もうこの「道化師のような」市場にはついていけない。だから Edgen を作った。

私はプロのライターではありません。正直な話、私がこの文章を書くべきかどうかさえ確信がありません。しかし、エッジンを構築した理由を自分自身からあなたに伝えたいと思いました。なぜなら、それは私にとって非常に意味のあることだからです。

おそらくあなたと同じ理由で暗号通貨に興味を持ったのですdid:私は自由を求めていました。成功する機会が欲しかったのです。正直に言いますが、お金を稼ぎたかったことも事実です。それには何の問題もありません。

私は暗号通貨の取引をしています。年今、私はこの分野に初めてというわけではありませんし、そこで多くの楽しみを味わってきました。私はエベレスト・ベンチャーズ・グループ(EVG)で働き続けており、有望なDeFiおよび...SocialFiアジアでのプロジェクトに取り組み、上昇相場と下落相場を乗り越え、私が考えるプロフェッショナルなネットワークを構築しました。結構いいですほとんどの基準において、私はそう言うでしょう。かなりつながりがある(非常に人脈がある)空間において、私は正直に言える。

しかし最近、私も圧倒される気持ちを感じ始めました。数年間を通じて、暗号通貨の取引が見えるほど簡単ではないことを学びました。これはバブル市場(それらは)でも同様です。実際に「クラウン」暗号通貨の市場において。もしもあなたが3時半にポートフォリオを確認して、自分が正しいことは分かっているのに、またもや遅すぎたと気付くような面倒な経験をしたことがあるなら、私が話していることがまさに分かるだろう。

今日、暗号通貨はこれまでよりもずっと早く動いている。あまりにも速すぎる。ウェイジーしすぎている。毎日何百ものトークンが出現している。メモコインそれが1時間で100倍になること、一夜にして物語が変わること、私が聞いたこともないクジラのウォレットにある隠れたシグナル…その騒音は止まない。どれほど経験があって、どれほど良いリサーチやネットワークを持っていても、追いつくことはただ不可能だ。

良いエントリーや機会を逃してしまい、常に遅れを取っている感じでした。私のリソースや関係性を持っていても、先んじようとするのは本当に気力が尽きるほど疲れます。そして私は特に悪いトレーダーだとは思っていません。

今では結婚して子供もいる。年を取った感じがして疲れてしまう。そして、広範な人脈と豊富な経験を持つような私ですらこのように圧倒されているのだから、普通で控えめな、初めてのトレーダーにとってはさらにそうだろうと知っている。しなければならないそれをより強く感じ、ときにはドラマティックな結果をもたらすこともある。

暗号通貨は、ゴールデンチケットであり、競争の場を平等にするものとされていました。誰であっても、最初に持っていたお金がいくらであっても、公平な機会を与えるものとされていました。しかし、今私たちが生きている現実はどうでしょうか?まったく公平とは感じられません。不正であるように感じます。だから私は、それを変えるために何かを作らなければならないと決めました。

私はエッジンを「小さな個人」のために作った(なぜなら私自身がそうだから)ちょっと(少し)アム・ワン)

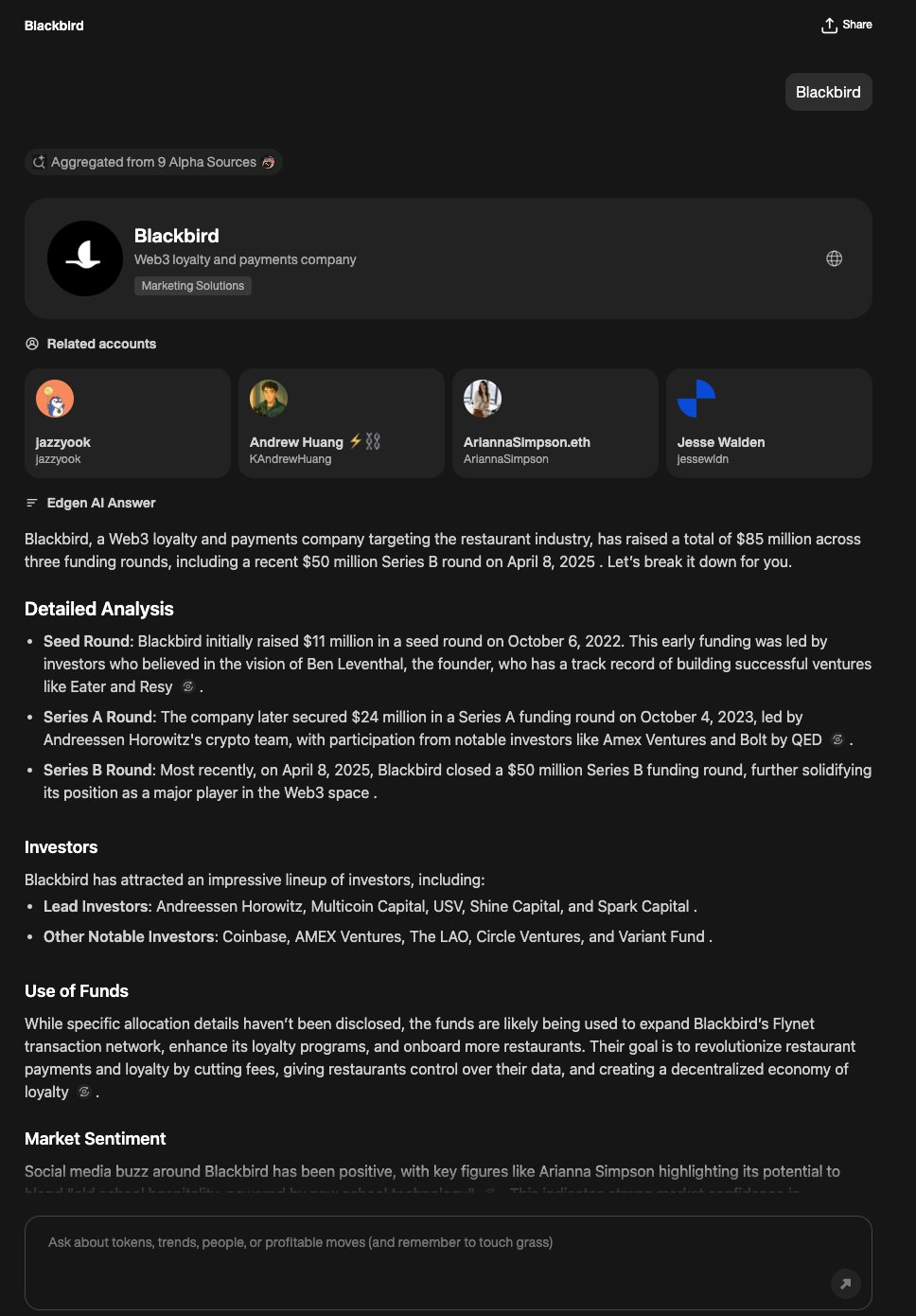

エッジンは、私が狂いそうになるのを防ぐために本当に必要なものでした。私は、暗号通貨のあらゆる領域、コインテレグラム、スマートウォレット、ブロックチェーン上のシグナル、開発者活動、最近のベンチャーキャピタルから即座に集約された集団知を収集できるツールを望んでいました。資金調達を行い、それを私に明確かつ迅速に届けます。

私が本当に重要なことを、それがあまりに遅くなる前に知らせてくれるような、shitpostsやrug(※)を濾し取る何か。

※「rug」は文脈によって意味が異なる可能性がありますが、ここでは「無駄な情報や不要な物」として解釈しています。もしこの単語に特定の意味がある場合は、追加情報を教えてください。

だから私たちは誰もが使いやすいように設計されたAIを活用したマーケットインテリジェンスプラットフォームを構築しましたが、それ以上に賢く、高度な分析が可能です。実際に役立つ私はあなたがすべての取引で利益を上げることを保証することはできません。誰もそのようなことを約束することはできませんし、そう言う者はあなたをだましているのです。しかし、私が約束できるのは、あなたが二度と盲目に取引することはないということです。

だから我々はまず2つのシンプルで強力なツールから始めます。膨大な時間をかけて蓄積・精査を重ねた独自のソーシャルおよびマーケットデータのおかげで、エッジンの目的に合わせて設計されたAIは、ブルーチップトークンの調査であれ、新規トークンの分析であれ、鋭いインサイトを提供する点において他を凌駕しています。メモコインズ、影響力のある市場参加者、または最新の資金調達取引。

エッジン検索:

持っているあらゆる暗号通貨に関する質問(複雑な質問でも簡単な質問でも)、リアルタイムデータから即座で実行可能なインサイトを得られます。もう深夜に不安になって情報を読み続けることはありません。私たちがカスタムで訓練したLLMは、正確さを保ちながらノイズを切り抜き、暗号通貨全体の市場においてシグナルや機会を瞬時に浮き彫りにします。それだけでなく、株式市場にも及んでいます。

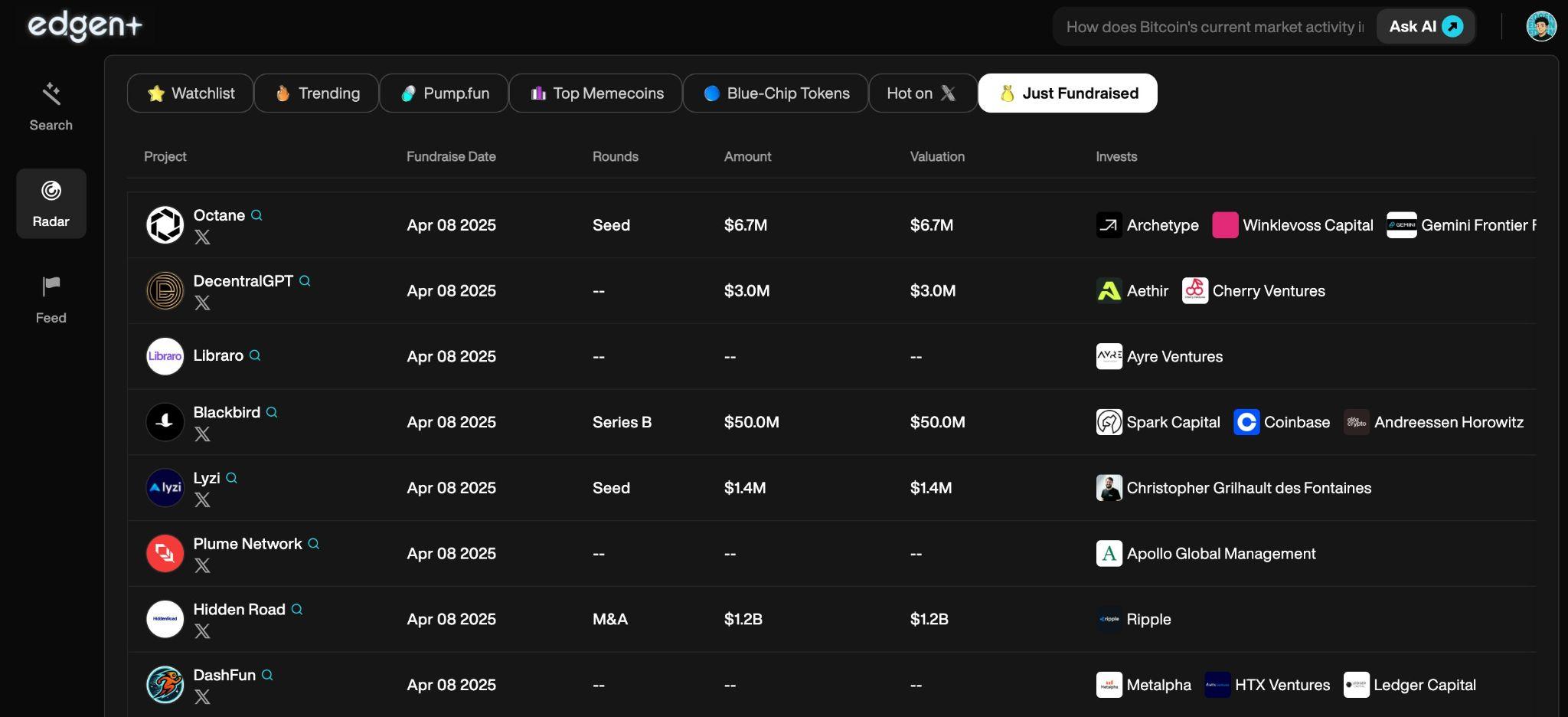

エッジン・ラダーリー:

レーダーをあなたの個人用スカウティングダッシュボードとして。それは常に様々なトークン、ブルーチップなどを継続的にスキャンします。pump.fun卒業生、ムーンショットトークン、トレンドトークン、などそして、スマートウォレットの購入や売却、コミュニティの人気、または主要なインフルエンサーがトークンをフォローすることで静かに注目対象を変えるなどの興味深い出来事が起こり始めると、あなたにアラートを通知します。

「検索から始めましょう!」と伝えてください。あなたが持つ最も馬鹿げた暗号通貨に関する質問を聞いてください。得られる答えはどちらかというと正直すぎるか、あるいは全く笑えるものになります 😂

今後、フィードや特にオーラ(Aura)など、もっとツールをリリースする予定ですが、それはまた別の話になります。ただ、ここでは少し紹介しておきます。

オーラ:本当に信頼できる人を特定する

ここであなたを止めておきます:Auraはトークンではありません。信頼システムです。しかし、ほぼ同じものだと言えます。なぜなら、この経済では信頼が通貨だからです。AuraはあなたのProof-of-Alphaスコアです。

エッジンコミュニティの誰かがツイッターで、正確な市場予測、新興トレンドの発見、または正しいと証明された予測などの価値ある洞察を共有するたびに、彼らはオーラを収穫し、エッジンのAIを日々より賢くしていきます。時間が経つにつれて、オーラは誰が信頼できるか、常に本物のアルファを提供しているか、そして誰に注意を払うべきかを正確に示します。

言い換えれば、Edgenはあなたが理解するのを助けます何が起こっているのかしかし、理解することもする誰を信頼すべきかこの騒がしい市場において。

我々が以前から蓄積してきたエッジンを他のLLMと異なるものにするための特許的で独自のデータに加え、Auraによって、他では再現不可能な方法で、専門的で目的別に構築された我々のLLMは日々より知能が高まっていくことになるでしょう。

私が始めた旅の中で知っている人もいるでしょう。OpenSocialエッジンは実際に、aから大幅なアップグレードOpenSocial、同じコアビジョンに基づいています:社会的資本と影響力に実際で測定可能な価値と本物の所有権を提供すること。Edgenでは、このミッションをさらに進めて、ソーシャルインサイトや集団知を明確で実行可能な市場アルファへと変換しています。それこそがすべてです。OpenSocial「あるべきもの」であり、それ以上であることを目指している。今日の市場を考慮すると、それは自然な進化である。

エッジンはグレート・マーケット・イコライザーである

私は、暗号通貨が内部者や常にオンラインである人々だけに利益をもたらすものであってはならないと考えて、Edgenを構築しました。もちろん、誰も常に収入を得られるわけではありません。それは現実的ではありません。しかし、適切な情報が明確かつ迅速に提供されれば、誰もが収入を得るための公平な機会を持つことができます。

私の夢は、Edgenが暗号通貨取引における大きな平等化要因となることである。私たちが適切な仕事をすれば、世界中でさまざまな背景を持つ一般のトレーダーは、常に遅れをとっていると感じることなくなります。

では、私の話はこれです。私はウォールストリートのバックグラウンドを持つ豪華なトレーダーではありませんし、私には…確かにしなかったこれを完璧に書いてください。私はただの、好きなことを愛する男です。暗号通貨、およびもっと良いものを望んでいた。

だから、私がエッジンを構築した本当の理由です。私自身が必要だったからです。そして、これがあなたにとっても役立つと考えています。

試していただいたことに感謝します。

シーン・タオ、エッジン社の共同創設者

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし