Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

Summary

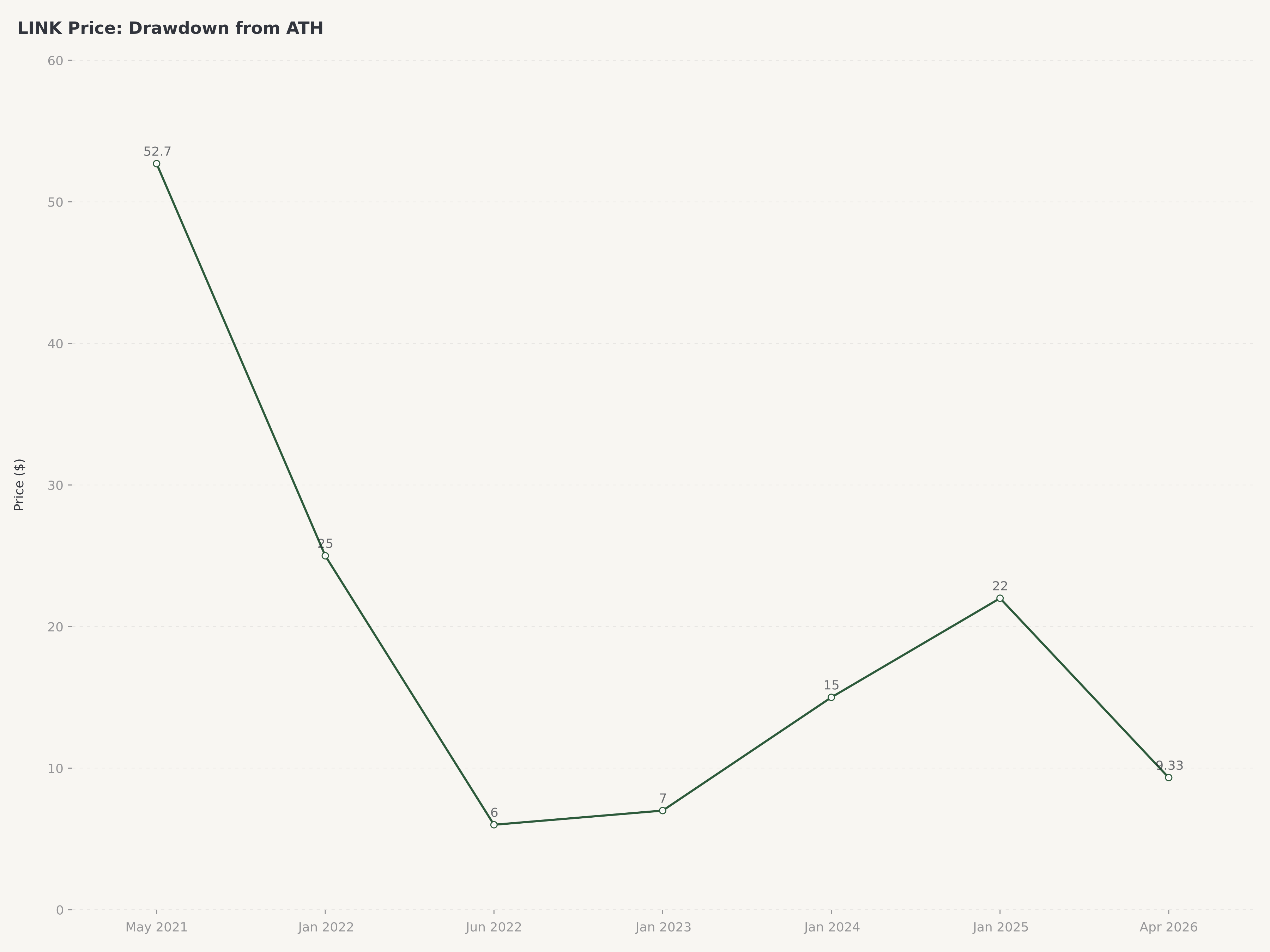

- Chainlink trades at $9.33 with a market capitalization of $6.78 billion and a fully diluted valuation of $9.33 billion, representing an 82% drawdown from its all-time high of $52.70 — a dislocation that prices the dominant oracle network as if its enterprise partnerships and cross-chain infrastructure are worth zero.

- The Cross-Chain Interoperability Protocol (CCIP) is live across 30+ blockchain networks and has been adopted by Swift, DTCC, and major global banks for tokenized asset settlement trials, positioning Chainlink as the default middleware layer for the estimated $16 trillion real-world asset tokenization opportunity over the next decade.

- The Chainlink Runtime Environment (CRE), launched in 2025, transforms the network from a single-purpose oracle into a full-stack Web3 services platform — combining data feeds, automation, verifiable randomness, and cross-chain messaging into a unified developer toolkit that deepens protocol lock-in.

- We rate LINK Buy with a $16 price target (~71% upside), supported by the network's ~$150 million in annualized on-chain fees, stable daily active usage averaging ~30 days of consistent engagement, growing staking participation, and an institutional pipeline that no competitor — not Pyth, not Band Protocol, not API3 — can replicate at scale.

The Oracle Problem in 2026: Why Smart Contracts Still Cannot See the Real World

The most important limitation of blockchain technology has not changed since Ethereum launched in 2015: smart contracts cannot access off-chain data on their own. A lending protocol needs real-time price feeds to calculate collateral ratios. A derivatives exchange needs settlement prices from traditional markets. An insurance contract needs weather data to trigger payouts. Every one of these functions requires an oracle — a mechanism for delivering real-world data to on-chain applications in a tamper-resistant, reliable manner. Sergey Nazarov, Chainlink's co-founder, has spent nearly a decade arguing that this problem is not a feature gap but the central bottleneck preventing blockchain adoption by institutions. In 2026, the evidence increasingly supports his thesis.

The macro backdrop for oracle infrastructure is defined by two converging forces. First, the tokenization of real-world assets (RWA) has moved from proof-of-concept to production deployment. BlackRock's BUIDL tokenized money market fund manages billions in on-chain assets. Franklin Templeton, JPMorgan, and Goldman Sachs have active tokenization programs. The Boston Consulting Group estimates the tokenized asset market could reach $16 trillion by 2030. Every single one of these tokenized assets requires price feeds, proof of reserves, and cross-chain settlement capabilities — precisely the services Chainlink provides. Second, the multi-chain reality of Web3 means that assets, liquidity, and users are fragmented across Ethereum, Solana, Avalanche, Polygon, Arbitrum, Base, and dozens of other networks. Moving value and data between these chains securely is an infrastructure problem that CCIP was purpose-built to solve.

The DeFi ecosystem that Chainlink services has matured considerably. Total value locked across all protocols exceeds $100 billion. Lending protocols like Aave, derivatives platforms like GMX and dYdX, and stablecoin systems like MakerDAO all depend on Chainlink price feeds for their core operations. This dependency is not theoretical — when Chainlink's ETH/USD feed updates, billions of dollars in liquidation thresholds shift. The network processes millions of on-chain transactions annually, generating fees that flow to node operators and, increasingly, to LINK stakers. In a crypto industry that has struggled to find sustainable revenue models, Chainlink's fee-generating infrastructure business stands out.

From Oracle Network to "Internet of Contracts": Chainlink's Strategic Evolution

Chainlink launched in 2017 with a focused value proposition: decentralized price feeds for smart contracts. Nazarov and co-founder Steve Ellis recognized that the oracle problem — how to get reliable off-chain data on-chain — would become the primary bottleneck as blockchain applications grew in complexity and economic value. The initial product, Chainlink Data Feeds, provided tamper-resistant price data by aggregating inputs from multiple independent node operators, each staking LINK tokens as collateral against dishonest behavior. This architecture solved the single-point-of-failure problem that plagued earlier oracle designs and quickly became the industry standard.

The network's evolution from single-purpose oracle to full-stack Web3 infrastructure platform represents one of the most ambitious product expansions in cryptocurrency. Chainlink Automation (formerly Keepers) enables smart contracts to trigger actions based on predefined conditions — a capability that powers liquidation bots, rebasing mechanisms, and yield harvesting strategies across DeFi. Chainlink VRF (Verifiable Random Function) provides provably fair randomness for gaming, NFT mints, and lottery applications. Chainlink Functions allows developers to connect smart contracts to any external API, extending the network's data reach far beyond financial price feeds.

The two products that define Chainlink's next chapter are CCIP and CRE. The Cross-Chain Interoperability Protocol, launched in 2023 and expanded aggressively through 2025-2026, enables secure token transfers and arbitrary messaging between blockchain networks. Unlike third-party bridges — whose vulnerabilities have resulted in billions of dollars in exploits including the Ronin Bridge ($625 million), Wormhole ($325 million), and most recently the Kelp DAO incident — CCIP leverages Chainlink's existing decentralized oracle network as a security layer, with an additional Risk Management Network that independently verifies every cross-chain transaction. Swift's adoption of CCIP for cross-chain settlement experiments with major banks is not a marketing partnership; it is a technical integration that positions Chainlink as the connective tissue between traditional finance and on-chain infrastructure.

The Chainlink Runtime Environment, announced and deployed in 2025, bundles all of these services — data feeds, automation, VRF, functions, and CCIP — into a unified developer platform. Nazarov has described CRE as enabling the "Internet of Contracts," where smart contracts on any chain can access any data, trigger any action, and communicate with any other chain through a single integration point. The strategic logic is clear: by becoming the default runtime environment for Web3 applications, Chainlink creates switching costs that rival those of AWS in cloud computing. A protocol that integrates Chainlink Data Feeds, Automation, and CCIP simultaneously faces enormous friction in migrating to an alternative provider, even if that provider offers cheaper oracle services for a single function.

On-Chain Performance: Fees, Usage, and Network Metrics

Chainlink's on-chain economics in April 2026 reflect a network that has achieved product-market fit but trades at a valuation that implies no growth. The network generates approximately $150 million in annualized on-chain fees, derived from payments by protocols and applications that consume Chainlink services. These fees are paid in LINK tokens, creating organic demand that is independent of speculative trading activity. Node operators — the decentralized network of entities that run Chainlink infrastructure — earn these fees in exchange for providing data feeds, executing automation tasks, generating verifiable randomness, and facilitating cross-chain messages.

Daily active usage has remained stable over the trailing 30-day average, indicating consistent protocol-level demand rather than the boom-bust cycles that characterize speculative tokens. The network secures value across more than 30 blockchain networks, with Ethereum, Arbitrum, Polygon, Avalanche, Optimism, Base, and BNB Chain representing the largest deployments. Over 1,900 projects have integrated Chainlink services, including the majority of top-50 DeFi protocols by TVL. This breadth of integration is Chainlink's most powerful moat: the network effect of having thousands of applications dependent on Chainlink data creates a self-reinforcing adoption cycle that no competitor has been able to replicate.

Metric | Value | Context |

Price | $9.33 | -82% from ATH $52.70 |

Market Cap | $6.78B | Based on ~727M circulating LINK |

Fully Diluted Valuation | $9.33B | 1B total supply x $9.33 |

Annualized On-Chain Fees | ~$150M | Node operator revenue from services |

Supported Networks | 30+ | Multi-chain deployment |

Integrated Projects | 1,900+ | DeFi, NFT, gaming, enterprise |

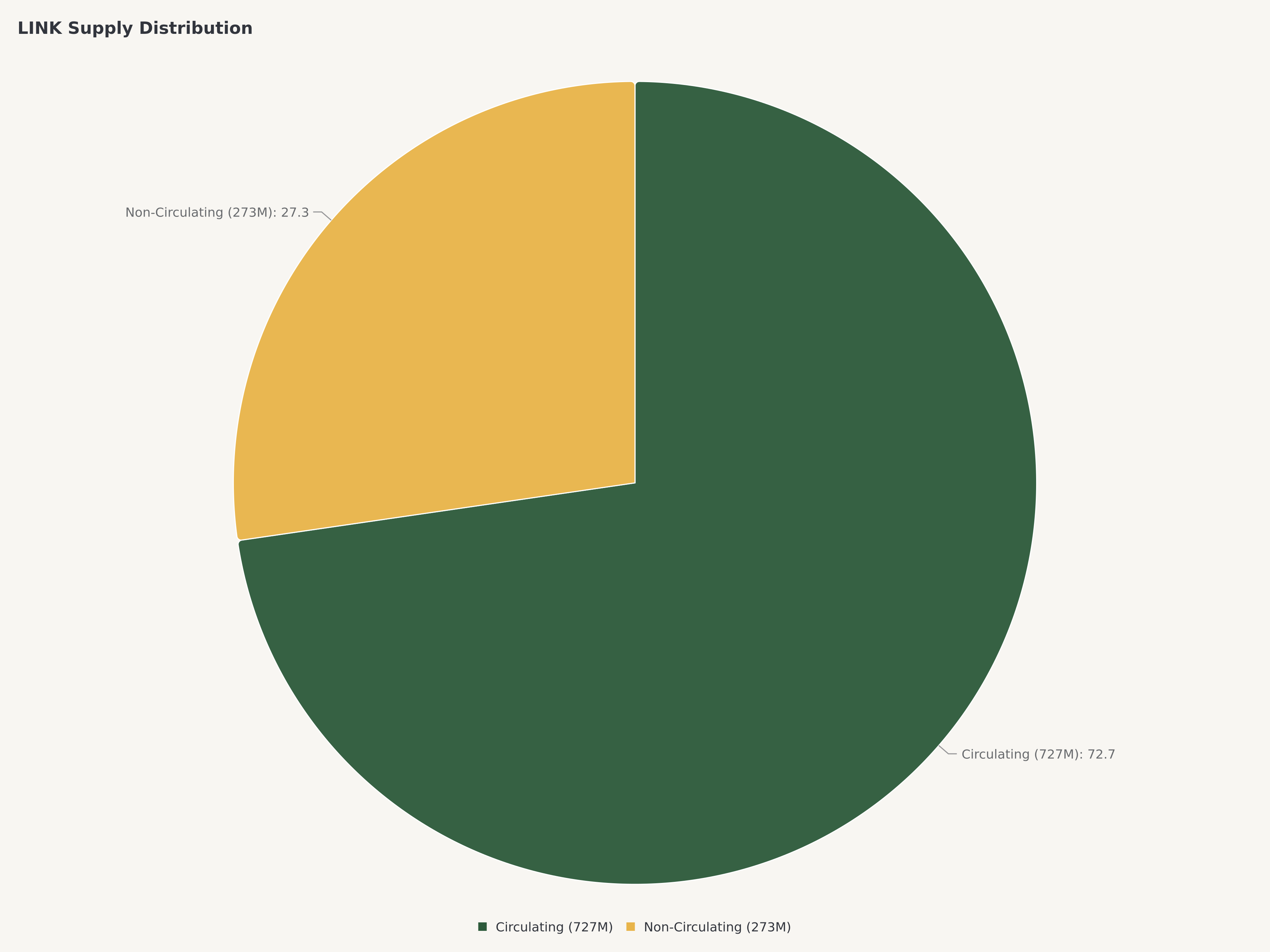

Circulating Supply | ~727M LINK | 72.7% of 1B total |

Non-Circulating Supply | ~273M LINK | 27.3% — team, ecosystem, staking |

The staking mechanism, launched in December 2022 as v0.1 and upgraded to v0.2 in late 2023, introduced cryptoeconomic security to the network. LINK stakers lock tokens to back node operator performance, earning staking rewards in exchange for absorbing slashing risk if nodes fail to deliver accurate data. While staking participation remains modest relative to protocols like Ethereum (where over 25% of supply is staked), the mechanism is directionally important: it converts LINK from a pure utility token into a yield-bearing asset with explicit security guarantees. As staking participation grows, the effective circulating supply contracts, creating a supply squeeze dynamic that could amplify price appreciation during periods of renewed demand.

Enterprise Adoption and CCIP: The TradFi Bridge That Competitors Cannot Build

Chainlink's enterprise partnership pipeline is the single most underappreciated element of its investment thesis. The distinction between Chainlink and every other oracle or interoperability project in cryptocurrency is that Chainlink has actual, production-level integrations with regulated financial institutions — not memoranda of understanding, not hackathon demos, not "exploring partnerships."

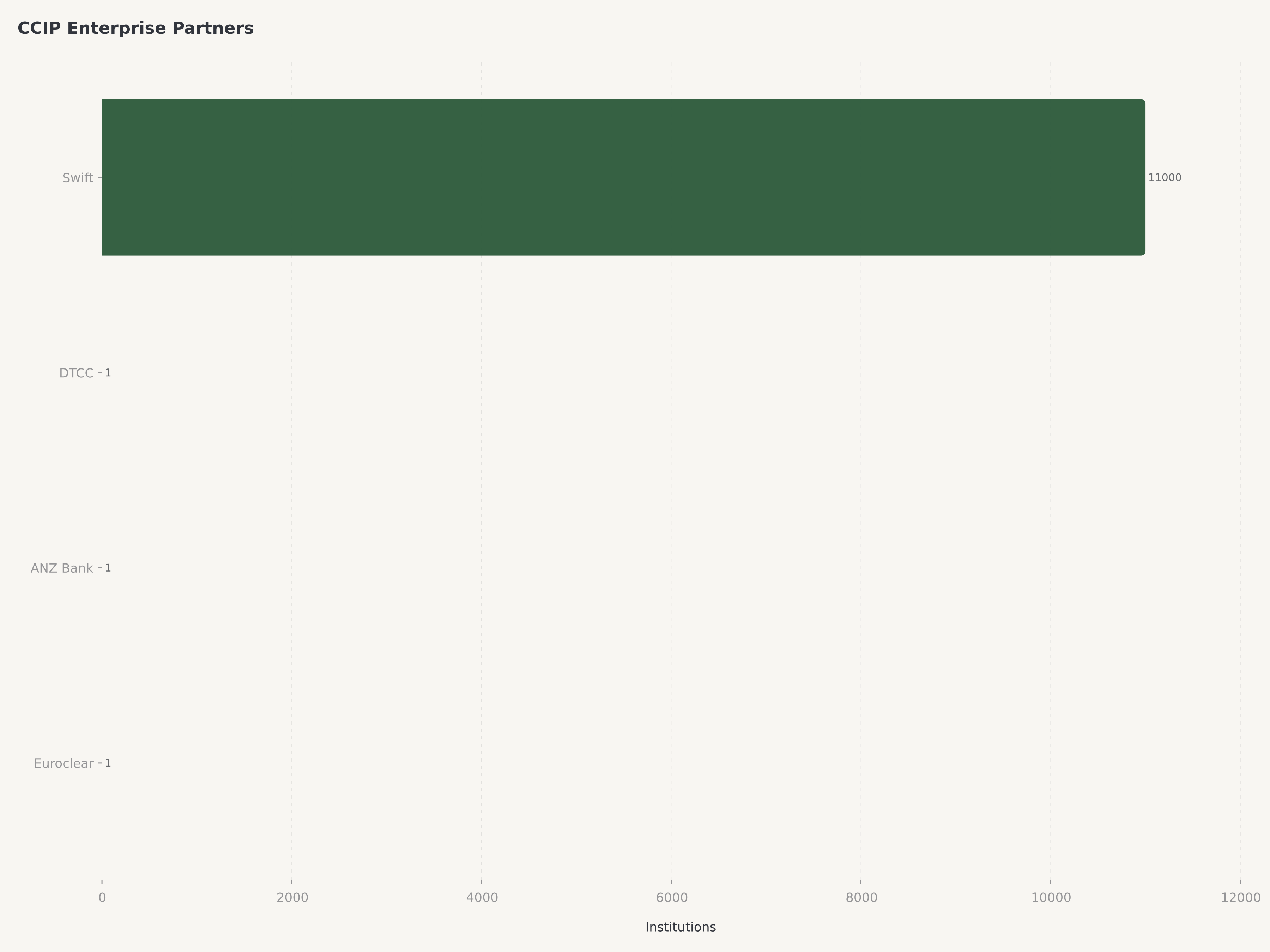

Swift, the global financial messaging network that processes $150 trillion in annual payment instructions for 11,000+ financial institutions, has been collaborating with Chainlink since 2022 on cross-chain interoperability for tokenized assets. The Swift-Chainlink experiments demonstrated that CCIP could enable a single Swift message to trigger token transfers across multiple blockchain networks simultaneously — a capability that eliminates the need for financial institutions to build individual integrations with each blockchain they want to support. In 2025, DTCC (the Depository Trust and Clearing Corporation), which processes the clearing and settlement of virtually all U.S. securities transactions, completed a pilot with Chainlink to deliver mutual fund NAV data on-chain in near-real time. ANZ Bank, BNP Paribas, Citi, and other global banks have participated in Chainlink's cross-chain settlement trials.

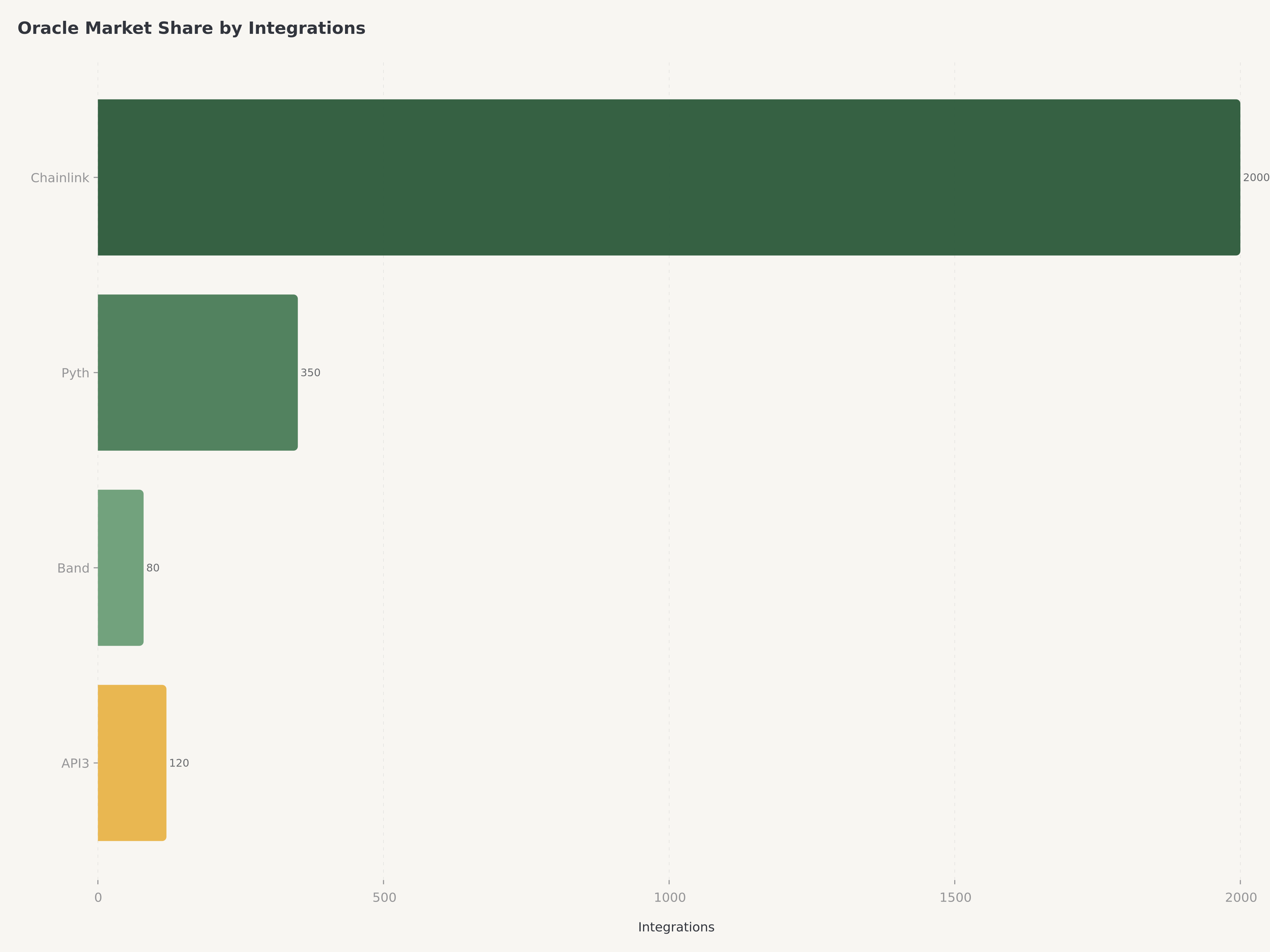

These partnerships matter because they represent the infrastructure layer for tokenized finance. When BlackRock tokenizes a money market fund, someone must provide the price data. When JPMorgan settles a tokenized bond, someone must verify the transaction across chains. When Swift routes a payment instruction that involves on-chain assets, someone must bridge the message between traditional infrastructure and blockchain networks. Chainlink is positioning itself to be that "someone" in every case. No competitor occupies this position. Pyth Network, backed by Jump Trading, has gained traction for low-latency price feeds on Solana and other high-performance chains, but its focus is DeFi-native rather than enterprise. Band Protocol and API3 have smaller network effects and no meaningful institutional partnerships. The enterprise moat is Chainlink's and Chainlink's alone.

The revenue implications are substantial but largely unrealized in the current token price. If even a fraction of the $16 trillion tokenized asset opportunity materializes by 2030, the oracle and interoperability infrastructure servicing those assets could generate billions in annual fees. Chainlink's current $150 million in annualized fees — derived primarily from DeFi applications — represents the floor, not the ceiling, of the network's revenue potential.

Valuation: An 82% Drawdown That Ignores the Enterprise Pipeline

What the market sees (above water): A token that peaked at $52.70 during the 2021 speculative mania, has been in a multi-year downtrend, and trades at $9.33 with 273 million non-circulating tokens that represent dilution risk. The market sees a crypto infrastructure project that generates fees but has no clear path to the kind of exponential growth that would justify paying a premium in a risk-off environment.

The real picture (below water): Chainlink has assembled the most comprehensive Web3 infrastructure stack in the industry, secured production-level partnerships with the largest financial institutions on Earth, and built a network effect across 1,900+ integrations that creates switching costs comparable to enterprise software. The 82% drawdown from ATH prices the token as if the enterprise pipeline, CCIP adoption, and CRE platform expansion are worth zero. The market is pricing Chainlink's past (speculative pump and dump) rather than its future (institutional infrastructure provider).

At $9.33, LINK trades at approximately 45x its annualized on-chain fees of ~$150 million. While this appears expensive relative to traditional valuation metrics, the comparison is misleading. Chainlink's fee base is growing as CCIP adoption accelerates and new services launch, and the network's operating leverage is enormous — incremental fee revenue requires minimal additional infrastructure investment. A more relevant comparison is the enterprise value-to-revenue multiples commanded by infrastructure software companies in traditional markets: Cloudflare trades at 15-20x revenue, Datadog at 12-15x, and Snowflake at 10-15x. Chainlink's fees, while protocol-native rather than subscription-based, represent a similarly sticky, infrastructure-level revenue stream.

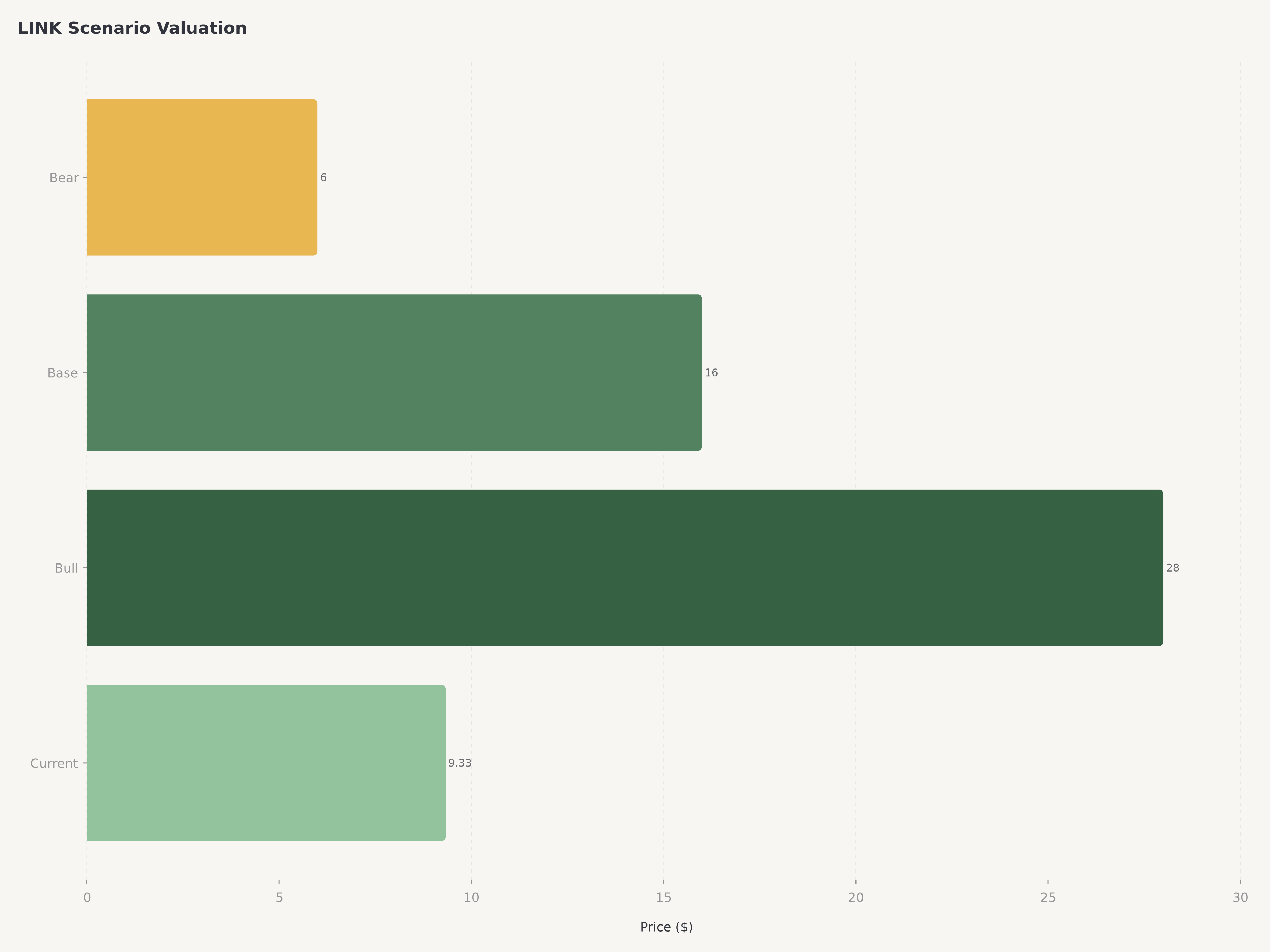

Scenario | Probability | LINK Price | Key Assumptions |

Bull | 25% | $28 | CCIP becomes standard for institutional cross-chain settlement; CRE drives 3x fee growth; staking locks 40%+ of supply; ETF or institutional product launches |

Base | 50% | $16 | CCIP adoption grows steadily; enterprise pilots convert to production; fees grow 50-80% over 12 months; supply dilution from non-circulating tokens is gradual |

Bear | 25% | $6 | Crypto winter deepens; enterprise timelines extend indefinitely; Pyth captures DeFi oracle share; full 273M token unlock creates sustained selling pressure |

**Probability-Weighted** | **100%** | **$16.50** |

The probability-weighted expected value is $16.50 (0.25 x $28 + 0.50 x $16 + 0.25 x $6), which aligns with our $16 price target. At the current price of $9.33, this represents approximately 71% upside. The symmetry between Bull and Bear probabilities reflects genuine uncertainty about the pace of institutional blockchain adoption — but importantly, even the Bear case of $6 implies only a 36% drawdown from current levels, while the Bull case of $28 implies 200% upside. The risk-reward is asymmetric in the investor's favor.

Risks: Dilution, Competition, and the Enterprise Execution Gap

Token Supply Dilution from Non-Circulating LINK. Approximately 273 million LINK tokens — 27.3% of the total 1 billion supply — remain non-circulating, held by the Chainlink team, ecosystem fund, and staking reserves. These tokens represent a latent supply overhang that could exert sustained selling pressure if released to the market. Chainlink Labs has historically sold tokens to fund operations and development, and while the pace of sales has moderated, the team's treasury management decisions remain opaque. Unlike Ethereum, where supply dynamics are transparent and governed by protocol rules (EIP-1559 burn, staking issuance), Chainlink's supply schedule is discretionary. If Chainlink Labs were to accelerate token sales during a market downturn — to fund operations precisely when the token price is weakest — the dilutive impact could be severe. The gap between the $6.78 billion circulating market cap and $9.33 billion FDV quantifies this risk: investors are paying for 72.7% of the network today but face dilution from the remaining 27.3%.

Competitive Pressure from Pyth Network and Emerging Oracles. Pyth Network, incubated by Jump Trading and launched on Solana, has emerged as Chainlink's most credible competitor in the DeFi oracle space. Pyth's pull-based oracle model — where consumers request data on-demand rather than receiving continuous push-based feeds — offers lower latency and lower costs for certain use cases, particularly high-frequency DeFi applications on Solana, Sui, and other high-performance chains. Pyth has secured over 500 integrations and provides price feeds for more than 450 assets. While Chainlink's push-based model remains superior for security-critical applications (lending, derivatives) and enterprise use cases, Pyth's growth demonstrates that the oracle market is not winner-take-all. API3, which provides first-party oracle services directly from data providers without intermediary node operators, represents an alternative architectural approach that could gain traction if the market prioritizes decentralization at the data source rather than at the node operator level. The risk is not that Chainlink loses its leadership position but that it loses pricing power as competitors offer "good enough" oracle services at lower cost.

Enterprise Adoption Timeline Uncertainty. Chainlink's investment thesis rests heavily on the assumption that institutional blockchain adoption will translate into meaningful CCIP and CRE revenue within 12-24 months. The partnerships with Swift, DTCC, and major banks are real and technically validated, but the gap between "pilot" and "production at scale" in enterprise finance is measured in years, not quarters. Regulatory uncertainty, internal technology governance at large banks, and the inherent conservatism of financial institutions could delay CCIP's revenue ramp indefinitely. If the tokenized asset market grows more slowly than projected — if the $16 trillion opportunity by 2030 is actually $2 trillion by 2030 — Chainlink's current valuation already prices in much of the upside. Investors are paying for an infrastructure monopoly in a market that may take longer to materialize than expected.

Conclusion

Chainlink occupies a unique position in cryptocurrency: a protocol that is simultaneously essential infrastructure for DeFi today and the leading candidate to become the connective layer between traditional finance and blockchain networks. The 82% drawdown from the 2021 all-time high has created a valuation that prices LINK as a speculative altcoin rather than the enterprise infrastructure platform it has become. At $9.33, with $6.78 billion in market capitalization, the market is implicitly assigning near-zero value to the CCIP enterprise pipeline, the CRE platform expansion, and the staking mechanism's impact on effective supply.

We rate LINK Buy with a $16 price target, representing approximately 71% upside. The thesis rests on three pillars: Chainlink's unchallenged dominance in oracle infrastructure with 1,900+ integrations, the CCIP protocol's positioning as the default cross-chain settlement layer for institutional tokenized assets, and the CRE platform's creation of switching costs that deepen protocol lock-in over time. The primary risk is execution — converting enterprise pilots into production revenue at scale while managing token supply dilution from the remaining 273 million non-circulating LINK. For investors with a 12-month horizon who can tolerate crypto-level volatility, the risk-reward at current levels is compelling. Readers tracking the broader crypto infrastructure thesis may find relevant context in our analysis of Ethereum's Layer 2 ecosystem and RWA tokenization catalysts, while our examination of Aave's DeFi lending resilience after the Kelp DAO hack illustrates how Chainlink's oracle infrastructure underpins the largest lending protocol in decentralized finance.

The one thing to watch: CCIP transaction volume. If cross-chain message throughput accelerates meaningfully in the second half of 2026 — driven by institutional tokenized asset settlement rather than DeFi-native activity — Chainlink's revenue trajectory will confirm the enterprise thesis and the current valuation will look dramatically cheap in retrospect.

Frequently Asked Questions

Is LINK a good investment right now?

We rate LINK Buy with a $16 price target, representing approximately 71% upside from the current price of $9.33. Chainlink is the dominant decentralized oracle network with over 1,900 integrations across 30+ blockchain networks, generating approximately $150 million in annualized on-chain fees. The 82% drawdown from the all-time high of $52.70 has created an attractive entry point, particularly given the network's enterprise partnerships with Swift, DTCC, and major global banks for cross-chain tokenized asset settlement through CCIP. The primary risks are token supply dilution from 273 million non-circulating LINK (27.3% of total supply) and uncertainty around the pace of institutional blockchain adoption.

What is Chainlink's price target for 2026?

Our three-scenario analysis produces a Bull case of $28 (25% probability, assuming CCIP becomes the institutional cross-chain standard and fee revenue triples), a Base case of $16 (50% probability, assuming steady CCIP adoption and 50-80% fee growth), and a Bear case of $6 (25% probability, assuming a prolonged crypto downturn and enterprise timeline delays). The probability-weighted expected value of $16.50 supports our $16 price target. At the current price of $9.33, the risk-reward is asymmetric: the Bear case implies 36% downside while the Bull case implies 200% upside.

What are the main risks of investing in Chainlink (LINK)?

Three primary risks define the investment case. First, approximately 273 million LINK tokens (27.3% of total supply) remain non-circulating, creating dilution risk if Chainlink Labs accelerates token sales. Second, Pyth Network has emerged as a credible competitor in DeFi oracles with a lower-latency, lower-cost pull-based model that has secured over 500 integrations. Third, enterprise adoption timelines are inherently uncertain — the partnerships with Swift and DTCC are technically validated but converting pilots to production-scale revenue could take years rather than quarters.

How does Chainlink compare to Pyth Network?

Chainlink and Pyth serve overlapping but distinct segments of the oracle market. Chainlink operates a push-based model with over 1,900 integrations across 30+ chains, generates ~$150 million in annualized fees, and has enterprise partnerships with Swift, DTCC, and major banks through CCIP. Pyth uses a pull-based model favored for low-latency DeFi applications, has 500+ integrations concentrated on Solana and other high-performance chains, and is backed by Jump Trading. Chainlink's advantages are network breadth, enterprise relationships, and the full-stack CRE platform; Pyth's advantages are speed and cost for DeFi-native use cases. The oracle market is large enough for both, but Chainlink's enterprise moat is unique and irreplicable by Pyth in the near term.

What is CCIP and why does it matter for LINK's value?

The Cross-Chain Interoperability Protocol (CCIP) is Chainlink's infrastructure for secure token transfers and messaging between blockchain networks. Unlike third-party bridges — which have suffered billions in exploits (Ronin $625M, Wormhole $325M) — CCIP leverages Chainlink's existing decentralized oracle network plus an independent Risk Management Network for security. Swift has adopted CCIP for cross-chain settlement experiments, and DTCC has used it for on-chain mutual fund NAV delivery. CCIP matters for LINK's value because it transforms Chainlink from an oracle provider into the default cross-chain settlement layer for the estimated $16 trillion tokenized asset market. Every institutional tokenized asset transaction that settles through CCIP generates fees paid in LINK, creating organic demand that scales with institutional blockchain adoption.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a solicitation, or a recommendation to buy or sell any securities or digital assets. The analysis reflects the author's opinion based on publicly available information, on-chain data, and proprietary Edgen research as of the publication date. Digital asset investments carry substantial risk, including the potential loss of all invested capital. DeFi protocols and infrastructure networks are subject to smart contract risk, governance risk, regulatory risk, and market risk. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions. Edgen and its analysts may hold positions in digital assets discussed. Price targets and ratings reflect 12-month forward expectations and are subject to revision.

Recommend