AI를 활용하여 더 스마트한 암호화폐 투자하는 방법

AI를 활용하여 더 스마트한 암호화폐 투자하는 방법

∙ SEO 제목: AI를 활용하여 Edgen AI로 더 스마트한 암호화폐 투자하는 방법

∙ 설명: Edgen AI가 온체인 분석, 예측 신호 및 포트폴리오 인텔리전스를 결합하여 암호화폐 투자자들이 더 빠르고 데이터 기반의 결정을 내릴 수 있도록 돕는 방법을 알아보세요.

∙ 태그 키워드: Edgen AI, 암호화폐 투자, 블록체인 분석, AI 투자 코파일럿, 온체인 인텔리전스, 예측 신호, 포트폴리오 최적화, 알파 발굴, 시장 예측

지능형 암호화폐 투자의 미래

암호화폐 시장에서의 성공은 타이밍, 데이터, 그리고 명확성에 달려 있습니다. 가격은 몇 초 만에 변동하고, 심리는 하룻밤 사이에 바뀌며, 기회는 나타나는 만큼 빠르게 사라집니다. 앞서 나가는 투자자들은 시장이 반응하기 전에 이해하는 사람들입니다.

Edgen은 바로 이러한 목적을 위해 만들어졌습니다. AI 분석, 블록체인 데이터, 소셜 인텔리전스를 하나의 적응형 시스템으로 통합합니다. 기술 신호(Technical Signals), Pre-TGE 탐지기(Pre-TGE Detector), 트레이딩 마인드셰어(Trading Mindshare)와 같은 에이전트를 통해 시장의 노이즈를 구조화된 통찰력으로 변환합니다.

이 가이드는 Edgen의 생태계를 사용하여 더 날카로운 결정을 내리고, 변동성을 관리하며, 디지털 자산 전반의 기회를 발굴하는 방법을 설명합니다.

II. Edgen 생태계 이해하기

1. Edgen은 무엇이 다른가요?

Edgen AI는 머신러닝, 블록체인 투명성, 행동 데이터를 융합하여 투자자들에게 시장에 대한 완전한 그림을 제공합니다. 통합 시스템은 다음을 제공합니다:

- 실시간 시장 통찰력

- 알파 신호 생성

- 예측 위험 분석

- 시장 심리 추적

- 포트폴리오 최적화 도구

모든 모듈은 Edgen 앱 내에서 동기화되어 작동하므로 업데이트가 기기 전반에 걸쳐 일관되게 유지됩니다.

2. AI를 활용하여 더 스마트한 결정 내리기

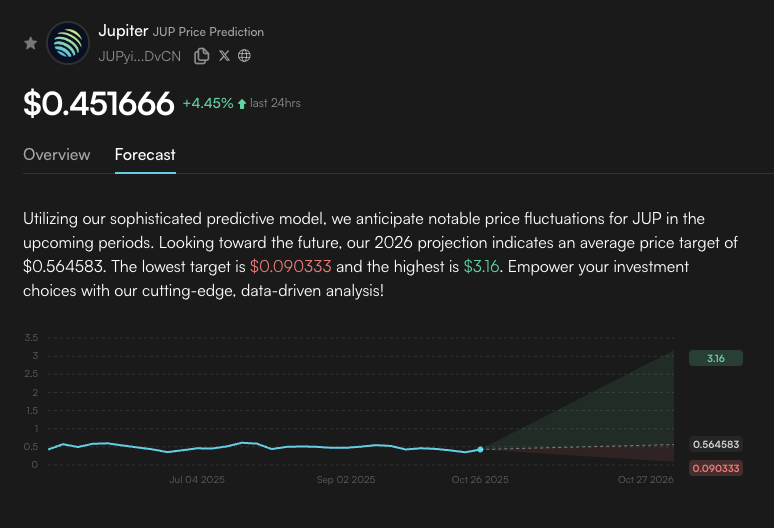

Edgen의 알고리즘은 비효율성이 가시화되기 전에 이를 감지합니다. 360° 보고서는 기술 및 기본 지표를 집계하여 실시간으로 예측 및 추세 분석을 생성합니다.

신규 사용자를 위해 Edgen의 학습 센터는 예측 도구를 일상적인 워크플로에 통합하기 위한 명확한 시작 경로를 제공합니다.

3. 온체인 분석 및 시장 신호 통합

Edgen의 온체인 스나이퍼(On-Chain Sniper)는 블록체인 활동을 모니터링하여 고래 움직임과 초기 축적 추세를 식별합니다. 알파 신호와 결합하여 거래 데이터를 실행 가능한 진입 및 청산 지점으로 변환합니다.

Pre-TGE 탐지기는 다가오는 토큰 출시를 강조하여 사용자가 더 넓은 시장 인식이 확산되기 전에 일찍 포지션을 잡을 수 있도록 돕습니다.

4. 변동성 조건에서 위험 관리

암호화폐의 변동성은 기회이자 위험입니다. Edgen의 위험 관리 스위트(Risk Management Suite)를 통해 사용자는 가격 하락 또는 심리 반전을 위한 맞춤형 경고 및 자동화 규칙을 설정할 수 있습니다.

최근 시장 변동성 동안 이 시스템은 갑작스러운 변동 전에 트레이더가 이익을 확보하거나 노출을 줄이는 데 도움이 되는 실시간 경고를 제공했습니다.

III. 시장 인식을 재정의하는 고급 기능

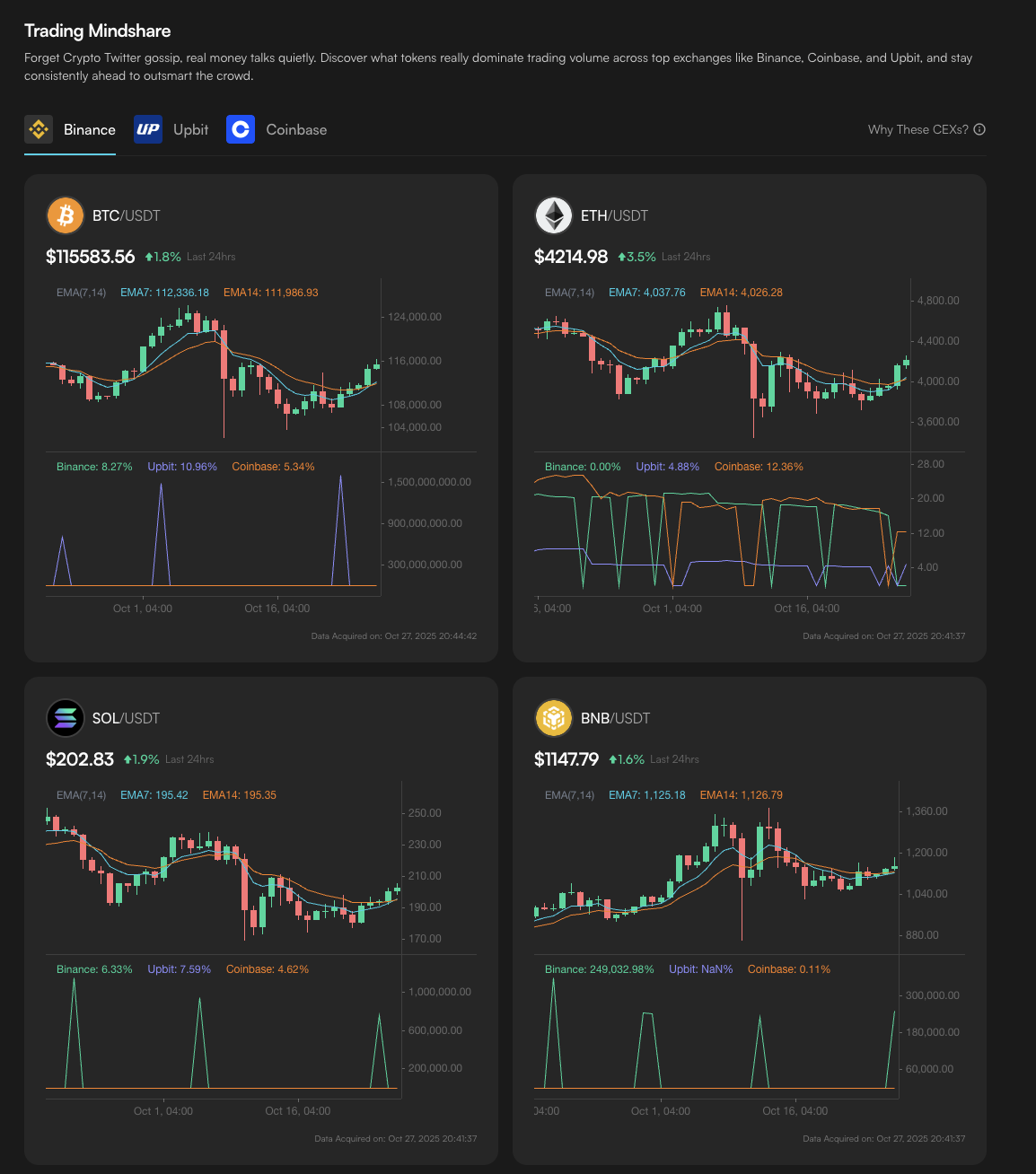

1. 트레이딩 마인드셰어

이 에이전트는 주요 거래소의 데이터를 분석하여 유동성 흐름을 측정합니다. 커뮤니티 분위기와 관심 수준의 변화를 해석하여 소셜 심리를 넘어 구체적인 시장 분위기를 조기에 측정할 수 있도록 합니다.

2. 기술 신호

Edgen은 머신러닝을 통해 RSI, MACD, 볼린저 밴드와 같은 지표를 평가합니다. 각 출력은 신뢰성을 보장하기 위해 과거 시장 행동과 비교하여 검증됩니다.

3. 포트폴리오 진단

360° 보고서는 보유 자산, 심리 지표 및 온체인 포지셔닝을 지속적인 성과 요약으로 통합합니다. 피벗 알림(Pivot Alert)과 결합하여 조기 경고 및 재조정 권장 사항을 통해 사전 예방적인 포트폴리오 관리를 가능하게 합니다.

IV. 통합 뉴스로 정보 얻기

Edgen은 여러 시장 소스에서 검증된 업데이트를 집계합니다.

사용자는 다음을 팔로우할 수 있습니다:

- 비트코인 및 이더리움 네트워크 분석

- DeFi 부문 보고서 및 토큰 흐름

- NFT 시장 동향

- 디지털 자산에 영향을 미치는 규제 및 거시 경제 변화

이 스트림은 의사 결정이 정확하고 최신 컨텍스트에 기반하도록 보장합니다.

V. 지능형 투자 루틴 구축

Edgen의 강점은 시장 인텔리전스의 모든 계층을 단일 피드백 루프로 연결하는 데 있습니다.

- 온체인 분석은 대규모 보유자들이 무엇을 하고 있는지 보여줍니다.

- 기술 신호는 추세가 강화되거나 약화되는 지점을 나타냅니다.

- 심리 데이터는 내러티브가 어떻게 진화하는지 설명합니다。

- 포트폴리오 진단은 이 모든 것을 명확한 권장 사항으로 변환합니다.

Edgen을 더 일관되게 사용할수록, 모델은 사용자의 투자 습관에 더 빠르게 적응하여 개인 전략에 맞게 경고와 예측을 정교하게 조정합니다.

VI. Edgen으로 시장을 마스터하세요

데이터는 거래에서 가장 가치 있는 자산입니다. Edgen AI는 투자자들에게 이러한 데이터를 정밀하고 자신감 있게 해석할 수 있는 능력을 제공합니다.

예측 분석, 알파 발굴 및 위험 통제를 통해 정보를 전략적 이점으로 전환합니다.

지금 Edgen AI를 사용해 보세요. 지능, 명확성, 타이밍이 암호화폐 투자 여정의 다음 단계를 어떻게 정의할 수 있는지 탐색해 보세요。

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.