalizadores que aterrizaron el mismo día: Jefferies elevó su precio objetivo mientras reiteraba una calificación de Compra, y Credo anunció la adquisición de 750 millones de dólares del innovador en fotónica de silicio DustPhotonics, un acuerdo que integra talento y propiedad intelectual de óptica coempaquetada (CPO) directamente sobre la pila existente de SerDes y DSP de 800G/1.6T de Credo.

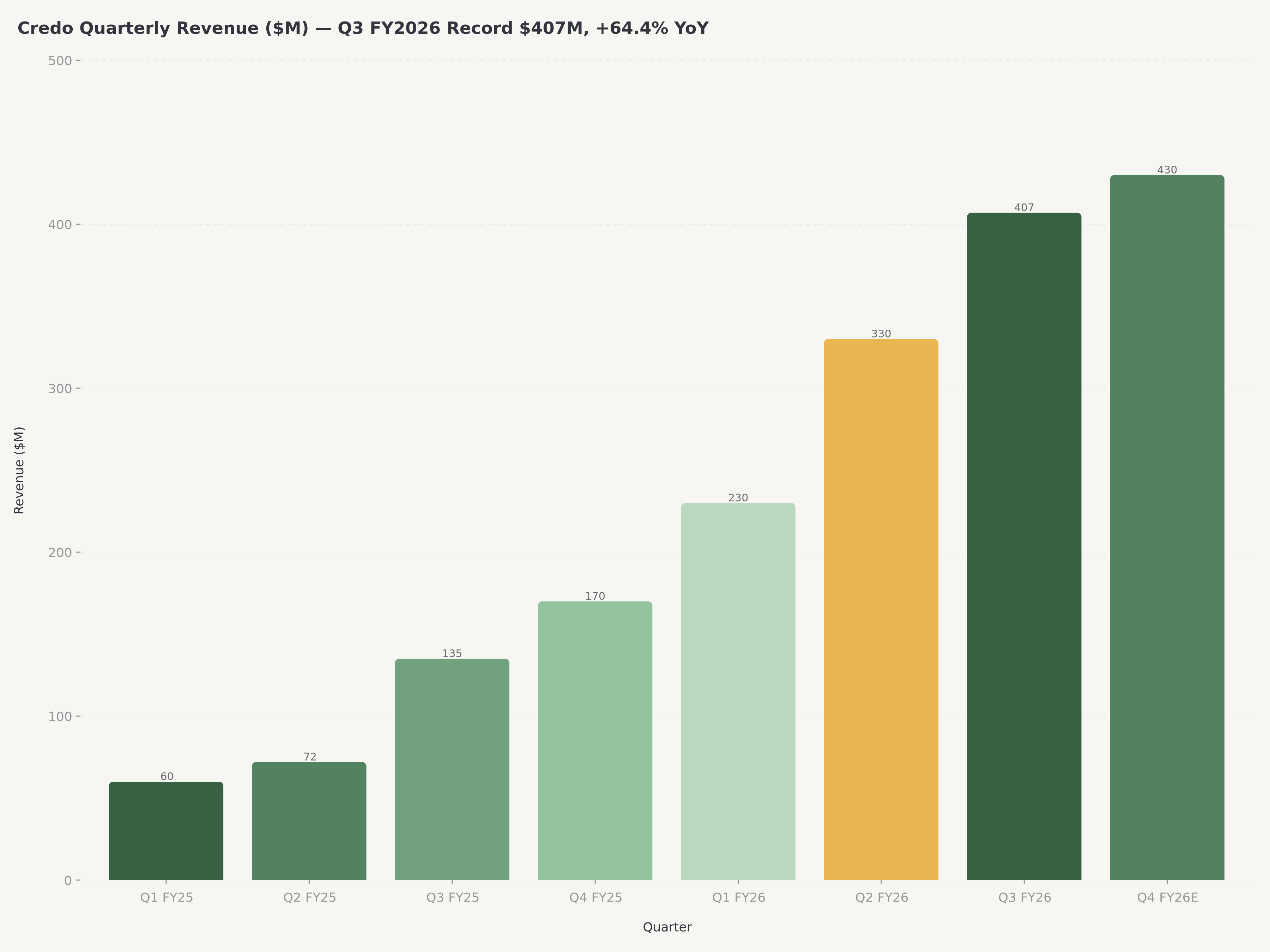

- El trasfondo financiero detrás de la revalorización es extraordinario: ingresos del tercer trimestre del año fiscal 2026 de 407 millones de dólares (+64,4 % interanual), margen bruto no-GAAP del 68,6 %, margen operativo no-GAAP del 49,6 %, y un crecimiento de ingresos para todo el año fiscal 2026 que apunta a más del doble interanual (muy por encima del 100 %).

- El modelo de cuatro escenarios de Edgen 360° enmarca el debate: escenario Alcista 273 $ (35 % de probabilidad), Caso Base 109 $ (15 %), escenario Bajista 85 $ (35 %) y escenario de Desastre 49 $ (15 %). El valor razonable ponderado por probabilidad se sitúa cerca de los 148 $, lo que significa que a 157,69 $ el mercado ya está valorando a Credo ligeramente por encima de la estimación central, pero el acuerdo con DustPhotonics eleva plausiblemente la probabilidad alcista.

- Calificamos a CRDO como Compra con un precio objetivo de 205 $, lo que refleja los escenarios reponderados tras DustPhotonics (Alcista 45 % / Base 15 % / Bajista 25 % / Desastre 15 %) que producen un valor razonable revisado cerca de 182 $, más una prima de catalizador de ~23 $ por el valor de opción de integración de fotónica de silicio.

¿Por qué esto importa ahora?: Dos catalizadores, un día

El 14 de abril de 2026 pasará a la historia de Credo como la sesión más importante desde su salida a bolsa. Dos catalizadores convergieron para hacer subir la acción un 15 %.

Catalizador #1 — Jefferies eleva el precio objetivo, reitera Compra. Jefferies elevó su precio objetivo tras haberlo recortado apenas seis semanas antes, lo que indica un cambio de opinión significativo y suele preceder a flujos institucionales. El rendimiento de +132,80 % en 6 meses frente al +25 % del S&P 500 convirtió a CRDO en un claro ganador relativo.

Catalizador #2 — Adquisición de DustPhotonics por 750 millones de dólares. DustPhotonics se especializa en óptica coempaquetada (CPO), la tecnología que reduce drásticamente el consumo de energía por bit en la próxima generación de interconexión de IA de 1.6T/3.2T. Este movimiento cierra la brecha tecnológica con competidores como Marvell (MRVL) y Broadcom (AVGO).

Quién es Credo y por qué importa el equipo directivo

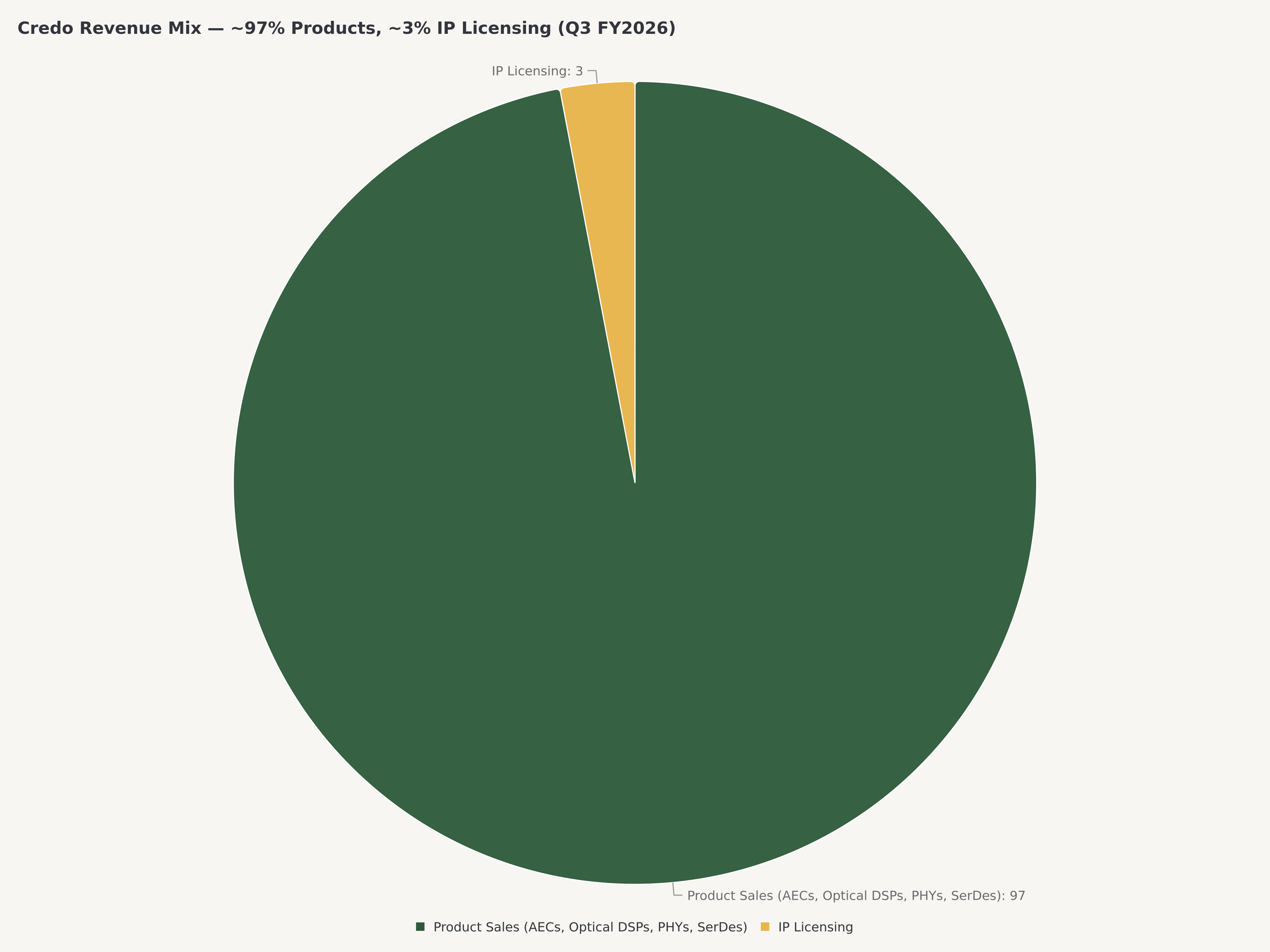

Credo es una empresa de semiconductores sin fábrica (fabless) centrada en la conectividad de alta velocidad para centros de datos. En el T3 fiscal de 2026, el 97 % de sus ingresos provino de la venta de productos.

El equipo ejecutivo, liderado por William Brennan, tiene un fuerte pedigrí de Marvell e Inphi. La junta directiva cuenta con figuras como Lip-Bu Tan. Esta experiencia operativa en redes de IA y relaciones con hiperescaladores es un activo competitivo genuino.

Rendimiento del T3 fiscal 2026

- Ingresos: 407 millones de dólares, un 64,4 % más interanual.

- Margen bruto no-GAAP: 68,6 %, récord en el sector.

- Margen operativo no-GAAP: 49,6 %.

Expandir el margen mientras se triplican los ingresos indica un fuerte poder de fijación de precios.

Riesgos clave

- Concentración de clientes: Un solo cliente representa más del 40 % de los ingresos.

- Riesgo de integración: Integrar una adquisición de 750 millones de dólares sin distraerse del crecimiento principal.

- Competencia: Marvell y Broadcom son rivales formidables con mayores recursos.

- Riesgo macro y geopolítico: Exposición a las fundiciones de Taiwán (TSMC) y a los controles de exportación de chips de EE. UU. a China.

Veredicto: Comprar CRDO con precio objetivo de 205 $

La historia fundamental de Credo es extraordinaria. Con ingresos que se duplican y márgenes líderes, la compra de DustPhotonics refuerza su posición en la futura tecnología CPO. Recomendamos entrar en retrocesos hacia los 140-145 $.

FAQ

¿Por qué subió la acción el 14 de abril?

Debido a la mejora de precio objetivo de Jefferies y la adquisición de DustPhotonics por 750 millones de dólares.

¿Cómo se compara con Astera Labs?

Astera Labs (ALAB) es el comparador más directo. Credo tiene una pila tecnológica más amplia que abarca interconexión eléctrica y óptica, mientras que ALAB está más concentrada en GPU-a-GPU dentro del rack.

Descargo de responsabilidad: Este artículo es solo para fines informativos y no constituye asesoramiento de inversión.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Edgen gratis. Sin tarjeta, sin compromiso.