Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

Micron vs SanDisk: The Two Faces of the AI Memory Supercycle — Why MU's HBM Wins Still Matter More Than SNDK's NAND Frenzy

· Apr 16 2026

Summary

- MU and SNDK both posted record Q2 FY2026 results and are leveraged to the same AI memory supercycle, but the risk/reward at current prices is meaningfully different: MU at $465.66 trades ~10% above its probability-weighted fair value of $423, while SNDK at $944.51 trades ~35% above its probability-weighted fair value of $698

- Micron's HBM franchise is the crown jewel: $2.18B in HBM revenue in Q2 FY2026 (+22% QoQ), with HBM3E 36GB already shipping in volume and HBM4 sampling to six partners — positioning MU to capture approximately 20% of the HBM TAM in CY2026 alongside SK Hynix and Samsung

- SanDisk has rallied 2,228% since its February 2025 spinoff from Western Digital and +301% year-to-date in 2026, with enthusiasm driven by BiCS10 (332-layer NAND, co-developed with NVIDIA) and the speculative "High Bandwidth Flash" (HBF) opportunity, but the stock is now pricing in a flawless execution scenario that has a historically compressed margin for error

- Buy MU for the clearest multi-year HBM visibility at a reasonable multiple; Hold SNDK and wait for either a meaningful pullback or concrete BiCS10/HBF revenue traction before adding — the Nasdaq-100 inclusion on April 20, 2026 creates passive flow support but does not change the underlying valuation math

Why Memory Matters Now: The AI Supercycle Has Two Engines

The memory semiconductor industry is experiencing a once-in-a-decade transformation. Unlike logic chips — where the market has largely consolidated around TSMC's foundry dominance — memory remains an oligopolistic but highly competitive market structured around two distinct technologies: DRAM (dynamic random-access memory, used for processor-adjacent volatile storage) and NAND flash (non-volatile storage for SSDs and mobile devices). For more than a decade, memory stocks were viewed as cyclical commodity plays with violent boom-bust cycles. The AI revolution has fundamentally changed that narrative.

The change is most visible in High Bandwidth Memory (HBM), a specialized 3D-stacked DRAM architecture originally developed for graphics cards that has become the indispensable companion to every AI accelerator shipped. An NVIDIA H100 GPU contains 80GB of HBM3. The newer H200 contains 141GB of HBM3e. The upcoming Blackwell B200 platform is designed with 192GB of HBM3e. Each successive generation doubles or triples the HBM per GPU, and hyperscaler capex — Microsoft, Google, Amazon, Meta combined spending over $350 billion on AI infrastructure in 2026 — is being deployed almost entirely into systems that consume HBM in volume. The result is that HBM, which represented less than 5% of the DRAM market by revenue in 2023, is expected to exceed 50% by 2027. This is the first engine of the AI memory supercycle, and Micron is one of only three players (alongside SK Hynix and Samsung) with the technical capability to manufacture it.

The second engine is the quieter but equally important transformation of enterprise NAND storage. AI inference workloads — the day-to-day operation of trained models serving user queries — require vast amounts of fast, high-capacity SSD storage to hold model weights, cache activations, and stream training data. Data center SSDs built on modern QLC NAND now ship in capacities of 122TB per drive, and the transition from traditional hard disk drives to enterprise SSDs is accelerating. SanDisk, freshly spun out of Western Digital in February 2025, is now a pure-play NAND company benefiting directly from this transition. Its BiCS10 architecture — a 332-layer NAND technology co-developed with NVIDIA — positions SanDisk for the next wave of AI-optimized storage.

What is unusual, and what makes this comparison article necessary, is that the market is currently pricing these two engines of the same supercycle very differently. Micron trades at roughly 12x forward earnings on AI-supercharged fundamentals. SanDisk trades at approximately 20x forward earnings after a near-quadrupling in four months. Both are Buy-rated by the majority of Wall Street analysts. The question for investors is which provides better risk-adjusted returns from here.

Two Companies, Two Paths: A Business Model Comparison

Micron Technology is a fully integrated memory manufacturer with operations spanning DRAM, NAND, and NOR memory. Headquartered in Boise, Idaho and led by CEO Sanjay Mehrotra (a veteran of SanDisk's original incarnation and Spansion), Micron has been a public company for decades and a Fortune 500 constituent throughout the modern memory era. Its business is structured around four segments: the Compute and Networking Business Unit (CNBU) — which houses HBM and data center DRAM and is currently the primary growth engine; the Mobile Business Unit (MBU) serving smartphone OEMs; the Storage Business Unit (SBU) for NAND-based client and enterprise SSDs; and the Embedded Business Unit (EBU) for automotive and industrial applications. In Q2 FY2026, CNBU represented approximately 57% of revenue and grew 120%+ year-over-year, driven almost entirely by HBM and high-capacity DDR5 server DRAM.

SanDisk Corporation, by contrast, is a pure-play NAND flash company that emerged from Western Digital's February 2025 spinoff. Under CEO David Goeckeler (who also led the parent company through the spinoff) and with a board that includes technology veterans from across the enterprise storage industry, SanDisk operates with a sharper, more focused strategy than its more diversified peers. Its business spans Cloud (the highest-growth segment — 24% of revenue in Q2 FY2026, up 185% year-over-year), Client (60% of revenue, including enterprise and consumer SSDs), and Consumer (removable flash cards and portable drives). SanDisk's manufacturing operations are primarily conducted through a long-standing joint venture with Kioxia in Japan — a partnership that both anchors the company's cost structure and creates ongoing speculation about a potential merger or closer integration.

The philosophical difference is important. Micron is a horizontally integrated memory leader: when DRAM cycles up, HBM cycles up, and NAND cycles up, Micron benefits from all three. When any one cycles down, the others often cushion the impact. SanDisk is a vertically focused NAND specialist: when NAND pricing strengthens and enterprise SSD demand surges, SanDisk leverages upside disproportionately. When NAND oversupply returns (as happened in 2023-2024), SanDisk suffers disproportionately. Investors in Micron are buying a diversified exposure to the memory complex. Investors in SanDisk are buying a concentrated, higher-beta exposure to NAND specifically.

Operating Performance: The Numbers Side-by-Side

Both companies reported Q2 FY2026 results within a few weeks of each other, and both exceeded consensus meaningfully. But the magnitude and composition of the beats tell different stories.

Micron Q2 FY2026 (Quarter Ended Feb 26, 2026)

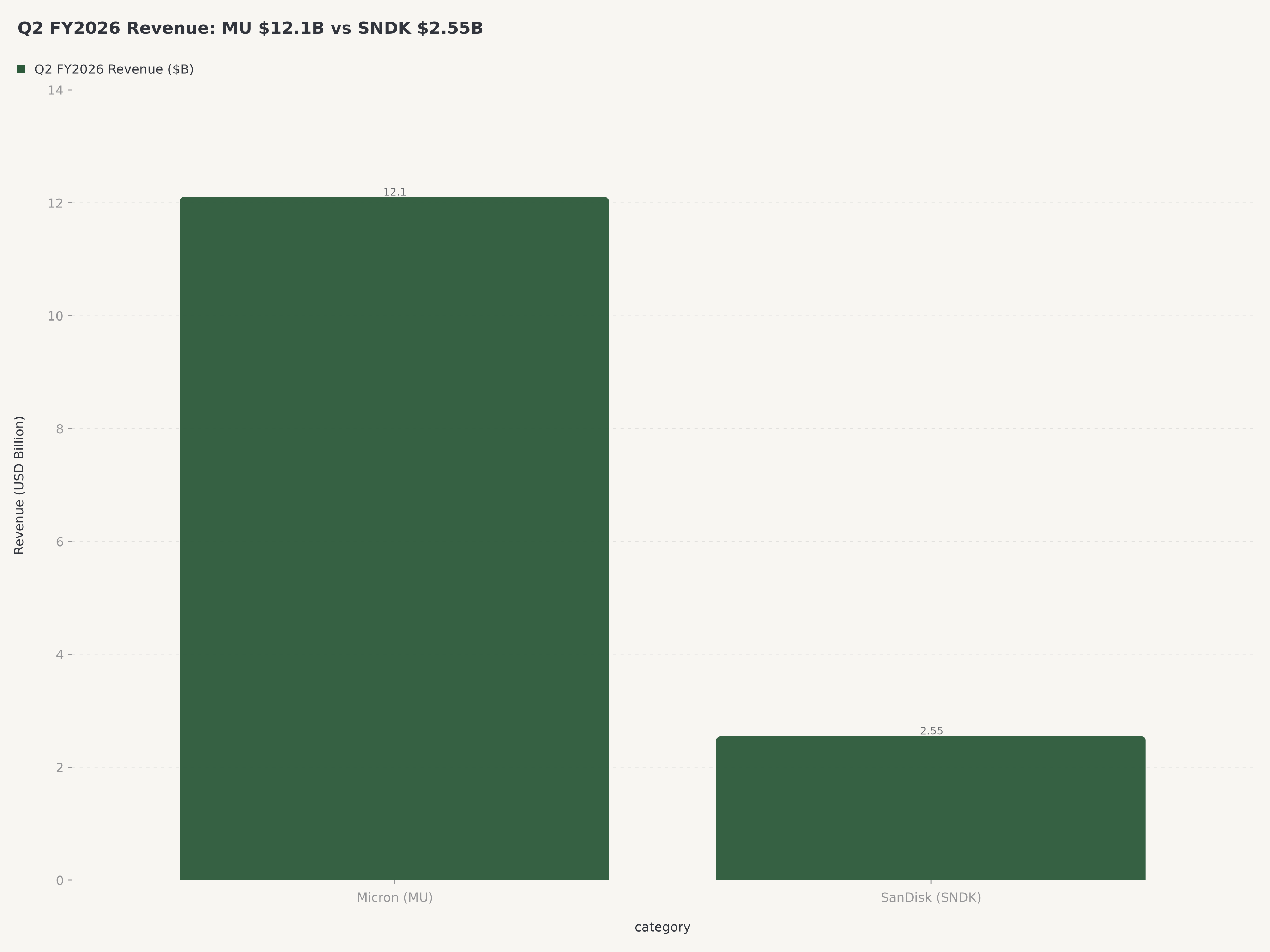

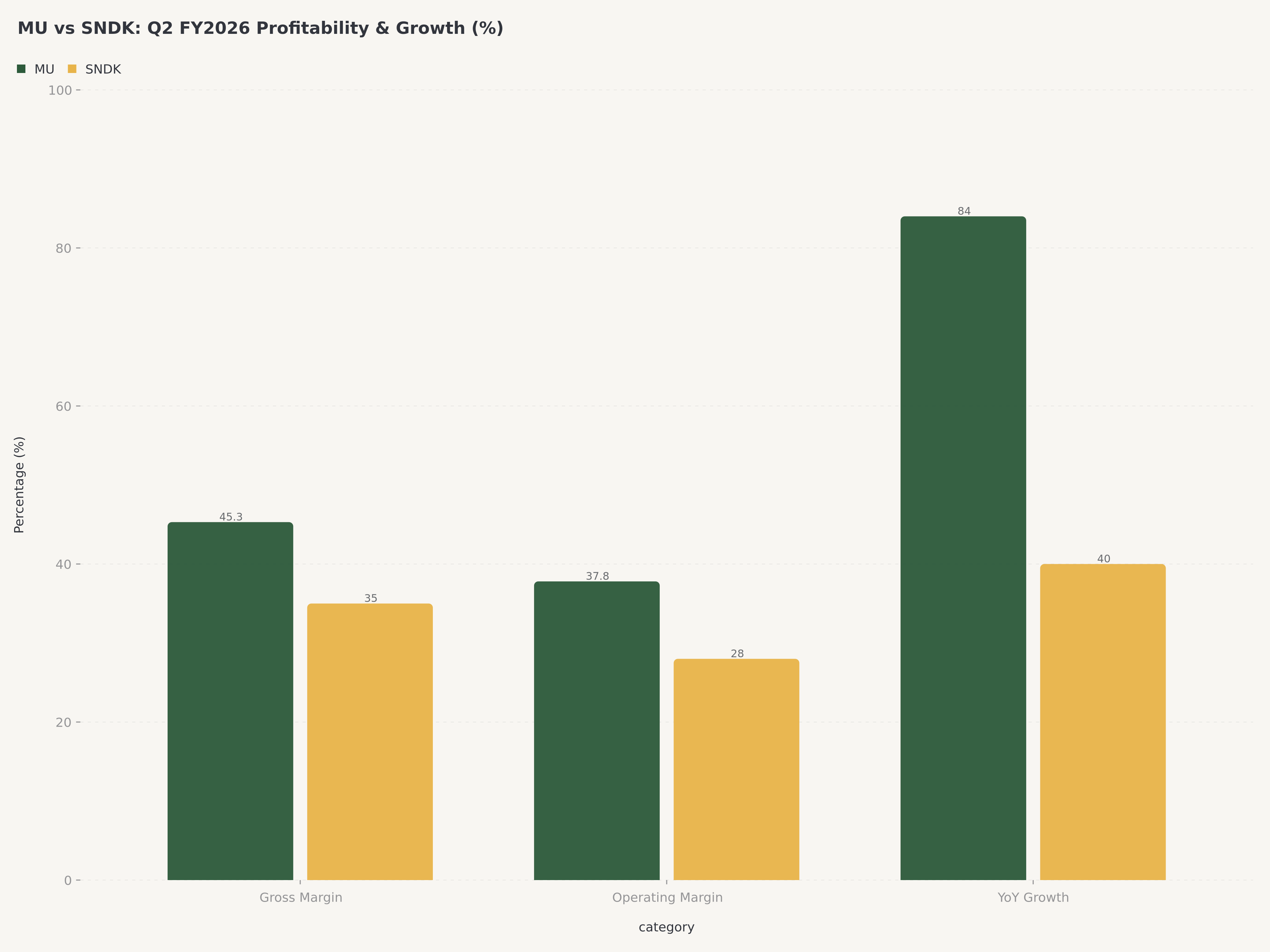

Micron delivered revenue of $12.1 billion (+84% YoY, +17% sequentially), a quarterly record. Non-GAAP diluted EPS came in at $3.22, beating consensus of $2.95 and representing the best quarterly profitability in the company's history. GAAP gross margin expanded to 45.3%, up from 22.5% in the year-ago quarter — a 23-point margin expansion that reflects both pricing power in HBM and the mix shift toward higher-margin data center products. Non-GAAP operating margin hit 37.8%, also a record.

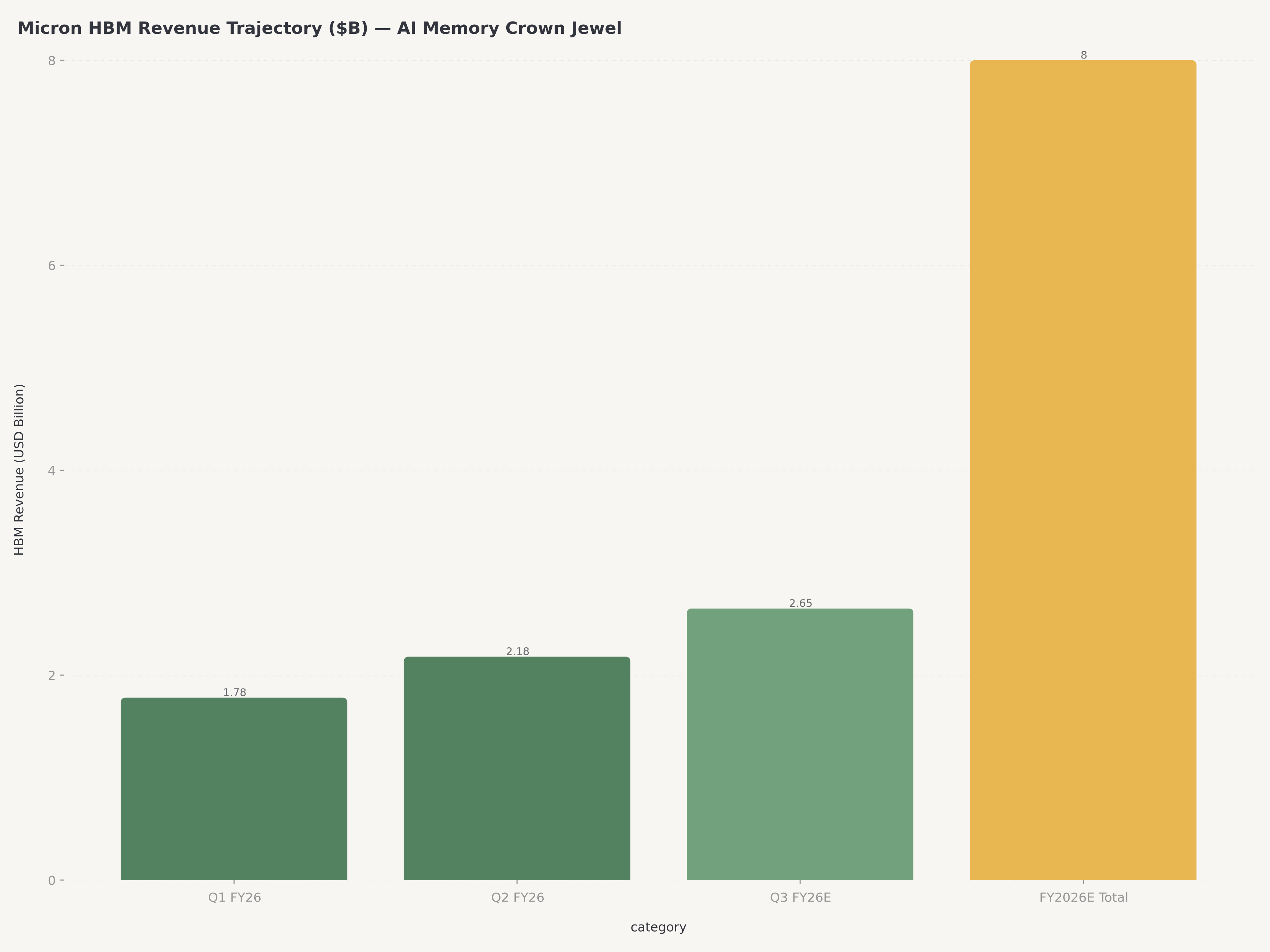

The segment breakdown tells the AI story clearly. CNBU (compute and networking) generated approximately $6.9 billion in revenue, of which HBM alone was $2.18 billion — up from $1.78 billion in Q1 FY2026 (+22% sequentially). Management guided that HBM revenue will exceed $8 billion in fiscal 2026, implying an exit run-rate of approximately $10-12 billion annualized by the end of the fiscal year. HBM3E 36GB is already shipping in volume to multiple hyperscaler customers, and HBM4 samples are being qualified with six partners for production ramp in calendar 2026-2027. Micron targets approximately 20% HBM market share in CY2026, up from an estimated 15% in 2025.

Q3 FY2026 guidance (announced at the Q2 earnings call) calls for revenue of approximately $12.5 billion plus or minus $500 million, with non-GAAP gross margin expected to expand further to the 46-47% range and non-GAAP EPS guided to approximately $3.25. Management characterized the outlook as "visibility that now extends multiple quarters into fiscal 2027" on HBM specifically, a notable shift in language from the more cautious quarterly commentary typical of memory companies.

SanDisk Q2 FY2026 (Quarter Ended Dec 26, 2025, reported Jan 2, 2026)

SanDisk delivered revenue of $2.55 billion (+40% YoY, +17% sequentially), meaningfully above the high end of prior guidance of $2.40-2.50 billion. Non-GAAP EPS came in at $3.00, above consensus of $2.94. Non-GAAP gross margin expanded dramatically to 35%, up from 23% in the year-ago quarter — a 12-point margin expansion driven by the mix shift toward enterprise and datacenter SSDs at higher average selling prices. Free cash flow reached $843 million in Q2 alone, a figure that would have been nearly unthinkable in the pre-spinoff NAND landscape.

The segment breakdown highlights where the growth is concentrated. The Datacenter segment contributed approximately 24% of revenue and grew 185% year-over-year, reflecting the explosive demand for enterprise SSDs built on SanDisk's advanced 3D NAND technology. Client, which includes both enterprise endpoint SSDs and consumer SSDs, represented 60% of revenue and grew in the 40-50% range. Consumer (removable storage) was the smallest and slowest-growing segment at 16% of revenue.

Q3 FY2026 guidance is notably aggressive: revenue of $3.20-3.40 billion (implying approximately 25-33% sequential growth from Q2), non-GAAP gross margin of 36-42%, and non-GAAP EPS of $3.35-4.45. The mid-point of this EPS range — $3.90 — would represent a 30% sequential increase from Q2's $3.00, and the range itself is unusually wide (±14% from the midpoint), reflecting high uncertainty about memory pricing trajectory, BiCS10 ramp timing, and the HBF opportunity monetization.

Head-to-Head Financial Summary

The scale disparity is important to internalize. Micron's Q2 FY2026 revenue of $12.1 billion is approximately 4.7x SanDisk's $2.55 billion. On an annualized run-rate basis, Micron is a ~$50 billion revenue company; SanDisk is a ~$10 billion revenue company. Micron's gross margins are materially higher (GAAP 45% vs non-GAAP 35% — roughly comparable when adjusting for accounting methodology). But SanDisk's sequential growth momentum is greater, both in absolute terms and in the guidance trajectory.

The Valuation Gap: Priced for Execution vs Priced for Perfection

This is where the comparison article becomes concrete. Both companies presented four-scenario valuation models in their respective Edgen 360° reports. The resulting probability-weighted fair value calculations produce meaningfully different conclusions.

Micron Valuation Scenarios (from Edgen 360° Report, Mar 21, 2026)

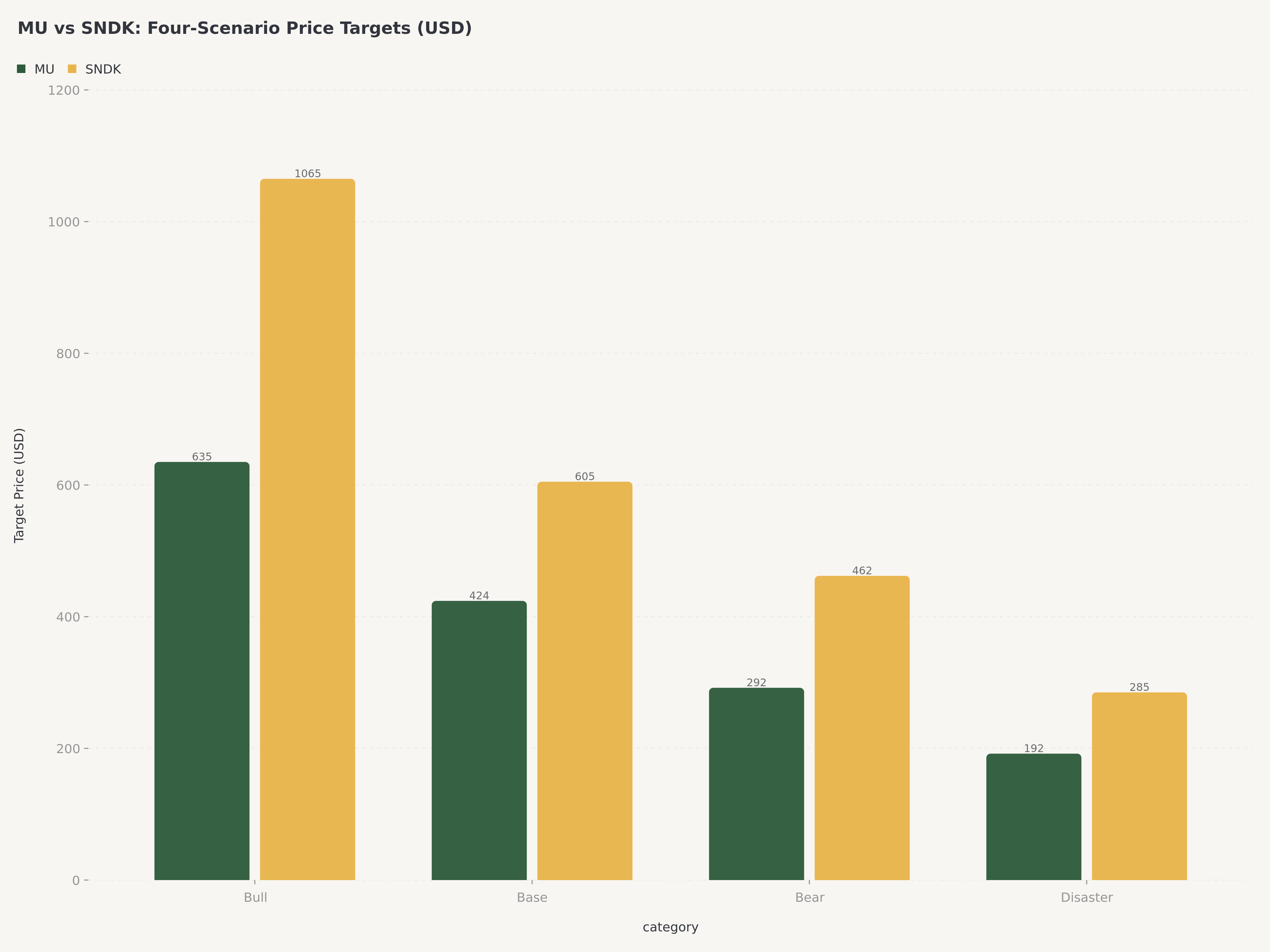

Scenario | Price Range | Market Cap Range | Multiplier | Probability |

Bull (Strong Growth + Favorable Macro) | $605–665 | $680–750B | 1.50x–1.65x | 35% |

Base (Weak Growth + Favorable Macro) | $403–445 | $450–500B | 1.00x–1.10x | 20% |

Bear (Strong Growth + Unfavorable Macro) | $262–322 | $295–363B | 0.65x–0.80x | 30% |

Disaster (Weak Growth + Unfavorable Macro) | $161–222 | $181–250B | 0.40x–0.55x | 15% |

Probability-weighted fair value: approximately $423. Current price (April 14, 2026): $465.66. The market is currently pricing Micron roughly 10% above the probability-weighted central estimate, with meaningful asymmetric upside to the Bull case (approximately +30-43% to the Bull midpoint of $635) that is not fully reflected. The Bull case specifically requires HBM execution — which, based on Q2 FY2026 results and Q3 guidance, is arguably already in progress.

SanDisk Valuation Scenarios (from Edgen 360° Report, Apr 12, 2026)

Scenario | Price Range | Market Cap Range | Multiplier | Probability |

Bull (Strong Growth + Favorable Macro) | $1,030–1,100 | $152–162B | 1.45x–1.55x | 40% |

Base (Weak Growth + Favorable Macro) | $570–640 | $84–94B | 0.80x–0.90x | 15% |

Bear (Strong Growth + Unfavorable Macro) | $425–500 | $63–74B | 0.60x–0.70x | 30% |

Disaster (Weak Growth + Unfavorable Macro) | $250–320 | $37–47B | 0.35x–0.45x | 15% |

Probability-weighted fair value: approximately $698. Current price (April 14, 2026): $944.51. The market is currently pricing SanDisk approximately 35% above the probability-weighted central estimate. The Bull case of $1,065 midpoint offers only approximately 13% upside from current levels, while the probability-weighted downside (Bear + Disaster = 45% combined probability) implies losses of 30-60%. The risk/reward at current prices is asymmetric in the opposite direction from Micron.

Stated plainly: at today's prices, Micron offers approximately 37% upside to its Bull case vs 38% downside to its Bear case, a roughly symmetric risk profile weighted by probability toward the bull outcome. SanDisk offers approximately 13% upside to its Bull case vs 45-55% downside to its Bear/Disaster cases, an asymmetric risk profile weighted by probability toward the downside despite the 40% Bull probability.

The AI Story, Differentiated: HBM Dominance vs NAND Acceleration

Both companies are AI beneficiaries, but through different mechanisms.

Micron's AI Exposure Is HBM-Centric and Multi-Year Visible. Every AI accelerator chip — whether NVIDIA's Blackwell, AMD's MI350, or custom silicon from Google, Amazon, or Meta — requires HBM. The number of accelerators shipped in 2026 is expected to exceed 8 million units, and the HBM content per accelerator is growing as each generation consumes more capacity. Micron has shipped HBM3E in volume to NVIDIA since mid-2025 and is one of only two suppliers of the 12-Hi 36GB HBM3E configuration that powers the highest-end AI training systems. HBM4, sampling now, will extend this leadership into 2027-2028. The HBM revenue stream is characterized by long-term volume agreements with hyperscaler customers, multi-quarter visibility, and pricing stability that looks more like specialty chemicals than traditional commodity memory.

SanDisk's AI Exposure Is NAND-Inference-Adjacent and Emerging. SanDisk's AI narrative rests on two pillars. First, enterprise SSD demand for AI inference workloads has accelerated as hyperscalers deploy more capacity to serve models. The Datacenter segment's 185% YoY growth in Q2 FY2026 is the concrete evidence. Second, BiCS10 — the 332-layer NAND technology co-developed with NVIDIA and scheduled for volume production ramp in 2027 — positions SanDisk to benefit from the next generation of AI-optimized storage. Third, and most speculatively, the "High Bandwidth Flash" (HBF) opportunity envisions a future where SanDisk's highest-density NAND can complement (or in some scenarios, partially replace) HBM for AI inference applications. The critical question is how much of this is fundamental vs narrative: current AI revenue from SanDisk is real and growing, but HBF specifically remains a 2027-2028 potential rather than a 2026 contributor.

The analytical conclusion is that Micron's AI exposure is validated, in-production, and extending; SanDisk's AI exposure is partially validated (enterprise SSDs) and partially aspirational (HBF).

To understand the broader AI semiconductor ecosystem, explore our analysis of Credo Technology's AI networking and connectivity thesis and our look at Tencent's AI-driven platform transformation in 2026.

Competitive Positioning: DRAM Oligopoly vs NAND Commodity

The memory industry's structure has historically been the primary determinant of company profitability, and Micron and SanDisk occupy very different positions within it.

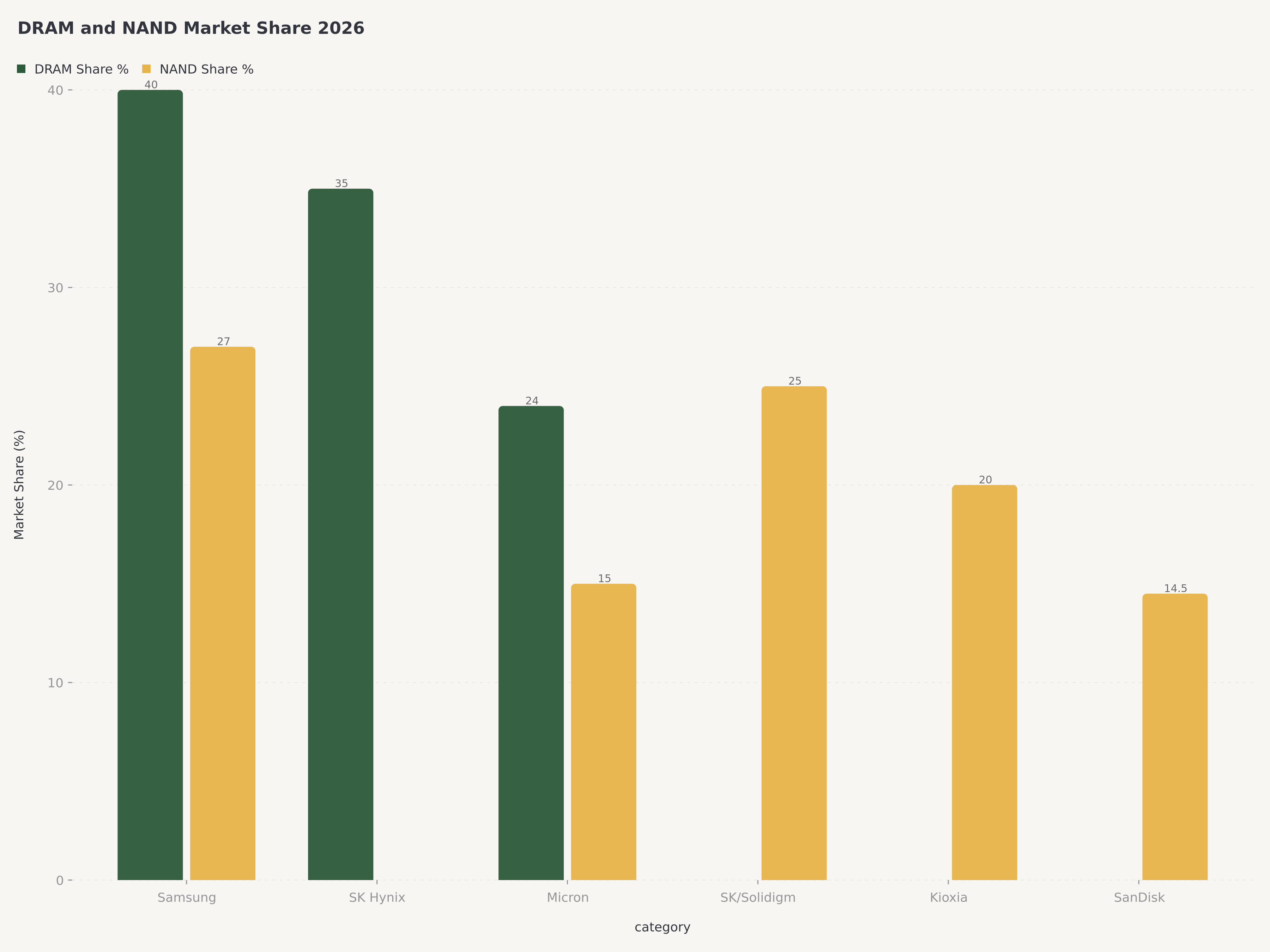

DRAM (Micron's primary franchise): The industry has consolidated to three major players — Samsung (~40% share), SK Hynix (~35%), and Micron (~24%). This 95%+ combined market share, plus substantial barriers to entry (technology, capital requirements, customer relationships), has historically produced better-than-average margins across the cycle. In HBM specifically, SK Hynix currently leads (approximately 50% share), Samsung follows (~30%), and Micron has aggressively ramped to approximately 20%. Micron's trajectory is upward in HBM share, which matters because HBM carries gross margins roughly 3-4x higher than commodity DRAM.

NAND (SanDisk's primary franchise): The industry has five major players — Samsung (~27%), SK Hynix/Solidigm (~25%), Kioxia (~20%), Micron (~15%), and SanDisk (~14.5%). The larger number of competitors, lower capital requirements vs DRAM, and higher propensity for boom-bust pricing cycles has historically produced lower and more volatile margins than DRAM. SanDisk's #5 position means it has less pricing power than Samsung or SK Hynix and must differentiate through technology (BiCS10) and partnerships (NVIDIA, Kioxia) to compete effectively.

HBM (the crown jewel of AI memory): This is where Micron plays and SanDisk does not. The HBM market was approximately $18 billion in 2024, is forecast to reach $85 billion by 2029, and carries gross margins of 55-65% based on industry estimates. Only three companies (SK Hynix, Samsung, Micron) have the technical capability to manufacture HBM at scale. SanDisk has no HBM presence today and its HBF concept is not a true substitute — HBM is on-package with the GPU, while HBF would operate at the system level.

Catalysts and Risks

Micron Catalysts (Near-term)

- Fiscal Q3 FY2026 earnings (June 2026) — potential beat on $12.5B revenue guide, further HBM upside

- HBM4 production ramp announcements (late 2026)

- HBM TAM expansion as B200 Blackwell deploys in volume

- Third production facility (Taichung) — $1.8B investment, initial contribution expected fiscal 2028

Micron Risks

- Memory cycle risk — while AI demand is structural, commodity DRAM and NAND can still oversupply

- Geopolitical exposure — Taiwan facility, China market access

- HBM supply-chain concentration (HBM3E advanced packaging capacity constrained)

- CapEx intensity — $13.8B in fiscal 2025 and rising to $16-18B in fiscal 2026

SanDisk Catalysts (Near-term)

- Nasdaq-100 inclusion — April 20, 2026 (passive flow support)

- Fiscal Q3 FY2026 earnings (late April 2026) — beat on $3.20-3.40B guide

- BiCS10 production ramp — initial revenue from NVIDIA partnership expected 2027

- Potential Kioxia consolidation — 12-24 month timeline, could create pricing power

- HBF (High Bandwidth Flash) positioning for AI inference — 2027-2028

SanDisk Risks

- Valuation stretched after 2,228% spinoff rally and +301% YTD in 2026

- NAND oversupply risk — five-player market with history of rapid pricing deterioration

- Execution risk on BiCS10 — technology ramps frequently slip

- HBF is aspirational — material revenue contribution is 2028+ at earliest

- Nasdaq-100 inclusion is fully priced in at current levels; event is likely a "sell the news"

- Customer concentration — approximately 70% of enterprise SSD revenue from top 10 hyperscaler/OEM customers

The Verdict: Buy MU, Hold SNDK

Micron (MU) — Buy, Price Target $550. Our price target reflects a blend of the Base case ($424) and Bull case ($635) weighted at 55%/45%, producing $518, rounded up to $550 to reflect the option value of upside from HBM4 ramp and continued DRAM pricing strength. At $465.66, Micron offers approximately 18% upside to our price target and a risk profile that is roughly symmetric. HBM execution is already proven, Q3 FY2026 guidance extends visibility, and the valuation multiple (~12x forward earnings) is reasonable for a company with structural secular tailwinds. Position sizing should reflect that Micron remains cyclical at heart — we do not recommend this as a core position in the absence of AI supercycle durability — but for investors who believe the current AI memory supercycle has multi-year legs, Micron offers the cleanest exposure with the best risk-adjusted return profile.

SanDisk (SNDK) — Hold, Price Target $750. Our price target reflects a blend of the Base case ($605) and Bull case ($1,065) weighted at 70%/30%, plus a 5% premium for passive flow support from Nasdaq-100 inclusion. This produces approximately $760, rounded to $750. At $944.51, SanDisk is trading approximately 20% above our price target. We rate Hold rather than Sell because (a) BiCS10 and HBF represent genuine optionality that could re-rate the stock higher, (b) Nasdaq-100 inclusion will create durable passive demand, and (c) the company's Q3 FY2026 guidance is credible. However, we cannot recommend adding positions at current levels. Investors holding SanDisk should consider trimming if the stock trades above $1,000 and would become more constructive below $800.

Risks to Our View

Risk to the Micron Buy Call: A sudden cyclical downturn in commodity DRAM or NAND pricing — driven by a slowdown in PC, smartphone, or enterprise IT spending — would compress Micron's margins disproportionately on the non-HBM portion of the business. If HBM ramp slips or NVIDIA delays Blackwell deployment, Micron's 2026 earnings trajectory could disappoint. Probability: 25-30%, already reflected in the Bear case scenario.

Risk to the SanDisk Hold Call: The biggest risk to our Hold call is that we are too cautious. BiCS10 production ramp could arrive earlier than 2027, HBF could achieve commercial validation by late 2026, and NAND pricing could sustain strength longer than expected. In this scenario, the Bull case probability should be revised higher, and the stock could move toward $1,100-1,200 during 2026. Conversely, the biggest risk to the other direction is that NAND oversupply returns — as it did in 2023-2024 — and SanDisk's pure-play NAND exposure crushes the stock back to the Bear case level of $425-500.

Conclusion

Micron and SanDisk are two of the cleanest public-market ways to express bullishness on the AI memory supercycle, but they are not equivalent investments at current prices. Micron offers diversified exposure across DRAM, NAND, and HBM — with HBM specifically providing the multi-year visibility and margin expansion that justifies a premium valuation. SanDisk offers concentrated, higher-beta exposure to NAND — with genuine AI tailwinds but aspirational catalysts and a stock price that has already captured the near-term optimism.

For investors building a new position in the memory complex today, we recommend Micron over SanDisk by a significant margin. For investors already long SanDisk after the post-spinoff rally, we recommend Hold with a watchful eye on execution — trim above $1,000, add below $800. The AI memory supercycle is real, multi-year, and favors companies with HBM exposure. Micron has it. SanDisk does not (at least not yet).

FAQ

Which memory stock is better in 2026 — MU or SNDK?

Micron (MU) offers better risk-adjusted returns at current prices. At $465.66, Micron trades at approximately 10% above its probability-weighted fair value of $423, with meaningful upside to its Bull case of $635 (35% probability). SanDisk at $944.51 trades approximately 35% above its probability-weighted fair value of $698, with limited upside to its Bull case of $1,065 (40% probability) but substantial downside (45% combined Bear+Disaster probability) to its Bear case of $462. We rate MU Buy with a $550 price target and SNDK Hold with a $750 price target.

What is HBM and why does it matter for Micron?

High Bandwidth Memory (HBM) is a specialized 3D-stacked DRAM architecture that provides dramatically higher memory bandwidth than conventional DRAM, making it essential for AI accelerator chips like NVIDIA H100, H200, and Blackwell B200. Micron is one of only three HBM manufacturers globally (alongside SK Hynix and Samsung), and HBM carries gross margins approximately 3-4x higher than commodity DRAM. Micron's HBM revenue grew to $2.18 billion in Q2 FY2026 (+22% QoQ) and is guided to exceed $8 billion in fiscal 2026, with target market share of approximately 20% in CY2026 — up from an estimated 15% in 2025.

Why has SanDisk stock risen so much in 2026?

SanDisk has risen approximately 301% year-to-date in 2026 (and 2,228% since its February 2025 spinoff from Western Digital) due to a combination of factors: (1) strong Q2 FY2026 results with revenue of $2.55 billion (+40% YoY), (2) AI-driven demand for enterprise datacenter SSDs (datacenter segment grew 185% YoY), (3) excitement around the BiCS10 332-layer NAND technology co-developed with NVIDIA, (4) speculation about the "High Bandwidth Flash" (HBF) opportunity that could challenge HBM for AI inference, and (5) anticipation of Nasdaq-100 inclusion on April 20, 2026 driving passive index flows.

What is the difference between DRAM and NAND, and which benefits more from AI?

DRAM is volatile memory (loses data when power is off) used for short-term processor-adjacent storage — this is where HBM fits as a specialized high-bandwidth variant. NAND is non-volatile flash memory used for longer-term storage in SSDs and mobile devices. AI training workloads require massive amounts of HBM (DRAM-based) to feed the GPU compute with model parameters. AI inference workloads require both HBM (to run the model) and NAND SSDs (to store model weights and cached results). Currently, HBM captures the majority of the AI-driven margin expansion because each AI accelerator consumes substantial and growing amounts of HBM, while NAND benefits more indirectly through enterprise SSD demand. Micron benefits from both; SanDisk benefits primarily from NAND.

What would change our Buy rating on MU or Hold rating on SNDK?

We would downgrade MU to Hold if: (1) HBM execution slips, with shipments or market share falling below guidance, (2) a cyclical memory downturn emerges in calendar Q3-Q4 2026, or (3) the stock rallies above $600 without corresponding earnings upside. We would upgrade SNDK to Buy if: (1) BiCS10 commercial validation arrives ahead of the 2027 schedule, (2) HBF achieves a meaningful design win with a hyperscaler, or (3) the stock pulls back meaningfully (below $800) without fundamental deterioration.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. The author and Edgen do not hold positions in the securities discussed. Past performance is not indicative of future results. Investors should conduct their own due diligence before making investment decisions.

Recommend