Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

IonQ's DARPA HARQ Moment: Why the Quantum Leader's 20% Rally Could Be the Start of a Multi-Year Re-Rating

· Apr 16 2026

Summary

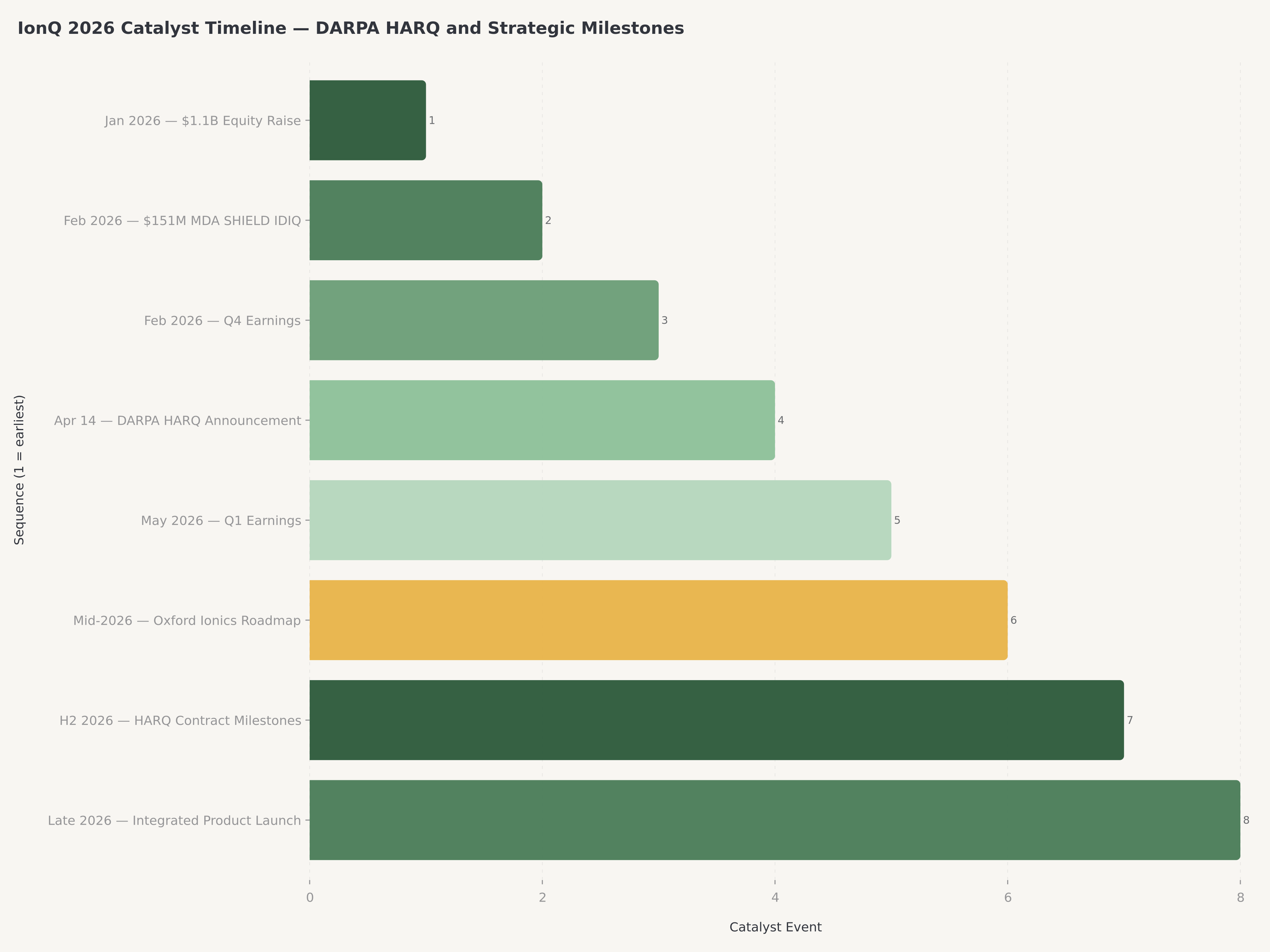

- IonQ rallied 19.9% on April 14, 2026 — from $29.76 to $35.73 — after the Defense Advanced Research Projects Agency (DARPA) announced IonQ as a participant in the Heterogeneous Architectures for Quantum (HARQ) program, a signature defense-science validation that joins the company's already formidable government customer list alongside AFRL, the Missile Defense Agency, and South Korea's KISTI.

- Underneath the catalyst, the investment case is bifurcated: IonQ is the clearest commercial pure-play in trapped-ion quantum computing (a full-stack model spanning hardware, cloud QCaaS on AWS/Azure/Google, and professional services), with bookings growth of approximately 429% year-over-year in FY2025 and remaining performance obligations of roughly $300M — but the company also burned through substantial cash to produce $83M of revenue and is not expected to reach adjusted EBITDA positive until the decade's end.

- The four-scenario valuation framework in the most recent Edgen 360° report implies a probability-weighted fair value of approximately $44 per share, against a current price of $35.73. We set a 12-month price target of $48, a modest premium reflecting the DARPA HARQ catalyst, the Oxford Ionics acquisition-driven technology roadmap acceleration, and the $3.3B cash cushion that funds the build-out through the next commercialization inflection.

- This is a Speculative Buy — appropriate as a 1–3% satellite position within a risk-tolerant portfolio, not a core holding. The 52-week range of $23.49–$84.64 tells you everything about the volatility profile. Investors should size for the possibility of both a further 100% re-rating toward the Bull case ($95–105) and a 50%+ drawdown to the Disaster case ($14) depending on the interplay between technical milestone execution and the 2026–2027 macro environment.

Why Quantum Matters Now: The DARPA HARQ Signal

For most of the past decade, quantum computing has been a "what if" asset class — a speculative bet on hardware physics that would, at some unknown future date, solve problems beyond the reach of classical supercomputers. That framing is no longer accurate. Quantum is transitioning from laboratory curiosity to national-security infrastructure, and the fastest way to see the change is to watch where the U.S. federal government is placing its bets.

On April 14, 2026, the Defense Advanced Research Projects Agency announced the participants in its Heterogeneous Architectures for Quantum (HARQ) program — a multi-year effort to develop quantum systems that combine heterogeneous architectures (mixing trapped-ion, superconducting, photonic, and neutral-atom qubits) to achieve utility-scale performance ahead of the trapped-ion-only or superconducting-only roadmaps. IonQ is one of the named participants. The market reaction was immediate and kinetic: IonQ's shares surged 19.9% intraday to close at $35.73, outpacing the broader quantum basket (D-Wave Quantum, Rigetti, Quantum Computing Inc.) by a clear margin.

The HARQ announcement matters for three overlapping reasons. First, it is a financial-commitment signal: DARPA contracts typically bring multi-year funding tied to specific milestones, and IonQ's existing government business — anchored by a $1.1M Air Force Research Laboratory (AFRL) contract, a $151M Missile Defense Agency SHIELD IDIQ contract signed in February 2026, and a partnership with South Korea's Korea Institute of Science and Technology Information (KISTI) — demonstrates that the government customer, once secured, tends to renew and expand. Second, it is a technological validation: DARPA's program office chose IonQ as one of a small number of commercial partners in a highly competitive solicitation, an implicit endorsement of the company's trapped-ion architecture and its integrated software-hardware stack. Third, and perhaps most importantly, HARQ addresses the single biggest bear thesis on trapped-ion quantum — that superconducting (IBM, Google) or neutral-atom (QuEra, Atom Computing, Infleqtion) approaches will prove more scalable — by explicitly funding heterogeneous architectures in which IonQ's trapped-ion expertise is a feature, not a vulnerability.

In short, HARQ reframes IonQ from "one of several quantum hopefuls" to "one of a handful of companies that the U.S. national security apparatus is betting will still be relevant in 2030."

The Company: A Full-Stack Trapped-Ion Quantum Platform

IonQ Inc. is a pure-play quantum computing company that operates what it describes as a "full-stack" platform — meaning it designs and manufactures its own trapped-ion quantum processors, builds the control software and compilers that program them, and delivers them to end users through both direct hardware sales and Quantum-as-a-Service (QCaaS) offerings on Amazon Web Services, Microsoft Azure, and Google Cloud. Trapped-ion computing, the technology underlying IonQ's flagship systems (the Forte and Forte Enterprise platforms), uses individual ytterbium ions held in electromagnetic traps as qubits — a qubit modality prized for its long coherence times, high-fidelity two-qubit gates, and all-to-all qubit connectivity. The trade-off is that trapped-ion systems are historically slower to execute and have scaled to fewer qubits per chip than superconducting competitors.

The company's strategic posture in 2025–2026 has been unusually aggressive for a company of its size. Through a combination of organic investment and a rapid-fire M&A cadence, IonQ has assembled a portfolio of businesses across the quantum value chain: Oxford Ionics (acquired for approximately $1.08B in mid-2025) for its ion-trap chip technology and its relationship with U.K. Ministry of Defence; Qubitek (acquired for approximately $118M) for control-system expertise; Lightsynq (photonic interconnects); Capella Space (satellite imagery and space-based networking applications); Vector Atomic (navigation and timing); SkyWater Technology (foundry integration for quantum photonics); and the strategic integration assets from ID Quantique (IDQ), which brought post-quantum cryptography and the $151M Missile Defense Agency SHIELD IDIQ contract into the IonQ umbrella. The acquisition strategy is both offensive (consolidating talent and IP in a fragmented industry) and defensive (locking down the next technological platform before competitors can reach it).

On the management side, Niccolò De Masi joined as CEO in 2025, bringing operational experience from Forte Biosciences and public-market exposure. He leads a technical bench that includes Peter Chapman (now Executive Chairman), co-founder Christopher Monroe (one of the original trapped-ion physicists), and a board with deep defense and quantum-industry representation including the former U.S. Director of National Intelligence and advisors from NGA and former DoD CISO Katie Arrington. The governance structure emphasizes national-security engagement — important given the growing share of government revenue — and long-term R&D execution.

Operating Performance: Hyper-Growth Paired with Heavy Losses

IonQ's Q4 2025 and full-year FY2025 results, reported on February 26, 2026, illustrated both the company's exceptional growth trajectory and its substantial burn rate.

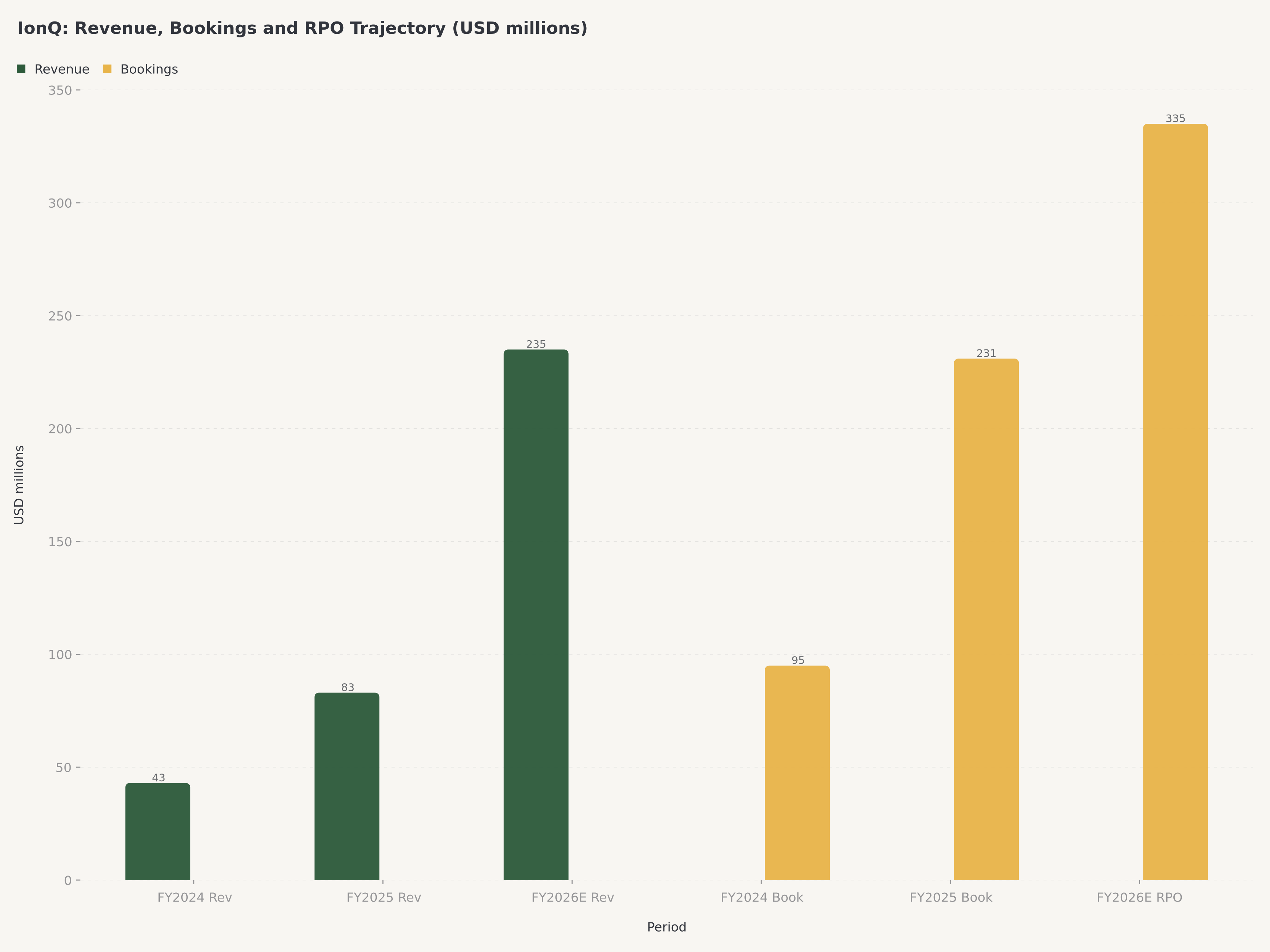

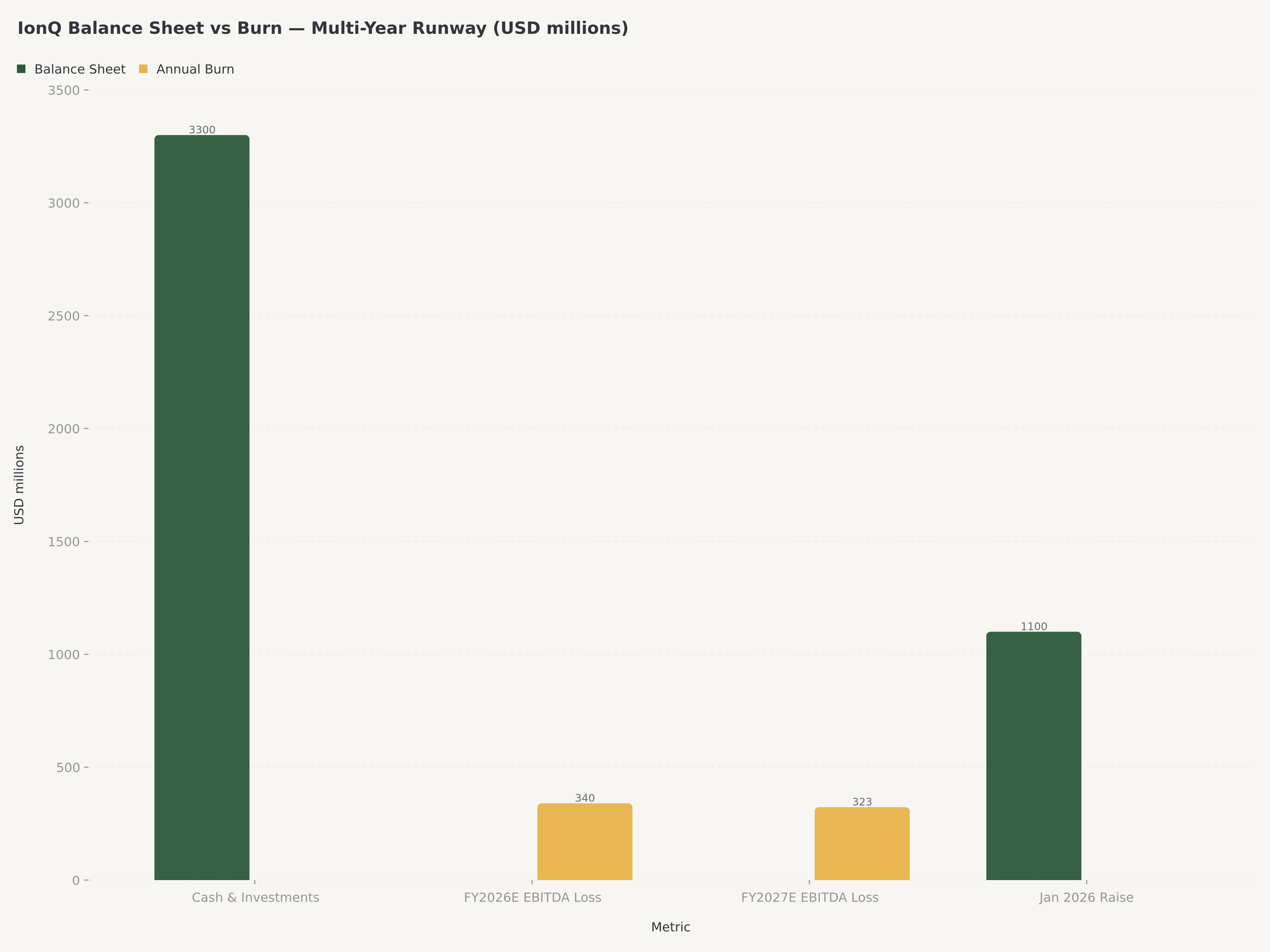

Revenue: Q4 2025 revenue came in at approximately $22M, narrowly missing consensus by roughly $0.48M. Full-year FY2025 revenue reached $83.13M, landing comfortably within the $75–95M guidance range. The deeper story is in bookings: IonQ reported Q4 2025 bookings of approximately $95.6M and full-year 2025 bookings of approximately $230.5M — roughly 429% year-over-year growth — with remaining performance obligations (RPO, the contracted-but-undelivered revenue backlog) reaching approximately $300M by year-end. Management is guiding to RPO of $325–340M by end of FY2026, a figure that provides tangible visibility into the next 18–24 months.

Profitability: The profitability side is the other half of the story, and it requires careful parsing of GAAP versus non-GAAP metrics. On a GAAP basis, Q4 2025 reported net income of approximately +$753.7M — but this headline figure is almost entirely driven by a roughly $950M non-cash fair-value gain on warrant liabilities (a mark-to-market accounting adjustment tied to the share-price decline during the quarter) and is not indicative of underlying operating performance. Stripping out that non-cash item, the operating picture is sharply negative: Q4 2025 Adjusted EBITDA loss was approximately -$186.8M, reflecting significant stock-based compensation associated with post-merger integration and M&A purchase accounting, plus genuine operating losses on a high R&D base. The fiscal 2026 consensus Adjusted EBITDA loss has widened to approximately -$340M — meaningfully worse than the prior consensus — reflecting the full-year impact of Oxford Ionics integration, heightened R&D across the post-acquisition roadmap, and SG&A scaling as the company builds its commercial sales organization. The 2027 consensus EPS is approximately -$2.92 with Adjusted EBITDA of approximately -$323M, indicating that losses will remain substantial for at least two more fiscal years.

Cash and Capital: Offsetting the losses is a cash fortress. IonQ raised approximately $1.1B in a January 2026 equity offering at approximately $55 per share — capturing equity financing near the 52-week high and well above today's $35.73 — and ended the quarter with approximately $3.3B in cash and short-term investments. Against a projected 2026 cash burn of approximately $340M (at the consensus EBITDA level), this is nine to ten years of runway at the current pace, which provides the company substantial room to execute the roadmap without imminent capital risk. Total debt remains modest, leaving the balance sheet net-cash positive.

Consensus Outlook: Wall Street consensus currently models FY2026 revenue of approximately $235M (up roughly 183% year-over-year) within a probabilistic range of $225–245M. The base case is another year of hyper-growth in bookings and revenue, continued margin pressure from ongoing R&D, and a cash balance that remains above $2.5B exiting 2026. Analyst price targets ranged from a cohort low of $35.35 to a high of $105 (Rosenblatt), with Morgan Stanley at $35.00 (Equal-Weight) near the low end, a median of $66.30, and a mean of approximately $72.77 as of early April 2026. The current price of $35.73 sits roughly at the Morgan Stanley bear-case target, reflecting the broader correction from the October 2025 peak of $84.64.

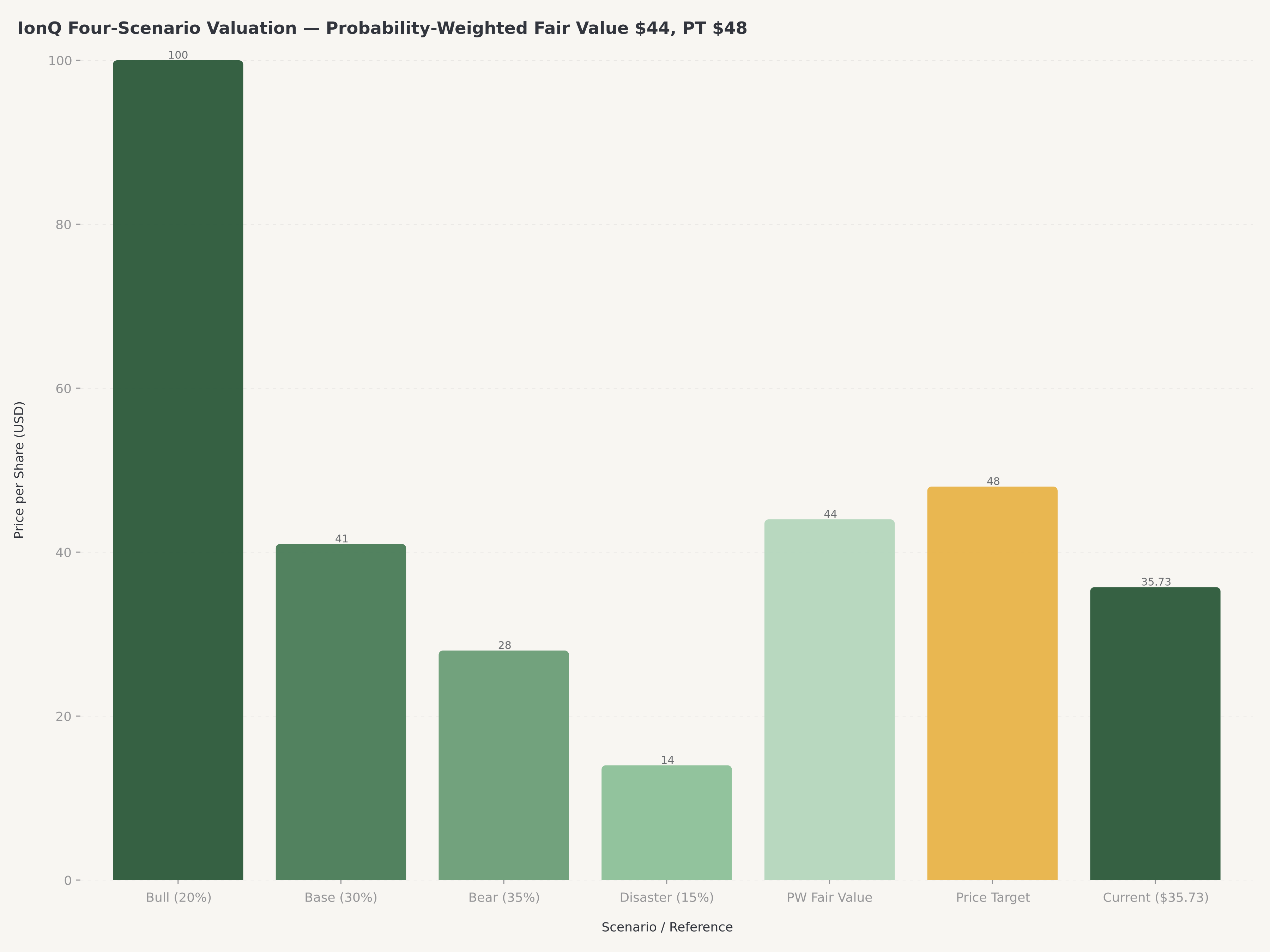

Four-Scenario Valuation: Where $35.73 Fits

The Edgen 360° framework for IonQ models a 2×2 valuation matrix across company growth execution (Strong vs Weak) and macro/capital flow environment (Favorable vs Unfavorable). The resulting four scenarios anchor the investment case.

| Scenario | Conditions | Target Price | Market Cap | Multiplier | Probability |

|---|---|---|---|---|---|

| Bull (A) | Strong growth + Favorable macro | $95–$105 | $35.0–$37.3B | 2.80x | 20% |

| Base (B) | Weak growth + Favorable macro | ~$41 | ~$14.6B | 1.10x | 30% |

| Bear (C) | Strong growth + Unfavorable macro | ~$28 | ~$10.0B | 0.75x | 35% |

| Disaster (D) | Weak growth + Unfavorable macro | ~$14 | ~$5.0B | 0.37x | 15% |

Probability-weighted fair value: approximately $44 per share.

The scenario analysis reveals the characteristic quantum-stock dichotomy. The Bull case of $100 assumes IonQ executes on the Oxford Ionics integration roadmap, delivers meaningful commercial revenue from the $300M RPO, wins additional defense contracts on the back of the HARQ validation, and does so in a macro environment of moderating interest rates and generous capital flows into high-risk technology equities. The Base case of $41 assumes a single execution stumble — a delayed product milestone or a slower-than-forecast revenue ramp — in an otherwise favorable macro environment. The Bear case of $28, interestingly, is where IonQ executes perfectly but sees its multiple compressed by tightening financial conditions and a rotation away from unprofitable growth — this is why Bear carries the highest probability (35%) in our model, and it is where the stock traded in early April before the DARPA HARQ announcement. The Disaster case of $14 represents the combination of both execution failure and macro tightening, and is the level at which the stock would reflect only the tangible value of cash and intellectual property.

At $35.73, IonQ is currently pricing somewhere between the Base and Bear scenarios — perhaps $5 above the pure Bear midpoint of $28, reflecting the April 14 rally. Our probability-weighted fair value of $44 implies that even today, after the HARQ-driven rally, the stock remains moderately below the blended central estimate. The implied upside to our 12-month price target of $48 is approximately 34%, with a Bull case that offers roughly 180% upside and a Disaster case that implies roughly 60% downside.

To frame the Bull case of $100 explicitly: on consensus FY26 revenue of $235M, this implies a forward P/S of approximately 150x. This level has historically been reserved for mega-trend sentiment peaks (cf. internet stocks 1999, COVID SaaS 2020). Our 20% probability reflects non-zero but low conviction in this multiple being sustained — investors should size positions with this asymmetry in mind. Commercially viable quantum computing remains a late-decade outcome (2028–2030+), so any sustained Bull-case pricing is best understood as a sentiment trade rather than a fundamentals-justified re-rating.

We also want to be explicit about the Base (30%) / Bear (35%) inversion visible in the scenario table: Base probability sits slightly below Bear because near-term sentiment swings and DARPA contract timing introduce 6–12 month downside risk even with solid fundamentals. The elevated Bear weight reflects this execution timing risk — a strong-execution-meets-unfavorable-macro outcome — rather than a view that the long-term thesis has failed.

The Competitive Landscape: IonQ vs the Quantum Cohort

Understanding IonQ requires understanding the competitive topology of quantum computing. The industry can be reasonably divided into three tiers.

Tier 1: Hyperscale Incumbents. IBM, Google (Alphabet), and Microsoft operate large internal quantum research programs with in-house hardware and software development. IBM has publicly committed to a superconducting qubit roadmap targeting error-corrected systems by the late 2020s; Google Quantum AI published the landmark "Willow" milestone in December 2024 demonstrating below-threshold error correction for the first time. These programs are well-funded (effectively unlimited R&D budgets within their parent companies) and give their cloud platforms deep integration advantages. They are not, however, pure-play quantum companies — their quantum businesses are loss-making segments embedded inside companies generating hundreds of billions in other revenue.

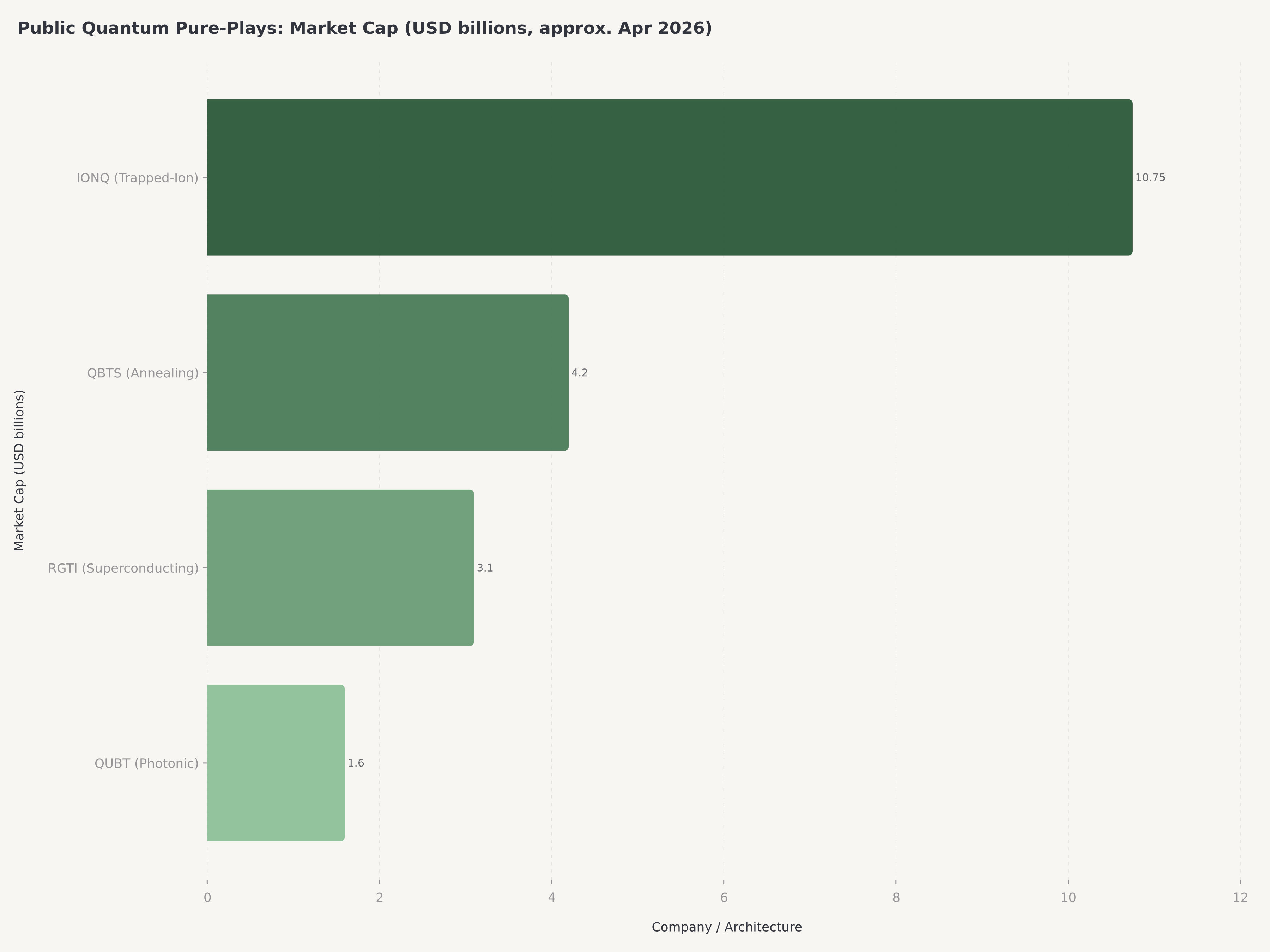

Tier 2: Public Pure-Plays. IonQ, D-Wave Quantum (QBTS), Rigetti Computing (RGTI), and Quantum Computing Inc. (QUBT) form the public pure-play cohort. Each takes a different architectural bet: IonQ on trapped-ion, D-Wave on quantum annealing, Rigetti on superconducting, and QUBT on photonic quantum and Reservoir Computing. IonQ is the largest by market capitalization and by revenue; D-Wave is the oldest and has the longest track record of commercial deployment (its annealers are used for specific optimization problems); Rigetti has a defense-heavy customer mix and recently raised capital to fund a superconducting roadmap; QUBT is the smallest and most speculative. Among this group, IonQ has the cleanest AI-era narrative (hybrid quantum-classical compute with AWS/Azure/Google integration) and the strongest government-customer footprint.

Tier 3: Private Disruptors. Among trapped-ion platforms, IonQ's primary competitive landscape includes Quantinuum (Honeywell-backed, private, estimated $5–10B valuation in last round) as the most direct trapped-ion competitor — a private peer to watch closely given its parallel architectural bet and deep industrial backing. Alongside Quantinuum, PsiQuantum (photonic), Atom Computing and QuEra (neutral-atom), Infleqtion (cold-atom), and Pasqal (neutral-atom) operate as private companies with substantial venture funding. IBM and Google represent alternate qubit modalities (superconducting) rather than direct trapped-ion peers. Their architectures target different pain points in the qubit-scaling problem, and the neutral-atom sub-tier in particular has attracted interest as a potential "second-generation" technology that could scale to thousands of qubits faster than trapped-ion or superconducting. This is the bear-thesis tier for IonQ — the private disruptors could, in theory, leapfrog IonQ's trapped-ion leadership. HARQ's heterogeneous-architecture focus, however, suggests that DARPA (and by extension the broader U.S. quantum strategy) expects multiple architectures to coexist, making leapfrog scenarios less likely.

Where IonQ Wins. IonQ has three defensible competitive advantages. First, trapped-ion qubit fidelity: the company reports 99.99% two-qubit gate fidelity on the Forte platform, which remains the industry benchmark. Second, cloud accessibility: IonQ is the only quantum hardware provider that is natively integrated across all three major U.S. hyperscaler clouds. Third, the M&A-driven IP stack: the Oxford Ionics acquisition in particular gives IonQ a proprietary ion-trap chip architecture that enables scaling to larger qubit counts without the linear hardware growth traditional trapped-ion systems require.

Where IonQ Is Vulnerable. The vulnerabilities are equally clear. First, revenue scale: IBM and Google will each spend multiples of IonQ's entire FY2026 revenue on quantum R&D alone. Second, physics risk: the question of whether trapped-ion architectures can reach million-qubit, error-corrected systems remains genuinely unresolved, and any future DARPA or scientific result that suggests another architecture will reach utility scale first would compress IonQ's multiple materially. Third, cash burn: even with $3.3B on the balance sheet, the burn rate of approximately $340M per year means capital discipline matters, and if revenue growth decelerates the equity story becomes harder to defend.

Catalysts and Risks

12-Month Catalysts (What Justifies the 12-Month Horizon)

- Q1 2026 Earnings (May 2026): Bookings and RPO updates; potential positive surprise on defense-contract timing

- MDA SHIELD Task Order Flow: Conversion of the $151M IDIQ framework into specific task orders through 2026

- Additional DARPA HARQ Contract Disclosures (Q2–Q4 2026): Formal contract award values, technical milestone schedules, and partner disclosures could add $50–200M in committed government revenue

- Oxford Ionics First Product Shipments (late 2026 / early 2027 — at the edge of the 12-month window): First integrated product shipments forecast for late 2026 or early 2027; this is the key 12-month milestone and the logical rating-review point

- Korean Quantum Computing Deployment: KISTI installation progress could enable additional Asia-Pacific government contracts

Multi-Year Thesis (What the Stock Is Really About)

- Commercially Viable Quantum by 2028–2030+: The fundamental investment thesis rests on utility-scale, error-corrected quantum systems reaching commercial deployment late this decade; this is a multi-year, not 12-month, outcome

- HARQ Integration Over 2026–2030: The DARPA heterogeneous architecture roadmap is a multi-year effort; near-term catalysts are progress markers, not terminal value

- Platform Monetization: Scaling QCaaS across AWS/Azure/GCP into a commercially meaningful recurring-revenue book is a 3–5 year execution story

We rate Speculative Buy on a 12-month horizon based on near-term catalyst flow (Q1 earnings, SHIELD task orders, additional HARQ disclosures, Oxford Ionics first shipments), while acknowledging that the fundamental thesis is multi-year. We plan to revisit the rating in January 2027 after Oxford Ionics shipments begin and 12-month catalyst execution can be assessed against realized data.

Near-Term Risks

- Cash Burn Trajectory: FY2026 adjusted EBITDA loss guidance of approximately -$340M is meaningfully worse than prior expectations; further deterioration would pressure the equity story

- M&A Integration Execution: Absorbing Oxford Ionics, Qubitek, Lightsynq, and Vector Atomic simultaneously is operationally ambitious; integration slippage would show up in cost lines and delayed product milestones

- Insider Selling: Persistent insider selling documented in April 2026 — including sales by senior executives during early-2026 price weakness — has added to the bearish technical picture

- Macro Rotation Risk: Quantum is a long-duration, unprofitable-growth asset class; any renewed hawkish inflection from the Federal Reserve would compress multiples across the entire cohort

- Physics / Architecture Risk: A major scientific milestone from a competing architecture (photonic, neutral-atom, superconducting) could reset the competitive landscape

- Customer Concentration: Government revenue is expanding faster than commercial, creating concentration in a single payer (the U.S. federal government and allied defense ministries)

- Dilution Risk from Further Capital Raises: IonQ completed a $1.1B equity raise in January 2026 at approximately $55 per share — well above the current $35.73 — and has pursued an acquisitive M&A pattern that includes the $1.08B Oxford Ionics deal plus Qubitek, Lightsynq, Vector Atomic, Capella Space, and SkyWater-related integrations. With annual cash burn of approximately $340M, a management team demonstrably willing to tap equity markets, and commercialization realistically a late-decade outcome (2028–2030+), the probability of additional capital raises before commercialization is non-trivial. Any follow-on raise executed below the January 2026 clearing price of $55 would be dilutive on a mark-to-market basis, and further M&A could require stock-funded consideration that pressures the share count even in the absence of a primary offering. Investors should model a realistic dilution path — not just the current share count — when assessing per-share upside.

The Verdict: Speculative Buy, $48 Price Target

IonQ is the cleanest available public-market expression of a long-duration bet on commercial quantum computing. The DARPA HARQ announcement on April 14 is not a financial catalyst in the immediate P&L sense — the contract values disclosed to date are modest in the context of a $235M revenue guide — but it is a strategic validation that addresses the single biggest bear thesis on trapped-ion systems by explicitly building heterogeneous architectures into the U.S. quantum roadmap. Combined with the $151M MDA SHIELD IDIQ signed in February 2026, the ID Quantique integration, the Oxford Ionics technology upgrade, and a $3.3B cash cushion providing multi-year runway, IonQ enters the next commercialization phase with genuine structural advantages.

We rate IonQ Speculative Buy on a 12-month horizon with a price target of $48, implying approximately 34% upside from $35.73 — while explicitly flagging that the fundamental thesis is multi-year (commercially viable quantum is a 2028–2030+ outcome). The 12-month rating is anchored to near-term catalyst flow; we plan to revisit the rating in January 2027 after Oxford Ionics shipments begin. The price target is calibrated to a blended outcome weighted 20% to the Bull scenario ($100), 30% to the Base scenario ($41), 35% to the Bear scenario ($28), and 15% to the Disaster scenario ($14), which produces approximately $44, with a modest premium of roughly $4 reflecting the DARPA HARQ catalyst and the strategic acceleration implied by the Oxford Ionics integration. Investors should size positions accordingly: this is a 1–3% satellite position in a diversified portfolio, appropriate for investors with explicit risk tolerance for binary technology outcomes and a multi-year holding horizon. The 52-week trading range of $23.49 to $84.64 is the single best forward-looking indicator of how volatile the journey to $48 will be.

We would upgrade to Buy if (1) the DARPA HARQ contract values disclosed in Q2 or Q3 2026 exceed $100M in cumulative bookings, (2) the Oxford Ionics integration delivers a published product milestone ahead of schedule, or (3) the stock pulls back below $28 without fundamental deterioration. We would downgrade to Hold if FY2026 adjusted EBITDA losses widen beyond the current -$340M consensus or if the cash balance drops below $2.5B exiting 2026.

For more on the AI and advanced computing investment landscape, read our analysis of Credo Technology's AI networking semiconductor thesis and our Micron vs SanDisk AI memory market comparison.

Risks to Our View

The most significant risk to our Speculative Buy call is the macro rotation risk embedded in Bear Case C. If the Federal Reserve signals a return to restrictive policy in 2026 — or if credit markets tighten for any reason — the quantum cohort will be among the hardest-hit sectors, regardless of fundamental execution. This is why we rate Bear (strong execution + unfavorable macro) the highest-probability scenario at 35%. Investors should consider position sizing and entry timing carefully; dollar-cost averaging is a sensible approach given the binary nature of individual catalysts.

The second risk is execution-driven: the M&A stack IonQ has built in 2025 is complex, and integrating multiple acquisition targets simultaneously while also delivering on an organic product roadmap is a challenging operational task. Any slippage would compress both revenue and multiple simultaneously.

The third risk is the most fundamental — physics risk. Our investment case rests on the assumption that trapped-ion qubits remain competitive on a path to error-corrected, utility-scale quantum computing. If another architecture reaches that milestone decisively first, the IonQ story would require substantial revision.

Conclusion

The DARPA HARQ announcement is the kind of catalyst that, in a speculative technology cycle, separates durable investment cases from purely narrative-driven ones. For IonQ, HARQ validates the trapped-ion architecture as a partner in the U.S. heterogeneous quantum roadmap, extends the government-customer moat that is already the most defensible feature of the business, and provides a multi-year reason for institutional capital to re-engage after a six-month correction from the October 2025 highs. At $35.73, the stock is not cheap by any classical measure — it trades at roughly 45x forward revenue — but it is modestly below our probability-weighted fair value of $44 and approximately 34% below our 12-month target of $48. For investors with an appropriately sized, long-duration position, this is where quantum starts to pay.

FAQ

What is the DARPA HARQ program and why did it move IONQ stock?

DARPA's Heterogeneous Architectures for Quantum (HARQ) program, announced April 14, 2026, is a multi-year initiative to develop quantum computing systems that combine multiple qubit architectures (trapped-ion, superconducting, photonic, neutral-atom) to achieve utility-scale performance faster than single-architecture approaches. IonQ was named as a participant, which both validates its trapped-ion technology as a component of the U.S. national quantum strategy and opens the door to multi-year contract funding. The stock rallied 19.9% to close at $35.73 on the news because it addresses the single largest bear thesis on trapped-ion — that it would be leapfrogged by competing architectures — by making trapped-ion a feature of the national roadmap rather than a stand-alone bet.

Is IONQ profitable, and when will it be?

IonQ is not sustainably profitable on an underlying-operations basis and is not expected to reach Adjusted EBITDA breakeven in 2026 or 2027. The GAAP numbers require careful parsing: Q4 2025 reported GAAP net income of +$753.7M, but this was driven almost entirely by a roughly $950M non-cash fair-value gain on warrant liabilities (a mark-to-market accounting item), not underlying operating performance. On the operating-performance side, Q4 2025 Adjusted EBITDA loss was approximately -$186.8M, and consensus FY2026 Adjusted EBITDA loss has widened to approximately -$340M. The FY2027 consensus is approximately -$323M in Adjusted EBITDA. Profitability is realistically a late-decade outcome dependent on commercial revenue scaling materially beyond the current $230M bookings base. The $3.3B cash balance provides multi-year runway to reach that inflection.

What is the IonQ price target and rating?

We rate IonQ Speculative Buy with a 12-month price target of $48, representing approximately 34% upside from the April 14, 2026 close of $35.73. Our price target is derived from a probability-weighted average of four scenarios: Bull ($100, 20%), Base ($41, 30%), Bear ($28, 35%), and Disaster ($14, 15%) — producing roughly $44 — plus a modest premium for the DARPA HARQ catalyst and the Oxford Ionics integration roadmap.

How does IonQ compare to QBTS, RGTI, and QUBT?

Among the public pure-play quantum cohort, IonQ is the largest by market capitalization and by revenue. D-Wave Quantum (QBTS) uses quantum annealing, a different architecture optimized for specific optimization problems, and has the longest commercial deployment history. Rigetti (RGTI) uses superconducting qubits and has a defense-heavy customer mix but is smaller by revenue. Quantum Computing Inc. (QUBT) uses photonic and reservoir computing approaches and is the smallest and most speculative. IonQ's differentiation is (1) trapped-ion fidelity, (2) triple-cloud (AWS, Azure, GCP) QCaaS integration, and (3) the largest government-customer footprint.

What are the biggest risks to owning IonQ?

The three biggest risks are (1) macro rotation risk — quantum is a long-duration, unprofitable-growth asset class and is highly sensitive to interest-rate and liquidity regimes; (2) execution risk — integrating multiple 2025 acquisitions (Oxford Ionics, Qubitek, Lightsynq, Vector Atomic) simultaneously while scaling commercial operations is operationally complex; and (3) physics/architecture risk — the trapped-ion approach may be leapfrogged by a competing architecture (photonic or neutral-atom) if that technology reaches error-corrected utility scale first. Our Bear case at $28 assigns 35% probability to a scenario combining strong execution with unfavorable macro, and the Disaster case at $14 assigns 15% probability to the combined downside.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. The author and Edgen do not hold positions in the securities discussed. Past performance is not indicative of future results. Quantum computing equities exhibit extreme volatility and binary outcomes; position sizing and risk management are essential. Investors should conduct their own due diligence before making investment decisions.

Recommend