Comercio con IA hoy: ¿Por qué los monederos inteligentes y los KOL dominan el mercado (ahora integrados con Edgen AI)

El Trading con IA se ha vuelto irresistible

El trading con IA transforma los mercados financieros en 2025: más rápido, más inteligente y más accesible que nunca.

Billeteras inteligentes y Líderes de Opinión Clave (KOLs) impulsan esta nueva era de trading. Sus conocimientos y tecnología empoderan a todos los traders, desde principiantes hasta expertos, nivelando el campo de juego.

Ya no existen los métodos tradicionales de inversión. Ahora los traders obtienen ventajas mediante análisis en cadena, señales de alpha y tendencias del mercado impulsadas por las redes sociales.

Según Wharton University of Pennsylvania, la IA está revolucionando las finanzas al permitir que los sistemas generen estrategias de trading novedosas, ejecuten operaciones y se adapten a las condiciones del mercado en tiempo real, transformando así el escenario de los servicios financieros.

Edgen AI"el 'AI de Trading que Lee la Sala', redefine por completo el paisaje del trading.

El auge del trading con inteligencia artificial

El trading con IA existía antes, pero hoy domina los mercados.

Los comerciantes ya no dependen únicamente de la intuición. La IA evalúa miles de millones de puntos de datos instantáneamente, identifica patrones claramente y ejecuta operaciones rápidamente.

¿Por qué el trading con inteligencia artificial lidera el mercado ahora:

- Velocidad: La IA analiza las tendencias del mercado más rápido de lo que los humanos podrían hacer.

- Precisión: Identifica tendencias emergentes y cambios en el mercado con bastante antelación a la conciencia general.

- Automatización: los bots de trading con IA ejecutan operaciones 24/7, sin estar afectados por el cansancio o las horas de mercado.

Las emociones humanas como la venta desesperada o las compras impulsivas ya no afectan el comercio. Las plataformas impulsadas por inteligencia artificial permanecen estables, basadas en datos y precisas.

Sin embargo, las herramientas tradicionales de trading con inteligencia artificial a menudo ignoran las narrativas sociales e la influencia de los KOL. Edgen AI cubre este vacío.

La Revolución de Edgen AI en el Espacio de Trading con IA

El AI Edgen integra análisis en cadena con los "pumpamentals" sociales, evaluando en tiempo real el sentimiento de KOLs, las transacciones de billeteras inteligentes y las narrativas del mercado.

¿Qué hace único a Edgen AI?

- Insumos de Consenso Social: Evalúa comentarios en tiempo real de KOL y narrativas en tendencia de plataformas como X (anteriormente Twitter).

- Análisis de datos en cadena: Rastrea transacciones, movimientos de billeteras de grandes tenedores, cambios en la liquidez y actividades de tokens en tiempo real.

- Toma de decisiones con IA: Predice los cambios del mercado combinando el análisis de datos tradicional con el impulso social.

Sin Edgen AI, los traders pierden señales ocultas generadas por el sentimiento social y figuras influyentes.

Características Clave de Edgen AI que Potencian a los Traders

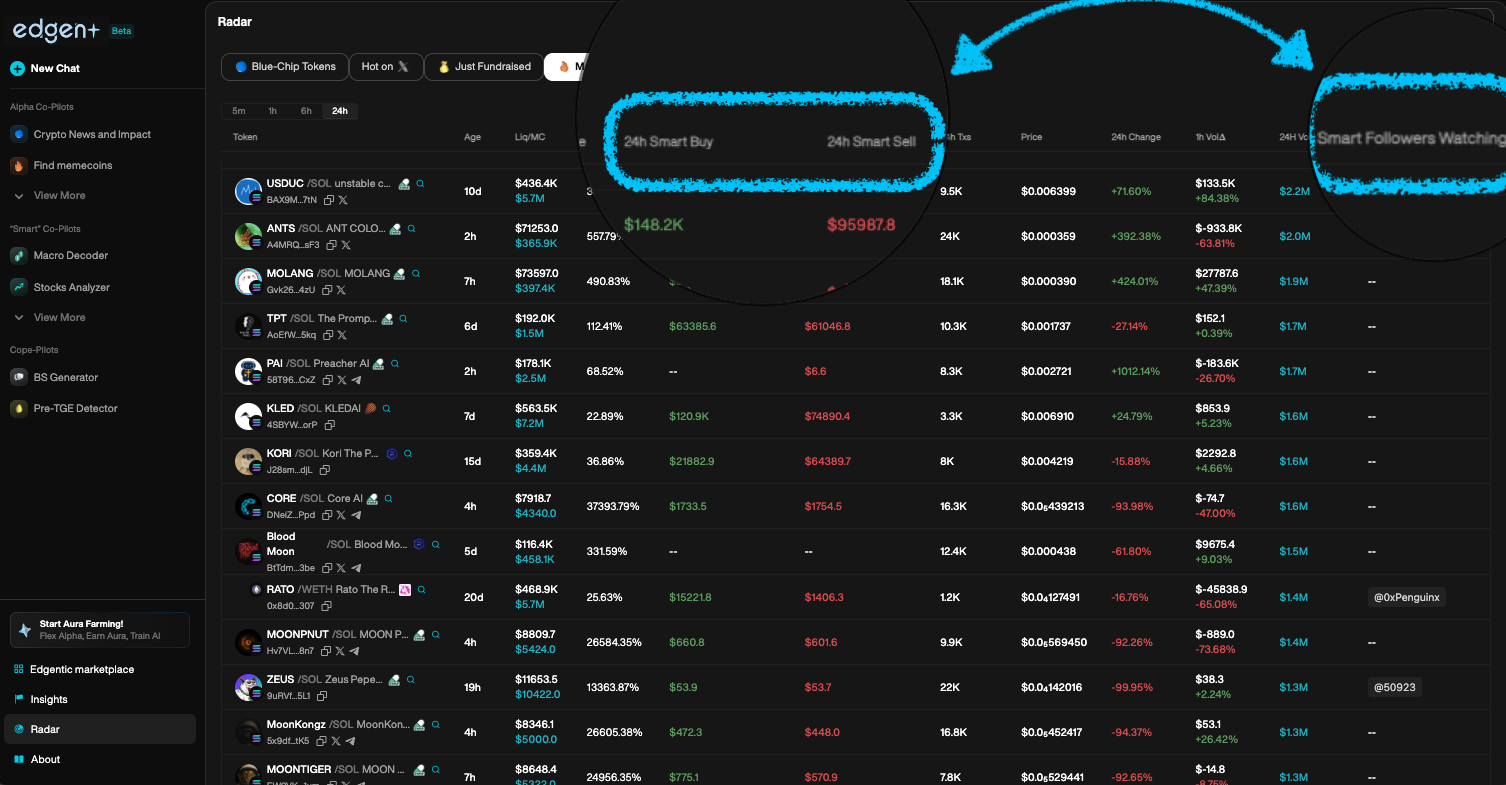

1. Radar Edgen: Visibilidad en tiempo real del mercado

Edgen Radarproporciona una vista en vivo y detallada de las condiciones del mercado actual:

- Destaca las monedas populares basándose en la actividad social en tiempo real y las actividades de la cadena de bloques.

- Rastrea claramente las actividades de la ballena y el monedero inteligente.

- Identifica narrativas impulsadas por KOL que predicen movimientos significativos en el precio.

Sin esta claridad en los datos, los operadores corren el riesgo de tomar decisiones informadas.

2. Búsqueda Edgen: Investigación de Mercado Potenciada por IA en Tiempo Real

Edgen Searchactúa como analista de inteligencia artificial para un operador:

- Responde preguntas relacionadas con el mercado de inmediato con respuestas seleccionadas y respaldadas por datos.

- Filtra el ruido de las redes sociales, entregando insights accionables de manera clara.

- Analiza rápidamente tendencias de múltiples plataformas (X, Telegram, blockchain).

Los operadores dependen de Edgen Search para distinguir las oportunidades reales de alpha de la euforia del mercado efímera.

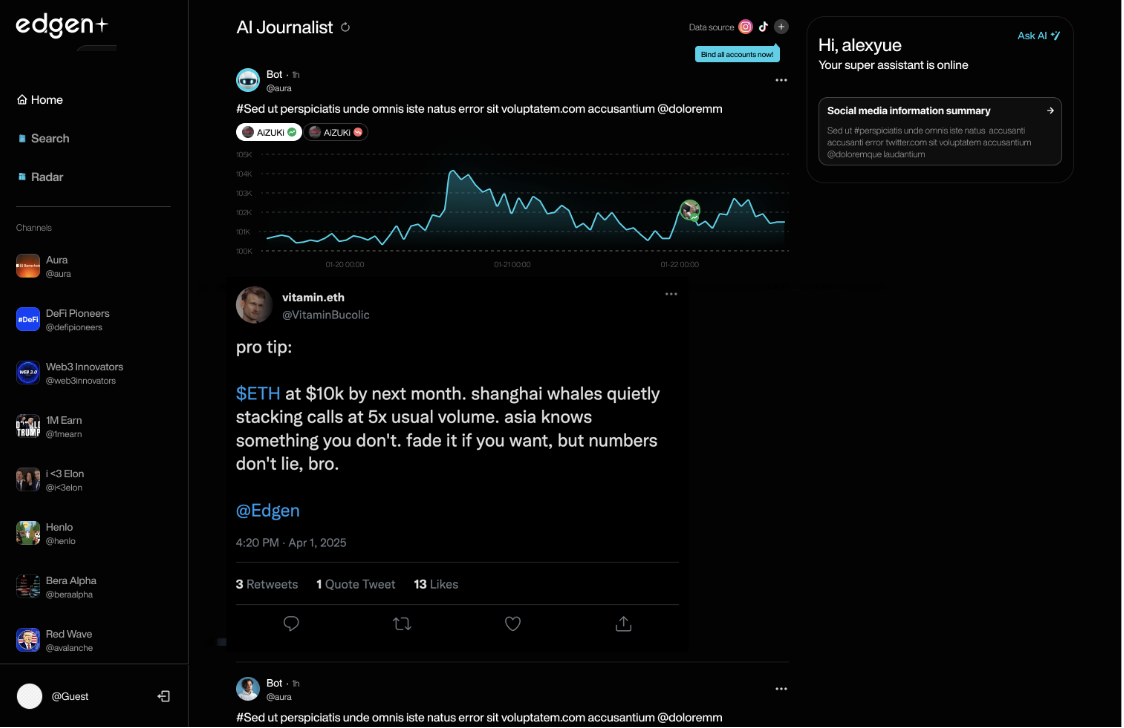

3. Insights de Edgen: Insights de Alpha impulsados por la comunidad

Edgen Insightsconecta a comerciantes, analistas e inteligencia artificial:

- Permite el intercambio en tiempo real de perspectivas alfa entre los operadores.

- Los filtros de moderación de IA detectan desinformación y aclaran los debates.

- Los traders y analistas expertos aportan insights de alta calidad, verificados.

Las Perspectivas fomentan una inteligencia colectiva transparente sin dependencia de una sola autoridad.

Billeteras Inteligentes: Motores de Trading Potenciados por IA

Billeteras inteligentes evolucionaron en herramientas de trading sofisticadas, integrando análisis de blockchain y estrategias impulsadas por inteligencia artificial.

Cómo las billeteras inteligentes mejoran el comercio:

- Monitoreo Inmediato de Blockchain: Detección temprana de señales de alfa antes de que los traders generales las detecten.

- Ejecución Rápida de Comercio: Operaciones automatizadas y instantáneas sin retrasos manuales.

- Prevención de Fraude: La IA detecta claramente transacciones sospechosas, evitando los rug pulls.

- Integración de Edgen AI: Los monederos inteligentes aprovechan las analíticas sociales de Edgen, mejorando la precisión en las operaciones.

Sin carteras inteligentes, los movimientos del mercado ocurren demasiado rápidamente para el trading manual.

KOLs: Influyentes que Definen los Movimientos del Mercado

Líderes de opinión clave tienen una gran influencia sobre el sentimiento del mercado. Sus llamadas, publicaciones y narrativas impactan rápidamente los precios de las criptomonedas.

Cómo los KOLs impulsan el trading con IA:

- Genere "Pumpamentals": el hype social impulsado por KOLs impacta directamente en la valoración de los activos.

- Ofrecer Oportunidades Alpha: El conocimiento de insiders proporciona puntos de entrada tempranos en operaciones rentables.

- Influencia del Sentimiento Claramente: La optimismo o pesimismo de los KOLs influye significativamente en la dirección del mercado.

Ignorar las señales sociales impulsadas por KOL limita en gran medida la efectividad del trading. Edgen AI escanea instantáneamente las actividades, discusiones y tendencias de sentimiento de los KOL, predeciendo las reacciones del mercado con anticipación.

La Revolución del Comercio con IA Ha Llegado

El trading con IA se transformó de una posibilidad futura en una necesidad actual.

Billeteras inteligentes, KOLs influyentes y las analíticas de vanguardia de Edgen AI definen una nueva era de trading, en la que la inteligencia del mercado combina perspectivas sociales y transparencia blockchain.

Los comerciantes que prosperan en esta era impulsada por la inteligencia artificial deben:

- Utiliza billeteras inteligentes impulsadas por IA para una ejecución rápida y precisa.

- Aprovecha Edgen AI para seguir claramente los "pumpamentals" impulsados por las redes sociales.

- Sigue las opiniones de KOL pero válalas utilizando análisis de blockchain.

- Monitorear constantemente las señales alfa para anticipar movimientos del mercado.

Los mercados cambian rápidamente. El siguiente movimiento significativo en el precio ya está en marcha.

¿Estás listo para operar antes que la multitud? PruebaEdgen AI¡Hoy!

Invertir, por fin, ya no es cosa de uno solo.

Prueba Ed gratis. Sin tarjeta, sin compromiso.