Summary

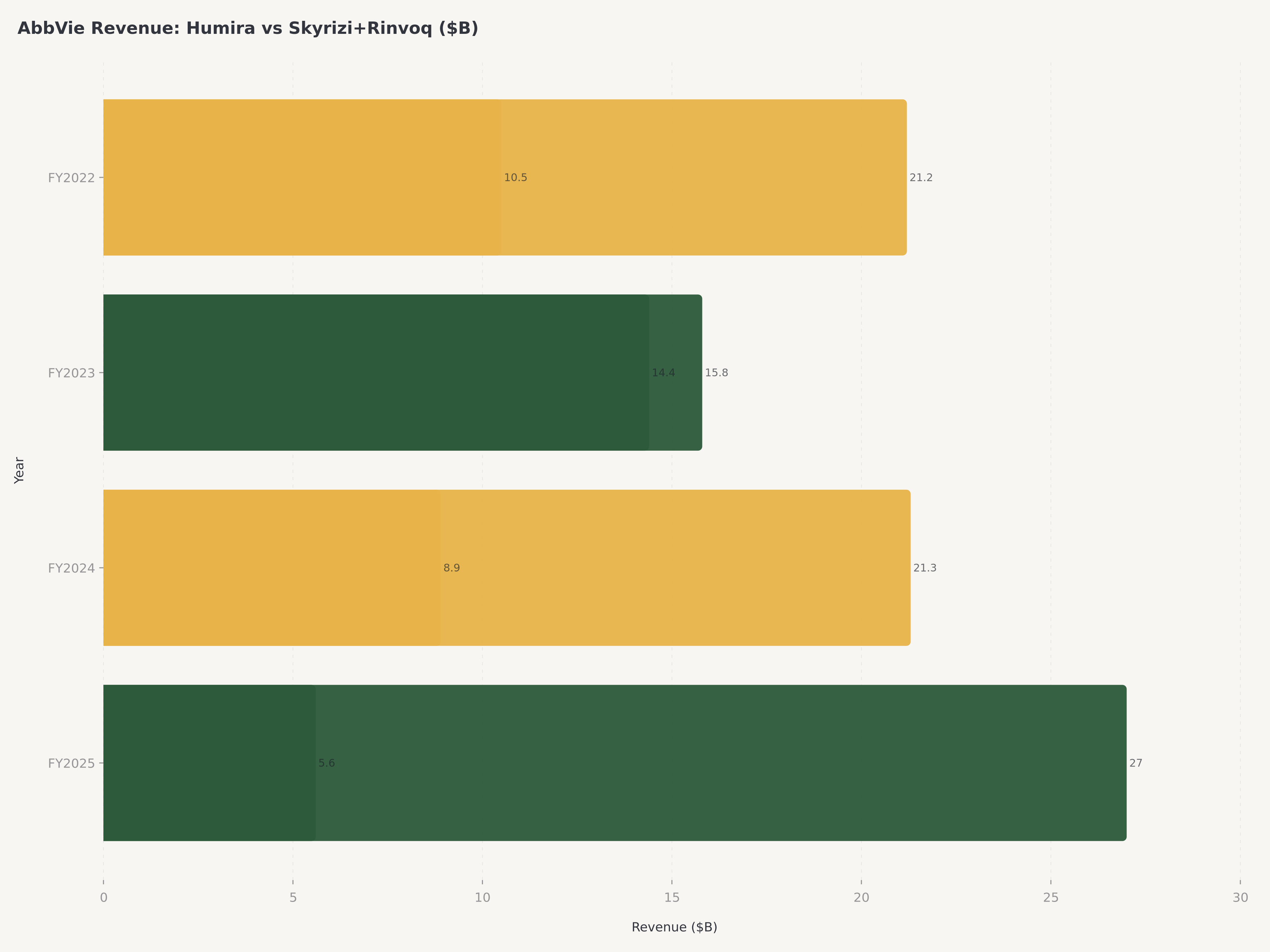

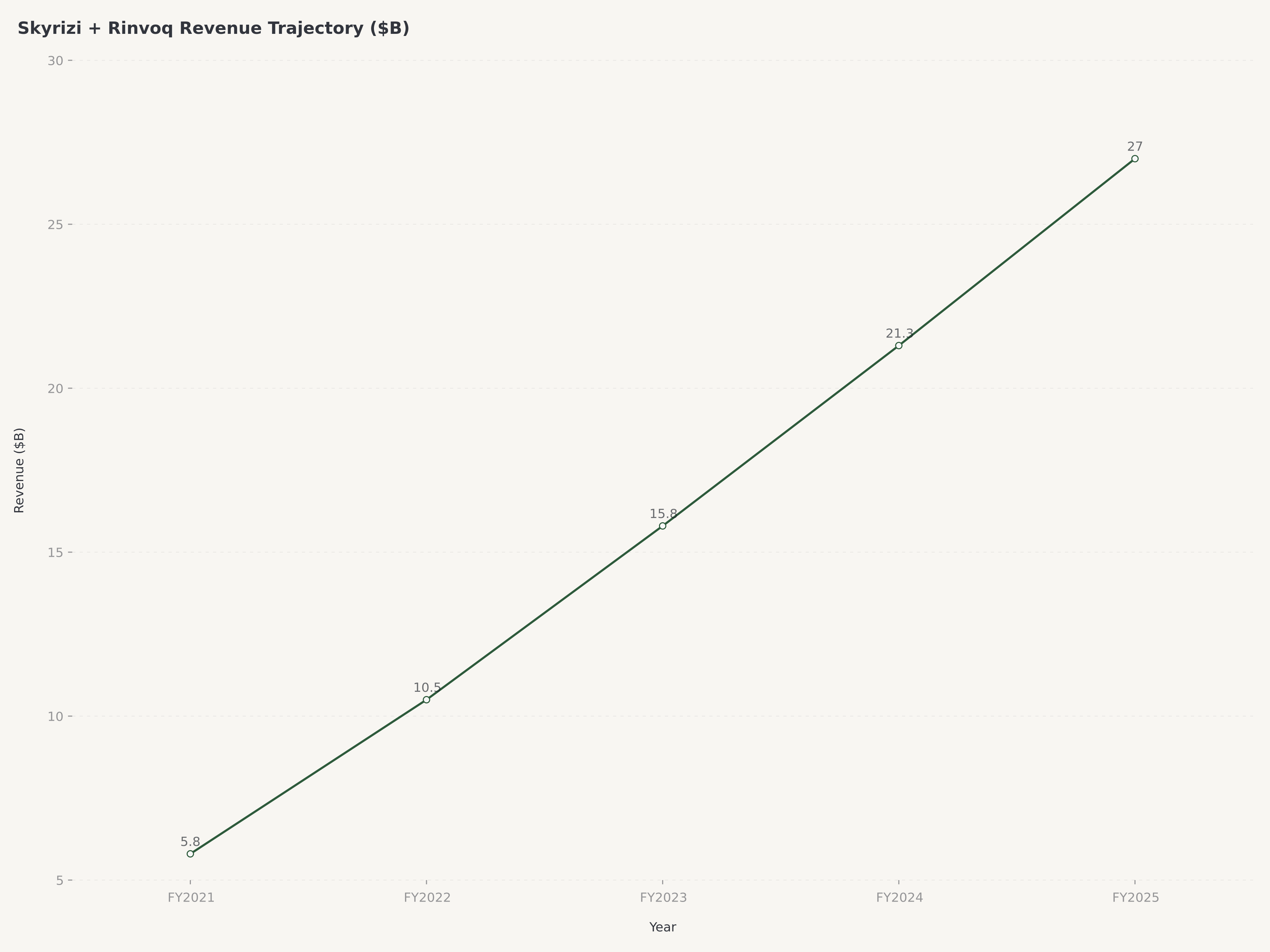

- AbbVie ($ABBV) delivered FY2025 revenue of approximately $61.16 billion, up 10.6% year-over-year, demonstrating that the most feared patent cliff in pharmaceutical history — the loss of Humira exclusivity — has been decisively navigated, with next-generation immunology assets Skyrizi and Rinvoq now generating a combined annual run rate approaching $27 billion and accelerating.

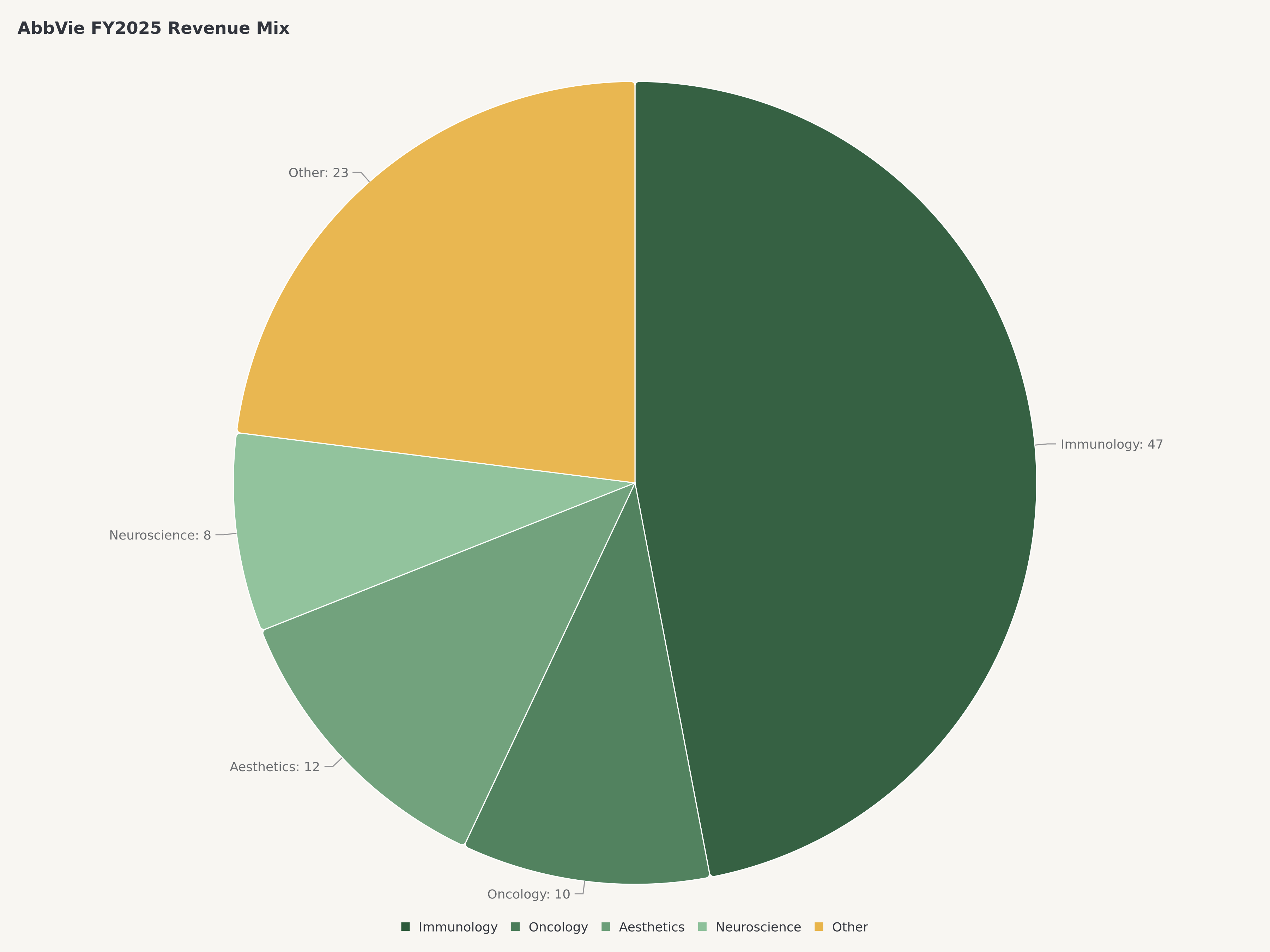

- The company's diversified portfolio spans Immunology (~47% of revenue), Oncology (~10%), Neuroscience, and Aesthetics (Botox), with the 2024 acquisition of Cerevel Therapeutics for $8.7 billion adding a deep neuroscience pipeline targeting schizophrenia, Parkinson's disease, and mood disorders — markets with significant unmet medical need and limited competition.

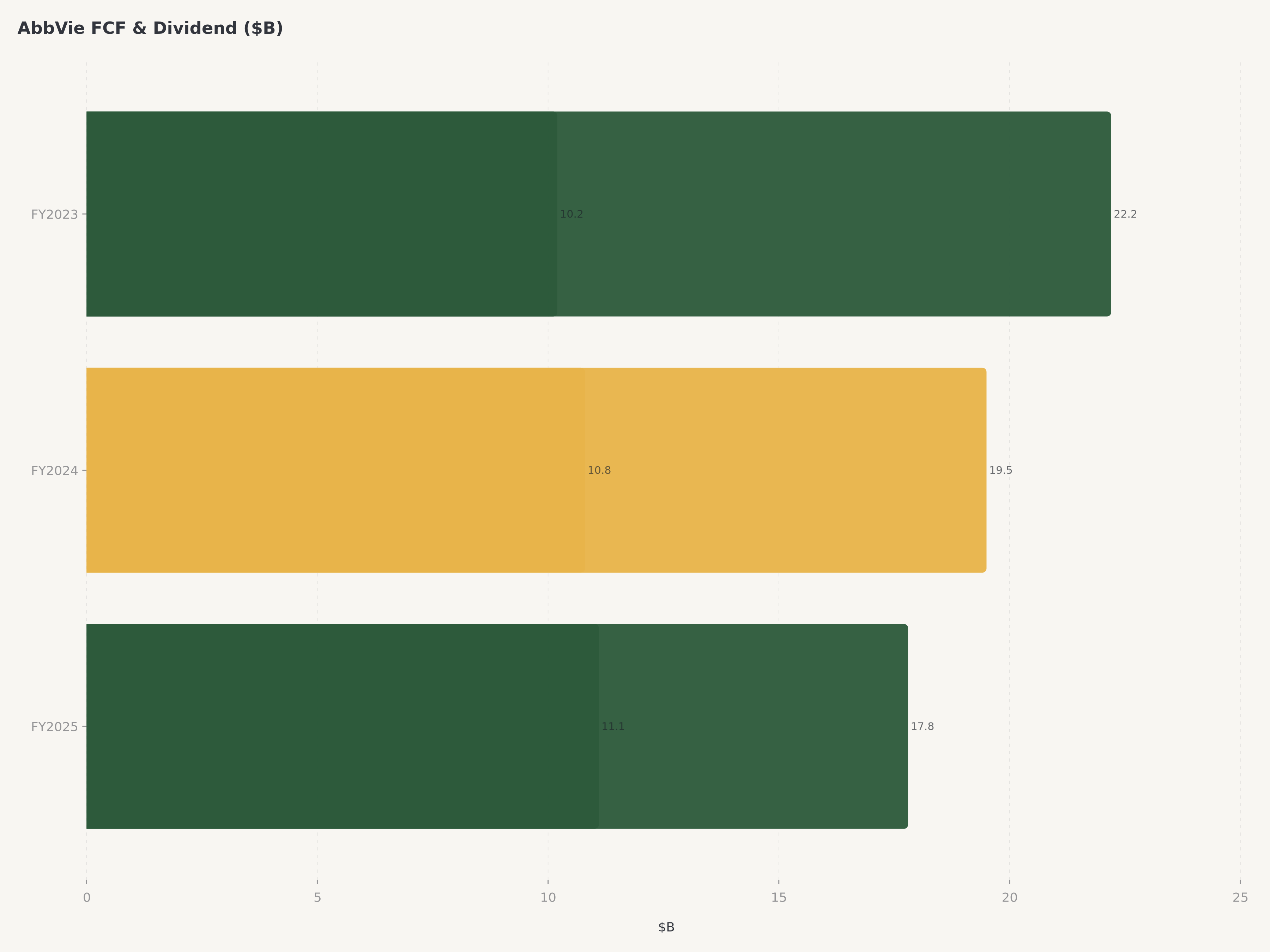

- Free cash flow of $17.8 billion supports AbbVie's status as a Dividend Aristocrat with 52 consecutive years of dividend increases, while the forward P/E of approximately 14.2x on non-GAAP EPS of ~$14.37 reflects a valuation that fails to account for the durability and growth trajectory of the Skyrizi/Rinvoq franchise.

- We rate AbbVie Buy with a $250 price target, representing approximately 22% upside from the current price of $205.48, supported by our conviction that the market is underpricing the company's successful platform transition, pipeline optionality from Cerevel, and the structural cash generation that funds both shareholder returns and bolt-on M&A without compromising the balance sheet.

The Pharmaceutical Landscape in 2026: Patent Cliffs, the IRA, and the Innovation Premium

The global pharmaceutical industry in 2026 is navigating a structural transformation driven by three converging forces: the largest patent cliff cycle in the sector's history, the implementation of the Inflation Reduction Act's drug price negotiation provisions, and a widening bifurcation between companies with genuine innovation engines and those reliant on mature, commoditizing portfolios.

Between 2023 and 2030, branded drugs representing over $250 billion in peak annual revenue will lose patent protection, exposing companies to biosimilar and generic competition that typically erodes 60-80% of branded revenue within three to five years of exclusivity loss. AbbVie's Humira, which peaked at $21.2 billion in annual sales in 2022 as the world's best-selling drug, was the poster child for this risk. The drug's U.S. biosimilar entry in January 2023 triggered an immediate and sustained revenue decline — Humira revenue fell to approximately $14.4 billion in FY2023, then approximately $10.2 billion in FY2024, and is estimated at roughly $7.5 billion in FY2025, with further erosion expected through 2027 as biosimilar penetration deepens.

The Inflation Reduction Act adds another layer of complexity. Beginning in 2026, Medicare will negotiate prices directly with manufacturers for a growing list of high-expenditure drugs. While AbbVie's Imbruvica and certain other assets face potential negotiation exposure in coming years, the company's proactive portfolio rotation toward newer drugs with longer patent runways (Skyrizi's composition-of-matter patent extends to 2033, Rinvoq to 2031 with pediatric extensions) provides a natural hedge against IRA-related pricing pressure. Companies with aging portfolios and limited pipeline depth — such as Bristol-Myers Squibb, which faces Revlimid and Eliquis cliffs simultaneously — are far more exposed.

The investment implication is clear: the pharma sector in 2026 rewards companies that can replace lost revenue with innovative, patent-protected assets faster than the erosion occurs. AbbVie has executed this transition more convincingly than any large-cap peer, and the market has not yet fully priced in the magnitude of that accomplishment.

AbbVie's Transformation: From Abbott Spinoff to the Skyrizi/Rinvoq Era

AbbVie was spun off from Abbott Laboratories in January 2013 as a research-based pharmaceutical company, inheriting Humira as its crown jewel. For the first decade of its independent existence, AbbVie's investment thesis was inseparable from Humira — the anti-TNF antibody generated over $200 billion in cumulative revenue during its commercial life, funded AbbVie's dividend, financed acquisitions (Allergan for $63 billion in 2020, Pharmacyclics for $21 billion in 2015), and became the most commercially successful pharmaceutical product ever developed.

The Humira dependency was simultaneously AbbVie's greatest strength and its most visible vulnerability. By 2021, the drug represented over 35% of total company revenue, and the approaching biosimilar entry date was the single most discussed risk factor in large-cap pharma. CEO Richard Gonzalez, who led AbbVie from its 2013 spinoff through 2024, staked his legacy on a dual strategy: build successor franchises in immunology (Skyrizi and Rinvoq) while diversifying the portfolio through M&A (Allergan for Botox and aesthetics, Pharmacyclics for Imbruvica in oncology).

Robert Michael, who assumed the CEO role in 2024 after serving as President and COO, inherited a company in the middle of this transition — Humira revenue was falling rapidly, but Skyrizi and Rinvoq were not yet large enough to fully offset the decline. The 2025 results vindicate the strategy decisively. Combined Skyrizi and Rinvoq revenue is approaching $27 billion on an annualized basis, making them collectively larger than Humira at its peak. Skyrizi, approved for plaque psoriasis, psoriatic arthritis, and Crohn's disease, is growing at over 50% year-over-year and is on track to become a $20 billion peak-sales product individually. Rinvoq, a JAK inhibitor approved across rheumatoid arthritis, psoriatic arthritis, atopic dermatitis, ulcerative colitis, and Crohn's disease, continues to expand its label and is tracking toward $10 billion+ in peak sales.

The Cerevel Therapeutics acquisition, completed in 2024 for $8.7 billion, represents the next phase of AbbVie's diversification strategy. Cerevel's pipeline is anchored by emraclidine, a selective muscarinic M4 agonist in Phase III trials for schizophrenia — a mechanism of action that, if validated, could represent the first genuinely new approach to treating schizophrenia in decades, addressing a $10 billion+ market where existing antipsychotics carry debilitating side effect profiles. Tavapadon, a D1/D5 partial agonist for Parkinson's disease, adds additional depth. The neuroscience portfolio complements AbbVie's existing Botox franchise (migraine, therapeutic indications) and positions the company for long-term optionality in one of pharma's highest-value therapeutic areas.

FY2025 Operating Performance: Proving the Skeptics Wrong

AbbVie's FY2025 results represent the clearest evidence that the Humira patent cliff has been managed successfully. Total revenue of approximately $61.16 billion grew 10.6% year-over-year despite Humira's continued decline, driven by the extraordinary ramp of Skyrizi and Rinvoq and steady contributions from Oncology and Aesthetics.

The revenue mix tells the story of a company in active transformation:

Segment | FY2025 Revenue (est.) | % of Total | Key Drivers |

Immunology | ~$28.7B | ~47% | Skyrizi, Rinvoq growth offsetting Humira decline |

Oncology | ~$6.1B | ~10% | Imbruvica (declining), Venclexta (growing) |

Aesthetics | ~$5.8B | ~9.5% | Botox Cosmetic, Juvederm |

Neuroscience | ~$5.2B | ~8.5% | Botox Therapeutic, Vraylar, Ubrelvy |

Other (Eye Care, etc.) | ~$15.3B | ~25% | Diverse specialty portfolio |

GAAP earnings per share have been volatile due to non-cash charges related to acquisitions — amortization of intangible assets from the Allergan and Cerevel deals distorts GAAP profitability significantly. Non-GAAP adjusted EPS of approximately $14.37 provides a cleaner picture of underlying earnings power, reflecting the high-margin nature of AbbVie's branded pharmaceutical portfolio.

Financial Metric | FY2025 |

Revenue | ~$61.16B |

YoY Revenue Growth | +10.6% |

Non-GAAP Adjusted EPS | ~$14.37 |

Free Cash Flow | ~$17.8B |

FCF Margin | ~29% |

Market Capitalization | $370.3B |

Current Price | $205.48 |

Dividend Yield | ~3.8% |

Consecutive Dividend Increases | 52 years |

Free cash flow of $17.8 billion — representing a 29% FCF margin — is the financial backbone that supports everything AbbVie does. It funds the $10.1 billion annual dividend (AbbVie has raised its dividend every year since the 2013 spinoff, maintaining its Dividend Aristocrat status inherited from Abbott), covers debt service on the balance sheet leverage acquired through M&A, finances the $7 billion+ annual R&D budget, and still leaves capacity for opportunistic share repurchases and bolt-on acquisitions.

Pharma Pipeline Deep Dive: The Next Decade of Growth

AbbVie's pipeline is the primary reason our price target implies significant upside. While the market focuses on the Humira cliff narrative (increasingly backward-looking) and gives partial credit for Skyrizi/Rinvoq (already reflected in consensus estimates), it is not fully pricing the optionality embedded in the neuroscience pipeline, immunology label expansions, and oncology next-generation assets.

Immunology — Skyrizi and Rinvoq Label Expansion. Skyrizi is currently approved in plaque psoriasis, psoriatic arthritis, and Crohn's disease, with a supplemental filing for ulcerative colitis expected to yield approval in 2026. Each new indication adds $1-3 billion in peak revenue potential. The drug's IL-23p19 mechanism has demonstrated best-in-class efficacy across inflammatory conditions with a favorable safety profile that does not carry the boxed warnings associated with JAK inhibitors. Rinvoq's label already spans five indications, with atopic dermatitis and Crohn's disease as the fastest-growing segments. The JAK class faces some competitive and regulatory headwinds — the 2023 FDA class-wide boxed warning for JAK inhibitors has required AbbVie to invest in physician education and real-world evidence generation — but Rinvoq's clinical data in head-to-head studies against adalimumab (Humira) and dupilumab (Dupixent) has been competitive, supporting continued share gains.

Neuroscience — Cerevel Assets. Emraclidine (Phase III, schizophrenia) is the highest-value pipeline asset acquired through the Cerevel deal. The M4 muscarinic agonist mechanism targets a $10 billion+ market where current standard-of-care drugs (olanzapine, risperidone, aripiprazole) cause metabolic side effects — weight gain, diabetes, movement disorders — that contribute to poor patient compliance and high discontinuation rates. Phase II data showed statistically significant reductions in PANSS scores with a tolerability profile markedly better than existing antipsychotics. Phase III results expected in 2027 could represent a significant value catalyst. Tavapadon (D1/D5 partial agonist, Parkinson's disease) is earlier-stage but addresses another high-unmet-need market where the current levodopa-based standard of care has not fundamentally changed in 50 years.

Oncology — Beyond Imbruvica. Imbruvica, the BTK inhibitor acquired through the $21 billion Pharmacyclics deal, has faced competitive erosion from AstraZeneca's Calquence and Lilly's Jaypirca, with revenue declining in the mid-single digits annually. However, AbbVie's oncology pipeline includes navitoclax (BCL-2 inhibitor combinations) and several partnered programs. Venclexta, the BCL-2 inhibitor partnered with Roche, continues to grow in hematological malignancies and represents a durable revenue stream extending beyond 2030.

Aesthetics — Botox Longevity. Botox Cosmetic and Botox Therapeutic together generate approximately $6 billion annually, with the cosmetic segment benefiting from secular demand growth driven by social media influence, expanding demographics (male consumers, younger cohorts), and geographic penetration in Asia-Pacific markets. The Juvederm dermal filler franchise adds another $1-2 billion. Importantly, Botox has no meaningful patent cliff risk — the product's competitive moat is built on brand recognition, physician training networks, and manufacturing complexity rather than composition-of-matter patents.

Valuation: The Market Is Still Pricing the Cliff, Not the Recovery

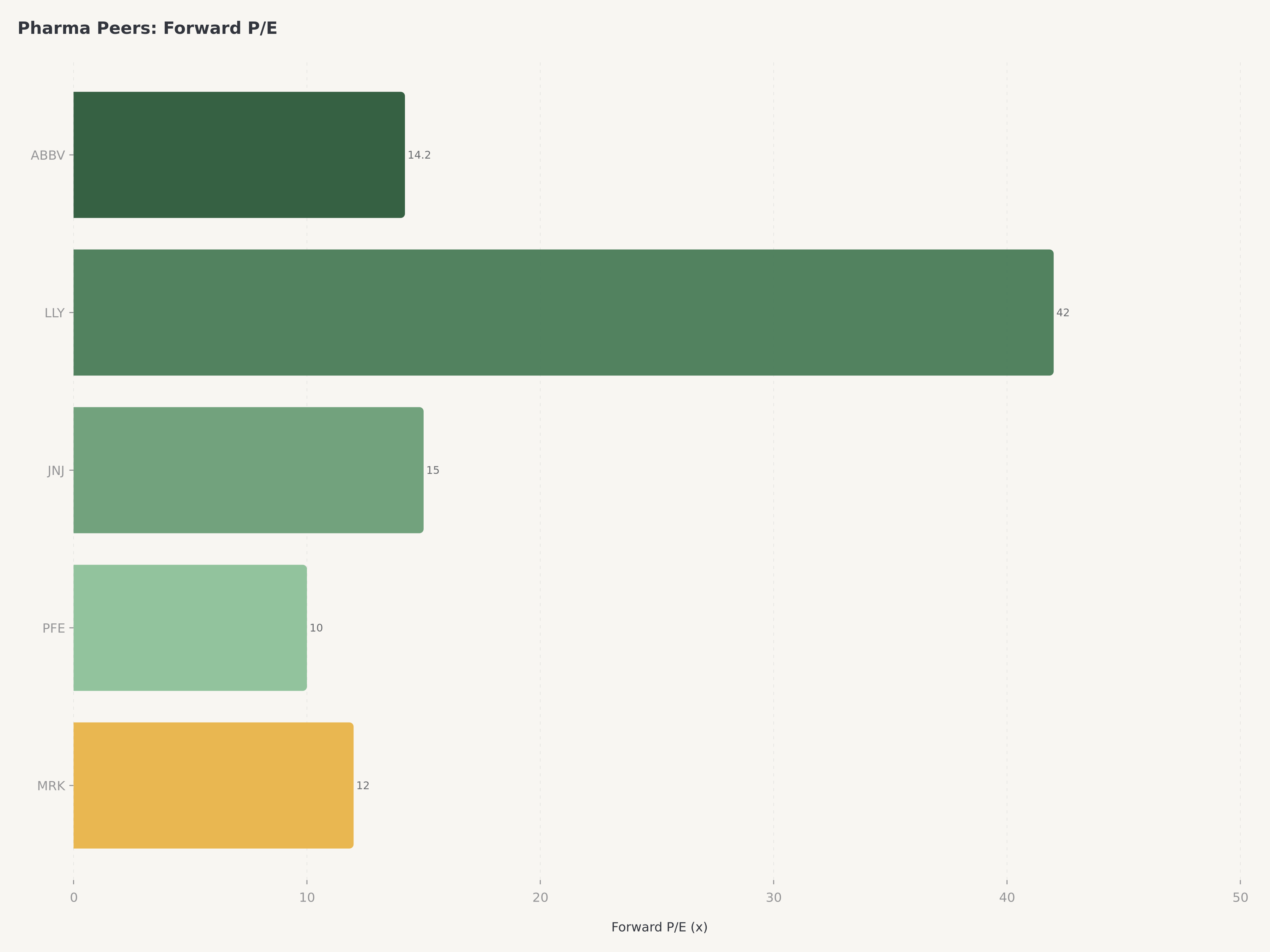

AbbVie trades at a forward P/E of approximately 14.2x on non-GAAP EPS of ~$14.37, which represents a notable discount to both the S&P 500 Healthcare sector average (~16x forward) and to growth-adjusted peers like Eli Lilly, which trades at 35x+ forward earnings on the back of GLP-1 momentum. The discount reflects lingering market skepticism about AbbVie's post-Humira trajectory — skepticism that is increasingly at odds with the company's actual financial performance.

Valuation Metric | AbbVie | Sector Median | Context |

Forward P/E (Non-GAAP) | ~14.2x | ~16x | Discount to sector |

GAAP P/E | N/M (distorted) | — | Acquisition amortization |

EV/EBITDA | ~11.5x | ~13x | Attractive for cash flow |

Dividend Yield | ~3.8% | ~1.5% | Aristocrat premium |

FCF Yield | ~4.8% | ~3.5% | Supports dividend + M&A |

PEG Ratio | ~1.3x | ~1.8x | Reasonable for 10%+ growth |

We construct a four-scenario probability-weighted model:

Bull Case ($300 — 20% probability). Skyrizi and Rinvoq combined revenue exceeds $30 billion in FY2026, emraclidine Phase III data reads out positively, and AbbVie executes a mid-size bolt-on acquisition in oncology or inflammation. The market re-rates the stock to 17x forward earnings as the Humira cliff narrative fully fades. Dividend growth accelerates to 6-7% annually.

Base Case ($245 — 50% probability). Revenue grows 7-9% in FY2026 as Skyrizi/Rinvoq growth continues to more than offset Humira erosion. Non-GAAP EPS reaches $15.50-$16.00. The market gradually narrows the valuation discount to peers, with the stock reaching 15.5x forward earnings. FCF remains above $18 billion, supporting continued dividend increases and debt reduction.

Bear Case ($175 — 25% probability). Rinvoq faces additional regulatory restrictions related to JAK inhibitor safety concerns, emraclidine Phase III data disappoints or is delayed, and the IRA price negotiation framework expands to cover more of AbbVie's portfolio sooner than expected. Revenue growth decelerates to low-single digits, and the market applies a 12x forward multiple reflecting increased uncertainty.

Disaster Case ($130 — 5% probability). A safety signal emerges for Skyrizi (highly unlikely given the mechanism's clean profile, but all biologics carry tail risk), combined with emraclidine failure and an aggressive IRA expansion that caps pricing on Rinvoq. Revenue declines, the dividend payout ratio becomes strained, and the stock de-rates to 10x forward earnings. This scenario requires multiple simultaneous adverse outcomes and is assigned low probability.

Probability-weighted fair value: $243. Our $250 price target includes a modest premium for the unpriced optionality in the Cerevel neuroscience pipeline and the secular growth embedded in the Botox/Aesthetics franchise. At current prices, investors are effectively getting the Aesthetics and Neuroscience segments for free while paying a discounted multiple on the immunology franchise alone.

Risks

Humira Erosion Pace and Immunology Transition Timing. While the transition from Humira to Skyrizi/Rinvoq is proceeding better than most forecasts, the pace of Humira's decline could accelerate if biosimilar pricing becomes more aggressive or if interchangeable biosimilar designations (which allow pharmacy-level substitution without physician intervention) erode remaining brand loyalty faster than expected. There is a window of 12-18 months during which Skyrizi/Rinvoq must continue growing at current rates to ensure the revenue crossover is smooth. Any disruption — manufacturing issues, supply chain constraints, competitive launches — during this critical period could create a temporary earnings gap.

JAK Inhibitor Regulatory and Safety Risk. Rinvoq, as a JAK inhibitor, carries a class-wide FDA boxed warning for serious infections, malignancies, blood clots, and cardiovascular events based on post-marketing safety data from the tofacitinib (Xeljanz) ORAL Surveillance study. While Rinvoq's own clinical trial data has not replicated the same safety signals seen with tofacitinib, the FDA has applied the warning to all JAK inhibitors as a class effect. Future regulatory action — such as additional prescribing restrictions, requirements for failed prior therapy before JAK use, or label modifications — could constrain Rinvoq's addressable market and growth trajectory.

Cerevel Pipeline Binary Risk. The $8.7 billion Cerevel acquisition is primarily a bet on emraclidine in schizophrenia. Phase II data was encouraging but not conclusive, and Phase III trials carry inherent binary risk — central nervous system drugs have historically had the lowest Phase III success rates of any therapeutic area (approximately 50-60%). If emraclidine fails to replicate its Phase II efficacy, or if unexpected safety issues emerge at scale, the acquisition would represent a significant capital misallocation that would not be recoverable through the remaining Cerevel assets alone.

Inflation Reduction Act and Pricing Pressure. The IRA's Medicare drug price negotiation framework is scheduled to expand its coverage over time, with additional drugs selected for negotiation each year. While AbbVie's newest assets (Skyrizi, Rinvoq) have longer runways before they become eligible for negotiation, the political trajectory is clearly toward broader pricing constraints on branded pharmaceuticals. State-level drug pricing legislation and international reference pricing could compound the pressure.

Balance Sheet Leverage from Acquisitions. AbbVie's acquisition strategy — $63 billion for Allergan, $21 billion for Pharmacyclics, $8.7 billion for Cerevel, plus smaller deals — has left the company with meaningful balance sheet debt. While the $17.8 billion in annual FCF provides ample coverage, the leverage constrains AbbVie's flexibility to pursue transformative M&A should an opportunity arise. Debt reduction is a stated priority, but the timeline for returning to investment-grade comfort levels depends on continued strong cash generation.

Conclusion

AbbVie has accomplished what many analysts considered improbable: it has replaced the revenue from the largest patent cliff in pharmaceutical history while simultaneously diversifying into neuroscience, aesthetics, and oncology, all without cutting the dividend or compromising the pipeline investment. FY2025 revenue of $61.16 billion, growing at 10.6%, is the definitive proof point. Skyrizi and Rinvoq are not merely Humira replacements — they are superior assets with broader label potential, better clinical profiles, and longer patent runways. The Cerevel acquisition adds genuine optionality in neuroscience, a therapeutic area where AbbVie's existing Botox franchise provides commercial infrastructure and physician relationships.

At a forward P/E of 14.2x with a 3.8% dividend yield and $17.8 billion in free cash flow, AbbVie offers a rare combination of value, income, and growth in a pharmaceutical sector increasingly bifurcated between expensive GLP-1 plays and challenged patent-cliff stories. We rate the stock Buy with a $250 price target and view current levels as an attractive entry point for investors seeking healthcare exposure with downside protection from the dividend and upside from pipeline catalysts.

For readers interested in other sector analyses, we recommend our coverage of Netflix's transformation into an ad-powered streaming platform as a parallel example of a company successfully navigating a business model transition, and our analysis of AMD's AI chip catalyst and TSMC partnership for insight into how companies leverage platform shifts to re-rate their equity.

Is AbbVie stock a buy after the Humira patent cliff?

We rate AbbVie a Buy with a $250 price target, representing approximately 22% upside from the current price of $205.48. The Humira patent cliff — which saw the drug's revenue decline from $21.2 billion at peak to an estimated $7.5 billion in FY2025 — has been successfully offset by the rapid growth of Skyrizi and Rinvoq, which are approaching a combined $27 billion annual run rate. Total company revenue grew 10.6% in FY2025 to $61.16 billion despite the Humira erosion, demonstrating the durability of the franchise transition. At a forward P/E of 14.2x with a 3.8% dividend yield and $17.8 billion in free cash flow, the risk/reward favors buyers.

What is AbbVie's Skyrizi and Rinvoq growth outlook?

Skyrizi and Rinvoq are AbbVie's most important growth drivers, with combined revenue approaching $27 billion on an annualized basis. Skyrizi, an IL-23p19 inhibitor approved for psoriasis, psoriatic arthritis, and Crohn's disease, is growing at over 50% year-over-year and is widely expected to become a $20 billion peak-sales product. Rinvoq, a JAK inhibitor approved across five indications including rheumatoid arthritis and atopic dermatitis, is tracking toward $10 billion+ in peak sales. Both drugs have patent protection extending into the early 2030s, providing a long runway of growth before biosimilar competition becomes a factor. Label expansions, particularly Skyrizi in ulcerative colitis, represent additional upside catalysts.

How does AbbVie's dividend compare to pharma peers?

AbbVie is a Dividend Aristocrat with 52 consecutive years of dividend increases, a streak inherited from parent company Abbott Laboratories and maintained through every year since the 2013 spinoff. The current dividend yield of approximately 3.8% is among the highest in large-cap pharma, significantly above the S&P 500 Healthcare sector average of roughly 1.5%. The dividend is well-supported by $17.8 billion in annual free cash flow, representing a payout ratio of approximately 57% on a cash basis. Management has signaled continued mid-single-digit annual dividend growth, consistent with the company's historical pattern.

What is the significance of AbbVie's Cerevel acquisition?

AbbVie acquired Cerevel Therapeutics in 2024 for $8.7 billion, gaining access to a neuroscience pipeline anchored by emraclidine, a selective M4 muscarinic agonist in Phase III trials for schizophrenia. If successful, emraclidine would represent the first mechanistically novel approach to schizophrenia in decades, addressing a $10 billion+ market where current treatments cause significant metabolic side effects. The deal also includes tavapadon for Parkinson's disease. Phase III data for emraclidine is expected in 2027 and represents a significant binary catalyst. The acquisition complements AbbVie's existing neuroscience portfolio, including Botox for migraine, Vraylar for bipolar disorder and depression, and Ubrelvy for acute migraine.

What are the biggest risks to AbbVie stock?

The five primary risks are: (1) faster-than-expected Humira biosimilar erosion creating a temporary revenue gap before Skyrizi/Rinvoq fully scale; (2) regulatory and safety risks specific to Rinvoq as a JAK inhibitor, including the class-wide FDA boxed warning and potential prescribing restrictions; (3) binary pipeline risk from the Cerevel acquisition, particularly the Phase III readout for emraclidine in schizophrenia; (4) Inflation Reduction Act pricing pressure as Medicare drug negotiations expand to cover more branded pharmaceuticals; and (5) balance sheet leverage from a decade of large-scale M&A that constrains financial flexibility. Of these, the JAK inhibitor safety risk and emraclidine Phase III binary are the most consequential near-term uncertainties.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a solicitation, or a recommendation to buy or sell any securities. The analysis reflects the author's opinion based on publicly available information and proprietary Edgen research as of the publication date. All investments carry risk, including the potential loss of principal. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions. Edgen and its analysts may hold positions in securities discussed. Price targets and ratings reflect 12-month forward expectations and are subject to revision.

추천합니다