Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

Summary

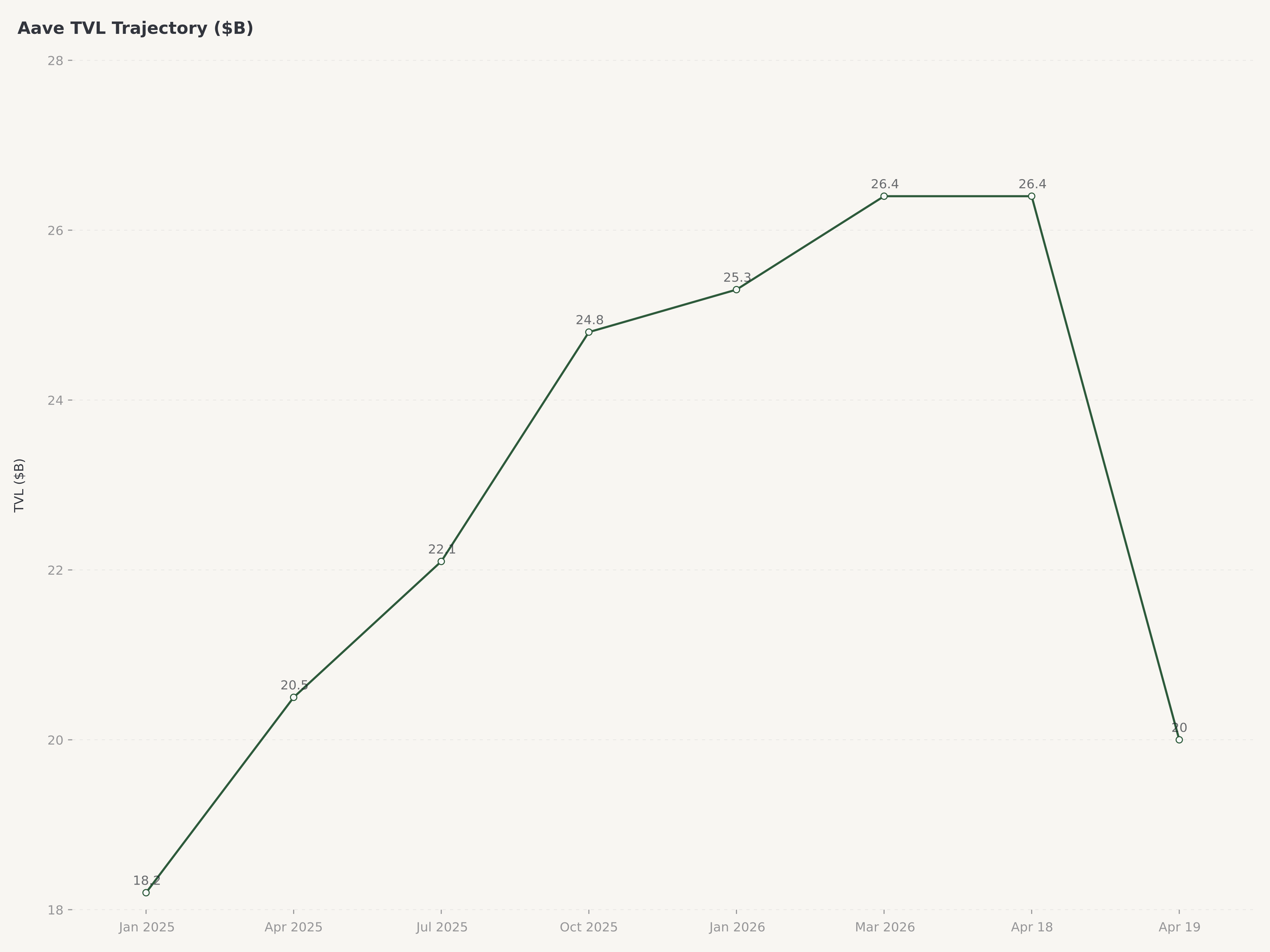

- Aave's total value locked stood at $26.4 billion before the April 19 Kelp DAO bridge exploit, which resulted in $196 million in bad debt on Aave V3 and triggered a $6.6 billion TVL outflow, temporarily pushing the AAVE token down 16-20% to a low of approximately $91 before recovering to the current ~$113 level.

- The protocol's core smart contracts were not compromised in the Kelp incident — the exploit was external to Aave, targeting Kelp's cross-chain bridge to mint fraudulent rsETH collateral — and the governance response was swift: freezing the rsETH reserve, removing borrowing power, and reducing LTV to zero within hours of detection.

- The "Aave Will Win" governance framework passed on April 13 with over 75% approval, directing 100% of Aave Labs revenue to the DAO treasury and implementing a fee switch for direct protocol revenue distribution — a structural milestone that resolves months of internal conflict over revenue ownership and aligns incentives between token holders and protocol development.

- We rate AAVE Buy with a $160 price target, supported by $1.5 million in daily protocol fees, ~9,700 daily active users, a net-zero-inflation token supply of approximately 16 million circulating tokens, and the upcoming Aave V4 mainnet launch that positions the protocol as a "DeFi operating system" — with the post-hack dip providing an attractive entry point at a ~$1.75 billion market cap for the largest lending protocol in decentralized finance.

The DeFi Landscape in April 2026: Cross-Chain Risk Comes Home

Decentralized finance in the spring of 2026 operates in a fundamentally different environment than the speculative frenzy of 2021 or the existential crisis of 2022. Total value locked across all DeFi protocols has stabilized above $100 billion, institutional participation is no longer experimental, and revenue-generating protocols have replaced yield-farming ponzis as the sector's center of gravity. Yet the Kelp DAO exploit on April 19 exposed a vulnerability that the industry has discussed theoretically for years but never experienced at this scale: the systemic risk that cross-chain bridge failures can propagate through composable DeFi protocols and create contagion in systems that were never themselves compromised.

The attack vector was not a flaw in Aave's lending logic, its liquidation engine, or its oracle infrastructure. It was a flaw in Kelp's cross-chain bridge — a separate protocol that issues rsETH, a liquid restaking token representing staked Ethereum. Attackers exploited this bridge to steal 116,500 rsETH, worth approximately $292 million, and deposited the stolen tokens as collateral on Aave V3. They then borrowed wETH against this fraudulent collateral, effectively extracting real assets from Aave's lending pools using collateral that would subsequently become worthless once the exploit was detected and rsETH's value collapsed. The result was approximately $196 million in bad debt on Aave — obligations owed to the protocol's liquidity providers that cannot be recovered from the now-worthless collateral.

The broader macro context for DeFi in 2026 is one of maturation under pressure. Regulatory frameworks are advancing in the United States, the European Union, and major Asian markets. The SEC's evolving stance on decentralized protocols, the EU's Markets in Crypto-Assets Regulation, and Hong Kong's licensing regime for virtual asset service providers collectively create an environment where protocols must demonstrate both technical resilience and governance credibility to survive. Aave's response to the Kelp crisis — and its governance trajectory more broadly — will determine whether institutional capital views it as critical financial infrastructure or an unacceptable counterparty risk.

From Lending Protocol to DeFi Operating System: Aave's Evolution

Aave launched in January 2020 as a rebrand of ETHLend, a peer-to-peer lending protocol founded by Stani Kulechov in 2017. The protocol introduced the concept of lending pools — shared liquidity reserves from which borrowers draw against posted collateral — and rapidly became the dominant lending platform in DeFi, overtaking Compound by mid-2021. What separated Aave from its peers was not merely execution speed but architectural ambition. Flash loans, rate switching between variable and stable interest rates, and cross-chain deployment across Ethereum, Polygon, Avalanche, Arbitrum, Optimism, and Base gave Aave a multi-chain presence that no competitor could match.

The protocol's current iteration, Aave V3, introduced efficiency modes (e-mode), isolation modes for new asset listings, and portal functionality for cross-chain liquidity movement. These features were designed to increase capital efficiency while containing risk — a balance that was tested to its limits by the Kelp exploit. The upcoming Aave V4, which the team has described as a "DeFi operating system," promises a unified liquidity layer, modular risk management, and native cross-chain functionality that would eliminate the need for external bridges — precisely the type of infrastructure that, had it existed, could have prevented the Kelp contagion from reaching Aave in the first place.

Kulechov's vision extends beyond protocol upgrades. The Aave App, a consumer-facing mobile application targeting 10 million users, represents a bet that DeFi can reach mainstream adoption through familiar user interfaces rather than the intimidating web3 frontends that have historically limited participation to crypto natives. The expansion into Latin America through embedded finance partnerships — integrating Aave's lending infrastructure into existing fintech applications — follows the playbook that Stripe and Plaid used to embed traditional financial infrastructure into consumer products. Whether a lending protocol built on Ethereum can replicate that trajectory remains an open question, but the strategic direction is clear: Aave is attempting to become the infrastructure layer for decentralized lending globally, not merely a dApp for crypto traders.

The April 2026 launch of Babylon Native BTC collateral adds another dimension. By enabling Bitcoin holders to use their BTC as collateral on Aave without wrapping it through centralized custodians, the protocol taps into the largest capital pool in cryptocurrency — Bitcoin's $1.3 trillion market cap — while eliminating the counterparty risk associated with wrapped assets like wBTC. This is infrastructure-level innovation that, if successful, could meaningfully expand Aave's addressable market.

On-Chain Performance: TVL, Revenue, and User Metrics

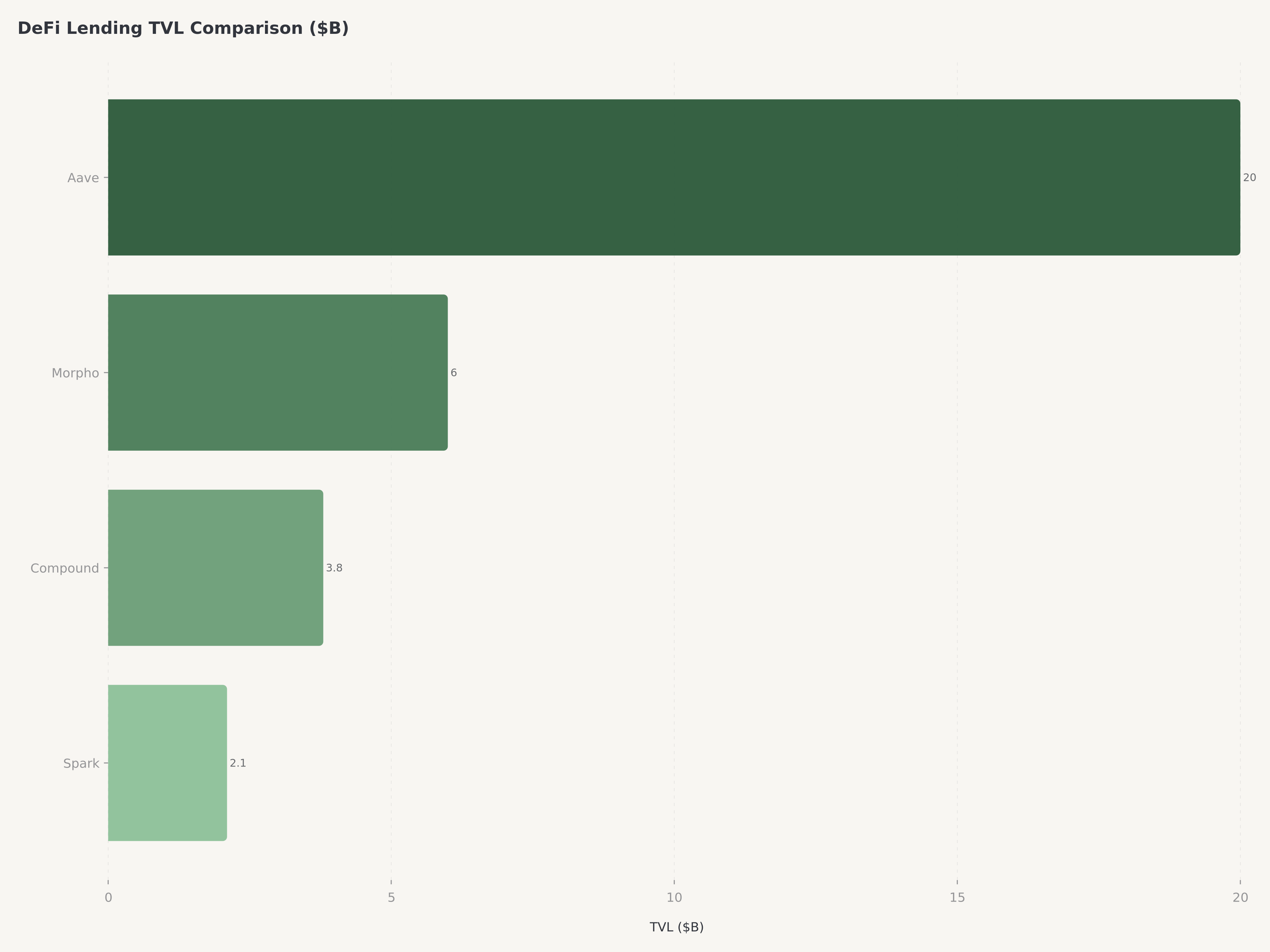

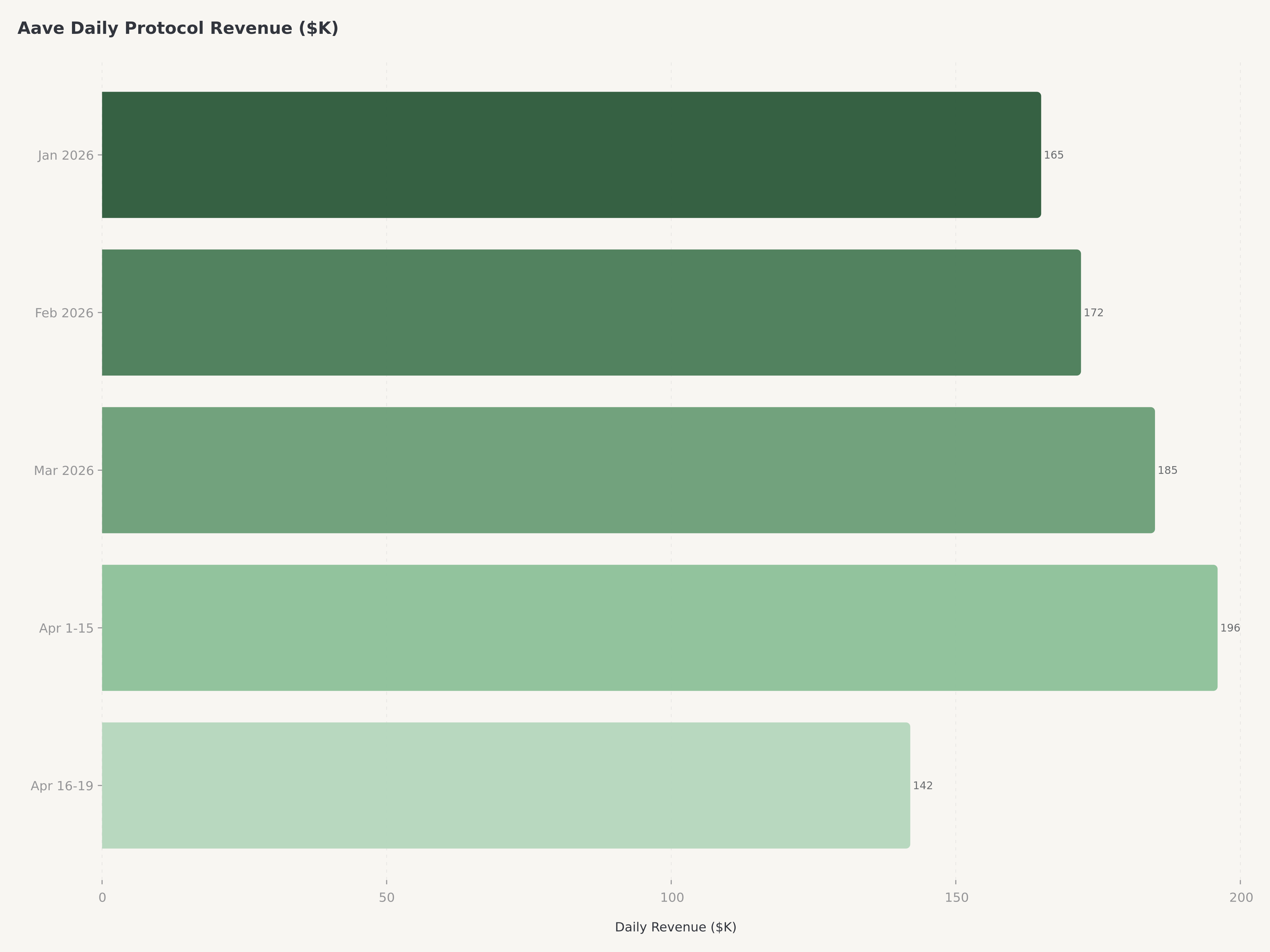

Before the Kelp exploit, Aave's on-chain fundamentals told the story of a protocol operating at industrial scale. Total value locked of $26.4 billion made Aave the single largest lending protocol in DeFi by a wide margin, with Morpho at approximately $6 billion and Compound at roughly $3 billion trailing far behind. Daily protocol fees averaged $1.5 million, translating to annualized revenue of approximately $548 million — a figure that places Aave alongside mid-cap SaaS companies in terms of revenue generation, albeit with radically different cost structures and no employees in the traditional sense.

Daily active users of approximately 9,716 may seem modest compared to consumer applications, but in DeFi lending, each user represents significant economic activity. The average transaction size on Aave dwarfs that of retail fintech platforms, and the protocol's utilization rates across major asset pools — ETH, USDC, USDT, DAI — consistently exceeded 80%, indicating robust demand for both borrowing and lending services.

Protocol revenue, defined as the spread between borrowing rates and lending rates after accounting for liquidation penalties, reached approximately $196,000 per day. This revenue accrues to the protocol treasury and, following the "Aave Will Win" governance vote, will increasingly flow to token holders through direct distribution mechanisms. The fee switch activation — long a point of contention between token holders who wanted dividends and developers who argued for treasury reinvestment — represents a maturation milestone comparable to a growth company initiating its first dividend.

Metric | Pre-Hack (Apr 16) | Post-Hack (Apr 20) | Change |

Total Value Locked | $26.4B | ~$20B | -$6.6B (-24%) |

Daily Fees | ~$1.5M | ~$1.1M (est.) | -27% (est.) |

Daily Protocol Revenue | ~$196K | ~$140K (est.) | -29% (est.) |

Daily Active Users | ~9,716 | ~8,500 (est.) | -13% (est.) |

AAVE Token Price | $115.20 | ~$113 | -2% (recovering) |

The post-hack TVL decline of $6.6 billion was painful but not catastrophic. Historical precedent suggests that DeFi TVL recovers within 4-8 weeks following exploit-driven outflows, provided the core protocol was not compromised. Aave's situation — where the protocol itself was not breached — is analogous to a traditional bank experiencing losses from a fraudulent asset that passed through its systems, rather than a bank whose vault was broken into. The distinction matters enormously for recovery dynamics.

Security Crisis and Governance Transformation: The Kelp Hack and What Follows

The April 19 Kelp DAO exploit was the most consequential security event in Aave's history, and understanding its implications requires examining three distinct dimensions: the technical attack vector, the protocol's response mechanism, and the governance context in which the crisis occurred.

The technical sequence was straightforward in concept if complex in execution. Attackers identified a vulnerability in Kelp's cross-chain bridge contract — the infrastructure that allows rsETH to be minted on chains other than Ethereum mainnet. By exploiting this vulnerability, they minted 116,500 rsETH without the corresponding staked ETH backing. This fraudulently minted rsETH was then deposited as collateral on Aave V3, where it was treated as legitimate by Aave's oracle and risk systems because the rsETH token contract itself was valid. The attackers borrowed wETH against this collateral, extracted the wETH, and disappeared. When the exploit was detected and rsETH's price collapsed to reflect the undercollateralization, Aave was left holding approximately $196 million in bad debt — loans backed by collateral that was now worth a fraction of its face value.

Aave's response was rapid by DeFi governance standards. The protocol's Umbrella safety module — a pool of staked AAVE tokens that serves as a backstop for exactly this type of event — was activated. The rsETH reserve was frozen, preventing further deposits or borrows. Borrowing power for rsETH was set to zero, and the loan-to-value ratio was reduced to zero, preventing any new positions from being opened. Stani Kulechov took to social media within hours, stating unequivocally that "the exploit was external; Aave contracts were not compromised." This framing — accurate but incomplete — became the central narrative around which the protocol's recovery would be organized.

The critical question now is whether Aave's Umbrella reserve is sufficient to absorb the $196 million in bad debt. If it is not, the shortfall could be socialized to stkAAVE holders — stakers who locked their AAVE tokens in the safety module in exchange for yield, accepting the tail risk that their staked tokens could be slashed to cover protocol losses. This mechanism has been a theoretical feature of Aave's risk architecture since inception but has never been tested at this scale. If stkAAVE slashing occurs, it will represent a defining moment for DeFi risk management: proof that decentralized insurance mechanisms can function as designed, or evidence that they cannot withstand real-world stress events.

The governance context amplifies both the crisis and the opportunity. The departure of BGD Labs, Aave's core development team, on April 1 had already triggered centralization concerns within the community. BGD Labs' exit, combined with the earlier departure of Chaos Labs (the protocol's risk manager), left Aave temporarily without two of its most critical service providers. A $200,000 security retainer proposal — covering just two months of emergency security services — highlighted the fragility of a decentralized protocol's ability to maintain operational continuity when key contributors leave.

Yet the "Aave Will Win" governance framework, passed on April 13 with over 75% approval just days before the Kelp hack, represents a constructive response to these centralization concerns. By directing 100% of Aave Labs revenue to the DAO treasury and implementing a fee switch for direct revenue distribution, the framework creates economic incentives for new service providers and developers to fill the gaps left by BGD Labs and Chaos Labs. The framework also resolves the months-long internal debate over who controls protocol revenue — the DAO or the Labs entity — in favor of the DAO, establishing a governance precedent that strengthens decentralization even as operational continuity challenges persist.

Valuation: Token Economics and Scenario Analysis

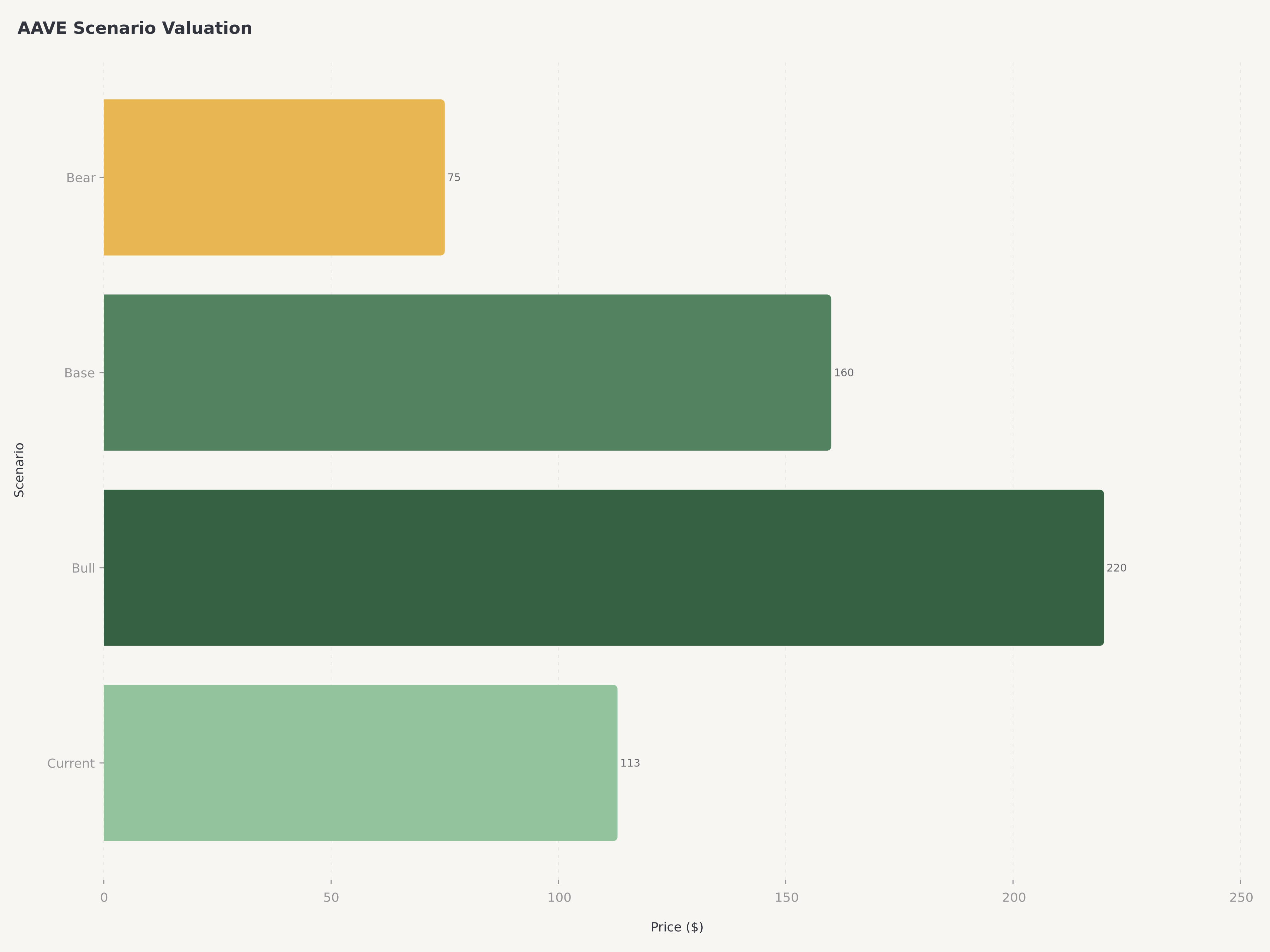

Valuing a DeFi governance token requires a fundamentally different framework than valuing equities. AAVE derives its value from three sources: governance rights over a $26 billion+ lending protocol, economic claims on protocol revenue through the fee switch, and the Umbrella safety module's insurance premium. With approximately 16 million tokens in circulation, a market cap of ~$1.75 billion, and a fully diluted valuation of ~$1.84 billion, AAVE trades at a modest premium to circulating supply, reflecting net-zero token inflation — a rarity in a sector plagued by aggressive unlock schedules.

Our scenario analysis models three outcomes over a 12-month horizon, with probabilities summing to 100%.

Scenario | Probability | AAVE Price | TVL | Key Assumptions |

Bull | 30% | $220 | $35B | V4 mainnet success, Umbrella covers bad debt fully, fee switch drives 4%+ staking yield, BTC collateral adds $5B+ TVL |

Base | 50% | $160 | $28B | TVL recovers to pre-hack levels within 8 weeks, V4 launches on schedule, governance stabilizes with new service providers, fee switch yields 2-3% |

Bear | 20% | $75 | $15B | stkAAVE slashing exceeds expectations, V4 delayed, regulatory action against DeFi lending, Morpho captures significant market share |

The probability-weighted expected value is $161 (0.30 x $220 + 0.50 x $160 + 0.20 x $75), which rounds to our $160 price target after applying a modest discount for execution risk during the post-hack governance transition and the Aave App consumer launch timeline uncertainty. At the current price of approximately $113, this represents roughly 42% upside.

The comparison to Morpho is instructive. Morpho, which has grown its TVL to over $6 billion through a capital-efficient peer-to-peer matching layer built originally on top of Aave and Compound, represents the most credible competitive threat. However, Morpho's approach — optimizing individual loan matching rather than pooled liquidity — serves a different market segment. Aave's pooled model offers instant liquidity and broader asset support, while Morpho's model offers better rates for patient, large-ticket borrowers. The two protocols are more complementary than competitive in practice, though Morpho's growth trajectory warrants monitoring.

On a protocol revenue multiple basis, AAVE's ~$1.75 billion market cap against annualized revenue of ~$548 million yields a price-to-revenue ratio of approximately 3.2x. For comparison, Compound trades at roughly 8x revenue with a fraction of Aave's TVL and feature set, while Morpho's implied valuation on secondary markets suggests multiples exceeding 15x. By this measure, AAVE is arguably the cheapest major DeFi protocol relative to its revenue-generating capacity.

Risks

Smart Contract and Cross-Chain Bridge Risk. The Kelp hack demonstrated that Aave's risk exposure extends beyond its own smart contracts to the entire ecosystem of assets it accepts as collateral. While Aave's core contracts have been audited extensively and have processed hundreds of billions of dollars in cumulative volume without a direct exploit, the composability that makes DeFi powerful also makes it fragile. Any asset listed on Aave — whether it is a liquid staking derivative, a wrapped token, or a restaking product — introduces the risk profile of the issuing protocol into Aave's system. The move to reduce LTV for rsETH to zero was reactive, not preventive. Until Aave V4's modular risk management framework is deployed, the protocol remains vulnerable to the same category of cross-protocol contagion that the Kelp exploit demonstrated. The $196 million in bad debt is not merely a balance sheet problem; it is a trust problem that could slow institutional adoption of DeFi lending.

Governance Centralization and Operational Continuity. The departures of BGD Labs and Chaos Labs within the same quarter exposed a structural fragility in Aave's governance model. A protocol with $26 billion in TVL was temporarily without its core development team and its primary risk manager — a situation that would be inconceivable at a traditional financial institution of comparable size. While the "Aave Will Win" framework creates economic incentives for new service providers to emerge, the transition period carries execution risk. Protocol upgrades could be delayed, security responses could be slower, and the quality of risk parameter management could degrade during the handover. The $200,000 security retainer proposal for just two months of coverage highlights how thin the operational safety net has become. AAVE token holders are effectively betting that decentralized governance can replace centralized organizational competence — a bet that has not been fully validated at this scale.

Regulatory and Macroeconomic Headwinds. DeFi lending protocols operate in a regulatory gray zone that is rapidly narrowing. The SEC's approach to decentralized protocols, the EU's MiCA framework, and emerging Asian regulatory regimes all have the potential to impose compliance requirements — KYC/AML obligations, licensing mandates, reserve requirements — that could fundamentally alter how Aave operates. A protocol that serves borrowers and lenders pseudonymously across 190 countries sits uncomfortably within any single regulatory jurisdiction, and a coordinated enforcement action could fragment liquidity and reduce TVL materially. On the macroeconomic front, DeFi lending demand is correlated with crypto market conditions: a sustained bear market in ETH and BTC would reduce collateral values, borrowing demand, and protocol revenue simultaneously.

Conclusion

The Kelp DAO exploit was a stress test that Aave did not choose but must now pass. The $196 million in bad debt is significant — there is no sugarcoating a loss of that magnitude — but the critical distinction is that Aave's own contracts were not compromised. The protocol's lending logic, liquidation engine, and oracle infrastructure performed as designed. The failure was in an external bridge protocol whose token Aave accepted as collateral, a risk management decision that will be revisited in the V4 architecture. For investors willing to underwrite the 4-8 week recovery period while TVL normalizes and governance addresses the bad debt through the Umbrella mechanism, the current price of approximately $113 represents an attractive entry point into the largest and most revenue-generative lending protocol in decentralized finance.

The "Aave Will Win" governance vote, the fee switch activation, the Babylon BTC collateral integration, and the V4 mainnet launch collectively represent a catalyst-rich roadmap for the next 12 months. Aave is not the same protocol it was in 2021 — it is more mature, more battle-tested, and now, more accountable to its token holders through direct revenue sharing. We rate AAVE Buy with a $160 price target. For readers interested in parallel narratives, our analysis of Netflix's platform transformation illustrates how a dominant platform monetizes its infrastructure advantage, and our coverage of Intel's foundry turnaround explores how legacy technology enterprises reinvent themselves under governance pressure — dynamics that echo Aave's own evolution from lending protocol to DeFi operating system.

Is AAVE a buy after the Kelp DAO hack?

We rate AAVE Buy with a $160 price target, representing approximately 42% upside from the current price of ~$113. The Kelp DAO exploit on April 19 resulted in $196 million in bad debt on Aave V3, but Aave's own smart contracts were not compromised. The attack exploited Kelp's cross-chain bridge, not Aave's lending logic. The protocol responded by freezing the rsETH reserve, removing borrowing power, and reducing LTV to zero. While the bad debt must be absorbed — potentially through the Umbrella safety module and stkAAVE slashing — the protocol's fundamental revenue generation ($1.5 million daily fees), governance improvements (fee switch activation), and upcoming V4 mainnet launch support a recovery thesis. Historical precedent suggests DeFi TVL recovers within 4-8 weeks after exploit-driven outflows when the core protocol was not breached.

How much bad debt does Aave have from the Kelp exploit?

Approximately $196 million in bad debt was created on Aave V3 as a result of the Kelp DAO bridge exploit. Attackers stole 116,500 rsETH (~$292 million) through a vulnerability in Kelp's cross-chain bridge, deposited the fraudulently minted rsETH as collateral on Aave, and borrowed wETH against it. When the exploit was detected and rsETH's value collapsed, the loans became undercollateralized. Aave's Umbrella safety module — a pool of staked AAVE tokens designed to backstop such events — is the primary mechanism for absorbing this loss. If the Umbrella reserve is insufficient, stkAAVE holders may face slashing of their staked tokens, a mechanism that has been part of Aave's risk architecture since inception but has never been tested at this scale.

What is the "Aave Will Win" governance vote?

The "Aave Will Win" framework is a governance proposal that passed on April 13, 2026, with over 75% approval. It directs 100% of Aave Labs revenue to the DAO treasury and implements a fee switch for direct protocol revenue distribution to token holders. This resolved months of internal debate over who controls protocol revenue — the Aave Labs entity or the decentralized DAO. The framework effectively functions as a structural dividend for AAVE token holders, making the token a direct claim on protocol cash flows rather than merely a governance right. It was passed in the context of BGD Labs' departure (Aave's core development team) and Chaos Labs' exit (risk manager), both of which heightened community concerns about centralization and accountability.

How does Aave compare to Morpho and Compound?

Aave is the largest DeFi lending protocol with ~$20 billion in current TVL (post-hack; $26.4 billion pre-hack), compared to Morpho at approximately $6 billion and Compound at roughly $3 billion. Aave generates approximately $1.5 million in daily fees versus significantly lower figures for both competitors. Morpho represents the most credible competitive threat, having grown rapidly through a capital-efficient peer-to-peer matching layer, but it serves a different market segment — optimizing rates for large, patient borrowers rather than providing instant pooled liquidity. Compound, once the dominant lending protocol, has fallen behind in multi-chain deployment and feature innovation. On a price-to-revenue basis, AAVE trades at approximately 3.2x annualized revenue, compared to roughly 8x for Compound, making it arguably the cheapest major DeFi protocol relative to its revenue generation.

What catalysts could drive AAVE higher in 2026?

Four primary catalysts support upside beyond our $160 base-case target. First, the Aave V4 mainnet launch — described as a "DeFi operating system" with unified liquidity, modular risk management, and native cross-chain functionality — could expand Aave's addressable market and eliminate the cross-chain bridge dependencies that enabled the Kelp exploit. Second, the Babylon Native BTC collateral integration allows Bitcoin holders to use BTC as collateral without wrapping, tapping into Bitcoin's $1.3 trillion market cap. Third, the Aave App consumer launch targeting 10 million users and embedded finance expansion into Latin America could drive user growth beyond the current ~9,700 daily active users. Fourth, the fee switch activation under the "Aave Will Win" framework creates a direct yield mechanism for token holders that could attract institutional capital seeking DeFi exposure with cash-flow backing.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a solicitation, or a recommendation to buy or sell any securities or digital assets. The analysis reflects the author's opinion based on publicly available information, on-chain data, and proprietary Edgen research as of the publication date. Digital asset investments carry substantial risk, including the potential loss of all invested capital. DeFi protocols are subject to smart contract risk, governance risk, regulatory risk, and market risk. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions. Edgen and its analysts may hold positions in digital assets discussed. Price targets and ratings reflect 12-month forward expectations and are subject to revision.

Recommend