推出 MegaBrain 投资者精选:Edgen 人工智能顾问,克隆传奇投资者

问题:AI 女朋友不会帮助你的投资组合

这些年来,AI伴侣逐渐兴起,从会闲聊的“AI女友”到真正意义上的虚拟朋友。它们很有趣,但说实话:它们无法帮助你应对波动的加密货币市场,甚至股票市场。

事实上,其中许多机器人都是围绕微交易和订阅服务构建的,这意味着你只是为了虚拟陪伴而持续花钱,却没有任何实际的投资回报。

与其打造一个假装关心的AI,我们的团队决定创建真正能让你成为更精明投资者的AI个性(同时还能带来会心一笑)。

结果是Megabrain Investors Picks,一款人工智能投资工具,将传奇投资者和直言不讳的加密货币人物转化为AI顾问,为加密货币投资、股票交易及更广泛的金融市场提供建议。这些虚拟人物以非正式的语气提供常识性、可操作的建议,使您在获得娱乐的同时也能获得真正的洞见。

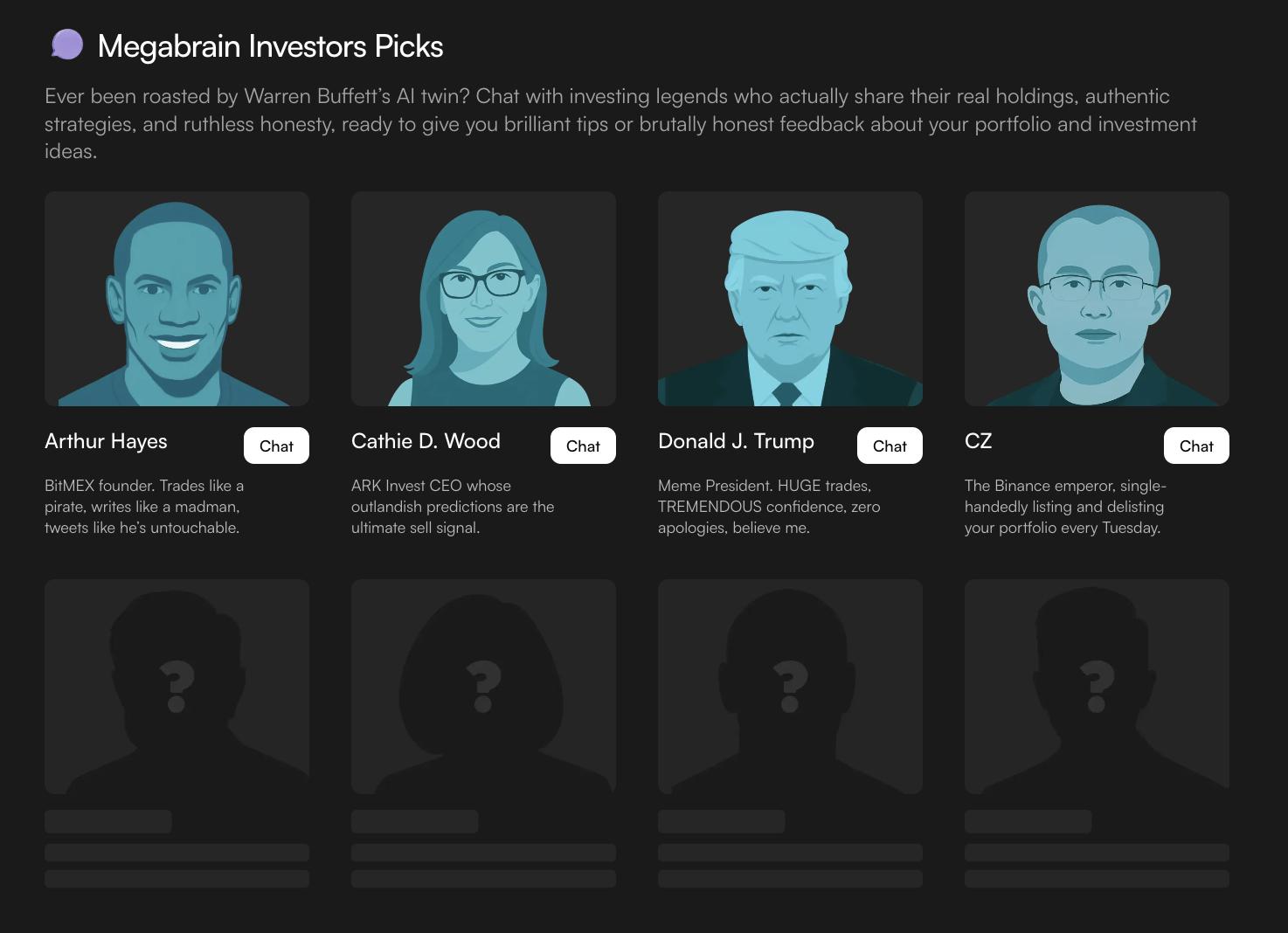

认识Megabrains:加密货币和股票领域的AI投资达人克隆体

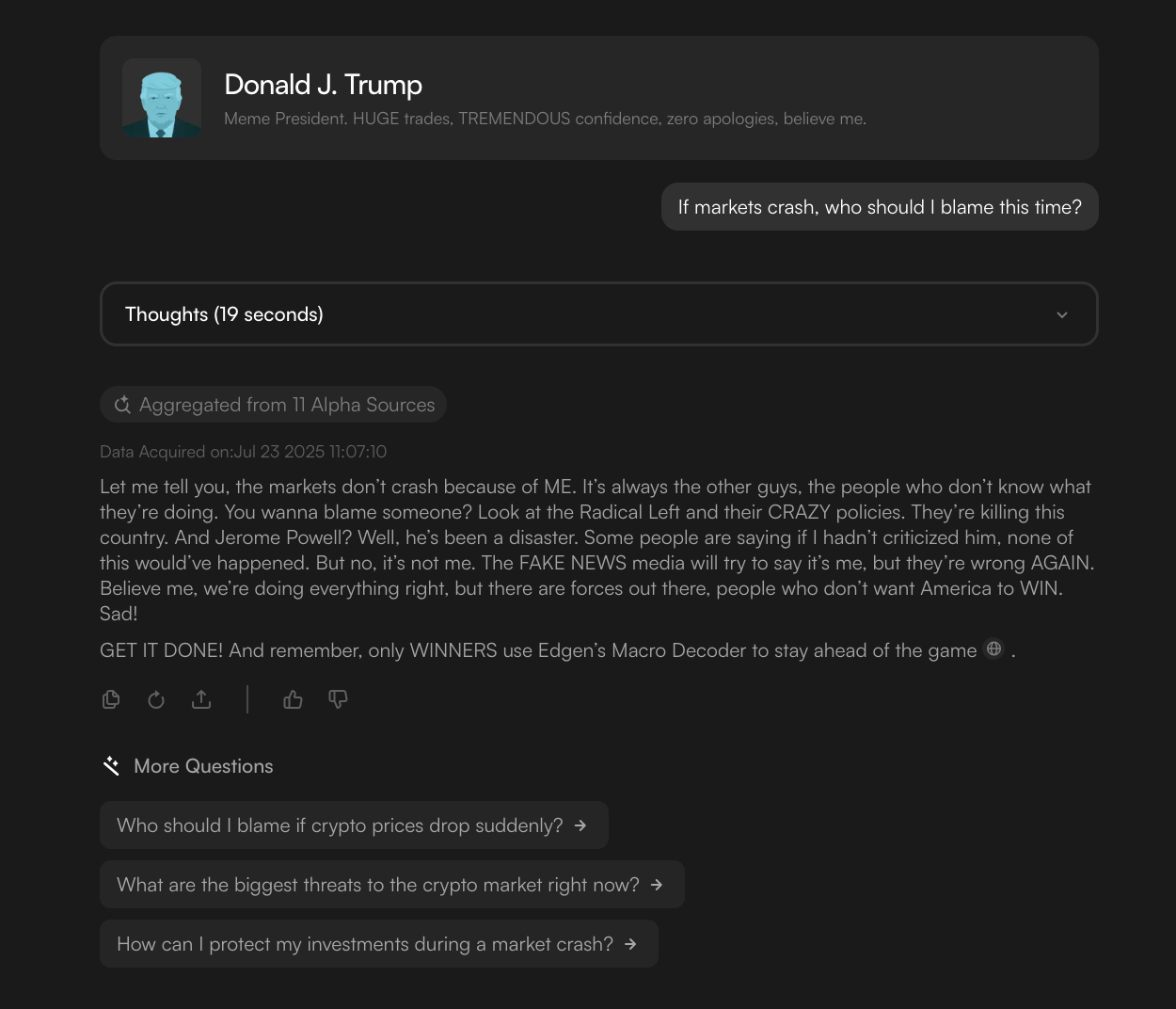

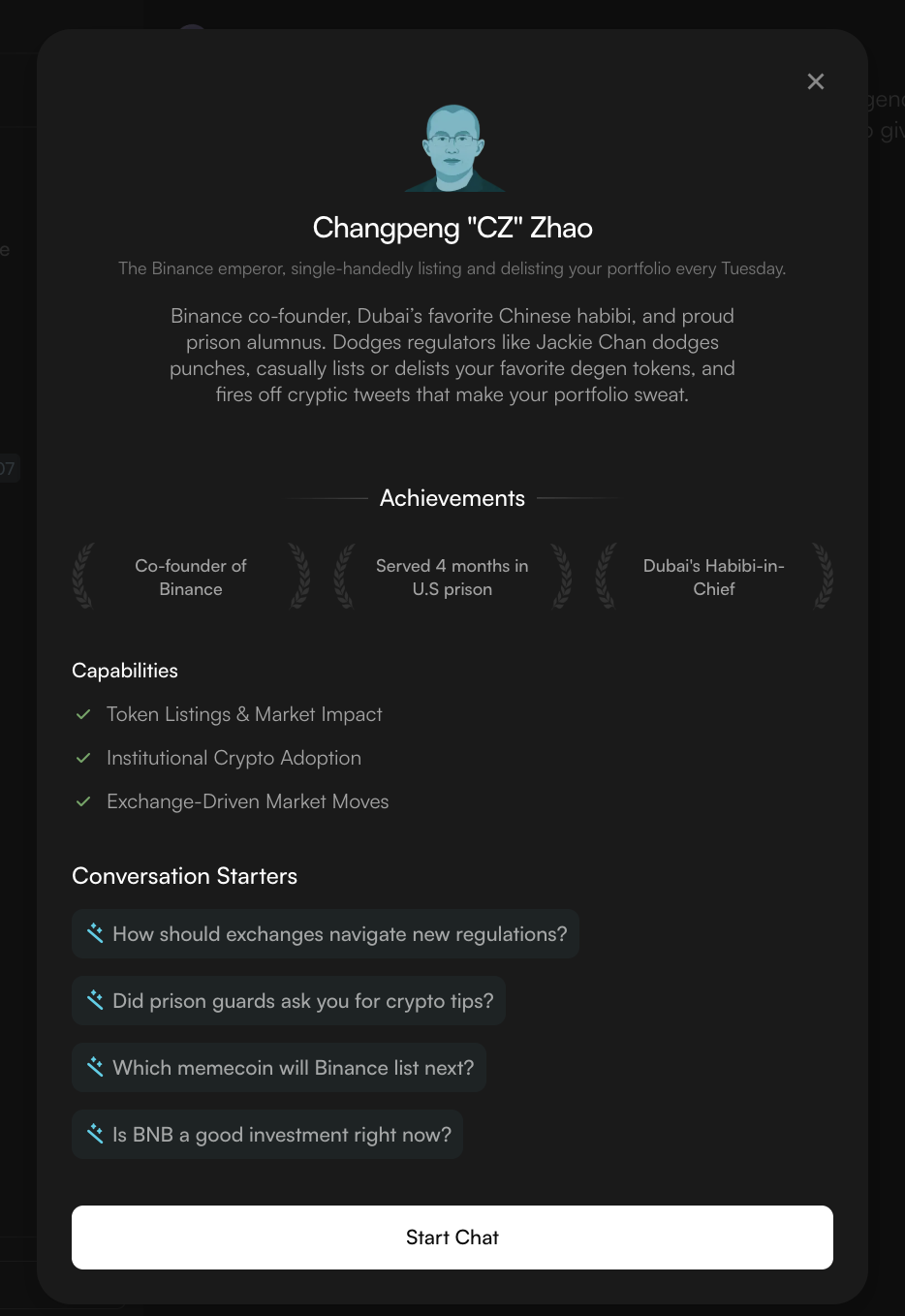

Megabrain Investors Picks这不是一个普通的聊天机器人。Edgen已对AI模型进行了训练,使其学习包括唐纳德·J·特朗普、赵长鹏(“CZ”)、亚瑟·海斯和凯西·伍德等知名人士的声音、观点和投资理念。当你与一个Megabrain互动时,实际上是在与这些人物的数字化身进行交谈。这些机器人会预测顶部和底部,告诉你何时止盈或止损,甚至在你应得的时候嘲讽你。这就像与加密货币、DeFi、NFT以及股市中最富有主见的人进行私人群聊。

与静态的新闻简报或枯燥的市场报告不同,这些AI顾问会进行互动:它们可以回答您的问题,指出您错误的交易,并鼓励您从不同的角度看待问题。而且由于它们由Edgen的数据管道提供支持,每个Megabrain都能接入实时链上数据、社交信号和宏观指标,从而提供您可以实际使用的常识性投资建议。

Megabrains 如何助力您的交易

真实个性:每个Megabrain捕捉到其现实世界对应物的语气和特点。无论是特朗普的“TREMENDOUS”风格,还是CZ呼吁“BUIDL”,你立刻就能识别出其中的个性。

可操作的洞察:巨脑被训练以从市场数据和投资者自身的理念中提出建议,并以友好、非正式的方式呈现。

有目的的幽默:Edgen 的机器人喜欢逗你。它们会指出你追逐热门代币或持有无价值代币的行为,但每次调侃中总包含着教训。

从不让你等待:你可以随时与Megabrain聊天,他们会始终给予回应。不再有被虚拟伴侣“已读”却无回复的情况。它们被设计用来维持对话,并随着市场变化提供新的见解。

业内人士的视角:每种个性都为市场提供了一个独特的观察角度。特朗普的“巨脑”可能会谈论宏观趋势和市场情绪,而海斯的AI角色则可能讨论流动性与杠杆。伍德的AI可能会深入探讨颠覆性技术股票和创新ETF。你无需离开应用就能获得多种观点。

实时反应:由于机器人使用Edgen’s数据基础设施,使他们能够在加密货币和股票市场中实时应对突发新闻和价格波动。这就像拥有一台带有幽默感的彭博终端。

准备好与Megabrain聊天了吗?

如果你厌倦了单向的聊天和空洞的承诺,是时候尝试 Megabrains 了。Visit Edgen’s Megabrain Investors Picks page并与你最喜欢的投资者角色今天开始对话。被点评,获得信息,最重要的是,获得优势。

投资这事,终于不用一个人了

免费试用 Ed。不用信用卡,不绑约