Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

Credo Technology After the DustPhotonics Deal: Why CRDO's $750M Silicon Photonics Grab and Jefferies Buy Rating Re-Rate the AI Networking Thesis

· Apr 16 2026

By David Hartley | 2026-04-15 Rating: Buy | Price Target: $205 (30% upside) Sector: Semiconductors — AI Networking, Optical DSPs, Active Electrical Cables Category: Tech & AI > Semiconductors | AI Infrastructure | Ticker: $CRDO

Summary

- Credo Technology (NASDAQ: CRDO) closed April 14, 2026 at $157.69, up 15% intraday, on the back of two hard catalysts landing on the same day: Jefferies raised its price target while reiterating a Buy rating, and Credo announced the $750 million acquisition of silicon photonics innovator DustPhotonics — a deal that slots co-packaged optics (CPO) talent and IP directly on top of Credo's existing 800G/1.6T SerDes and DSP stack.

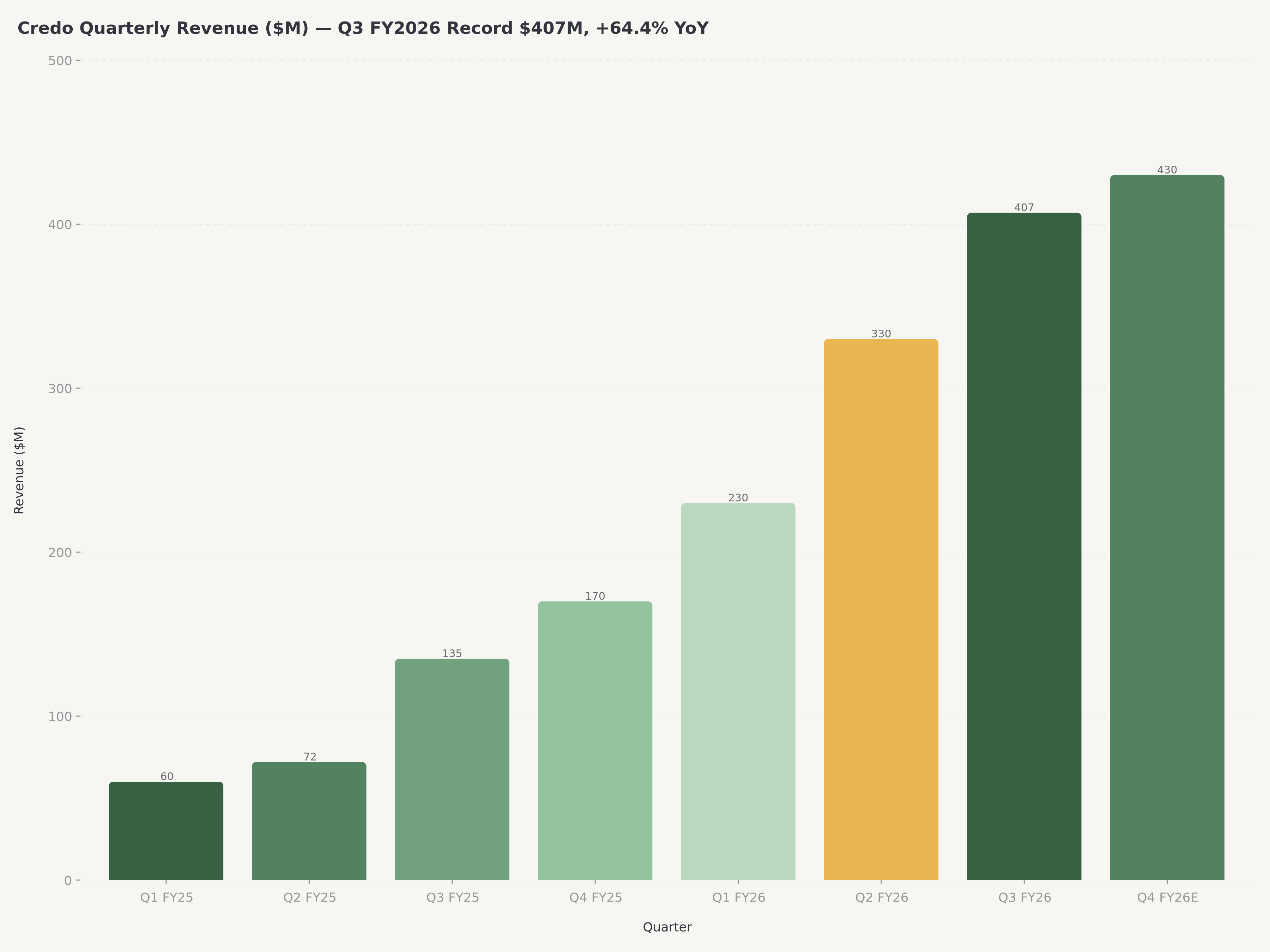

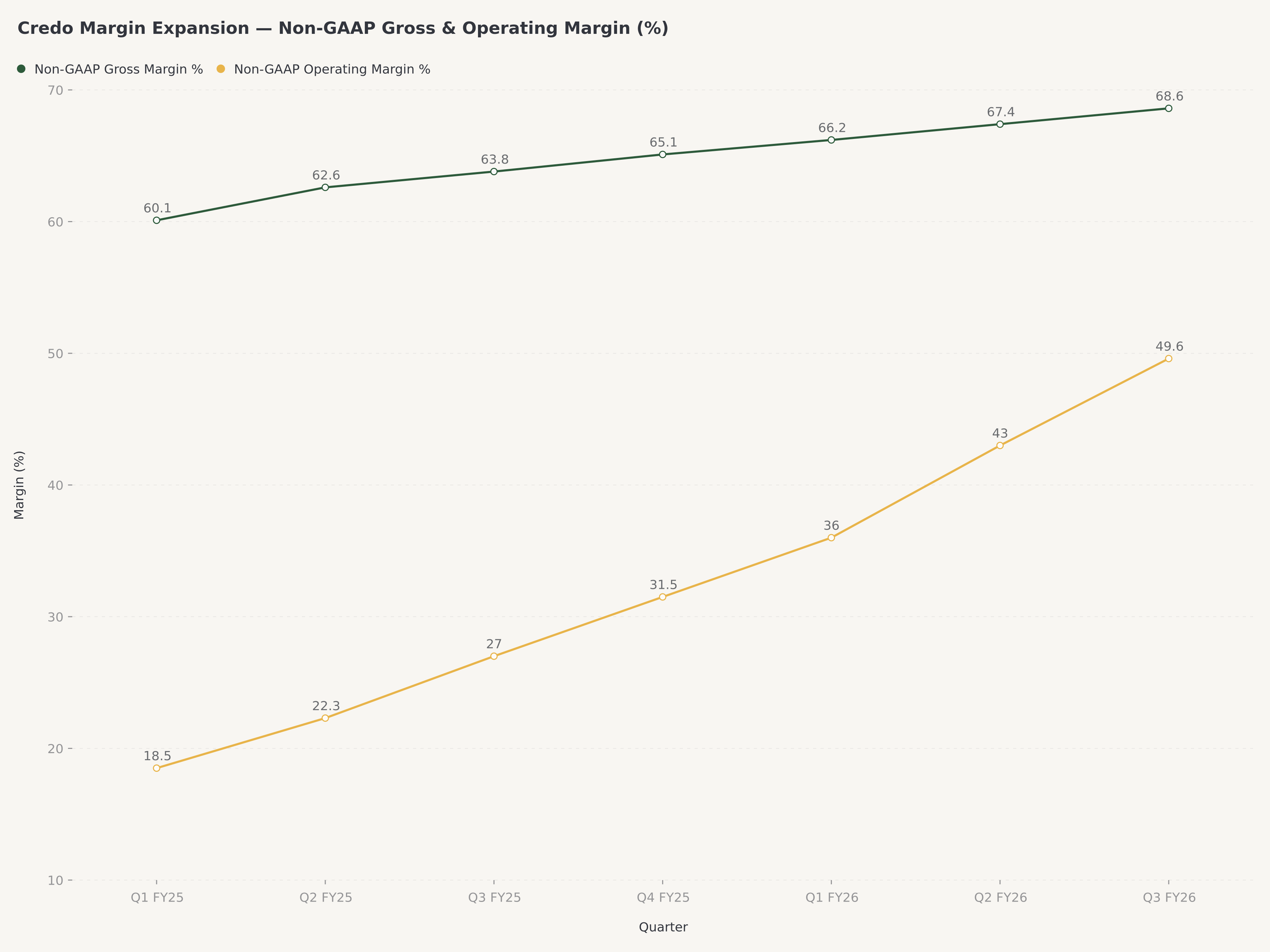

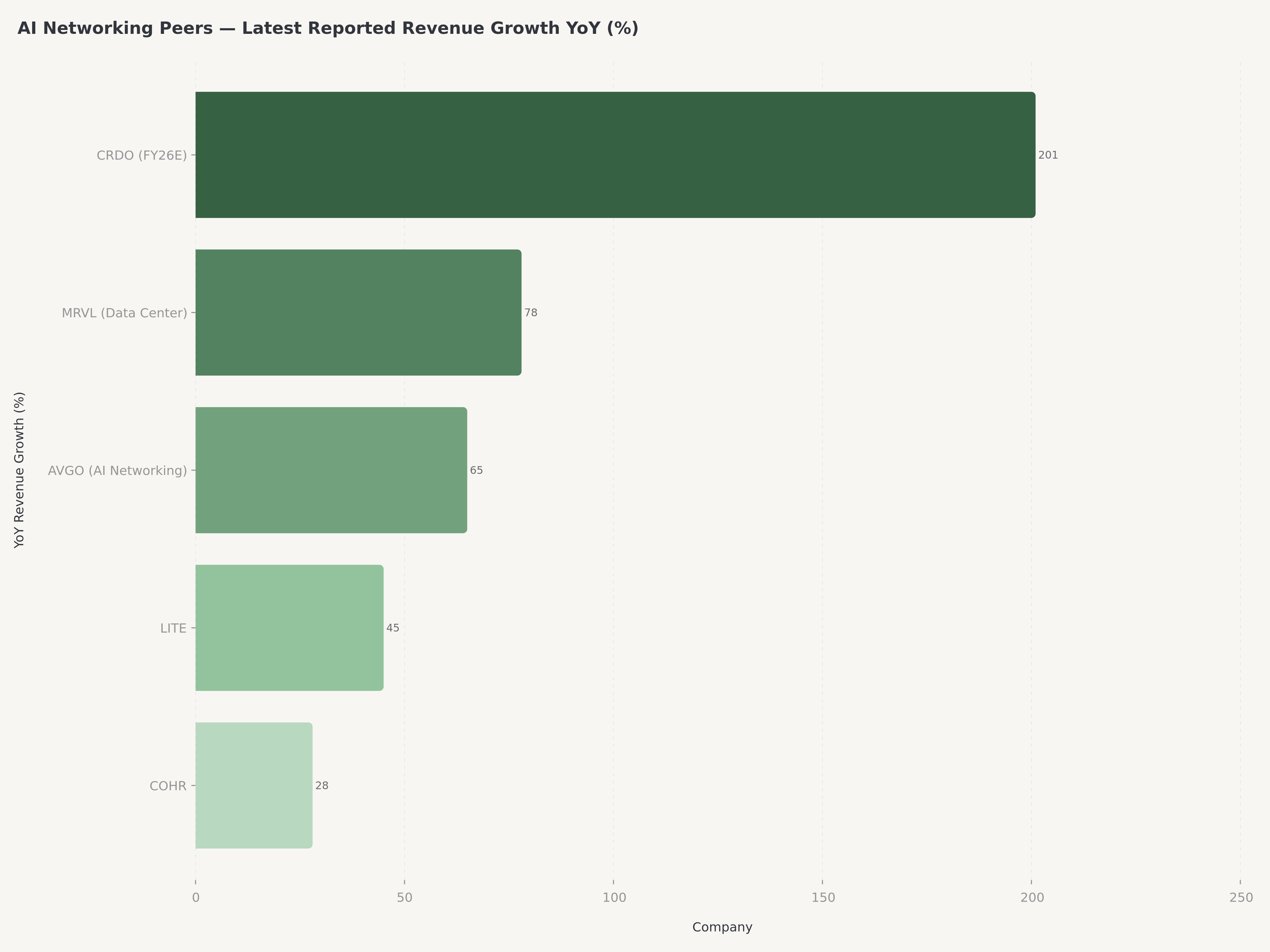

- The financial backdrop behind the re-rating is extraordinary: Q3 FY2026 revenue of $407 million (+64.4% YoY), Non-GAAP gross margin of 68.6%, Non-GAAP operating margin of 49.6%, and full-year FY2026 revenue growth tracking to more than double YoY (well above 100%) — performance that puts Credo ahead of virtually every peer in AI networking silicon, including Marvell and Broadcom on growth rate (if not yet scale).

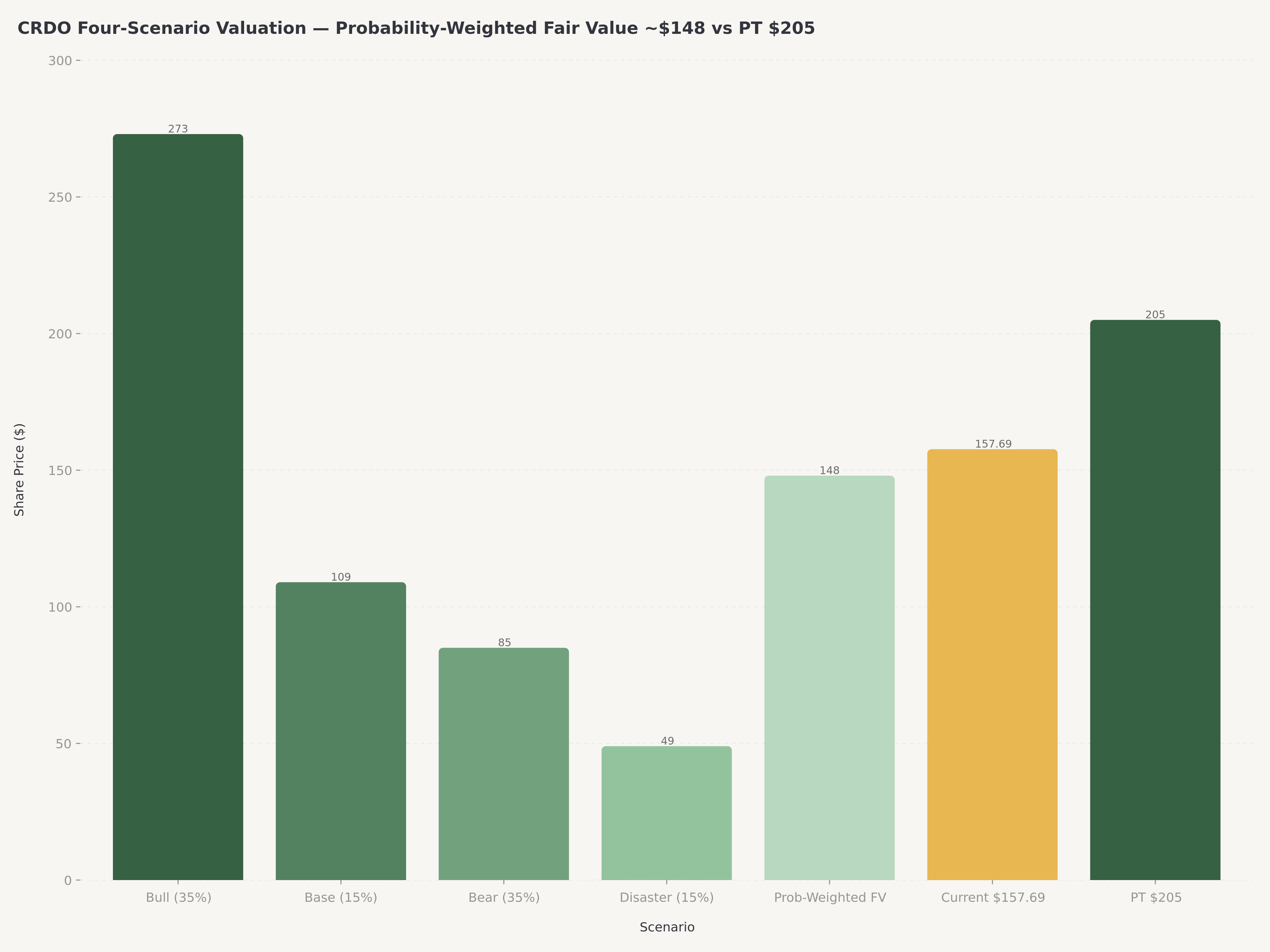

- The Edgen 360° four-scenario model frames the debate honestly: Bull case $273 / $49.4B market cap (35% probability), Base case $109 / $19.7B (15%), Bear case $85 / $15.4B (35%), Disaster case $49 / $8.8B (15%). The probability-weighted fair value sits near $148, which means at $157.69 the market is already pricing Credo slightly above the central estimate — but the DustPhotonics deal plausibly shifts Bull probability higher and raises the Bull ceiling itself.

- We rate CRDO Buy with a $205 price target, reflecting re-weighted scenarios post-DustPhotonics (Bull 45% / Base 15% / Bear 25% / Disaster 15%) that produce a revised probability-weighted fair value near $182, plus a ~$23 catalyst premium for silicon photonics integration option value. The risk/reward remains attractive for investors with high risk tolerance and conviction in the AI buildout — but a single customer still represents >40% of revenue, the 90-day put/call ratio recently spiked to 1.39, and the 50% combined Bear/Disaster probability cannot be dismissed.

Why This Matters Now: Two Catalysts, One Day

April 14, 2026 will go down as the single most important session in Credo's public-market history since the IPO. Two separate catalysts converged in a single news cycle and sent the stock up 15% intraday to close at $157.69.

Catalyst #1 — Jefferies raises price target, reiterates Buy. Jefferies — already an active CRDO analyst (per the Edgen 360° report dated Mar 14, 2026, Jefferies had cut its PT from $240 to $200 on Mar 3, 2026 while maintaining Buy) — raised its price target on Apr 14, 2026 and reiterated the Buy call. The PT raise is important for two reasons beyond the rating itself. First, it reinforces a consensus stack that was already leaning constructive (per the Edgen 360° report, the mean price target was approximately $206 with a Strong Buy consensus), tightening the bull narrative. Second, analyst PT raises of this kind — coming from a house that had trimmed its target just six weeks earlier — signal a meaningful mind-change and typically precede incremental institutional inflows. The stock's 6-month +132.80% performance vs the SPX500 S&P 500's +25% made CRDO a conspicuous relative outperformer, and the Jefferies upward revision adds a fresh catalyst for accounts re-underwriting the name.

Catalyst #2 — DustPhotonics acquired for $750 million. This is the more structurally important event. DustPhotonics is a silicon photonics innovator specializing in co-packaged optics (CPO) — the technology that moves the optical engine directly onto the switch or GPU package, dramatically reducing power per bit and enabling the 1.6T/3.2T generation of AI interconnect. Credo historically built its franchise around electrical SerDes (the underlying high-speed signal IP), optical DSPs, and Active Electrical Cables (AECs) — categories where Credo's technology advantage is well established. DustPhotonics fills the silicon photonics gap that separates Credo from deeper-pocketed competitors like Marvell (MRVL) and Broadcom (AVGO), and does so at a price that looks manageable against Credo's $21B+ market cap and cash-generating FY2026.

Combined, these catalysts re-frame Credo from a pure-play SerDes/DSP/AEC vendor into an integrated AI networking company with a credible optical engine of its own. The market's 15% reaction reflects that re-framing, not just a revenue multiple bump.

Who Credo Is, and Why the Management Team Matters

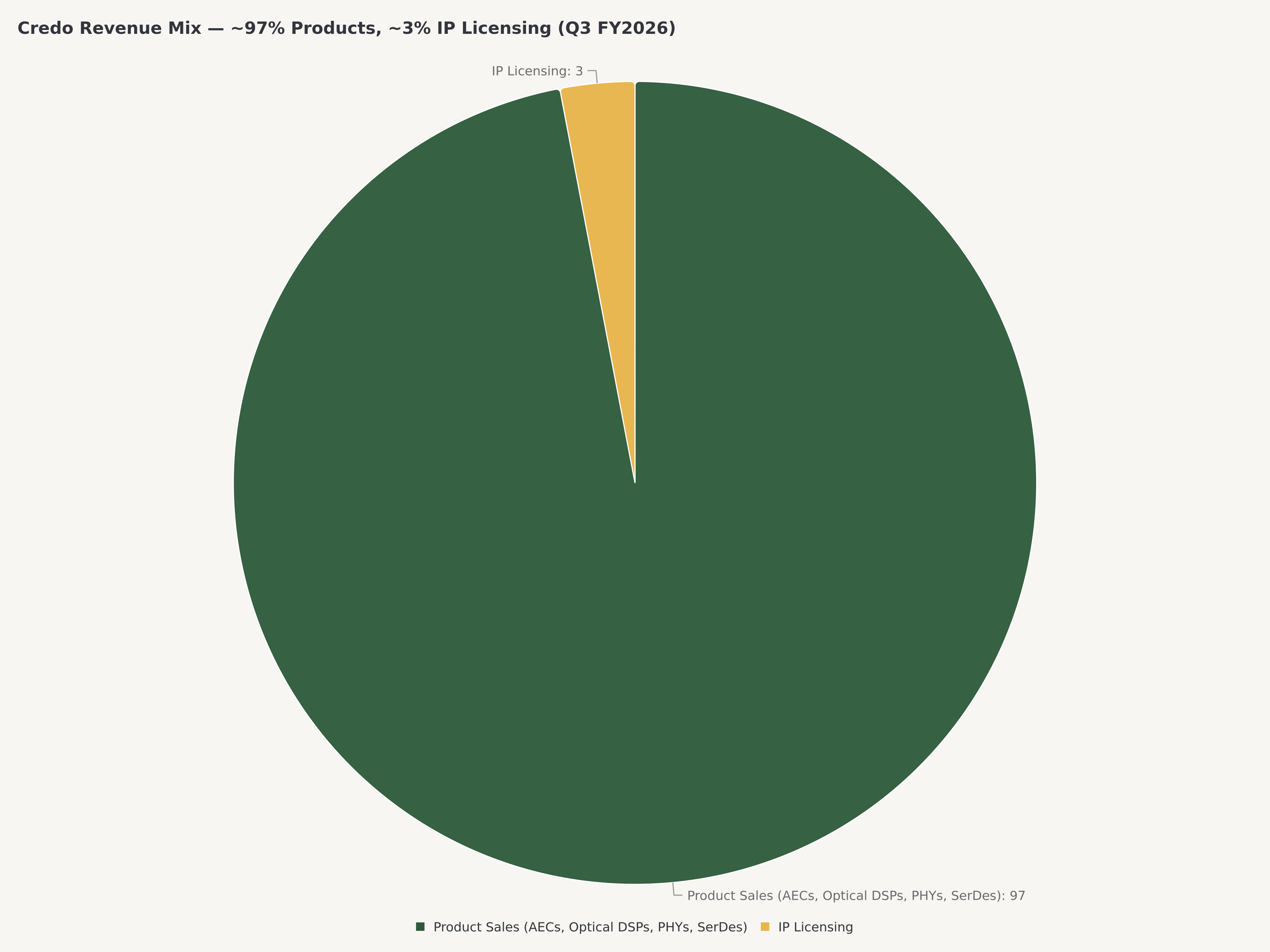

Credo Technology Group Holding Ltd is a fabless semiconductor company founded to address the escalating demand for high-speed, power-efficient connectivity in global data infrastructure markets. The company's core mission is to deliver breakthrough technologies that ease system-level bandwidth bottlenecks — a critical challenge exacerbated by the exponential growth of Artificial Intelligence (AI), cloud computing, and hyperscale networks. Evidence from the most recent filings is overwhelmingly product-focused: across Q3 FY2026, Credo derived approximately 97% of total revenue from product sales with the remaining 3% from Intellectual Property (IP) licensing.

The product portfolio is organized around several complementary families, each targeting a specific layer of the AI data infrastructure hierarchy: Active Electrical Cables (AECs) marketed under the HiWire brand; optical DSPs covering 100G/400G to 800G and 1.6T (a 1.6T DSP was introduced in Q2 FY2026); Line Card PHYs; original SerDes chiplets; and a portfolio of IP licensing and discrete components aimed at hyperscale, enterprise, and HPC customers. The key competitive edge is not just product count but architectural integration — Credo's SerDes chiplets and DSP PHYs cover the same design wins, which allows bundling that discrete competitors struggle to match.

Leadership. The executive team is led by William Brennan (CEO and President) and CFO Daniel Fleming, with seasoned technology veterans across product, engineering, and operations. CRDO's management carries strong Marvell and Inphi pedigree — founder/CEO Bill Brennan held senior roles at Marvell and Inphi prior to founding Credo, and Pantas Sutardja (Marvell co-founder) is cited as a co-founder of Credo. (Note: Marvell's current CEO Matt Murphy runs a direct competitor and is not affiliated with CRDO's board or governance.) Credo's own board has been steadily strengthened, including Jim Laufman (Chief Legal Officer) on the executive team and Lip-Bu Tan, who was named a director (announced March 2025). This is not a team learning semiconductors on the job — the combined operating experience across AI networking, fabless execution, and hyperscaler relationships is a genuine competitive asset in an industry where customer trust is compounded over years.

Q3 FY2026 Performance: The Operating Proof

The operating proof behind the investment thesis is unusually clear. For Q3 FY2026 (quarter ended roughly early February 2026, reported in March 2026), Credo delivered:

- Revenue: $407 million, up 64.4% YoY — the Company's largest quarterly revenue in its history.

- Non-GAAP Gross Margin: 68.6%, a record and among the best in the AI networking silicon peer group.

- Non-GAAP Operating Margin: 49.6%, up significantly on revenue scaling against a relatively fixed R&D and operating base.

- EPS: $1.13 reported for the trailing twelve months against recent earnings power; the most recent quarterly EPS ($0.50 reported near-term) matched or beat consensus.

- Full-Year FY2026 Guidance (implied): full-year revenue growth is tracking well above 100% YoY (i.e., more than doubling), with Q4 FY2026 guided to revenue of $425–435 million — a sequential acceleration despite Q3 being a record.

Two things stand out. First, 68.6% gross margin is remarkable for a hardware company selling into hyperscaler customers who typically extract price concessions as volumes scale. That Credo is expanding margin while tripling revenue tells you the company has genuine pricing power — the product is differentiated enough, and customers are constrained enough, that Credo is getting paid for the technology.

Second, the guidance for Q4 implies continued sequential acceleration: Q3 at $407M, Q4 guided to $425–435M, implies roughly 4.4–6.9% sequential growth on top of a record quarter. Management is not signalling a digestion pause. They are signalling that the ramp is still in its early innings.

AI Networking Positioning: Where Credo Actually Fits

The AI data center is built on three layers of networking silicon, and Credo plays in the layer that is arguably the most defensible: in-rack and rack-to-rack connectivity.

- GPU-to-GPU (within-rack): Dominated by NVIDIA's NVLink and proprietary solutions — Credo does not compete here directly.

- Rack-to-rack / scale-out (the Credo zone): Requires 224G SerDes, 800G/1.6T optical DSPs, AECs for short reach, and increasingly CPO for the 3.2T era. This is where Credo's technology stack lives and where the DustPhotonics acquisition extends reach.

- Data-center to data-center (long-haul optical): Dominated by Lumentum (LITE), Coherent (COHR), and other specialist optical players.

Within the scale-out zone, Credo has been taking share from Broadcom and Marvell in AEC specifically. The HiWire AEC family replaces passive copper cables and active optical cables (AOCs) for short-reach (sub-5m) links between top-of-rack switches and servers — and at the power and cost curve of AI clusters, AECs are frequently the best choice. On the optical DSP side, Credo has been displacing incumbents on 800G design wins and has already announced 1.6T DSP products that are sampling with customers ahead of the 2027 deployment wave.

The DustPhotonics integration is meaningful precisely because CPO is the next battleground. By 2027-2028, the highest-end AI switch platforms are expected to co-package the optical engine directly with the switch ASIC to cut power by 40-50% vs pluggable optics. Marvell (via its Inphi and other silicon photonics assets) and Broadcom (via Apache/Ranovus relationships) are both ahead of Credo organically. Acquiring DustPhotonics compresses that gap in months rather than years. Whether Credo executes on the integration is the operational question — and the Bull case is effectively a bet that they will.

Peer comparison — why Astera Labs (ALAB) is the cleanest public comp. The Edgen 360° report explicitly names Astera Labs (ALAB) alongside Marvell and Broadcom as a direct competitor, and ALAB is the most direct public pure-play comparable to CRDO given its similar scale, hyperscaler-driven growth profile, and pure-play AI connectivity focus. The two companies differ on portfolio breadth: CRDO has a broader DSP/SerDes/AEC/(soon) CPO stack that spans electrical and optical interconnect, while ALAB is narrower and more concentrated in CXL/PCIe retimers and smart cable modules for in-rack GPU-to-GPU fabric. Multiples diverge accordingly — ALAB typically trades at a higher forward P/S (mid-20s) reflecting narrower but deeper hyperscaler design-win concentration, while CRDO has historically traded slightly below ALAB on multiple but on stronger YoY growth. Against MRVL and AVGO, scale and silicon photonics depth still favor the incumbents, though CRDO is closing the CPO gap post-DustPhotonics.

Valuation: The Four-Scenario View

The Edgen 360° report (March 14, 2026) applies a 2x2 scenario framework that crosses Company Growth (Strong vs Weak) with Macro & Capital Flow Environment (Favorable vs Unfavorable). The result is four scenarios with share-price targets and market-cap implications. All multipliers are defined against the March 14, 2026 reference market cap of approximately $21 billion and reference share price of approximately $121.50.

| Scenario | Conditions | Multiplier | Share Price Target | Market Cap | Probability |

|---|---|---|---|---|---|

| Bull (A) | Strong Growth + Favorable Macro | 2.00x–2.25x | ~$273 | ~$49.4B | 35% |

| Base (B) | Weak Growth + Favorable Macro | 0.80x–0.90x | ~$109 | ~$19.7B | 15% |

| Bear (C) | Strong Growth + Unfavorable Macro | 0.60x–0.70x | ~$85 | ~$15.4B | 35% |

| Disaster (D) | Weak Growth + Unfavorable Macro | 0.30x–0.40x | ~$49 | ~$8.8B | 15% |

Note on probabilities. In the 360°'s 2x2 valuation matrix, Base case represents the specific cell where Weak Growth intersects with Favorable Macro — a structurally low-probability intersection, which is why Base (15%) sits below Bear (35%). The 35% Bear probability reflects concern that Strong Company Growth can still coexist with Unfavorable Macro (e.g., CRDO keeps executing but AI-trade multiples de-rate), not a broader bearish view of the business.

Probability-weighted fair value ≈ $148 (0.35×273 + 0.15×109 + 0.35×85 + 0.15×49 ≈ $148).

At $157.69 (April 14, 2026), the market is pricing Credo approximately 7% above the probability-weighted central estimate. Two observations are critical:

- The asymmetry has re-loaded. The Bull case offers approximately +73% upside to $273; the combined Bear+Disaster (50% probability) offers approximately -46% to -69% downside to $85 or $49. That is not a symmetric distribution, but it is a distribution that rewards conviction if you believe the Bull scenario probability should be higher than 35%.

- DustPhotonics plausibly raises Bull probability. The March 14, 2026 360° report pre-dates the DustPhotonics acquisition. If the integration goes well and CPO design wins materialize in 2027, the Bull probability should migrate toward 40–45% and the Bull ceiling could extend above the $273 reference. That is the case for adding to positions on pullbacks rather than chasing.

Adjusted Probability (post-DustPhotonics, post-Jefferies PT raise). Following the DustPhotonics acquisition ($750M, April 14, 2026) and the Jefferies PT raise on the same day, we re-weight scenarios: Bull 45% (up from 35%), Base 15%, Bear 25%, Disaster 15%. Probability-weighted fair value revises to approximately $182 (0.45×273 + 0.15×109 + 0.25×85 + 0.15×49 ≈ $182), to which we add a $23 catalyst premium for silicon photonics integration option value, producing our $205 price target. The $205 figure sits ~38% above the unadjusted $148 math, reflecting our higher conviction in the Bull case post-DustPhotonics. If the CPO integration disappoints, the catalyst premium collapses and the honest PT compresses back toward $180.

On the Bull 2.00x–2.25x multiplier (~22x P/S). The Bull-case multiplier implies a forward P/S in the ~22x range at peak. This sits between ALAB's recent high multiple (mid-20s forward P/S during peak AI-connectivity enthusiasm) and AVGO's more mature level (high-single-digit to low-teens P/S given larger scale and diversified mix). That reference anchors the Bull case to observable market pricing rather than an abstract growth multiple.

Key Risks

No investment at this margin of execution is free of real risk. The concrete hazards investors must underwrite:

- Customer concentration. A single customer represents more than 40% of revenue, and a handful of hyperscalers represent nearly the entire top line. Any single-customer order slowdown — whether from a product architecture change, a dual-sourcing move, or hyperscaler capex moderation — would have a disproportionate impact on the quarter.

- Acquisition integration risk. The $750M DustPhotonics acquisition must be integrated — engineering teams merged, product roadmaps aligned, customers re-briefed — without distracting from the core AEC/DSP ramp. Credo has not previously completed an acquisition of this size.

- Competitive response. Marvell and Broadcom are not passive observers. Marvell in particular has deeper silicon photonics expertise and broader customer relationships. A competitive response on pricing or a hyperscaler design decision to consolidate around Marvell/Broadcom solutions would compress Credo's growth trajectory.

- Macro and valuation risk. CRDO's 5-year beta of 2.67 means the stock moves roughly 2.7x the market in either direction. A broader risk-off rotation — even one unrelated to AI fundamentals — could compress the multiple sharply. The 90-day put/call ratio has recently spiked to 1.39, indicating elevated hedging activity.

- Insider selling. Persistent insider selling has been noted (including on or around Mar 13, 2026, pursuant to Rule 10b5-1 plans), which, while programmatic, introduces a potential supply overhang.

- AEC product cycle timing. Credo's revenue is still concentrated in a relatively narrow product category (AECs + optical DSPs). A shift in hyperscaler architecture — for example, toward direct optical interconnect that bypasses AECs — would threaten the core franchise.

- Regulatory and geopolitical risk. As a fabless vendor reliant on Taiwan foundries (TSMC) for advanced-node production and selling into a customer base with material AI-chip exposure, CRDO is exposed to two evolving policy vectors. First, US-China AI chip export controls continue to tighten — any extension of restricted-technology lists to cover high-speed SerDes, 800G/1.6T DSPs, or CPO subsystems would foreclose certain China-adjacent end-customer revenue and add compliance overhead. Second, Taiwan fabless exposure means any Taiwan Strait escalation or cross-strait supply disruption would hit CRDO's production pipeline directly; while this risk is shared with the entire fabless cohort, CRDO's smaller scale makes second-source qualification less nimble than it is for MRVL/AVGO.

Verdict: Buy CRDO at $205 Price Target

We rate Credo Technology Group Holding Ltd (CRDO) Buy with a $205 price target, representing approximately 30% upside from the April 14, 2026 close of $157.69. The core reasoning:

The fundamental story — revenue more than doubling YoY, 68.6% Non-GAAP gross margin, 49.6% Non-GAAP operating margin, and accelerating sequential guidance — is extraordinary and not mis-priced so much as still being re-rated in real time. The DustPhotonics acquisition plausibly shifts the Bull probability upward in the Edgen 360° framework and adds silicon photonics capability that Credo previously had to buy from partners. The Jefferies PT raise and reiterated Buy add fresh sell-side conviction that should support fund flows in the next 30-60 days.

The risks are real and concentrated: a single customer, an unproven M&A integration, a formidable pair of competitors (MRVL, AVGO), and a high-beta stock in a macro-sensitive AI trade. Position sizing should reflect those risks — we do not consider CRDO a core position and would recommend sizing below 2-3% for most diversified investors. For aggressive AI-infrastructure-focused portfolios, sizing toward 4-5% is defensible with rigorous attention to entry discipline.

Enter on pullbacks toward $140-145. Hold through the next two earnings reports to see DustPhotonics integration milestones. Reassess at $205 or if the DustPhotonics integration shows early design-win evidence.

For related AI infrastructure investment analysis, see our Micron vs SanDisk memory chip comparison for AI demand and our exploration of IonQ's quantum computing breakthrough and DARPA catalyst.

FAQ

What happened to CRDO stock on April 14, 2026?

Credo Technology (CRDO) closed at $157.69 on April 14, 2026, up approximately 15% intraday. The move was driven by two simultaneous catalysts: (1) Jefferies raised its price target on CRDO while reiterating a Buy rating (Jefferies had been covering the name already; the prior move was a PT cut from $240 to $200 on Mar 3, 2026), and (2) Credo announced the $750 million acquisition of silicon photonics innovator DustPhotonics — a deal that extends Credo's AI networking stack into co-packaged optics.

Why is the DustPhotonics acquisition strategically important?

DustPhotonics brings silicon photonics and co-packaged optics (CPO) expertise that Credo historically lacked. As AI switch platforms move toward 1.6T and 3.2T interconnect speeds in 2027-2028, CPO becomes critical for reducing power per bit by 40-50% vs pluggable optics. The acquisition closes a capability gap vs Marvell (MRVL) and Broadcom (AVGO) and, if integrated well, could extend the Bull-case revenue trajectory beyond what the March 2026 Edgen 360° scenarios modeled.

How does Credo compare with Marvell, Broadcom, and Astera Labs?

Marvell (MRVL) and Broadcom (AVGO) are significantly larger and have broader product portfolios (including merchant switch silicon, where Credo does not compete). Astera Labs (ALAB) is the closest public pure-play comparable — similar AI-connectivity focus and hyperscaler dependence — but narrower, concentrated in CXL/PCIe retimers and in-rack GPU-to-GPU fabric, while CRDO covers a broader DSP/SerDes/AEC/(now) CPO stack. Within its lanes (AEC, optical DSPs, SerDes chiplets), Credo has demonstrated best-in-class growth rates (revenue more than doubling YoY in FY2026) and margins (68.6% Non-GAAP GM) and has been taking share on 800G and 1.6T design wins. The DustPhotonics acquisition narrows Credo's gap in silicon photonics vs MRVL/AVGO. Scale favors MRVL/AVGO; narrower focus favors ALAB; agility, breadth and margin profile favor CRDO.

Is CRDO overvalued at $157.69?

Relative to the Edgen 360° probability-weighted fair value of approximately $148, CRDO at $157.69 trades about 7% above the central estimate — not materially overvalued. Relative to our $205 price target (which incorporates a DustPhotonics-driven uplift to the Bull probability), CRDO offers approximately 30% upside. The asymmetry is favorable, but the 50% combined Bear+Disaster probability is a genuine downside risk that justifies cautious position sizing.

What are the single biggest risks?

Customer concentration is the single largest risk: one customer represents >40% of revenue. A change in that relationship — dual-sourcing, design-win loss, or customer capex moderation — would have an outsized impact. Integration risk on the DustPhotonics acquisition is the second largest, and the high 5-year beta of 2.67 means CRDO is exposed disproportionately to any AI-trade de-rating.

What would change our Buy rating?

We would downgrade to Hold if (1) Q4 FY2026 revenue guidance is missed or sharply lowered, (2) customer concentration exceeds 50% from a single account, (3) DustPhotonics integration shows significant dis-synergies (engineering departures, product roadmap slips) within 6-12 months, or (4) the stock rallies above $240 without corresponding earnings upside. We would upgrade our price target if Q1 FY2027 revenue exceeds $475M (implying Bull trajectory) or if CPO design wins with a top hyperscaler are announced.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. The author and Edgen do not hold positions in the securities discussed. Past performance is not indicative of future results. Investors should conduct their own due diligence before making investment decisions.

Recommend