Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

Summary

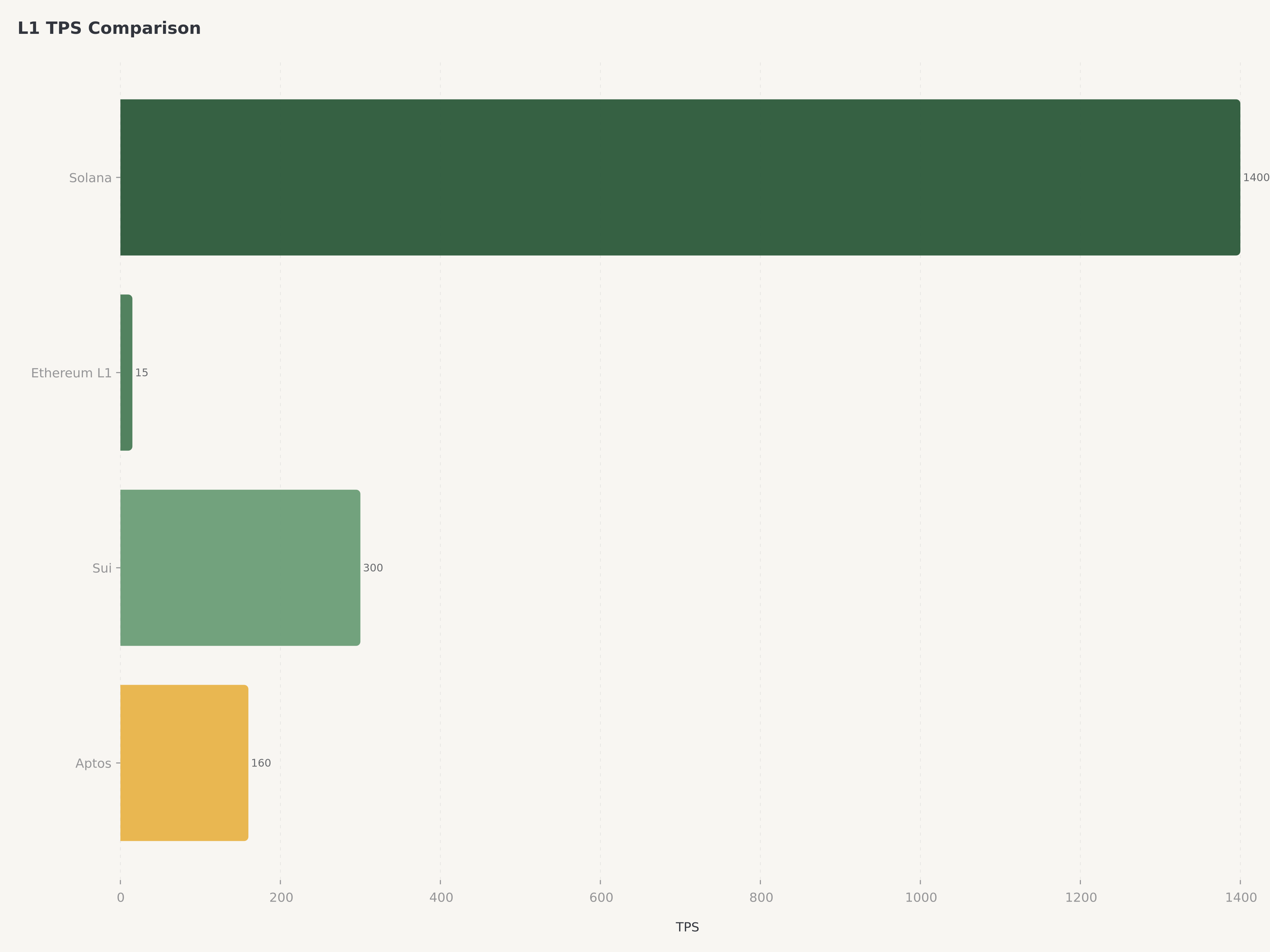

- Solana trades at $85.41 with a market capitalization of $49.12 billion and a fully diluted valuation of $53.33 billion, positioning it as the fourth-largest cryptocurrency by market cap and the highest-throughput Layer 1 blockchain in production, consistently processing 1,400+ transactions per second with sub-400-millisecond block times — performance metrics that no competing chain has matched at scale.

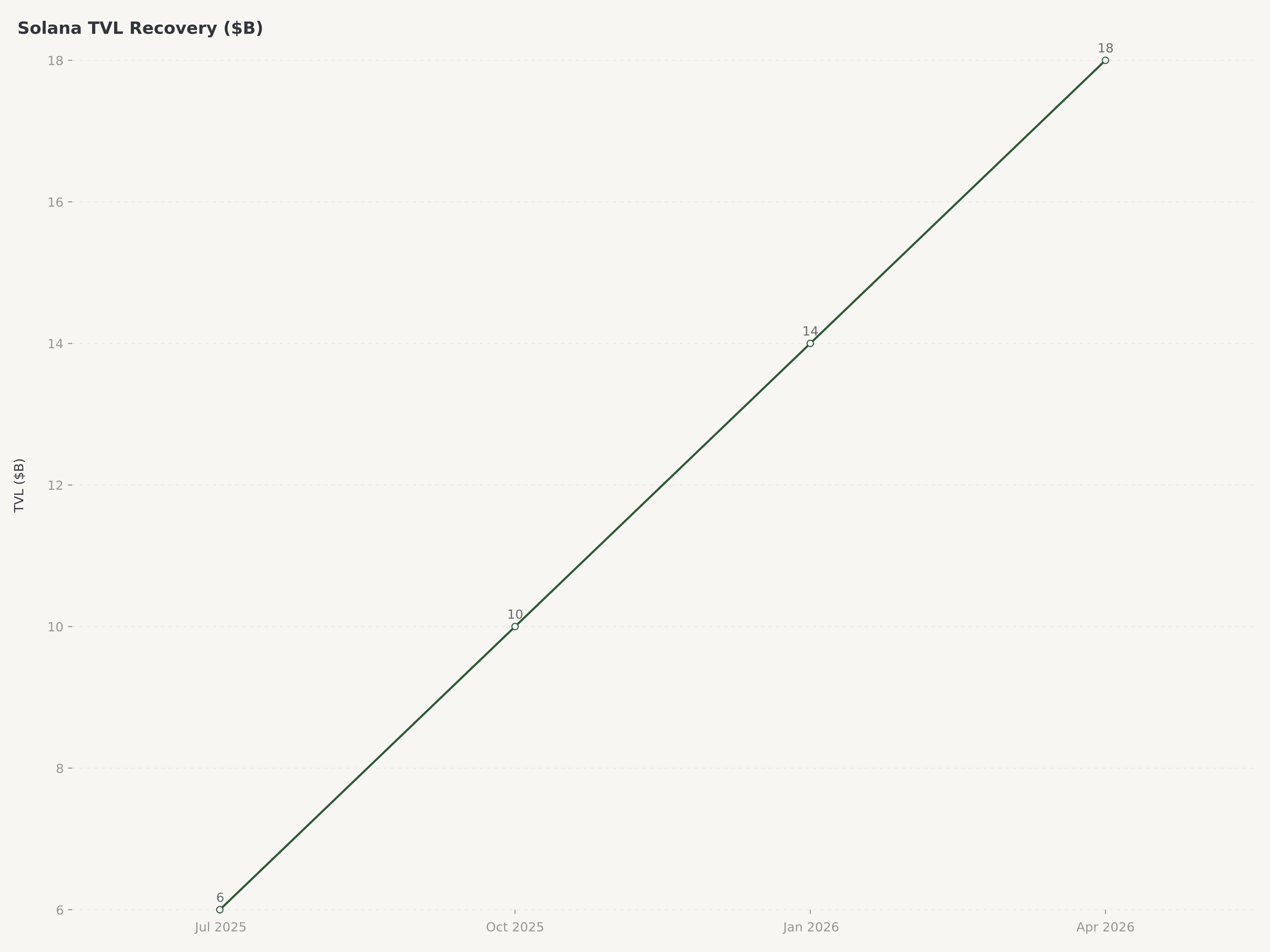

- Total value locked on Solana has surged over 110% from its 2025 lows, driven by explosive growth in DeFi protocols such as Jupiter (the dominant DEX aggregator), Raydium (concentrated liquidity AMM), and the migration of real economic activity onto the network through DePIN projects like Helium, NFT marketplaces, and the memecoin phenomenon that brought millions of new wallets onto the chain.

- The Firedancer validator client, developed by Jump Crypto, is progressing toward full mainnet deployment and represents the most significant infrastructure upgrade in Solana's history — a second independent client implementation that eliminates single-client risk, dramatically improves validator performance, and could push theoretical throughput above 1 million TPS once fully optimized.

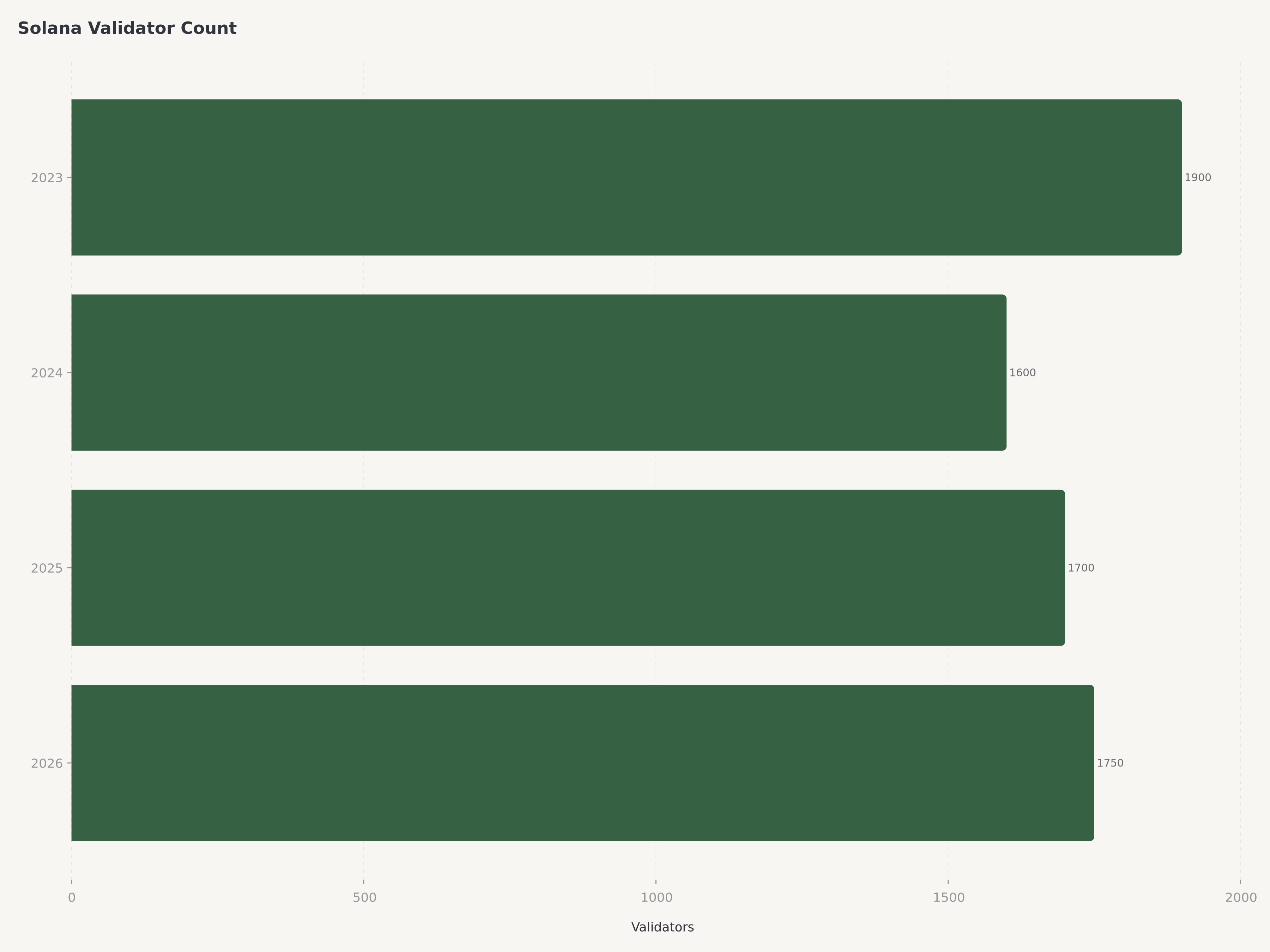

- We rate SOL Buy with a $130 price target (~52% upside), supported by the network's unmatched throughput advantage, a validator set of 1,700+ nodes, the deflationary issuance proposal SIMD-0096 that would reduce SOL inflation, and a catalyst-rich roadmap including Firedancer mainnet, Solana Mobile expansion, and continued DeFi/DePIN ecosystem growth — with key risks centered on historical network outages, validator centralization concerns, and MEV extraction dynamics that remain partially unresolved.

The Layer 1 Landscape in 2026: Performance as the Competitive Moat

The blockchain infrastructure wars of 2024-2025 produced a clear hierarchy. Ethereum secured its position as the settlement layer for institutional finance and Layer 2 rollups. A handful of alternative Layer 1s survived the bear market by finding genuine product-market fit rather than relying on incentive programs and vapor metrics. Solana emerged from that shakeout as the undisputed performance leader — the chain where applications that require speed, low cost, and high throughput actually choose to deploy.

The numbers tell the story with precision. As of April 16, 2026, Solana consistently processes over 1,400 transactions per second in real-world conditions, with block times averaging 400 milliseconds and transaction costs measured in fractions of a cent. For context, Ethereum's mainnet processes roughly 15-30 TPS, with Layer 2s adding capacity but introducing bridging complexity and fragmented liquidity. Sui and Aptos, the Move-language chains that were positioned as Solana competitors, have achieved respectable throughput in controlled conditions but have yet to demonstrate the sustained, organic transaction volume that Solana generates daily.

What changed between 2023 and 2026 was not merely technical improvement but ecosystem composition. The Solana of 2023 was heavily reliant on speculative trading volume and NFT flipping — economic activity that evaporated when markets turned. The Solana of 2026 hosts Helium's decentralized wireless network (over 1 million active hotspots), Jupiter's DEX aggregator (processing billions in monthly volume), Drip's creator economy platform, and a growing number of payments and fintech applications that chose Solana specifically because no other chain could deliver the user experience their products required. This shift from speculative to productive activity is the foundation of our bullish thesis.

The macro context for Layer 1 investment in 2026 is shaped by two competing forces. On one hand, the total addressable market for blockchain infrastructure continues to expand as tokenization, DePIN, and decentralized finance attract institutional participation. On the other, the winner-take-most dynamics of network effects mean that capital is concentrating in the chains that have demonstrated real usage rather than theoretical capability. Solana sits at the intersection of these forces: proven throughput attracting builders, builders attracting users, users attracting liquidity, and liquidity attracting more builders.

Architecture and Technical Differentiation: Why Solana Is Fast

Understanding Solana's investment case requires understanding why its architecture delivers performance that competitors cannot replicate by simply increasing hardware requirements or tweaking consensus parameters. The chain's throughput advantage is not a single innovation but the product of eight interlocking technical decisions made by co-founder Anatoly Yakovenko when he designed the network in 2017-2018.

Proof of History is the foundational innovation — a cryptographic clock that timestamps transactions before they enter consensus, allowing validators to agree on the order of events without the message-passing overhead that slows other chains. Combined with Tower BFT (Solana's optimized PBFT consensus), Turbine (block propagation via erasure coding), Gulf Stream (mempool-less transaction forwarding), and Sealevel (parallel smart contract execution across available cores), the result is a system designed from the ground up for parallelism. Where Ethereum processes transactions sequentially and Layer 2s batch transactions for later settlement, Solana processes them concurrently at the hardware level.

The Firedancer validator client, under development by Jump Crypto since 2022, is the most consequential upgrade to this architecture since mainnet launch. Solana has historically run a single validator client (the Labs client, written in Rust), which created single-point-of-failure risk — a bug in the client could halt the entire network, as occurred during several outage events in 2022 and 2023. Firedancer is a ground-up reimplementation in C/C++, optimized for modern data center hardware with techniques drawn from high-frequency trading infrastructure. Early benchmarks have demonstrated over 600,000 TPS in controlled environments. While production performance will be lower due to real-world network conditions, the client's architecture is designed to scale with hardware improvements — meaning Solana's throughput ceiling rises as commodity server performance improves, without requiring protocol-level changes.

The dual-client architecture that Firedancer enables is arguably more important than the raw performance gains. When both the Labs client and Firedancer are running on mainnet, a critical bug in either client cannot halt the network as long as the other client maintains sufficient stake. This is the same resilience model that Ethereum achieved with its Geth/Nethermind/Besu client diversity, and it addresses the single most frequently cited technical risk in Solana's investment case.

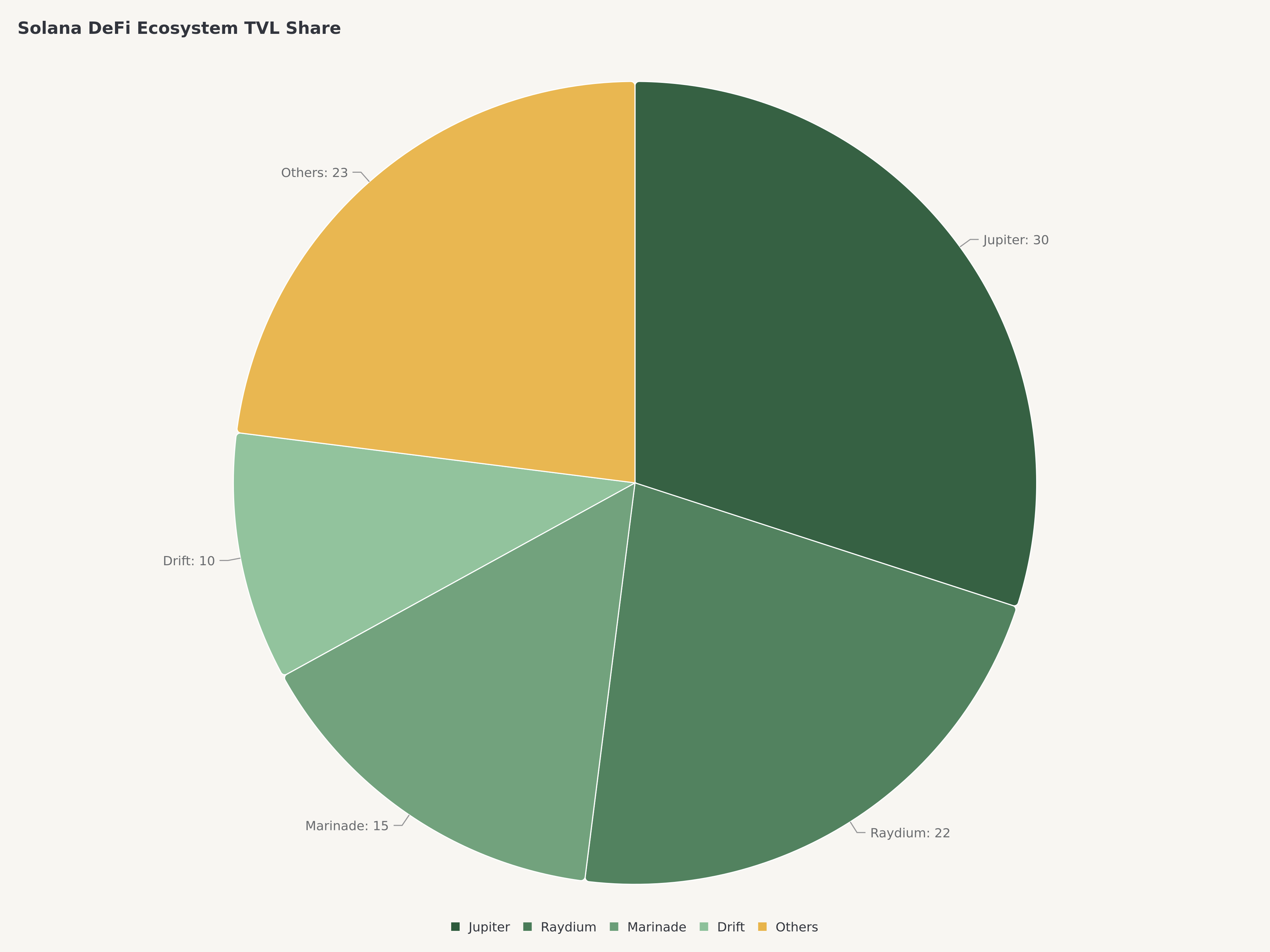

DeFi Ecosystem: Jupiter, Raydium, and the Liquidity Flywheel

Solana's DeFi ecosystem has transformed from a speculative playground into a mature financial infrastructure layer. Total value locked across Solana DeFi protocols surged over 110% from the lows reached during the 2025 consolidation, a recovery driven not by incentive farming but by genuine demand for high-speed, low-cost financial services.

Jupiter has established itself as the dominant DEX aggregator on Solana, routing trades across multiple liquidity sources to deliver optimal execution. Jupiter's monthly trading volume regularly exceeds $10 billion, and its perpetual futures product — Jupiter Perps — has captured meaningful market share from centralized exchanges by offering similar execution speed with on-chain settlement and self-custody. The JUP token's launch and subsequent governance activity created one of the most active DeFi communities in the ecosystem.

Raydium operates as Solana's core AMM and concentrated liquidity venue, providing the base liquidity that Jupiter and other aggregators route through. Raydium's concentrated liquidity model, similar to Uniswap V3 but optimized for Solana's block times, allows liquidity providers to allocate capital more efficiently. The protocol's daily volume consistently ranks among the top five DEXs across all chains.

The memecoin phenomenon, while often dismissed as frivolous, played a material role in Solana's ecosystem expansion. Platforms like Pump.fun democratized token creation, generating enormous transaction volume and onboarding millions of new wallets. While the speculative excess produced predictable casualties, the infrastructure built to support this activity — wallets, DEXs, analytics tools, social trading platforms — remains and now serves broader use cases. It is the same pattern that played out with NFTs in 2021: the speculative wave recedes, but the infrastructure it funded persists and matures.

DePIN (Decentralized Physical Infrastructure Networks) represents Solana's most differentiated DeFi-adjacent vertical. Helium, which migrated from its own chain to Solana in 2023, now operates over 1 million active wireless hotspots providing real-world cellular coverage through partnerships with T-Mobile and other carriers. Render Network processes GPU computing jobs for AI and graphics rendering on Solana. Hivemapper is building a decentralized mapping network with over 200,000 dashcam contributors. These are not speculative DeFi protocols — they are businesses with real revenue, real users, and real physical infrastructure, and they chose Solana because no other chain could handle their transaction throughput requirements at acceptable cost.

Protocol | Category | TVL / Volume | Significance |

Jupiter | DEX Aggregator | $10B+ monthly volume | Dominant trading venue, perps competitor |

Raydium | AMM / CLMM | Top-5 DEX by volume | Core liquidity layer for ecosystem |

Marinade | Liquid Staking | ~$1.5B staked | Largest native liquid staking protocol |

Helium | DePIN / Wireless | 1M+ hotspots | Real-world infrastructure on Solana |

Render | DePIN / GPU | Growing compute network | AI/graphics decentralized rendering |

Tokenomics and the SIMD-0096 Deflationary Proposal

SOL's token economics have evolved significantly since the network's 2020 launch. The initial inflation schedule started at 8% annual issuance, declining at 15% per year toward a long-term terminal rate of 1.5%. As of April 2026, the effective inflation rate has declined to approximately 4.5%, with roughly 480 million SOL in circulation out of a maximum supply that is not hard-capped but governed by the declining issuance schedule.

Staking participation is robust, with approximately 65-70% of circulating SOL staked across the validator set. Staking yields currently range from 6-8% APY depending on validator commission rates, making SOL one of the higher-yielding proof-of-stake assets among major Layer 1s. This high staking ratio has positive implications for supply dynamics: staked tokens are effectively removed from liquid circulation, reducing sell pressure and creating a natural floor under the price during drawdowns.

The SIMD-0096 proposal represents a potentially transformative shift in Solana's monetary policy. The proposal would redirect a portion of transaction priority fees — currently burned — toward a mechanism that offsets new SOL issuance, creating conditions for net deflationary supply dynamics during periods of high network activity. If implemented, SIMD-0096 would align Solana's tokenomics more closely with Ethereum's EIP-1559 burn mechanism, but with the advantage of higher base transaction volume generating larger absolute fee burns.

The economic logic is straightforward: as Solana's transaction volume grows, more fees are generated; if those fees offset or exceed new issuance, the circulating supply contracts. For a network already processing 1,400+ TPS, the math is favorable. At current activity levels, the proposal would not achieve full deflation, but it would meaningfully reduce net inflation. At projected activity levels — factoring in Firedancer's throughput expansion and continued DeFi/DePIN growth — net deflation becomes plausible within 12-18 months of implementation.

The fully diluted valuation of $53.33 billion versus the current market cap of $49.12 billion implies relatively modest dilution from unreleased tokens, a marked improvement from earlier periods when large foundation and team unlocks created significant overhang. The majority of remaining locked tokens are staked and subject to governance decisions about release schedules, providing the community with meaningful control over future supply dynamics.

Validator Network and Decentralization Metrics

Solana's validator network comprises over 1,700 active validators, a number that has grown steadily from roughly 1,000 in early 2023. The Nakamoto coefficient — the minimum number of validators required to control 33% of stake and theoretically halt the network — currently stands at approximately 20-22, which places Solana below Ethereum (~30+) but above most alternative Layer 1s.

The centralization critique has been a persistent overhang on Solana's valuation. Critics correctly note that Solana's hardware requirements — validators need high-performance servers with substantial RAM, fast NVMe storage, and high-bandwidth connections — create barriers to entry that favor institutional operators and data center deployments. This stands in contrast to Ethereum, where solo staking is possible on commodity hardware. The Solana Foundation has addressed this through delegation programs, validator subsidies, and geographic diversity initiatives, but the fundamental tension between high performance and low-barrier decentralization remains.

However, the centralization narrative deserves nuance. Solana's 1,700+ validators significantly exceed the validator counts of Sui (~120), Aptos (~120), and most other alternative Layer 1s. The network's stake distribution, while concentrated at the top, features a long tail of smaller validators that collectively provide meaningful censorship resistance. And the Firedancer client, by offering an alternative implementation, ensures that no single development team controls the network's software stack — a form of decentralization that the validator count alone does not capture.

The network's last significant outage occurred in February 2024, more than two years ago. Since that incident, Solana has maintained continuous uptime through multiple high-traffic events, including memecoin launches that generated transaction volumes exceeding anything the network had previously experienced. This operational track record, while not erasing the memory of earlier outages, demonstrates that the engineering improvements implemented in 2023-2024 have produced meaningful resilience gains.

Valuation: Scenario Analysis and Price Target Framework

Valuing a Layer 1 blockchain token requires assessing the economic value that flows through the network and the token's claim on that value. SOL derives value from three sources: transaction fee generation (which benefits stakers and, under SIMD-0096, would reduce supply), staking yield (direct economic return to holders), and the network's role as the base currency for a growing DeFi ecosystem (creating organic demand for SOL as collateral, gas, and liquidity).

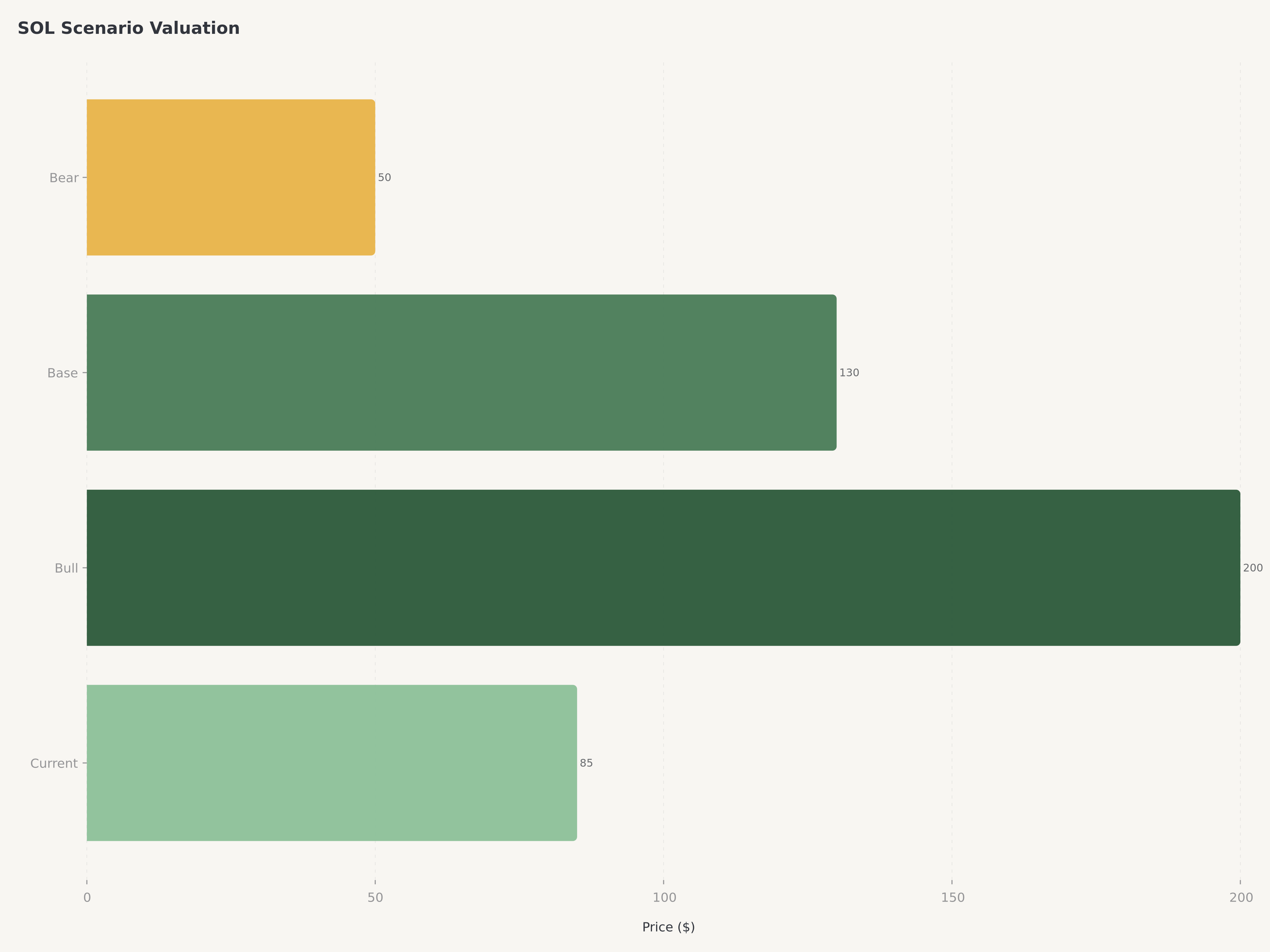

Our scenario analysis models three outcomes over a 12-month horizon.

Scenario | Probability | SOL Price | TVL | Key Assumptions |

Bull | 25% | $200 | $30B+ | Firedancer mainnet drives throughput above 10K TPS, SIMD-0096 implemented with net deflationary dynamics, DePIN adoption accelerates, Solana Mobile gains traction, ETF speculation |

Base | 50% | $130 | $18-22B | Firedancer partial rollout, continued DeFi/DePIN growth, TVL stabilizes at 2x 2025 lows, SIMD-0096 passes governance, validator count exceeds 2,000, no major outages |

Bear | 25% | $50 | $6-8B | Network outage damages confidence, Firedancer delayed significantly, regulatory crackdown on Solana-based tokens, Ethereum L2s capture DeFi mindshare, sustained crypto bear market |

The probability-weighted expected value is $127.50 (0.25 x $200 + 0.50 x $130 + 0.25 x $50). We round to $130 for our price target, reflecting the base case plus a slight premium for the optionality embedded in the Firedancer upgrade and SIMD-0096 catalysts. At the current price of $85.41, this represents approximately 52% upside.

On a relative basis, SOL's market cap of $49.12 billion against the network's daily fee generation and DeFi TVL compares favorably to competing Layer 1s. Ethereum trades at a significantly higher market cap ($280B+) but with proportionally lower throughput per dollar of network value. Sui and Aptos, while technically capable, trade at valuations that imply optimistic adoption trajectories that have not yet materialized. SOL occupies a middle ground: proven adoption, established ecosystem, and a throughput advantage that grows wider as Firedancer matures.

The comparison to Ethereum is not adversarial — the two chains increasingly serve complementary roles. Ethereum is the settlement layer for high-value transactions, institutional DeFi, and Layer 2 rollups. Solana is the execution layer for high-frequency, consumer-facing applications that require speed and low cost. This coexistence thesis, rather than a zero-sum competition narrative, better explains the market structure and supports the case for owning both. Investors interested in the broader Layer 1 thesis should review our Ethereum analysis covering the Layer 2 and RWA tokenization catalysts for a complementary perspective.

Risks

Network Outage and Reliability History. Solana experienced multiple network outages between 2021 and early 2024, including events where the chain halted entirely for hours and required coordinated validator restarts. While the last significant outage occurred in February 2024 — over two years ago — the reputational damage persists and creates an asymmetric risk: months of flawless uptime earn modest confidence, while a single outage event can erase it. The Firedancer dual-client architecture mitigates this risk substantially, but until both clients are running on mainnet with significant stake, the network remains on a single-client implementation. A major outage during a high-profile event — a memecoin launch, a DePIN milestone, or a period of market volatility — could trigger a disproportionate price decline and institutional exodus.

Validator Centralization and MEV Extraction. The economic structure of Solana's validator network creates incentives that trend toward centralization. High hardware requirements favor well-capitalized operators. MEV (maximal extractable value) extraction — where validators reorder transactions to profit at users' expense — has become a growing concern on Solana, with some estimates suggesting that MEV extraction costs users hundreds of millions of dollars annually. While Jito's MEV auction system has brought some transparency to this process, the fundamental dynamic of validators extracting value from users is a governance and trust problem that remains partially unresolved. If MEV extraction becomes egregious enough to damage user experience, it could push activity to competing chains or Layer 2 solutions.

Competitive Pressure from Ethereum Layer 2s, Sui, and Aptos. Ethereum's Layer 2 ecosystem — Arbitrum, Optimism, Base, and zkSync — collectively offers high throughput with the security guarantees of Ethereum settlement. As L2 technology matures and cross-L2 interoperability improves, the user experience gap between Solana and Ethereum L2s narrows. Sui and Aptos, while smaller today, have well-funded development teams and technical architectures (Move language, object-centric model) that could prove superior for certain use cases. A scenario where L2 fees drop to near-zero and L2 throughput matches Solana's would erode the network's primary competitive advantage. Additionally, the regulatory environment remains uncertain: enforcement actions targeting Solana-based tokens or protocols could create ecosystem-specific headwinds that do not affect competing chains.

Conclusion

Solana in April 2026 is a fundamentally different network than the one that suffered repeated outages in 2022. The chain has survived its existential test — FTX's collapse, which wiped out its largest institutional backer and triggered a 96% drawdown in SOL's price — and emerged with a stronger ecosystem, more diverse application base, and a technical upgrade path that no competitor can match in the near term. The 110%+ TVL recovery, 1,400+ TPS sustained throughput, and 1,700+ validators represent real traction rather than manufactured metrics.

The investment case rests on three pillars: Firedancer's mainnet deployment transforming Solana from a single-client network to a resilient, multi-client infrastructure; SIMD-0096 creating deflationary tokenomics that reward holders as network activity grows; and the DeFi/DePIN ecosystem generating organic demand for SOL as the base currency of the highest-throughput blockchain in production. At $85.41, the market is pricing in the risks — centralization, outage history, competitive pressure — while undervaluing the catalysts. We rate SOL Buy with a $130 price target. For additional context on the DeFi ecosystem dynamics that drive Solana's growth, our analysis of Aave's DeFi lending landscape and governance evolution explores the institutional maturation of decentralized finance that benefits infrastructure layers like Solana.

Is Solana (SOL) a good investment in 2026?

We rate SOL Buy with a $130 price target, representing approximately 52% upside from the current price of $85.41. Solana's investment case is built on its position as the highest-throughput Layer 1 blockchain in production, consistently processing over 1,400 transactions per second with sub-400ms block times. The network's TVL has surged 110%+ from 2025 lows, driven by genuine DeFi adoption through Jupiter, Raydium, and DePIN projects like Helium. The Firedancer validator client upgrade and SIMD-0096 deflationary tokenomics proposal provide near-term catalysts. Key risks include historical network outages (last significant event in February 2024), validator centralization, and competitive pressure from Ethereum Layer 2s.

What is the Firedancer upgrade and why does it matter for SOL?

Firedancer is a ground-up reimplementation of Solana's validator client, developed by Jump Crypto in C/C++ using techniques from high-frequency trading infrastructure. It matters for three reasons. First, it creates client diversity — with two independent validator clients running on mainnet, a bug in either one cannot halt the network, eliminating the single-client risk that contributed to previous outages. Second, early benchmarks have demonstrated over 600,000 TPS in controlled environments, suggesting that Solana's throughput ceiling will rise dramatically once Firedancer is fully deployed. Third, Firedancer's architecture scales with hardware improvements, meaning Solana's performance advantage grows over time without requiring protocol-level changes.

How does Solana compare to Ethereum in 2026?

Solana and Ethereum increasingly serve complementary rather than competitive roles. Ethereum processes 15-30 TPS on mainnet and relies on Layer 2 rollups (Arbitrum, Optimism, Base) for scalability, making it the preferred settlement layer for high-value transactions, institutional DeFi, and RWA tokenization. Solana processes 1,400+ TPS natively with sub-cent transaction costs, making it the preferred execution layer for high-frequency, consumer-facing applications — DEX trading, DePIN, payments, and social applications. SOL's $49.12 billion market cap versus Ethereum's $280B+ reflects this positioning. The coexistence thesis, rather than zero-sum competition, better explains the current market structure.

What is SIMD-0096 and how would it affect SOL's supply?

SIMD-0096 is a governance proposal to redirect a portion of Solana's transaction priority fees toward a mechanism that offsets new SOL issuance, creating conditions for net deflationary supply dynamics during periods of high network activity. Currently, SOL's inflation rate is approximately 4.5% annually, declining toward a 1.5% terminal rate. If SIMD-0096 is implemented, fee burns during high-activity periods could offset or exceed new issuance, contracting the circulating supply. This would align Solana's tokenomics with Ethereum's EIP-1559 burn mechanism, but with the advantage of higher base transaction volume generating larger absolute fee burns. The proposal must pass Solana governance before implementation.

What are the biggest risks for Solana investors?

Three primary risks warrant attention. First, network reliability: while Solana has maintained over two years of continuous uptime since the February 2024 outage, the historical pattern of halts creates asymmetric reputational risk where a single incident could trigger disproportionate price decline. Second, centralization: Solana's high hardware requirements favor institutional validators, the Nakamoto coefficient (~20-22) is lower than Ethereum's (~30+), and MEV extraction costs users hundreds of millions annually. Third, competitive pressure: Ethereum Layer 2s are narrowing the performance gap while offering Ethereum's security guarantees, and newer chains like Sui and Aptos present longer-term competitive threats. Regulatory uncertainty around Solana-based tokens and protocols adds an additional layer of risk.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a solicitation, or a recommendation to buy or sell any securities or digital assets. The analysis reflects the author's opinion based on publicly available information, on-chain data, and proprietary Edgen research as of the publication date. Digital asset investments carry substantial risk, including the potential loss of all invested capital. Layer 1 blockchain tokens are subject to network risk, governance risk, regulatory risk, and market risk. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions. Edgen and its analysts may hold positions in digital assets discussed. Price targets and ratings reflect 12-month forward expectations and are subject to revision.

Recommend